- Transportation & Logistics

- Robotaxi Market

Robotaxi Market Size, Share, and Growth Forecast 2026 - 2033

Robotaxi Market by Propulsion Type (Electric Vehicles, Hybrid Electric Vehicles, Fuel Cell Vehicles), Component (LiDAR, Radar), Vehicle Type (Cars, Shuttles/Vans), Application (Passengers, Goods), and Regional Analysis, 2026 - 2033

Robotaxi Market Size and Trends Analysis

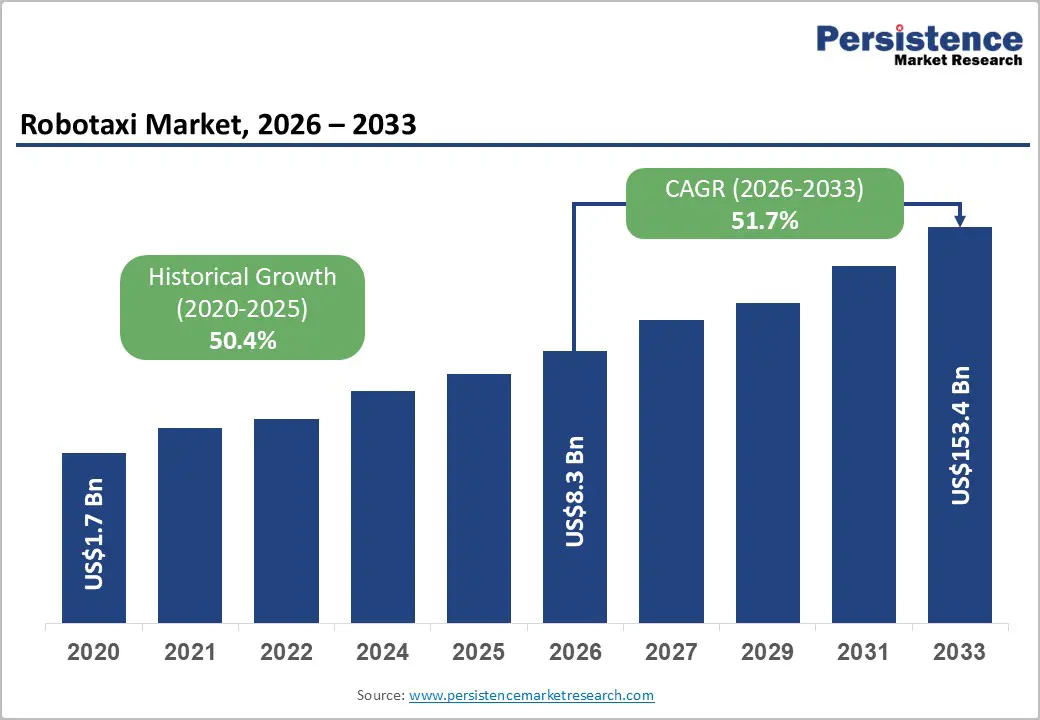

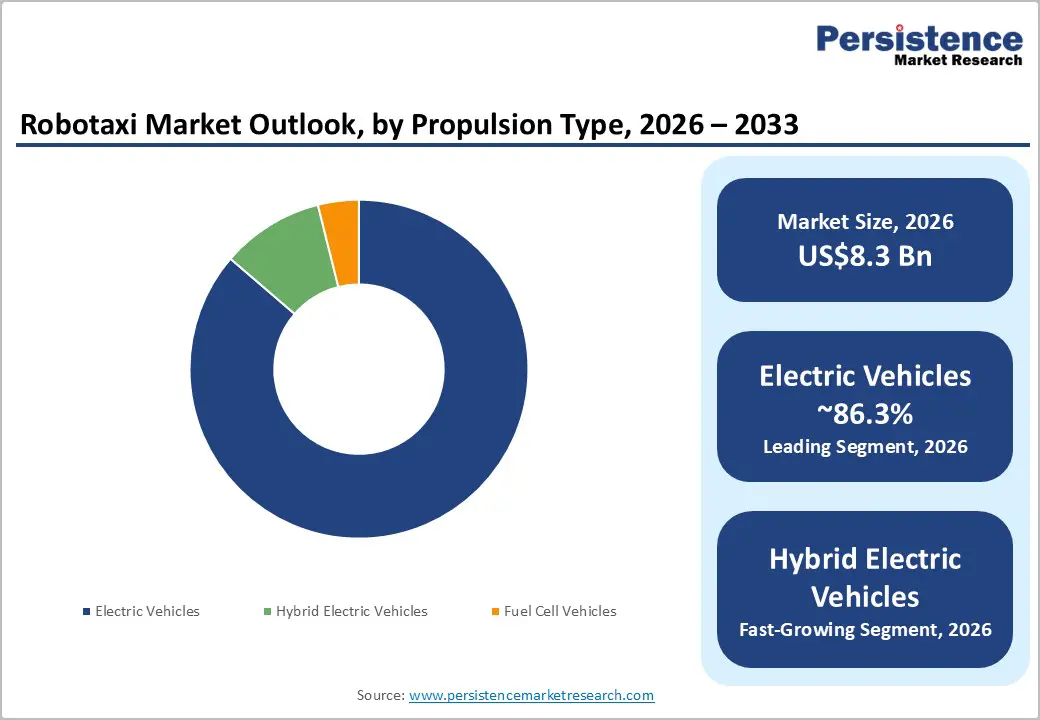

The global robotaxi market size is likely to be valued at US$8.3 billion in 2026 and is expected to reach US$153.4 billion by 2033, growing at a CAGR of 51.7% during the forecast period from 2026 to 2033, driven by developments in autonomous driving technologies, especially in AI-assisted perception systems, LiDAR cost optimization, and high-definition mapping, which are improving vehicle safety and navigation accuracy in complex urban environments.

