- Transportation & Logistics

- Third Party Logistics Market

Third Party Logistics Market Size, Share, and Growth Forecast 2026 – 2033

Third Party Logistics Market by Service Type (Dedicated Contract Carriage, Freight Forwarding, Warehousing & Distribution, Value-added Logistics Services, Reverse Logistics, Cold Chain Logistics), Transport Mode (Roadways, Railways, Waterways, Airways, Intermodal Transport, Others), End-use Industry (Manufacturing, Retail & E-commerce, Healthcare & Pharmaceuticals, Automotive, Consumer Goods, Food & Beverage, Others), Deployment Type (Domestic Transportation Management, International Transportation Management, Integrated Logistics Services, Managed Transportation Services, Supply Chain Consulting, Digital Logistics Solutions), and Regional Analysis for 2026–2033

Third Party Logistics Market Size and Trend Analysis

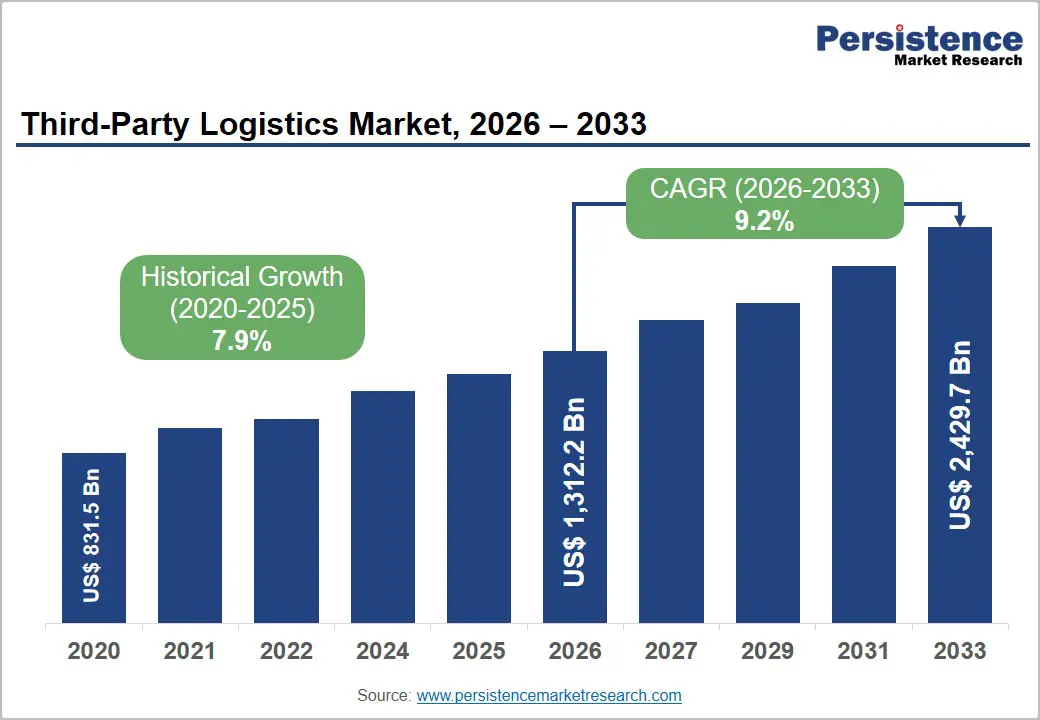

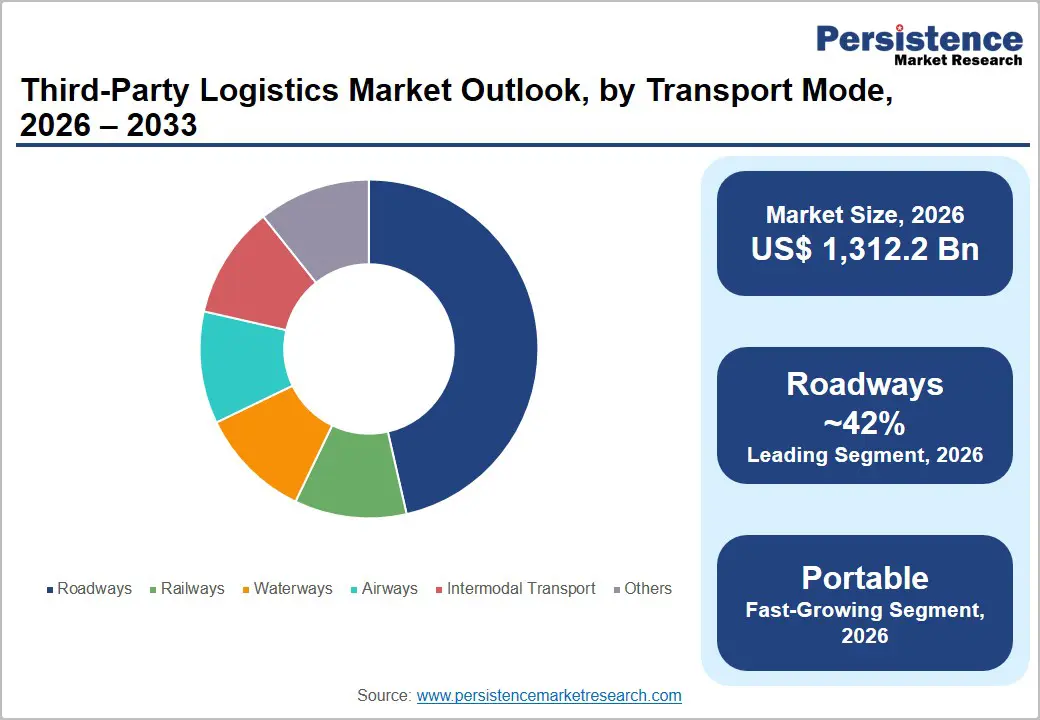

The global third party logistics (3PL) market size is valued at US$ 1,312.2 Bn in 2026 and is projected to reach US$ 2,429.7 Bn by 2033, growing at a CAGR of 9.2% between 2026 and 2033.

This robust growth trajectory is primarily driven by the accelerating expansion of global e-commerce, increasing outsourcing of non-core logistics functions by manufacturers and retailers, and the rapid digitalization of supply chain operations. According to the World Trade Organization (WTO), global merchandise trade volume grew by approximately 2.7% in 2023 and is expected to sustain upward momentum, directly amplifying freight volumes handled by 3PL providers.

Additionally, the post-pandemic reconfiguration of supply chains marked by nearshoring, multi-modal sourcing, and just-in-case inventory models has compelled enterprises across sectors to leverage specialized 3PL capabilities for resilience and cost efficiency.

