- Transportation & Logistics

- Dock and Yard Management Systems Market

Dock and Yard Management Systems Market Size, Share, and Growth Forecast 2026 - 2033

Dock and Yard Management Systems Market by Component (Software, Services), Deployment (On-premises, Cloud), Functionality (Yard Visibility & Asset Tracking), End-user (Transportation & Logistics), and Regional Analysis, 2026 - 2033

Dock and Yard Management Systems Market Size and Trends Analysis

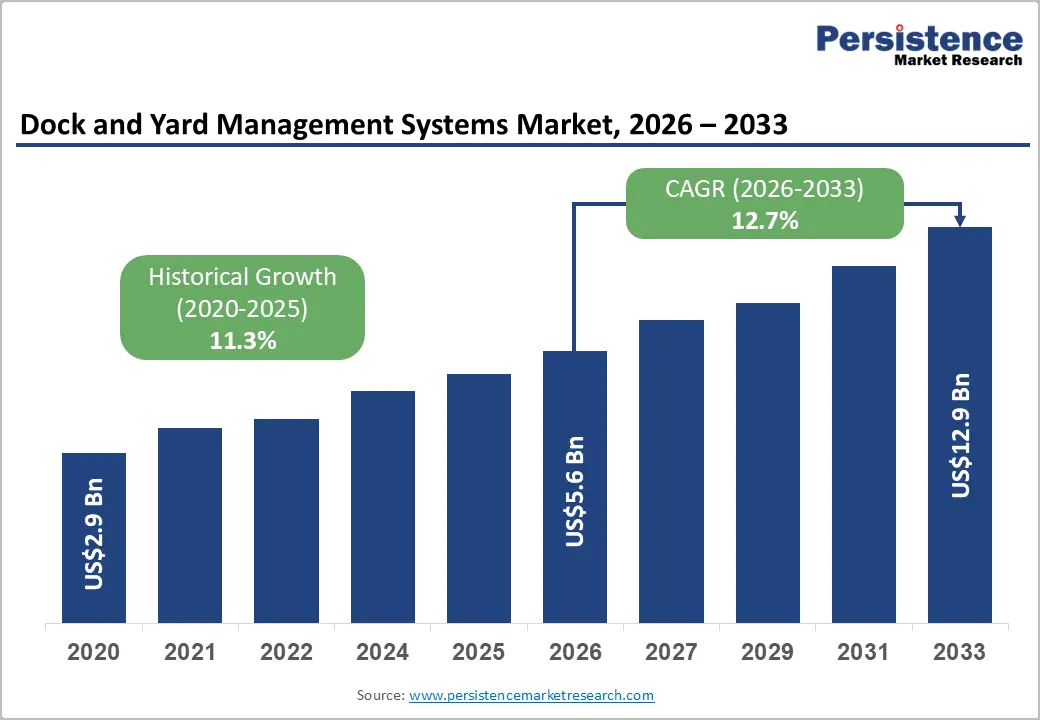

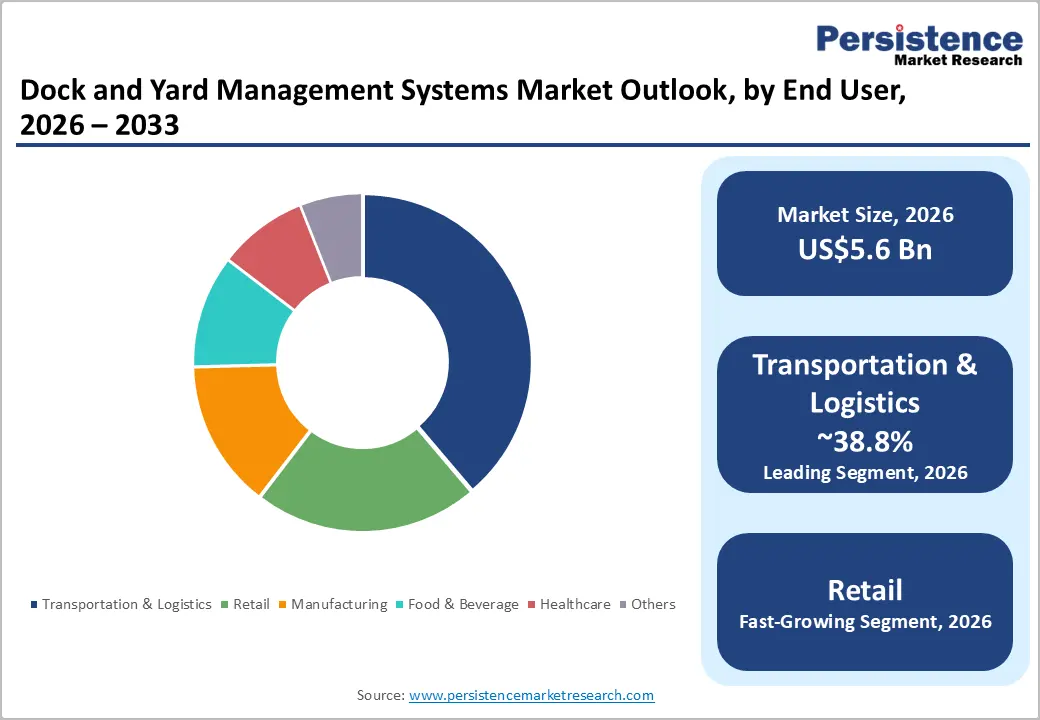

The global dock and yard management systems market size is likely to be valued at US$5.6 billion in 2026 and is expected to reach US$12.9 billion by 2033, growing at a CAGR of 12.7% during the forecast period from 2026 to 2033, driven by rising demand for real-time yard visibility, increasing warehouse congestion, and surging complexity of supply chain operations across e-commerce and manufacturing sectors. Expansion of omnichannel retail models is also pushing logistics providers to adopt dock and yard management systems to reduce truck dwell times.