Key Industry Highlights:

- Leading Propulsion Type: Electric vehicles, approximately 86.3% share in 2026, backed by their simple architecture and low maintenance requirements that support high-utilization robotaxi fleets.

- Dominant Component: LiDAR, nearly 42.5% in 2026, as it delivers highly accurate 3D spatial mapping, which improves object detection and safety in complex urban driving conditions.

- New Launch: In March 2026, Amazon's Zoox announced plans to deploy its purpose-built robotaxis in Austin and Miami. The expansion marked a new milestone for the self-driving unit, which had previously opened rides to the public in Las Vegas and San Francisco.

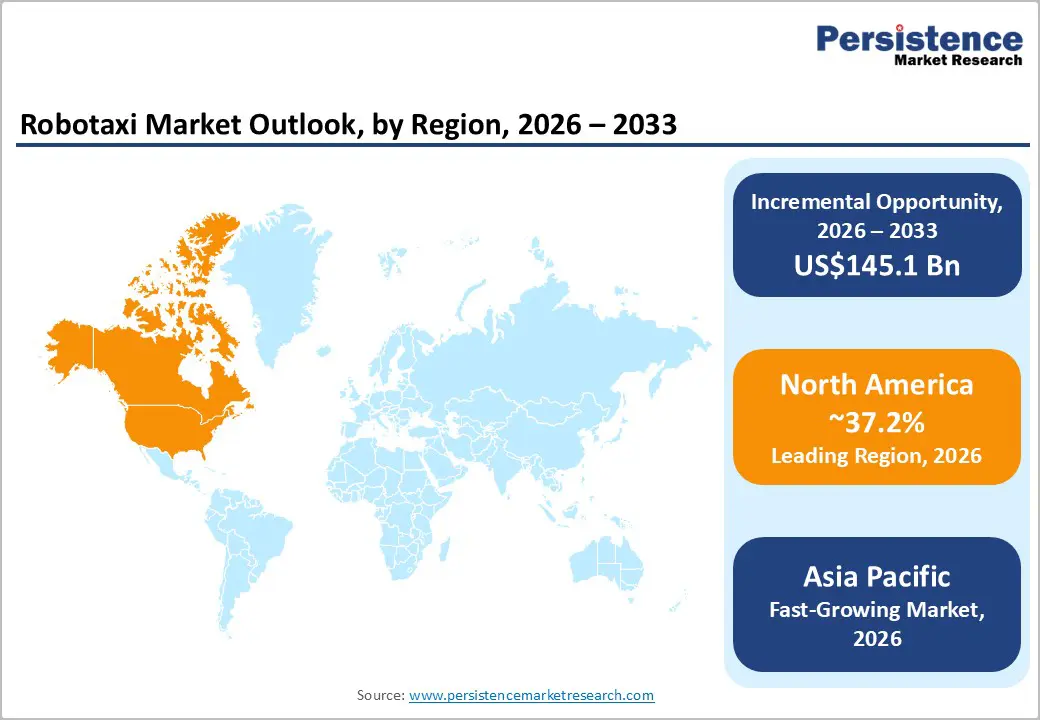

- Leading Region: North America, with about 37.2% share in 2026, spurred by early regulatory approvals, surging private investment, and the presence of commercial-scale operators such as Waymo.