Key Market Highlights

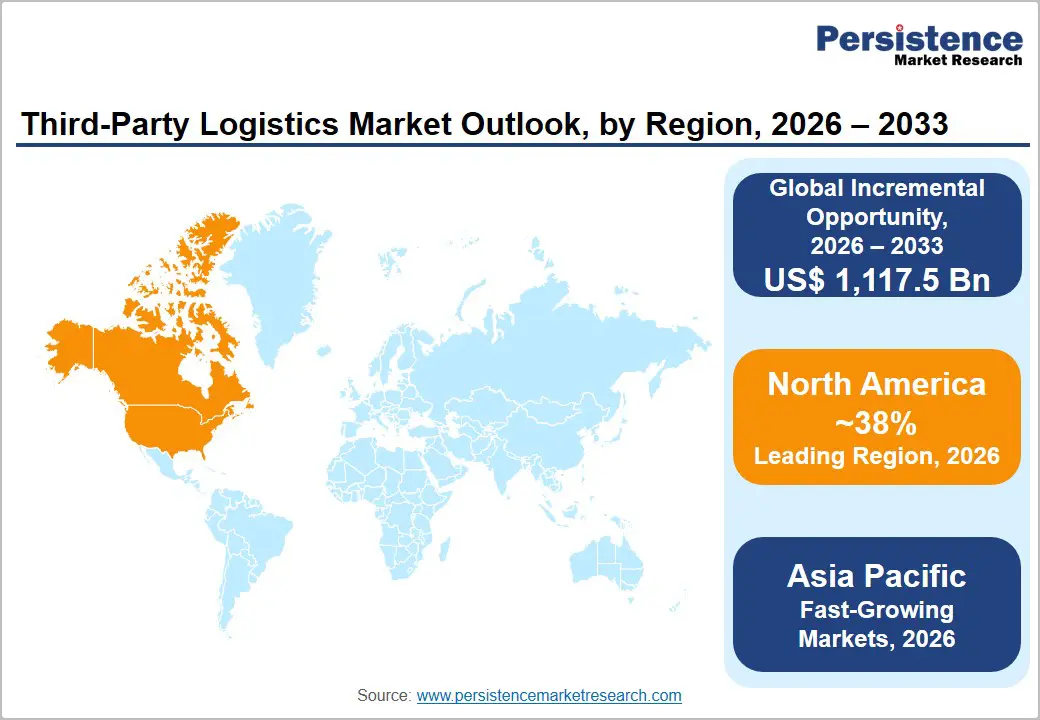

- Leading Region – North America: North America dominates the global 3PL market with approximately 38% revenue share, underpinned by high e-commerce penetration, advanced logistics infrastructure, and strong outsourcing culture across manufacturing, retail, and healthcare sectors.

- Fastest Growing Region – Asia Pacific: Asia Pacific is the fastest growing regional market, driven by China's logistics modernization, India's infrastructure push under PM Gati Shakti, and ASEAN e-commerce expansion, collectively delivering above-average CAGR through 2033.

- Dominant Segment – Warehousing & Distribution: Warehousing & Distribution commands ~29% market share in the Service Type category, driven by omnichannel retail fulfillment needs, e-commerce order volume growth, and value-added service integration within outsourced warehousing contracts.

- Fastest Growing Segment – Digital Logistics Solutions: Digital Logistics Solutions is projected to expand at ~14.2% CAGR through 2033, driven by AI-powered TMS platforms, real-time visibility tools, and blockchain-enabled traceability adoption across enterprise supply chains.

- Key Market Opportunity – Cold Chain Logistics: Cold chain logistics expansion driven by biopharmaceutical distribution, mRNA vaccine logistics, and growing perishable food trade across Asia Pacific and Africa presents high-value, high-margin outsourcing opportunities for specialized 3PL providers.

Market Dynamics

Market Growth Drivers

Surge in Global E-commerce Fueling Outsourced Logistics Demand

The exponential rise in e-commerce is one of the most consequential demand drivers for the 3PL market. According to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales surpassed US$ 27 trillion in recent years, with business-to-consumer (B2C) channels expanding rapidly across emerging economies. This growth creates immense pressure on shippers to manage complex last-mile delivery, returns processing, and inventory replenishment at scale functions increasingly delegated to specialized 3PL providers.

In the United States, the U.S. Census Bureau reported that e-commerce accounted for over 15.6% of total retail sales in 2023, up from 11.0% in 2019. Retailers, particularly in the consumer goods and food & beverage segments, are integrating multi-channel fulfillment architectures that depend on robust 3PL networks to achieve speed, cost efficiency, and customer satisfaction across geographically dispersed markets.

Manufacturing Globalization and Supply Chain Complexity Driving 3PL Adoption

The deepening integration of global manufacturing ecosystems has substantially elevated demand for third-party logistics solutions. As companies diversify sourcing across regions particularly across Asia Pacific, Eastern Europe, and Latin America managing multi-tier supplier networks has become operationally complex. According to a Deloitte survey, over 79% of companies with high-performing supply chains reported that their logistics was handled partially or entirely by external partners.

The trend toward lean manufacturing and just-in-time (JIT) inventory widely adopted across the automotive and electronics manufacturing sectors necessitates precise, time-sensitive logistics coordination that third-party specialists are uniquely positioned to deliver. Furthermore, regulatory compliance demands around customs, tariffs, and import/export documentation have reinforced the reliance on experienced freight forwarding and international transportation management services offered by established 3PL operators.

Market Restraints

High Capital Investment and Technology Integration Costs

Despite the favorable demand environment, the 3PL industry faces significant cost-related headwinds. Establishing and maintaining large-scale warehousing infrastructure, transportation fleets, and advanced technology platforms requires substantial capital outlay. According to the International Monetary Fund (IMF), rising interest rates in the 2022–2023 period increased financing costs for logistics infrastructure globally, constraining expansion plans for mid-tier 3PL providers.