Key Industry Highlights:

- Leading Functionality: Yard visibility and asset tracking, approximately 41.6% share in 2026, as it enables real-time trailer location and reduces dwell time.

- Dominant End-user: Transportation and logistics, nearly 38.8% in 2026, as it handles high freight volumes where even minor yard delays increase detention costs.

- New Launch: In October 2025, Royal 4 Systems launched Titan, its new stand-alone Yard Management System (YMS) for enterprise customers, bringing additional features and functions as well as being delivered as a stand-alone product.

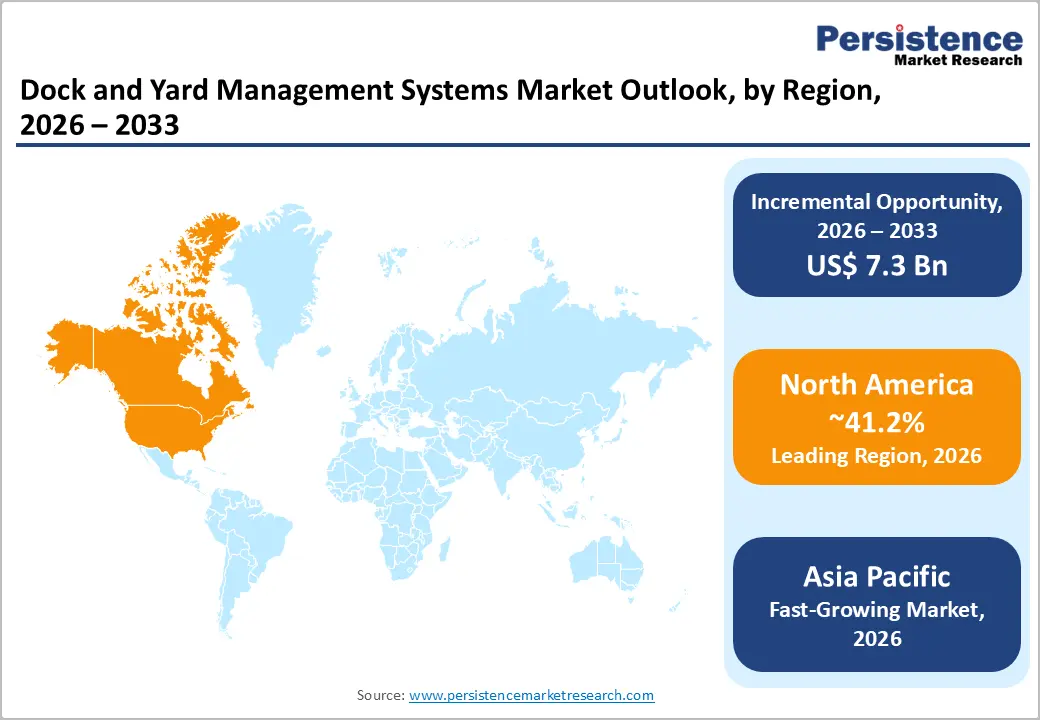

- Leading Region: North America, with about 41.2% share in 2026, spurred by early adoption of warehouse automation and the presence of large logistics firms.

- Fast-growing Region: Asia Pacific, backed by the expansion of e-commerce and new smart logistics parks.