- Fast-growing Region: Asia Pacific, as governments are enabling large-scale real-world deployments through dedicated autonomous driving zones and fast approvals.

DRO Analysis

Driver - Increasing Demand for Low-cost Transportation Options

Removing the human driver is transforming the cost structure of urban mobility. Labor accounts for a key share of taxi and ride-hailing expenses, so eliminating it allows operators to lower fares while maintaining margins. This is already visible in China, where Baidu’s Apollo Go reported in 2024 that fully driverless rides in Wuhan were priced close to or below traditional taxis on several routes.

The company also disclosed that its unit economics improved after expanding to thousands of rides per day. In the U.S., Waymo stated in its public safety reports that high vehicle utilization enabled by autonomous operation helps spread fixed costs across more trips. This makes robotaxis more viable in dense cities where vehicles can run almost continuously without driver fatigue or shift limits.

Surging Need to Lower Emissions and Improve Operational Efficiency

Most robotaxi fleets are designed as electric-first systems, which improves both emissions and operational efficiency. According to the International Energy Agency (IEA), electric vehicles can cut lifecycle emissions significantly when powered by clean grids, making them suitable for city-level decarbonization goals. Cities such as San Francisco and Phoenix are already using autonomous electric fleets from Waymo, which operate in shared mobility formats.

Shared usage reduces idle time and increases vehicle occupancy, which can lower the total number of cars required. A 2023 study published in Nature Energy also noted that shared autonomous EVs could reduce urban vehicle stock if widely adopted. This combination of electrification and high utilization supports both environmental targets and better asset productivity for fleet operators.

Restraint - Reliability Risks from Software and Sensor Errors

Despite progress, system reliability remains a key barrier. Autonomous systems rely on sensors such as LiDAR, cameras, and radar, along with complex AI models. Errors in perception or decision-making can lead to sudden braking or vehicles stopping unexpectedly. The U.S. National Highway Traffic Safety Administration (NHTSA) has opened multiple investigations into autonomous driving systems after incidents involving erratic behavior, including unnecessary stops and collisions with stationary objects.

In 2023, General Motors’ Cruise temporarily paused operations in several cities after safety concerns linked to software responses in complex traffic scenarios. These cases highlight that edge situations, including unusual road layouts or unpredictable pedestrian movement, are still difficult for AI systems to handle consistently. Until these issues are reduced, public trust and regulatory approvals may remain limited.

Opportunity - Expanding Alliances between Tech Firms and Mobility Platforms

Partnerships between technology providers and ride-hailing companies are opening new deployment channels. Uber has publicly stated its plan to act as a platform for multiple autonomous fleet operators rather than building its own full-stack system. It has partnered with companies such as Waymo and announced collaborations involving AI infrastructure players, including NVIDIA, to improve simulation and real-world data integration.

These partnerships allow speedy expansion because ride-hailing apps already have large user bases and routing systems in place. In 2024, Uber began integrating autonomous rides in select U.S. cities, showing how hybrid fleets can coexist. This model reduces entry barriers for new robotaxi players while helping platforms transition without disrupting existing services.

Emergence of Custom-Built and Bidirectional Autonomous Vehicles

The industry is shifting from modified cars to vehicles designed specifically for autonomy. Amazon-owned Zoox is a key example, developing bidirectional, steering wheel-free vehicles customized for dense city environments. These vehicles are already being tested in Las Vegas and parts of California. Unlike retrofitted cars, purpose-built models optimize passenger space, safety, and sensor placement from the ground up. This improves both rider experience and system performance.

China’s Pony.ai and AutoX are also working on dedicated robotaxi designs to improve durability and reduce maintenance costs. Custom-built vehicles further support features such as easy entry or exit and better energy efficiency, which are important for high-frequency urban operations.