Additionally, integrating enterprise resource planning (ERP), transportation management systems (TMS), and warehouse management systems (WMS) across heterogeneous client IT architectures remains costly and time-consuming, with implementation cycles often exceeding 12–18 months. These barriers disproportionately affect small and medium-sized 3PL operators, limiting competitive scalability.

Workforce Shortages and Rising Labor Costs in Logistics Operations

Labor availability and cost escalation represent persistent structural restraints for the 3PL sector. The American Trucking Associations (ATA) estimated a truck driver shortage of approximately 60,000 drivers in the U.S. alone, with the gap projected to widen significantly by 2030. Similarly, warehouse staffing challenges are documented across Europe and Asia Pacific, where demographic shifts and post-pandemic labor market realignments have elevated wage expectations.

Higher labor costs erode operating margins for 3PL providers, limiting their ability to offer competitive pricing without operational innovation such as automation and robotics adoption investments that themselves demand significant upfront expenditure.

Market Opportunities

Digital Logistics and AI-Driven Supply Chain Optimization

The accelerating deployment of artificial intelligence, machine learning, and Internet of Things (IoT) technologies across logistics operations presents a transformative opportunity for 3PL providers to enhance value propositions and capture premium service contracts. According to the World Economic Forum (WEF), digital supply chain transformation could unlock up to US$ 1.5 trillion in value globally by 2025. Platforms offering real-time shipment visibility, predictive demand forecasting, and autonomous route optimization are increasingly differentiating 3PL providers in competitive tendering processes.

The emergence of digital logistics solutions as a formal deployment category encompassing blockchain-based traceability, AI-powered warehouse management, and cloud-native TMS platforms signals a structural shift in how enterprises procure and evaluate 3PL partnerships. Market participants investing in proprietary digital ecosystems are well-positioned to secure long-term, high-value contracts across healthcare & pharmaceuticals, retail, and automotive end-use verticals.

Cold Chain Logistics Expansion Driven by Biopharmaceuticals and Perishable Food Trade

The global expansion of cold chain logistics infrastructure represents one of the most significant near-term growth opportunities for 3PL providers. The World Health Organization (WHO) estimates that approximately 50% of vaccines worldwide are wasted annually due to inadequate cold chain management, underscoring the critical need for reliable temperature-controlled logistics. The biopharmaceutical boom driven by mRNA vaccine production, biologics distribution, and specialty drug therapies is compelling pharmaceutical companies to outsource cold chain operations to certified 3PL specialists.

Simultaneously, the global trade of perishable food products, including fresh produce, seafood, and dairy, is expanding rapidly, supported by improved cold chain infrastructure investments across Southeast Asia, Africa, and Latin America. According to the International Institute of Refrigeration (IIR), the global refrigerated warehouse capacity is growing at over 3.5% annually, creating sustained demand for 3PL-managed cold storage and distribution networks.

Category-wise Insights

Service Type Analysis

Warehousing & Distribution is the dominant segment within the Service Type category, commanding approximately 29% of the global 3PL market share in 2025. This leadership position is underpinned by the proliferation of omnichannel retail models that demand sophisticated inventory management, order fulfillment, and last-mile distribution capabilities. The expansion of fulfillment center networks by leading e-commerce platforms across North America, Europe, and Asia Pacific has substantially elevated outsourced warehousing demand.

According to the Warehousing Education and Research Council (WERC), over 85% of distribution centers in the U.S. report using at least one outsourced warehousing service. Additionally, value-added logistics services (VALs) including kitting, labeling, packaging, and quality inspection embedded within warehousing contracts are deepening revenue per client, further reinforcing the segment's dominant position. The segment's extensive infrastructure requirements and long-term contractual nature create durable barriers to entry, insulating incumbent 3PL operators from competitive displacement.

Cold Chain Logistics is the fastest growing segment within the Service Type category, projected to expand at a CAGR of approximately 11.8% between 2026 and 2033, surpassing the overall market growth rate. This acceleration is driven by surging biopharmaceutical distribution needs, expanding processed food trade, and increasingly stringent food safety regulations globally. Investments in temperature-controlled warehousing and refrigerated transportation across Asia Pacific and Middle East markets are further amplifying segment growth.

