- Specialty & Fine Chemicals

- Thermic Fluid Market

Thermic Fluid Market Size, Share, and Growth Forecast, 2026 - 2033

Thermic Fluid Market by Product Type (Silicone & Aromatic-Based Fluids, Glycol-Based Fluids, Others), Application (Oil & Gas, Concentrated Solar Power (CSP), Others), Temperature Grade, End-use Industry, and Regional Analysis for 2026 - 2033

Thermic Fluid Market Size and Trends Analysis

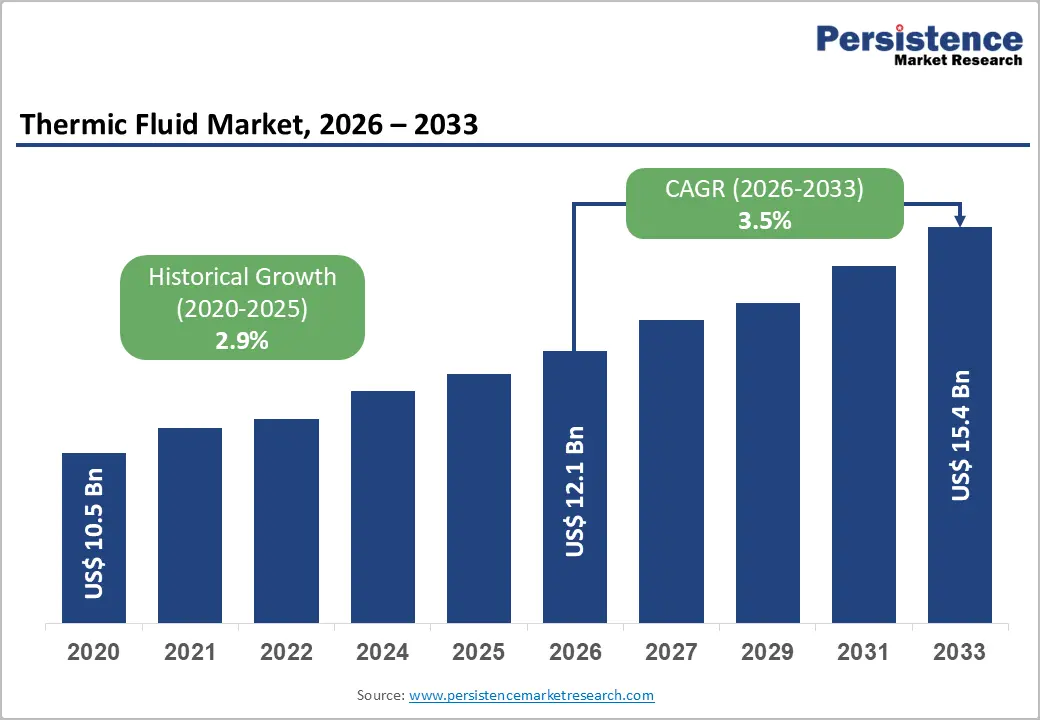

The global thermic fluid market size is likely to be valued at US$12.1 billion in 2026 and is expected to reach US$15.4 billion by 2033, growing at a CAGR of 3.5% during the forecast period from 2026 to 2033, driven by the evolving role of thermic fluids from traditional process heating agents to essential thermal management solutions across industries including oil & gas, chemicals, pharmaceuticals, food processing, and renewable energy.

Industrial heat remains a major contributor to demand, representing nearly 40% of global final energy consumption, with consumption expected to rise by 14% (+16 EJ) between 2025 and 2030. In addition, the increasing deployment of concentrated solar power (CSP) plants and thermal energy storage systems is strengthening the long-term demand for advanced heat transfer fluids.