DRO Analysis

Driver - Surge in E-Commerce Parcel Volumes

Traditional warehouses were built for bulk shipments. E-commerce flips that model entirely as it sends a flood of individual parcels through the same dock doors. In 2024, U.S. e-commerce sales reached US$1.19 trillion, accounting for 16.1% of total retail sales, according to the U.S. Census Bureau. This shift has overwhelmed manual dock scheduling systems built for far lower throughput. Retail and e-commerce already account for the largest share of Dock and Yard Management Systems (DYMS) deployments.

Beverage distribution pilots that adopted automated dock appointment tools cut truck waiting times by 40% and lifted throughput capacity by 25% during peak weeks, according to an Opendock case study. Brick-and-mortar retailers moving to omnichannel fulfillment face the same pressure. As parcel volumes continue climbing, facilities have little choice but to replace clipboards and spreadsheets with intelligent dock and yard platforms.

Workforce Gaps to Boost Automation in Yard Operations

A shrinking labor pool is compelling logistics operators to rethink how yards are managed. Between December 2024 and April 2025, U.S. employers posted more than 320,000 openings for skilled hourly warehouse roles. The average turnover rate for warehouse workers now sits around 45%, one of the highest across all industries. On top of that, according to the Bureau of Labor Statistics, only 3.5% of Generation Z respondents expressed interest in working in manufacturing, and only 2.9% in transportation, distribution, and logistics.

It shows that the pipeline is not improving. Dock and yard systems help bridge this gap by automating driver check-ins, trailer tracking, and gate management with minimal human intervention. As per a few research studies, by 2028, there is expected to be more smart robots than frontline workers in manufacturing, retail, and logistics due to labor shortages.

Restraint - Security Vulnerabilities in Networked Yard Environments

As yards become more connected, they also become bigger targets. Modern DYMS platforms integrate with IoT sensors, RFID readers, gate cameras, and cloud-based WMS as well as TMS tools. Every integration adds a potential entry point for attackers. In late 2024, Blue Yonder's cloud platform, used by Morrisons and other leading retailers, was compromised by a cyberattack, compelling a return to manual processes in most Morrisons' U.K. warehouses.

The broad picture is equally alarming. Cyble documented 6,604 ransomware attacks in 2025, up 52% from 4,346 in 2024, with supply chain attacks nearly doubling, from 154 incidents in 2024 to 297 in 2025. For yard operators, a breach can mean halted shipments, missed delivery windows, and regulatory non-compliance. This fear slows down technology adoption, mainly among mid-sized operators who lack dedicated security teams to manage connected infrastructure risks.

Opportunity - Regulatory Pressure to Cut Truck Dwell Times

Government bodies are pushing hard on dock and detention inefficiencies. The Federal Motor Carrier Safety Administration’s (FMCSA) detention time study was the result of a directive from Congress included in the 2021 infrastructure law, requiring the agency to study the prevalence and impact of detention time in the trucking industry. The findings have commercial consequences. A 2018 DOT Office of Inspector General report estimated that a 15-minute increase in average dwell time increases the expected crash rate by 6.2%.

That detention time costs for-hire CMV drivers between US$1.1 billion and US$1.3 billion in lost annual earnings. On the emissions front, the California Air Resources Board (CARB) has been tightening rules on trucks idling at ports and facilities. FMCSA suggests that drivers experiencing short detention periods are more likely to operate within prescribed hours-of-service limits. It makes dock scheduling tools a compliance asset and not just an operational one. This regulatory backdrop gives shippers a concrete business case to invest in automated dock management.

Cloud-Native Suites to Bring YMS Within Reach of Mid-Market Operators

The shift to cloud has changed who can afford a yard management system. Enterprise-grade platforms that once required six-figure on-premise deployments are now available as SaaS subscriptions. Leading players in supply chain software, including SAP, Manhattan Associates, and Blue Yonder, all reported double-digit revenue growth in 2024, with cloud-based solutions and SaaS models accounting for a big part of that growth.

In June 2025, Manhattan Associates partnered with a cloud provider to deliver yard modules customized specifically for mid-market operators. Blue Yonder reported a 35% jump in yard software bookings in May 2025, spurred by automotive and pharmaceutical demand. Even start-ups are entering this field. In February 2025, Tansect launched OptiYard.ai, a free cloud-based YMS, dramatically lowering barriers for small facilities that previously relied on spreadsheets.