Category-wise Analysis

Propulsion Type Insights

The electric vehicles segment is predicted to lead with a share of approximately 86.3% in 2026, as EVs are easy to integrate with full autonomy. Robotaxis require high uptime, low maintenance, and smooth control systems. EVs deliver all three. They have a few moving parts, which reduces breakdown risk in fleet operations. Governments are also pushing EV-only fleets for urban mobility. For example, the California Public Utilities Commission has approved fully electric autonomous fleets for commercial services. In China, Baidu’s Apollo Go robotaxis are fully electric and operate in cities such as Wuhan. This shows that large deployments are already EV-first, not hybrid or ICE-based.

Hybrid electric vehicles are estimated to be the fastest-growing segment in the forecast period, as they solve range anxiety, which still affects robotaxi deployment. Various cities lack dense charging infrastructure. Hybrids allow long operating hours without frequent charging breaks. This is useful in early-stage markets. For instance, Pony.ai has tested hybrid robotaxis to maintain continuous service in Beijing and California. Industry whitepapers from the International Energy Agency highlight that hybrid adoption remains strong in transitional mobility systems, especially where infrastructure gaps exist.

User Insights

The LiDAR segment is anticipated to dominate with a share of nearly 42.5% in 2026, as it provides precise 3D mapping, which is important for safe navigation. Robotaxis operate in dense urban areas with unpredictable objects. Cameras alone cannot deliver accurate depth perception. LiDAR creates a real-time 3D point cloud, improving object detection accuracy. Waymo’s safety reports show that LiDAR helps detect pedestrians and cyclists even in low-light conditions. A study published in the journal Nature Electronics also confirms that LiDAR-based perception systems reduce object detection errors in autonomous driving compared to vision-only systems.

The camera segment is expected to remain in the second position in 2026, because they capture visual context that LiDAR cannot. They detect colors, traffic lights, road signs, and lane markings. This information is critical for decision-making. Companies such as Tesla rely heavily on camera-based systems for training AI models using real-world driving data. Tesla’s 2024 AI Day presentation showed that its fleet collects billions of miles of visual data, which helps improve object recognition and driving behavior. This makes cameras a core component even in LiDAR-based systems.

Regional Insights

North America Robotaxi Market Trends

In 2026, North America will dominate with a share of around 37.2%, owing to early regulatory approvals and increasing private investment. The U.S. has allowed commercial robotaxi operations in multiple cities. Waymo operates fully driverless services in Phoenix and San Francisco. The National Highway Traffic Safety Administration has also created frameworks for autonomous vehicle testing. Companies, including Cruise, received permits for paid rides before pausing operations for safety reviews. This regulatory openness has accelerated real-world deployment compared to other regions.

U.S. Robotaxi Market Trends

The U.S. market is expected to broaden through multi-city expansion and partnerships. Waymo is extending into Los Angeles and Austin. Uber has partnered with multiple Autonomous Vehicle (AV) companies to integrate robotaxis into its platform. According to a U.S. Department of Transportation report, autonomous vehicle testing miles continue to rise every year, showing steady progress toward commercialization. The focus is now shifting from pilot testing to fleet economics and profitability.

Asia Pacific Robotaxi Market Trends

Asia Pacific is growing fast as governments are actively supporting deployment. China has designated multiple pilot zones for autonomous driving. Cities such as Wuhan and Shenzhen allow fully driverless operations in large areas. Companies are also expanding speedily due to low operational costs. According to China’s Ministry of Industry and Information Technology, several cities now allow commercial robotaxi services without safety drivers. This level of policy support is unmatched globally.

Japan Robotaxi Market Trends

Japan’s growth is propelled by a structural need rather than just innovation. The country faces a severe shortage of drivers due to an aging population. This has pushed the government to actively support Level 4 autonomous deployment. The Ministry of Land, Infrastructure, Transport, and Tourism has already approved driverless services in rural areas. These are not just pilot projects, but they are operational mobility solutions for local communities. Toyota is also investing in long-term infrastructure through its Woven City project, which will act as a testing ground for fully autonomous urban mobility. Japan’s approach is focused on reliability and social impact rather than speedy expansion.

China Robotaxi Market Trends

China’s advantage is not just size. It is the speed of execution. Baidu has deployed fully driverless robotaxis in multiple cities, with no safety drivers in certain zones. WeRide has expanded into the Middle East, including Abu Dhabi, through government-backed partnerships. Pony.ai is focusing on reducing hardware costs to make robotaxi rides commercially viable. What makes China lucrative is the combination of high local demand, government-backed pilot zones, and quick approval cycles. This reduces the time required to move from testing to revenue generation.