Key Industry Highlights:

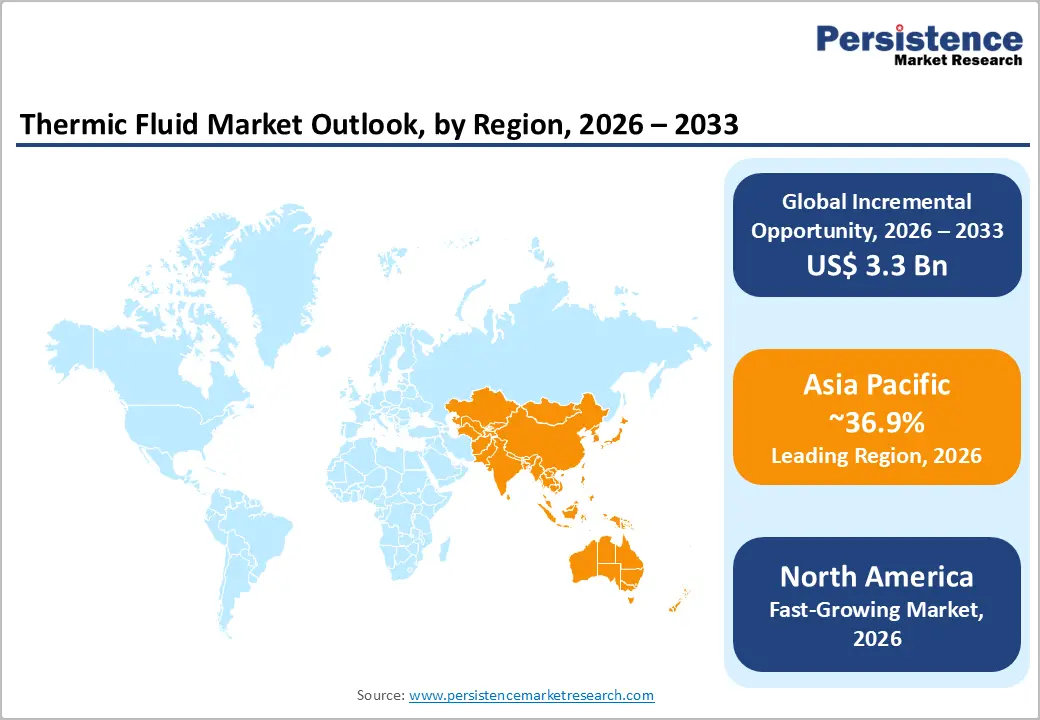

- Leading Region: Asia Pacific is projected to account for approximately 36.9% of the market share, driven by strong industrial expansion, refining capacity, and manufacturing growth across China, India, and ASEAN countries.

- Fastest-growing Region: North America is emerging as the fastest-growing region, supported by advancements in thermal energy systems, CSP innovation, and increasing adoption of high-performance thermic fluids in industrial and renewable applications.