Category-wise Analysis

Functionality Insights

The yard visibility and asset tracking segment is predicted to lead with a share of approximately 41.6% in 2026, as it reduces delays and hidden costs in yard operations. Several logistics yards still struggle with lost trailers and poor coordination between gate, yard, and dock teams. Real-time visibility using RFID, GPS, and IoT sensors solves this gap. For example, the U.S. Department of Transportation has highlighted that idle truck time at freight facilities remains a key inefficiency, contributing to congestion and fuel waste. Companies are responding by deploying real-time tracking systems that show exact trailer location, dwell time, and movement history.

The mobile task and shunter management segment is estimated to be the fastest-growing segment over the forecast period, as it improves workforce efficiency in real time. Yard operations depend heavily on shunters or yard drivers who move trailers between gates and docks. Traditionally, tasks were assigned manually using radios or paper lists, which caused delays and miscommunication. Mobile-based task management apps now allow real-time job allocation, route optimization, and instant updates. For instance, Körber Supply Chain introduced mobile-first yard solutions that guide drivers with live instructions, reducing idle movement.

End User Insights

The transportation and logistics segment is anticipated to dominate with a share of nearly 38.8% in 2026, as yard operations are central to freight movement efficiency. Logistics companies manage high volumes of inbound and outbound trucks daily, making yard coordination important. Delays at docks directly increase detention costs and disrupt delivery schedules.

The Federal Motor Carrier Safety Administration has emphasized that detention time remains a key issue for carriers, often leading to productivity losses and driver dissatisfaction. Large logistics players such as DHL and XPO Logistics have invested heavily in yard management systems to reduce turnaround times and improve fleet utilization.

The retail segment is expected to remain in the second position in 2026, owing to the pressure from e-commerce and omnichannel fulfillment. Retailers are dealing with unpredictable demand patterns and high return volumes, especially after the rise of online shopping. This creates heavy congestion at distribution centers and store backyards. The U.S. Census Bureau reported that e-commerce continues to account for a growing share of total retail sales, increasing the load on fulfillment networks. Companies such as Walmart have implemented advanced yard management systems with AI-based scheduling to handle peak volumes during events like Black Friday.

Regional Insights

North America Dock and Yard Management Systems Market Trends

In 2026, North America will dominate with a share of around 41.2%, owing to infrastructure maturity, regulatory pressure, and a dense concentration of large-scale logistics operators. Hours-of-Service and Electronic Logging Device (ELD) mandates reward shippers that minimize detention, pushing continuous improvement initiatives across grocery, retail, and automotive supply chains. These regulations have effectively made dock efficiency a compliance issue, not just an operational one.

U.S. Dock and Yard Management Systems Market Trends

The U.S. dominates North America owing to speedy development in e-commerce, deployment of automated solutions in modern warehouses, rising popularity of 3PL logistics, and ongoing adoption of multimodal transport hubs. Reshoring trends are adding further momentum, as manufacturers relocating production back to the U.S. are building new facilities that require yard management from the ground up. Integrated visibility suites now relay trailer Estimated Time of Arrival (ETA) data to facility staff, allowing proactive labor and door allocation.

Asia Pacific Dock and Yard Management Systems Market Trends

Asia Pacific is anticipated to be the fastest-growing market over the forecast period, backed by a booming e-commerce sector, massive government-backed warehouse construction, and rising automation investment. In China, e-commerce giants fund automated mega-hubs, while government logistics corridors under the Belt and Road Initiative push sustained warehouse construction. India's National Logistics Policy incentivizes warehouse modernization, and Japan leans on automation to counter demographic labor gaps.

China Dock and Yard Management Systems Market Trends

China is considered the single largest contributor to Asia Pacific's growth. Its e-commerce expansion alone justifies enormous logistics technology investment. During the country’s Singles' Day 2024, platforms processed 2.9 billion parcels in 72 hours, compelling logistics providers to adopt sortation robots capable of handling 30,000 packages per hour. JD Logistics, by the end of 2024, was operating approximately 3,600 warehouses, including cloud warehouses for partners. Cainiao's global push also reflects how domestic logistics operations are now exporting dock and yard infrastructure requirements beyond domestic borders.

Japan Dock and Yard Management Systems Market Trends

Japan's urgency around dock and yard automation stems from a government-imposed labor crisis. In April 2024, the country’s government implemented new working time legislation limiting truck drivers' annual overtime. The new cap is anticipated to result in a 14% reduction in truck transport capacity in 2024, potentially extending to a 34% shortage by 2030 if no countermeasures are implemented.

With fewer drivers spending less time at facilities, every minute at the dock becomes more valuable, which spurs demand for automated dock scheduling and yard visibility tools. The government responded with a policy package to encourage increasing developments in logistics in June 2023.