Transport Mode Analysis

Roadways transport is the leading segment by Transport Mode, accounting for approximately 42% of the total third party logistics market share in 2025. Road freight remains the backbone of domestic distribution networks globally due to its flexibility, door-to-door connectivity, and cost competitiveness for short-to-medium distance hauls. According to the International Road Transport Union (IRU), road freight accounted for over 75% of total inland freight volumes across Europe and North America.

The expansion of highway infrastructure under government investment programs including the U.S. Infrastructure Investment and Jobs Act (IIJA) which allocated over US$ 110 Bn for roads and bridges is enhancing connectivity and supporting 3PL road networks. The integration of GPS tracking, electronic logging devices (ELD), and fleet telematics across trucking fleets has further improved service reliability and compliance, making road-based 3PL services increasingly attractive for time-sensitive manufacturing and retail shipments.

Airways transport is the fastest growing Transport Mode segment, projected to register a CAGR of approximately 12.4% during the 2026–2033 forecast period. This growth is driven by the surge in cross-border e-commerce, demand for expedited pharmaceutical shipments, and the expansion of dedicated cargo airline capacities globally. High-value electronics, luxury goods, and perishable products increasingly rely on air freight 3PL solutions for time-definite delivery, supporting premium segment growth.

End-use Industry Analysis

The Retail & E-commerce segment dominates the End-use Industry category, holding an estimated 31% share of the global 3PL market in 2025. The transformation of consumer purchasing behavior accelerated by the COVID-19 pandemic and sustained by expanding digital payment infrastructure has created unprecedented demand for agile, scalable logistics solutions. According to Statista, global retail e-commerce sales reached approximately US$ 5.8 trillion in 2023 and are projected to exceed US$ 8 trillion by 2027.

Retailers require 3PL partners capable of managing multi-node fulfillment networks, same-day and next-day delivery services, and efficient reverse logistics for product returns. The rise of marketplace platforms and direct-to-consumer (DTC) brands has further diversified the 3PL client base within this segment, compelling providers to develop scalable, technology-integrated fulfillment ecosystems capable of supporting rapid inventory turnover across SKU-intensive product catalogues.

Healthcare & Pharmaceuticals is the fastest growing End-use Industry segment, expected to achieve a CAGR of approximately 11.5% during 2026–2033. Stringent regulatory requirements under frameworks such as EU GDP (Good Distribution Practice) guidelines and U.S. FDA 21 CFR Part 211 compel pharmaceutical companies to utilize compliant 3PL providers with validated cold chain and serialization capabilities. The post-pandemic buildup in vaccine distribution and specialty biologics logistics continues to drive robust outsourcing activity in this segment.

Deployment Type Analysis

Integrated Logistics Services constitute the leading Deployment Type segment, capturing approximately 27% of market share in 2025. This segment encompasses the holistic outsourcing of transportation, warehousing, distribution, and value-added services to a single 3PL provider under a unified contract framework. Enterprises across the manufacturing and automotive sectors increasingly prefer integrated logistics models for their capacity to streamline vendor management, reduce inter-functional coordination costs, and deliver unified performance reporting.

A Capgemini Research Institute study found that companies using integrated 3PL services achieved average logistics cost reductions of 11–15% compared to fragmented multi-vendor approaches. The growing preference for supply chain visibility platforms that consolidate real-time data across transportation and warehousing legs is further cementing integrated logistics as the preferred deployment model for multinational shippers seeking end-to-end operational transparency and risk management capabilities.

Digital Logistics Solutions is the fastest growing Deployment Type segment, anticipated to expand at a CAGR of approximately 14.2% from 2026 to 2033. Cloud-native TMS platforms, AI-driven demand sensing tools, and blockchain-enabled supply chain traceability solutions are redefining how shippers interact with and evaluate their 3PL partners. The proliferation of API-first logistics platforms and digital freight brokerage models is fundamentally reshaping the market's competitive architecture.