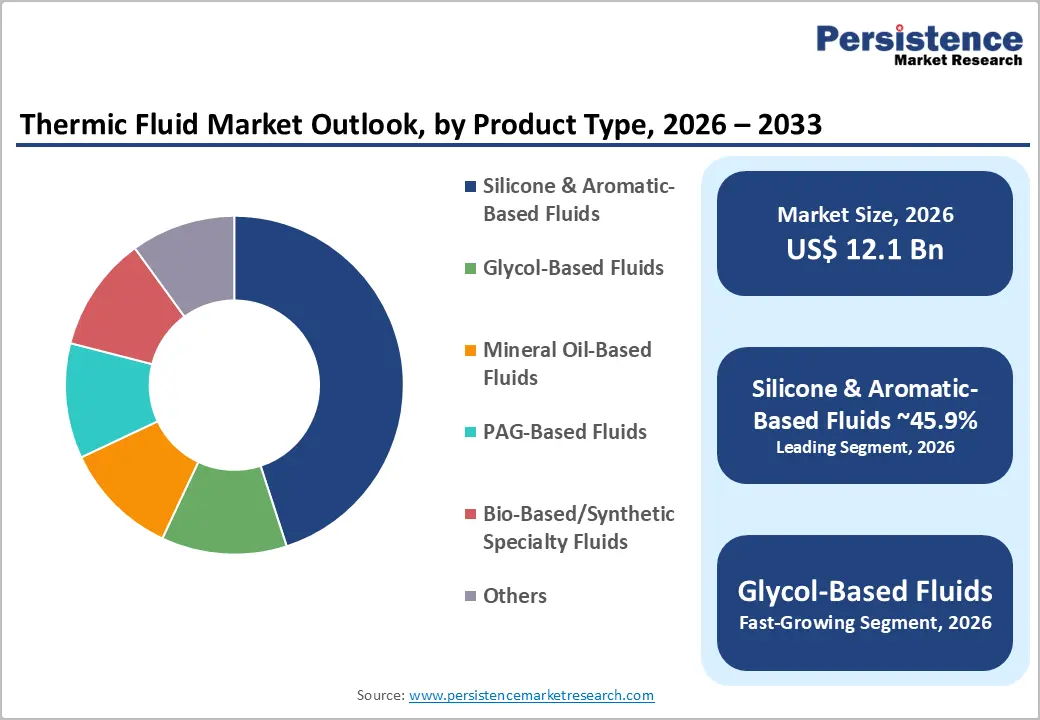

- Dominant Product Type: Silicone and aromatic-based fluids are anticipated to lead, holding approximately 45.9% of market share, due to their superior thermal stability and suitability for high-temperature industrial applications.

- Leading Application: The oil and gas segment is estimated to lead, accounting for approximately 31.8% of market share, supported by sustained demand from refining and petrochemical operations requiring precise and reliable heat transfer systems.

DRO Analysis

Drivers - Industrial Heat Decarbonization Driving Demand for High-Performance Fluids

Industrial process heat decarbonization is significantly increasing the value of advanced thermic fluids. Global industrial energy demand continues to expand, with China and India expected to account for more than half of incremental industrial heat demand through 2030. Thermic fluids play a critical role in closed-loop heating systems where thermal stability, low volatility, and operational safety are essential.

Policy frameworks in major economies are accelerating this shift. Europe’s industrial decarbonization initiatives and energy transition programs are pushing industries to adopt energy-efficient and low-emission heating systems. These policies do not eliminate thermic fluid systems but instead increase demand for premium-grade fluids that can deliver higher efficiency, reduced degradation, and longer service life. This trend is driving upgrading cycles, where end users replace conventional mineral oils with synthetic or specialty fluids, increasing average revenue per system and strengthening margins for manufacturers.

Growth of CSP and Thermal Energy Storage Supporting High-Temperature Fluids

The expansion of concentrated solar power (CSP) and thermal storage systems is reinforcing demand for high-temperature thermic fluids. CSP plants rely on heat transfer fluids to capture solar energy and convert it into steam for electricity generation. These systems require fluids capable of operating at temperatures ranging from 400°C to over 500°C.

As renewable energy systems increasingly incorporate thermal storage for grid stability, thermic fluids are becoming essential in enabling dispatchable renewable power. This is particularly relevant in regions with high solar irradiance and energy transition targets.

The demand for silicone-based, aromatic, and synthetic specialty fluids is rising, as these formulations offer superior thermal stability and oxidation resistance, making them ideal for high-temperature and cyclic operations.

Restraint - Operational Complexity and Electrification Alternatives Limiting Adoption

High operational requirements and emerging electrification technologies are moderating market growth. Thermic fluid systems require careful system design, leak prevention, and ongoing maintenance to ensure safety and efficiency. These requirements increase lifecycle costs and operational complexity, especially in high-temperature applications.

At the same time, industrial electrification is gaining traction, particularly in developed regions. Electric heating technologies, supported by policy incentives and renewable energy integration, are becoming viable alternatives for low- and medium-temperature applications.