Europe Robotaxi Market Trends

Europe is not lagging in technology. It is prioritizing safety and standardization. The European Union is developing unified rules under its automated mobility strategy. Programs under Horizon Europe are funding cross-border AV projects. Countries such as France and Germany are running controlled urban pilots instead of open commercial deployments. This reduces risks but slows down expansion. However, it builds strong public trust, which is important for long-term adoption. The region is also focusing on integrating robotaxis with public transport systems rather than replacing them.

Germany Robotaxi Market Trends

Germany’s strategy is different from both the U.S. and China. It is integrating autonomy into its existing automotive ecosystem step by step. The country legalized Level 4 autonomous driving in 2021, which allows driverless operation in defined areas. Mercedes-Benz has already introduced Level 3 systems, such as Drive Pilot, approved for highway use. The focus is first on premium vehicles and controlled environments, including highways and logistics hubs. Robotaxis will likely follow once the technology proves reliable in these conditions. Germany’s strength lies in engineering quality and regulatory clarity, which support steady and predictable growth rather than swift expansion.

U.K. Robotaxi Market Trends

The U.K. is taking a software-first approach. It is focusing on AI-based autonomy rather than hardware-heavy systems. The government has passed the Automated Vehicles Act to support commercial deployment. Cities such as London and Oxford are being used as real-world testing grounds due to their complex traffic environments. Wayve is a key example. It is developing self-learning AI models that adapt to different driving conditions without relying heavily on pre-mapped data. The Center for Connected and Autonomous Vehicles is funding multiple projects, making the U.K. one of the most active AV research hubs in Europe.

Competitive Landscape

The global robotaxi market is highly fragmented but rapidly consolidating around a few leaders. The competitive landscape is dominated by two regional power blocs. In the U.S., Waymo remains the operational leader with fully driverless commercial services already running across multiple cities. Tesla, on the other hand, is influencing the market differently. Instead of using expensive LiDAR-heavy systems, it is betting on a vision-only AI model assisted primarily by cameras and neural networks. This has divided the industry.

Early robotaxis used costly sensor suites that made profitability difficult. New generations from Pony.ai, WeRide, and Xpeng are focusing on reducing hardware costs significantly while maintaining Level 4 capability. Several firms now claim their robotaxi hardware costs are approaching premium EV pricing levels rather than experimental prototype costs. This shift is important as the industry’s long-term success depends less on whether autonomous driving works and more on whether autonomous rides become cheaper than human-driven ride-hailing.

Key Industry Developments:

- In May 2026, Uber moved to reduce its dependence on Waymo by committing more than US$10 billion to build a parallel autonomous vehicle fleet. The company struck new partnerships with Rivian, Lucid, and Nuro for vehicle supply, while also investing US$100 million in fast-charging hubs specifically for autonomous vehicles.

- In February 2026, Waymo closed a US$16 billion funding round, valuing the Alphabet-owned company at US$126 billion. The funds were earmarked to support expansion to 20 additional cities through 2026, including London and Tokyo.

- In January 2026, Lucid Group, Nuro, and Uber launched a jointly developed production-intent global robotaxi at the Consumer Electronics Show. The companies revealed the Uber-designed in-cabin rider experience and announced that autonomous on-road testing had begun in December 2025 in the San Francisco Bay Area.

Companies Covered in Robotaxi Market

- Waymo LLC

- Baidu, Inc.

- WeRide Inc.

- Pony AI Inc.

- Tesla Inc.

- Zoox, Inc.

- Didi Chuxing Technology Co., Ltd.

- EasyMile

- Aptiv

- Uber Technologies Inc.

Frequently Asked Questions

The global robotaxi market is projected to be valued at US$8.3 billion in 2026.

The market is expected to reach US$153.4 billion by 2033.

Key market trends include a shift toward fully driverless operations and cost reduction in sensor hardware.

Electric vehicles are expected to be the leading propulsion type with a share of nearly 86.3% in 2026, as they comply with strict urban emission policies that favor zero-emission autonomous mobility deployments.

The market is expected to grow at a CAGR of 51.7% from 2026 to 2033.

Waymo LLC, Baidu, Inc., WeRide Inc., and Pony AI Inc. are a few key market players.