Regional Insights

North America Third Party Logistics Trends

North America represents the largest regional market for third party logistics, accounting for approximately 38% of global revenue in 2025. The region's logistics ecosystem is distinguished by its advanced infrastructure, high e-commerce penetration, and regulatory environment conducive to outsourcing. The U.S. Bureau of Transportation Statistics (BTS) reports that freight movements in the U.S. are expected to grow by over 50% in tonnage by 2040, creating structural long-term demand for 3PL services. Cross-border trade facilitated by the United States–Mexico–Canada Agreement (USMCA) has further expanded regional freight volumes, benefiting intermodal and customs brokerage-focused 3PL operators.

Major 3PL hubs including Chicago, Dallas, and Los Angeles continue to attract logistics infrastructure investment. The adoption of automation technologies including autonomous mobile robots (AMRs) and AI-driven warehouse management platforms is accelerating across North American fulfillment centers, improving throughput and labor efficiency. Canadian cold chain infrastructure expansion is also supporting 3PL growth, particularly in food & beverage distribution.

- U.S.: E-commerce Backbone Driving North American 3PL Growth Leadership

The United States commands approximately 82% of the North American 3PL market, reflecting its position as the world's largest individual logistics economy. The U.S. market is projected to grow at a CAGR of approximately 8.9% during 2026–2033, supported by sustained e-commerce expansion, defense logistics outsourcing, and healthcare supply chain investments. The U.S. logistics industry constitutes approximately 8% of GDP according to the Council of Supply Chain Management Professionals (CSCMP). Federal infrastructure investments, expanding intermodal rail networks, and growing pharmaceutical distribution requirements position the U.S. as the global benchmark for 3PL operational sophistication and technology adoption. Key verticals including automotive, retail, and defense logistics continue to drive outsourcing activity across domestic and cross-border supply chains.

Europe Third Party Logistics Trends

Europe is the second-largest regional market for 3PL services, characterized by a densely integrated transportation network, stringent regulatory standards, and a mature outsourcing culture. The European Commission's Trans-European Transport Network (TEN-T) program, which targets the completion of a multimodal core network by 2030, is actively expanding cross-border freight capacity across EU member states. This infrastructure momentum is translating directly into volume growth for 3PL operators managing pan-European distribution mandates.

Sustainability is a defining strategic theme across European logistics, with the EU Green Deal and Fit for 55 package compelling shippers and 3PL providers to accelerate decarbonization. The adoption of electric and hydrogen-powered commercial vehicles, combined with carbon accounting requirements for logistics contracts, is reshaping competitive differentiation strategies. Germany, Netherlands, and France collectively anchor European 3PL capacity, hosting the region's largest warehousing and intermodal logistics hubs.

- Germany: Central European Logistics Hub Powering Industrial Supply Chains

Germany holds approximately 22% of the European 3PL market share, underscoring its position as the continent's logistics epicenter. The country's central geographic location, world-class road and rail infrastructure, and the strength of its automotive and manufacturing industries which collectively generate substantial inbound and outbound freight volumes drive sustained 3PL demand. Germany's 3PL market is projected to grow at a CAGR of approximately 8.4% during 2026–2033. The German Logistics Association (BVL) identifies digitalization and multi-modal integration as the two most critical competitive priorities for German 3PL providers. The country's Rhine-Ruhr, Hamburg, and Frankfurt logistics corridors host extensive industrial warehousing and distribution networks serving both domestic and pan-European supply chains.

- U.K.: Post-Brexit Trade Adaptation Reshaping Logistics Outsourcing Patterns

The United Kingdom accounts for approximately 15% of the European 3PL market, with a projected CAGR of 8.1% through 2033. Post-Brexit trade reconfiguration has restructured customs brokerage and cross-border freight management requirements, creating incremental demand for specialized 3PL operators with cross-border compliance expertise. The growth of U.K. e-commerce with online retail penetration exceeding 30% of total retail sales continues to drive investment in urban fulfillment centers and last-mile delivery networks. The U.K. Logistics Confidence Index, published by the Chartered Institute of Logistics and Transport (CILT), indicates sustained outsourcing momentum across retail, healthcare, and cold chain segments.