While thermic fluids remain indispensable in high-temperature systems, adoption rates may slow in segments where electrification offers lower capital or operational costs, creating a partial substitution effect rather than full displacement.

Opportunity - Policy-Driven Industrial Heat Projects Creating Premium Product Demand

Government-backed decarbonization initiatives are creating new opportunities for advanced thermic fluid solutions. Large-scale funding programs for industrial heat optimization are encouraging the adoption of energy-efficient heating technologies, including high-performance thermic fluid systems.

This shift enables suppliers to move beyond commodity fluid sales and offer integrated solutions, including system design, monitoring, maintenance, and performance optimization. End users increasingly prioritize total cost of ownership, reliability, and emissions reduction. This trend supports value-added business models, allowing companies to differentiate through service offerings and long-term contracts rather than price competition alone.

Asia Pacific Industrial Expansion Expanding Addressable Market

Rapid industrialization in Asia Pacific is significantly increasing thermic fluid demand. The region accounts for over 37% of the global market, supported by strong growth in manufacturing, refining, and chemical processing industries. Countries such as China and India are experiencing sustained industrial expansion, leading to higher demand for process heating and thermal management solutions. Industrial output growth directly correlates with increased adoption of thermic fluid systems in both new installations and capacity expansions.

Suppliers that invest in regional manufacturing, distribution networks, and technical support capabilities are well-positioned to capture growth in both replacement and greenfield markets.

Category-wise Analysis

Product Type Insights

Silicone & aromatic-based fluids are anticipated to remain the leading segment, accounting for approximately 45.9% of market revenue over the forecast period. These fluids offer high thermal stability, low vapor pressure, and wide operating temperature ranges, making them well-suited for demanding applications such as oil refineries, petrochemical plants, and concentrated solar power (CSP) systems.

For example, silicone-based fluids are widely used in parabolic trough CSP plants due to their ability to operate reliably at temperatures approaching 400°C, while aromatic fluids are commonly deployed in ethylene and styrene production units where precise heat control is critical. Their ability to maintain consistent performance under extreme conditions translates into longer fluid life, reduced oxidation, and lower system downtime, which are key considerations for continuous-process industries.

Glycol-based fluids are anticipated to be the fastest-growing segment. Their advantages include freeze protection, corrosion resistance, and ease of handling, making them particularly suitable for HVAC systems, food processing facilities, and moderate-temperature industrial operations.

For instance, propylene glycol-based fluids are extensively used in food and beverage heat exchangers where non-toxicity is essential, while ethylene glycol formulations are common in district cooling and refrigeration systems. Their lower maintenance requirements and compatibility with existing infrastructure make them an attractive option for retrofit projects and decentralized thermal systems, driving adoption across a broad range of industries.

Application Insights

The oil & gas segment is anticipated to dominate, accounting for approximately 31.8% of market share over the forecast period. Thermic fluids are extensively used in refining and petrochemical processes, where precise temperature control, thermal efficiency, and operational reliability are critical.

For example, thermic fluids are used in crude oil distillation units, asphalt processing, and sulfur recovery systems, where stable heat transfer ensures consistent product quality and safe operations. In petrochemical complexes, they support processes such as polymerization and reactor heating, where temperature fluctuations can significantly impact output quality. The sector’s ongoing focus on energy efficiency, process optimization, and asset longevity continues to sustain steady demand for thermic fluids.

Concentrated solar power (CSP) is anticipated to be the fastest-growing application segment. The integration of thermal energy storage systems in CSP plants enhances grid stability by enabling electricity generation even during non-solar hours.

Thermic fluids play a central role in both heat collection and storage processes, making them indispensable to CSP infrastructure. For example, synthetic heat transfer oils are widely used in parabolic trough systems, while molten salt-based fluids are deployed in tower-based CSP plants with thermal storage capabilities. Projects in regions such as the Middle East, North Africa, and parts of Asia are increasingly adopting CSP with storage, reinforcing long-term demand for high-temperature, high-performance thermic fluids.