Europe Dock and Yard Management Systems Market Trends

Europe's growth is more measured than Asia Pacific's but structurally durable, accelerated by regulatory compliance requirements and a superior industrial base. Between 2019 and 2024, the European Union introduced regulations mandating improved IT security and data protection across supply chains, compelling dock and yard management providers to implement GDPR-compliant protocols. The EU's Smart Logistics initiative, launched in 2021, also focuses on digitization and sustainability, thereby encouraging the adoption of energy-efficient and interoperable management systems in ports and logistics hubs.

Germany Dock and Yard Management Systems Market Trends

Germany sits at the crossroads of Europe’s automotive manufacturing and logistics, making it a natural hub for dock and yard technology adoption. Its automotive sector, home to Volkswagen, BMW, Mercedes-Benz, and their vast supplier networks, depends on precise yard scheduling to keep assembly lines moving.

In March 2025, local supply chain software provider EPG (Ehrhardt Partner Group) acquired Berlin-based dock and yard management company byways, integrating its real-time coordination platform into the EPG ONE Suite. The move aimed to eliminate dock scheduling inefficiencies by enabling intelligent automation and synchronized communication between warehouses, carriers, suppliers, and freight forwarders.

U.K. Dock and Yard Management Systems Market Trends

The U.K. market is being pushed forward by tight urban logistics constraints and hard lessons from cybersecurity failures. The market is witnessing momentum driven by rising investment in logistics infrastructure, increased adoption of automation in last-mile hubs, surging pressure to optimize limited urban yard space, and a growing focus on sustainable yard operations.

The November 2024 ransomware attack on Blue Yonder was a defining moment. Morrisons, which operates about 500 stores across the U.K., had its warehouse management system for fresh food and produce knocked offline, compelling the retailer to build an entirely new warehouse management system to maintain stock levels.

Competitive Landscape

The global dock and yard management systems market is moderately fragmented, with the presence of large enterprise software providers and specialized logistics technology vendors. Companies such as Manhattan Associates, Blue Yonder, SAP, Oracle, and Descartes Systems Group dominate large enterprise deployments. Niche players, including C3 Solutions and Loadsmart, are gaining traction through AI-led innovations and speedy SaaS deployments. The top five vendors collectively account for slightly over half of the market presence, indicating increased competition from mid-sized and emerging providers.

Vendors are no longer competing only on scheduling efficiency. They are positioning themselves as end-to-end logistics orchestration partners. For example, in 2024, FourKites integrated EAIGLE’s AI and computer vision technology into its yard and appointment management platform to enable autonomous gate operations and continuous trailer monitoring. Large companies are also actively acquiring niche logistics software providers to strengthen AI, automation, and analytics capabilities instead of building everything organically.

Key Industry Developments:

- In January 2026, Vector announced its acquisition of YardView, a pioneer in yard management and dock visibility. By unifying Vector's digital workflows with YardView's real-time asset tracking, the company aimed to close the visibility gap between the transfer of custody and the increasing pressure to digitize handoffs across the supply chain.

- In February 2025, Loadsmart announced the launch of its new Yard Management System (YMS) at Manifest in Las Vegas. The YMS digitizes docks, yards, and gates by enabling customers to oversee truck movements, track assets, and improve coordination from one interface.

- In February 2025, Tansect unveiled OptiYard.ai, a free cloud-based Yard Management System (YMS) designed for both small and large facilities. The platform was free for the first two users at a site and for the first 25 yard/dock locations, with the maximum paid tier priced at US$599 annually.

Companies Covered in Dock and Yard Management Systems Market

- Manhattan Associates, Inc.

- Blue Yonder Group, Inc.

- C3 Solutions, Inc.

- Descartes Systems Group Inc.

- 4SIGHT Connect (4sight Solution)

- Epicor Software Corporation

- Oracle Corporation

- SAP SE

- Infor, Inc.

- Zebra Technologies Corporation

- Others

Frequently Asked Questions

The global dock and yard management systems market is projected to be valued at US$5.6 billion in 2026.

The market is expected to reach US$12.9 billion by 2033.

Key market trends include rising adoption of AI for yard automation and a shift toward cloud-based platforms.

Transportation and logistics are expected to be the leading end user with a share of nearly 38.8% in 2026, as it relies on synchronized yard, fleet, and dock operations.

The dock and yard management systems market is expected to grow at a CAGR of 12.7% from 2026 to 2033.

Manhattan Associates, Inc., Blue Yonder Group, Inc., and C3 Solutions, Inc. are a few key market players.