- France: Sustainable Logistics Leadership Anchoring Strategic 3PL Investments

France holds approximately 12% of the European third party logistics market share, with growth projected at a CAGR of approximately 8.6% between 2026 and 2033. The French government's National Low Carbon Strategy (SNBC) and investments in electric freight vehicles are positioning French 3PL operators as early movers in sustainable logistics. Major logistics clusters around Paris, Lyon, and Marseille support high-capacity warehousing and multimodal freight services. The robust French automotive and luxury goods sectors generate consistent 3PL demand, particularly for time-sensitive and high-value goods distribution.

- Italy: Mediterranean Gateway Driving Intermodal and Cold Chain 3PL Services

Italy accounts for approximately 9% of the European 3PL market, with an estimated CAGR of 8.0% over the 2026–2033 period. Italy's position as a key Mediterranean trade gateway anchored by the ports of Genoa, Trieste, and Gioia Tauro generates robust freight handling and intermodal logistics demand. The country's significant agri-food export trade, including olive oil, wine, and perishables, underpins consistent cold chain 3PL activity. Government investments in southern Italian logistics infrastructure as part of the National Recovery and Resilience Plan (PNRR) are expected to attract new 3PL investment and enhance capacity across underserved domestic corridors.

Asia Pacific Third Party Logistics Trends

Asia Pacific is the fastest growing regional market for third party logistics, driven by the convergence of manufacturing expansion, e-commerce acceleration, and infrastructure investment across China, India, Japan, and Southeast Asia. The region benefits from a deep manufacturing base accounting for over 40% of global goods production and rapidly growing middle-class consumer demand that is amplifying both B2C and B2B freight volumes. The Asian Development Bank (ADB) estimates that Asia will require over US$ 26 trillion in infrastructure investment through 2030, a significant portion of which encompasses logistics and transportation, creating a favorable operating environment for 3PL expansion.

Policy initiatives such as China's Belt and Road Initiative (BRI), India's PM Gati Shakti National Master Plan, and ASEAN's Master Plan on ASEAN Connectivity 2025 are reshaping regional logistics infrastructure and creating new freight corridors that 3PL operators are actively positioning to serve. The growing adoption of warehouse automation, digital freight platforms, and integrated cold chain solutions across China, South Korea, and India is additionally accelerating market maturation and elevating service quality benchmarks.

- China: Manufacturing Scale and E-commerce Dominance Fueling 3PL Supremacy

China is the dominant 3PL market within Asia Pacific, capturing approximately 48% of regional revenue in 2025, with a projected CAGR of approximately 10.2% through 2033. China's logistics ecosystem is being reshaped by the integration of advanced robotics, drone delivery, and AI-powered supply chain platforms, led by technology-first 3PL operators. According to China's National Development and Reform Commission (NDRC), logistics costs as a share of GDP declined from 18% in 2012 to 14.7% in 2022, reflecting ongoing efficiency improvements. The explosive growth of platforms like Taobao, JD.com, and Pinduoduo continues to drive parcel and warehousing outsourcing, while the BRI is extending Chinese 3PL operator networks across Central Asia and Europe.

- India: Infrastructure Modernization Unlocking High-Growth 3PL Opportunities

India represents one of the most dynamic growth frontiers for third party logistics, holding approximately 14% of Asia Pacific market share in 2025 and projected to grow at a CAGR of approximately 12.8% through 2033 among the highest nationally. The Government of India's PM Gati Shakti National Master Plan and the National Logistics Policy (NLP) 2022 explicitly target reducing logistics costs from ~14% of GDP to under 8% of GDP, directly incentivizing 3PL infrastructure investment. The rapid formalization of the Indian retail and manufacturing sectors following GST implementation has streamlined multi-state logistics, benefiting organized 3PL providers. Strong growth in pharmaceutical exports, automotive manufacturing, and e-commerce fulfillment across Tier-2 and Tier-3 cities is creating new demand pockets.

- South Korea: Advanced Technology Adoption Elevating 3PL Service Standards

South Korea accounts for approximately 8% of Asia Pacific's 3PL market share, with a projected CAGR of 9.6% for the 2026–2033 period. South Korea's logistics sector is distinguished by its high automation density, world-class port infrastructure (anchored by the Port of Busan, one of the world's top container ports), and strong domestic e-commerce activity. The country's advanced electronics, semiconductor, and automotive manufacturing industries generate complex, high-precision logistics requirements that favor specialized 3PL operators. The Korean government's National Logistics Masterplan and green logistics commitments are further supporting investment in smart logistics infrastructure and electric freight vehicles, reinforcing South Korea's position as a regional 3PL technology benchmark.