Regional Insights

North America Thermic Fluid Market Trends

North America represents a high-growth region, supported by a strong industrial base and advanced energy infrastructure.

U.S. Thermic Fluid Market Trends

The U.S. continues to lead the market due to its extensive refining capacity, well-established chemical manufacturing sector, and increasing investment in renewable and thermal energy systems. For instance, ExxonMobil and Chevron Corporation have ongoing refinery optimization and petrochemical expansion projects along the U.S. Gulf Coast, which sustain steady demand for high-performance thermic fluids in process heating applications.

Government-backed innovation is also shaping regional demand. The U.S. Department of Energy’s continued funding for CSP and industrial heat efficiency programs has encouraged the deployment of advanced heat transfer systems. Companies such as Eastman Chemical Company are actively promoting high-performance thermic fluid solutions such as Therminol for renewable energy and waste heat recovery applications. These developments are accelerating the shift toward premium-grade fluids with longer operational life and higher thermal efficiency.

Key drivers include industrial efficiency improvements, renewable energy integration, and advanced manufacturing technologies. The rise of high-tech manufacturing clusters and data center cooling applications is also expanding the scope of thermic fluid usage beyond traditional industries.

Investment trends indicate strong momentum toward premium formulations, digital monitoring systems, and lifecycle service models. Companies are increasingly integrating IoT-enabled thermal system monitoring to reduce downtime and improve operational safety. This positions North America as a high-value, innovation-driven market where advanced solutions command higher margins.

Europe Thermic Fluid Market Trends

Europe’s thermic fluid market is strongly influenced by stringent environmental regulations and aggressive decarbonization targets. Policies aimed at reducing industrial emissions are driving the adoption of energy-efficient and low-carbon heating technologies, while also pushing industries to upgrade existing thermic fluid systems.

Germany Thermic Fluid Market Trends

Germany remains a critical market due to its large chemical and industrial manufacturing base. Companies such as BASF SE and LANXESS AG are investing in energy-efficient production processes and advanced chemical formulations, which indirectly support demand for high-performance thermic fluids. However, rising energy costs have pressured industrial output, prompting companies to focus on efficiency optimization and system upgrades rather than large-scale expansions.

U.K. Thermic Fluid Market Trends

The U.K. market is evolving under strong policy pressure to decarbonize industrial heat. Initiatives promoting electrification and low-carbon technologies are influencing the adoption of thermic fluids, particularly in applications where thermal efficiency and emissions reduction are critical. Companies are increasingly integrating hybrid systems that combine thermic fluids with renewable energy sources.

Key Drivers include regulatory pressure for decarbonization, growth in renewable energy projects, and industrial efficiency improvements. At the same time, electrification initiatives and high energy costs are creating competitive pressure on traditional thermic fluid systems.

Investment trends are focused on high-performance, regulation-compliant fluids and integrated thermal management solutions. European companies are prioritizing sustainability, emissions compliance, and lifecycle performance, making the region a hub for advanced and environmentally compliant thermic fluid technologies.

Asia Pacific Thermic Fluid Market Trends

Asia Pacific is the largest regional market, accounting for 36.9% of market share, with strong growth supported by rapid industrialization and increasing energy demand. The region’s expansion is closely tied to its role as a global manufacturing hub and its ongoing investments in refining, chemicals, and infrastructure.

China Thermic Fluid Market Trends

China dominates regional demand due to its massive industrial base and large-scale chemical and petrochemical production. State-owned enterprises such as Sinopec continue to expand refining and petrochemical capacities, driving consistent demand for thermic fluids in process heating systems. The country’s push toward energy efficiency and emissions reduction is also encouraging the adoption of advanced and longer-lasting fluid formulations.