Competitive Landscape

Market Structure Analysis

The global third party logistics market exhibits a moderately consolidated structure at the top tier, with a small number of large multinational operators including DHL Supply Chain, XPO Logistics, C.H. Robinson, and Kuehne+Nagel commanding disproportionate market share through extensive global networks, proprietary technology platforms, and long-term contractual relationships with Fortune 500 clients. However, the mid and lower tiers remain highly fragmented, with thousands of regional and niche operators competing on specialized capabilities, geographic density, and pricing flexibility.

Strategic growth priorities across leading players include digital platform development, sustainability-aligned fleet electrification, acquisitive expansion into high-growth geographies, and the build-out of integrated cold chain and pharma-grade logistics networks. Partnerships with e-commerce platforms and technology integration with shippers' ERP and TMS systems are increasingly defining competitive differentiation.

Key Market Developments

- March 2025: DHL Supply Chain announced a €300 million investment in expanding its European automated warehousing network, deploying over 20,000 autonomous mobile robots (AMRs) across 15 major fulfillment centers to enhance throughput capacity and reduce operational costs.

- November 2024: XPO Logistics launched its proprietary AI-driven freight visibility platform, 'XPO Connect 2.0,' enabling real-time shipment tracking and predictive disruption alerts across its North American and European trucking networks, improving on-time delivery performance by an estimated 18%.

- January 2024: Kuehne+Nagel completed its acquisition of a leading Southeast Asian regional 3PL operator, expanding its ASEAN cold chain logistics footprint and gaining access to pharmaceutical distribution networks across Singapore, Malaysia, and Thailand.

Companies Covered in Third Party Logistics Market

- DHL Supply Chain

- Kuehne+Nagel

- DSV A/S

- DB Schenker

- C.H. Robinson

- Nippon Express

- XPO Logistics

- CEVA Logistics

- Sinotrans Limited

- GEODIS

- Expeditors International

- UPS Supply Chain Solutions

- FedEx Logistics

- Ryder System, Inc.

- Maersk Logistics

Frequently Asked Questions

The global Third Party Logistics (3PL) market is valued at US$ 1,312.2 Bn in 2026 and is expected to reach US$ 2,429.7 Bn by 2033, expanding at a CAGR of 9.2% during the forecast period of 2026–2033.

The primary growth drivers include the rapid expansion of global e-commerce and associated outsourced fulfillment demands, increasing manufacturing globalization requiring complex multi-modal freight management, post-pandemic supply chain reconfiguration favoring specialized logistics outsourcing, and accelerating adoption of digital logistics solutions and AI-driven supply chain optimization technologies by shippers worldwide.

Warehousing & Distribution is the dominant service type segment, capturing approximately 29% of global 3PL market share in 2025. The segment's leadership is driven by omnichannel fulfillment growth, e-commerce order volume expansion, and the integration of value-added logistics services within outsourced warehousing contracts across retail, consumer goods, and manufacturing sectors.

North America is the leading region, holding approximately 38% of the global 3PL market revenue in 2025. The region's leadership is underpinned by high e-commerce penetration, mature logistics outsourcing culture, advanced transportation infrastructure, and robust demand from the manufacturing, retail, and healthcare & pharmaceuticals sectors.

Cold chain logistics expansion represents the most compelling near-term opportunity. Driven by the global biopharmaceutical distribution boom including mRNA vaccines, biologics, and specialty drugs combined with growing international perishable food trade, demand for temperature-controlled 3PL capabilities is accelerating across Asia Pacific, Middle East, and Africa. Providers with certified cold chain infrastructure are positioned to command significant premium contracts across healthcare & pharmaceutical and food & beverage end markets.

The global 3PL market is served by leading multinationals including DHL Supply Chain, XPO Logistics, Kuehne+Nagel, C.H. Robinson, DB Schenker, Geodis, DSV A/S, and Maersk Logistics, among others. These players differentiate through global network scale, proprietary digital platforms, industry specialization, and sustainability-aligned logistics capabilities.