India Thermic Fluid Market Trends

India is one of the fastest-growing markets in the region, supported by expanding refining capacity, pharmaceutical production, and food processing industries. Companies such as Indian Oil Corporation Ltd. and Bharat Petroleum Corporation Ltd. are investing in refinery upgrades and downstream expansion projects, which increase demand for thermic fluids. India’s growing focus on renewable energy and CSP projects is further contributing to the adoption of high-temperature thermic fluid systems.

Japan Thermic Fluid Market Trends

Japan contributes through its advanced manufacturing and specialty chemical industries. Companies such as Mitsubishi Chemical Group are focused on high-performance materials and precision industrial processes, where thermic fluids are essential for maintaining tight temperature control and operational stability.

Key Drivers include industrial expansion, infrastructure development, and rising energy consumption. The region’s manufacturing growth directly translates into higher demand for thermal management solutions. Investment trends emphasize localization of production, distribution networks, and technical services. Companies are establishing regional facilities to reduce supply chain risks and improve responsiveness, positioning Asia-Pacific as both the largest and fastest-expanding market for thermic fluids.

Competitive Landscape

The global thermic fluid market is moderately fragmented, characterized by the presence of both global chemical manufacturers and regional suppliers. Large multinational companies such as BASF SE, Dow Inc., and Eastman Chemical Company maintain a strong position in the premium segment, offering high-performance synthetic and specialty thermic fluids designed for demanding industrial and renewable energy applications. These players leverage advanced R&D capabilities, global distribution networks, and strong brand recognition to capture higher-margin opportunities.

Regional companies and national oil firms such as Indian Oil Corporation Ltd. and Hindustan Petroleum Corporation Ltd. focus on cost-competitive offerings, particularly mineral oil-based and mid-range thermic fluids. Their competitive advantage lies in localized production, pricing flexibility, and established relationships with domestic industrial customers. This dual structure creates a market environment where premium innovation and cost efficiency coexist, catering to different end-user priorities across regions.

Companies are expanding their portfolios to include digital monitoring tools, predictive maintenance services, and customized fluid formulations tailored to specific industrial applications. This evolution reflects a broader industry trend where differentiation is achieved through performance optimization, lifecycle cost reduction, and customer-specific solutions, rather than relying solely on product pricing.

Key Industry Developments:

- In January 2025, Global Heat Transfer Ltd. launched Globaltherm® Q, a high-performance synthetic organic heat transfer fluid designed for a wide operating temperature range, strengthening its portfolio for demanding industrial process heating applications.

- In August 2025, Global Heat Transfer Ltd. introduced Globaltherm DBT, a synthetic heat transfer fluid developed for closed-loop, forced circulation systems, targeting enhanced performance and reliability in chemical and plastics processing industries.

Companies Covered in Thermic Fluid Market

- Dow Inc.

- Eastman Chemical Company

- ExxonMobil

- Shell plc

- BASF SE

- Chevron Corporation

- TotalEnergies SE

- Huntsman Corporation

- Clariant AG

- LANXESS AG

- Wacker Chemie AG

- Arkema S.A.

- Indian Oil Corporation Ltd.

- Bharat Petroleum Corporation Ltd.

- Hindustan Petroleum Corporation Ltd.

- Global Heat Transfer Ltd.

- Paratherm

- Schultz

- Dynalene

- Radco Industries

Frequently Asked Questions

The global thermic fluid market is projected to be valued at US$12.1 billion in 2026.

The market is expected to reach approximately US$15.4 billion by 2033.

Key trends include the shift toward high-performance synthetic fluids, increasing adoption in concentrated solar power (CSP) and thermal storage systems, and rising demand for energy-efficient industrial heating solutions.

The silicone and aromatic-based fluids segment leads the market, accounting for approximately 45.9% of revenue share, due to its superior thermal stability and suitability for high-temperature applications.

The thermic fluid market is expected to grow at a CAGR of 3.5% between 2026 and 2033.

Major companies include Dow Inc., Eastman Chemical Company, ExxonMobil, Shell plc, and BASF SE.