- Specialty & Fine Chemicals

- Silicone Elastomers Market

Silicone Elastomers Market Size, Share, and Growth Forecast 2026 - 2033

Silicone Elastomers Market by Product Type (High Temperature Vulcanized (HTV), Room Temperature Vulcanized (RTV), Liquid Silicone Rubber (LSR)), by Form (Solid Silicone Elastomers, Liquid Silicone Elastomers, Silicone Gels, Silicone Foams, Silicone Sponges, Conductive Silicone Elastomers), Function, Application, End-user, and Regional Analysis, 2026 - 2033

Silicone Elastomers Market Size and Trend Analysis

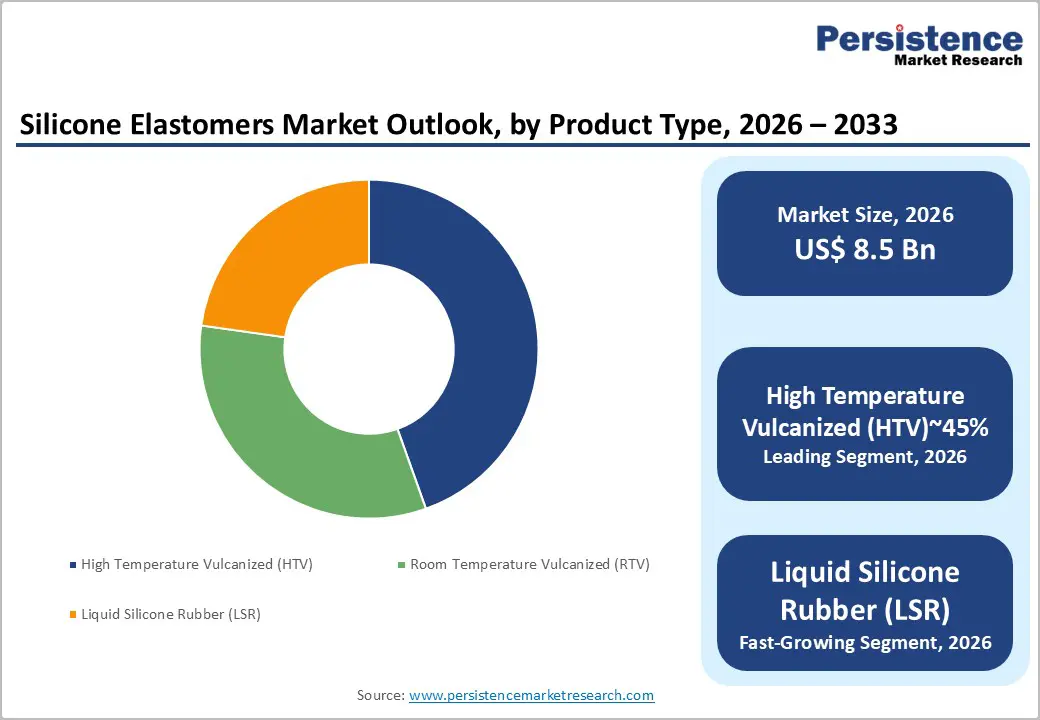

The global Silicone Elastomers market size is likely to be valued at US$8.5 billion in 2026 and is expected to reach US$13.9 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033. The silicone elastomers market is experiencing sustained growth driven by deepening penetration in high-value end-use industries, including automotive, healthcare, and electrical & electronics, where silicone's unique combination of thermal stability, biocompatibility, and electrical insulation properties is irreplaceable.

Key Industry Highlights:

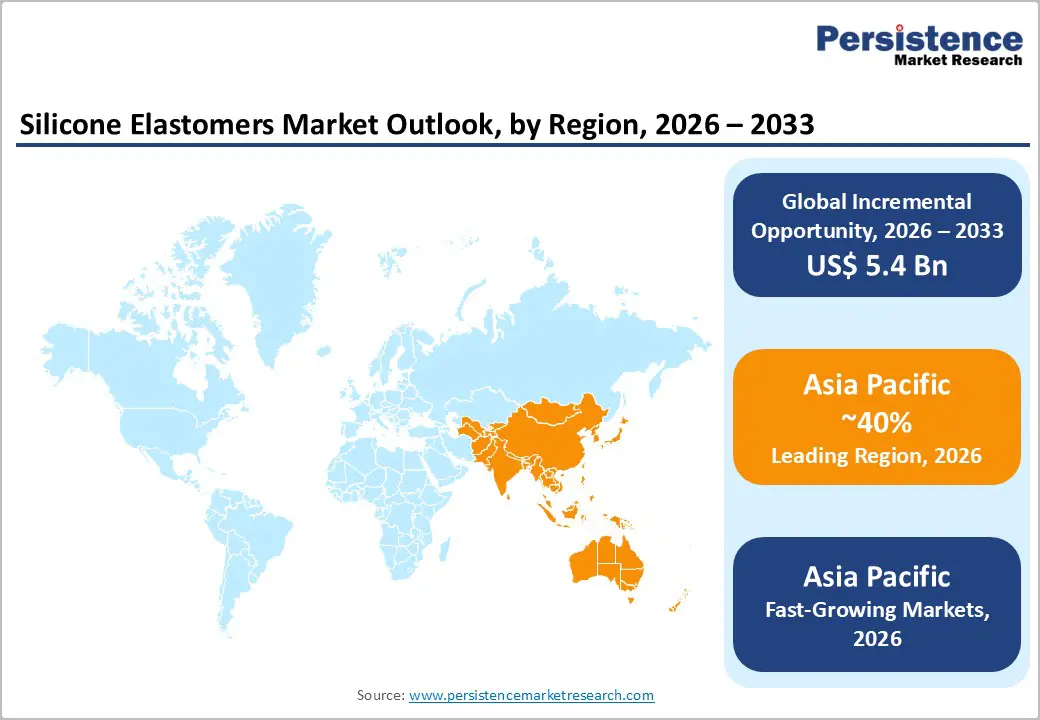

- Leading Region: Asia Pacific leads the global silicone elastomers market holding 40% share, with China as both the world's largest producer and consumer, supported by Japan's technology leadership in high-purity grades and India's rapidly expanding automotive and healthcare sectors.

- Fastest Growing Region: Asia Pacific also registers the fastest growth with a rising CAGR of 8.9%, driven by China's EV manufacturing boom, India's PLI-backed automotive expansion, and accelerating 5G electronics and medical device production across ASEAN countries, including Vietnam and Thailand.

- Dominant Segment: High Temperature Vulcanized (HTV) silicone rubber leads by product type with approximately 45% market share, driven by its widespread adoption in automotive sealing, industrial cable insulation, and electrical applications demanding sustained thermal performance.

- Fastest Growing Segment: Liquid Silicone Rubber (LSR) is the fastest growing product type, propelled by precision injection molding demand from the medical device industry, infant care products, and advanced electronics encapsulation requiring biocompatible, high-clarity silicone formulations.

- Key Opportunity: 5G infrastructure expansion and advanced electronics adoption present a high-growth opportunity for LSR and conductive silicone elastomers in antenna sealing, EMI shielding, and encapsulation, with global 5G connections projected to exceed 5.9 billion by 2027 per the ITU.

Market Dynamics

Drivers - Accelerating Electric Vehicle Production Driving Automotive Silicone Elastomer Demand

The global transition to electric vehicles is generating substantial incremental demand for silicone elastomers in battery pack sealing, thermal management components, high-voltage cable insulation, and motor encapsulation. Silicone elastomers withstand continuous operating temperatures from -60°C to +230°C, making them uniquely suited for EV powertrain environments.

According to the International Energy Agency (IEA), global EV sales exceeded 14 million units in 2023, with the global stock surpassing 40 million vehicles. EV battery packs require up to 4 or 5 kg of silicone-based materials for sealing, thermal interface pads, and gaskets, significantly more than internal combustion engine vehicles. This structural demand shift is a long-term growth engine for Dow Inc., Wacker Chemie AG, and Shin-Etsu Chemical Co., Ltd. across the automotive silicone segment.

Rapid Expansion of the Medical Device and Healthcare Industry

Silicone elastomers, particularly biocompatible Liquid Silicone Rubber (LSR) and RTV grades, are experiencing robust demand growth from the global medical device industry. Their ISO 10993 biocompatibility, resistance to sterilization, and inertness make them the material of choice for implantable devices, surgical instruments, drug-delivery components, and neonatal care products. The U.S. Food and Drug Administration (FDA) has approved silicone as a Class II/III medical device material, underpinning clinical acceptance.

According to the U.S. Department of Commerce, the global medical device market is projected to grow significantly through 2030, driven by aging populations in developed markets and expanding healthcare infrastructure in Asia. NuSil Technology LLC (a subsidiary of Avantor) and Momentive Performance Materials supply specialized medical-grade silicone elastomers addressing this high-value demand segment.

Restraints - High Raw Material Costs and Price Volatility of Silicon Metal

Silicone elastomers are derived from silicon metal, a commodity whose price is highly volatile, driven by energy costs, Chinese export policies, and supply chain disruptions. Silicon metal prices spiked sharply in 2021 following Chinese energy rationing policies that curtailed production in key provinces, with benchmark prices rising over 300% within months, according to Metal Bulletin.

Such cost spikes compress manufacturer margins and create uncertainty in long-term contract pricing, particularly challenging for mid-tier silicone elastomer producers who lack backward integration into siloxane monomer production, limiting their ability to buffer input cost volatility.

Competition from Alternative Elastomers in Cost-Sensitive Applications

In numerous applications, silicone elastomers face direct substitution pressure from lower-cost alternatives, including EPDM, fluoroelastomers (FKM), and thermoplastic elastomers (TPE). Silicone commands a 3–5 times premium over conventional rubber in standard grades, limiting its penetration in cost-sensitive segments such as general-purpose sealing, construction joint fillers, and consumer goods.

The European Rubber Journal notes that EPDM and TPE continue to displace silicone in non-critical automotive and construction sealing applications, restricting market expansion in lower-performance specification tiers and moderating overall volume growth in commodity segments.

Opportunities - Surge in 5G Infrastructure and Advanced Electronics Driving LSR and Conductive Silicone Demand

The global rollout of 5G networks and proliferation of advanced electronics are creating significant opportunities for silicone elastomers in high-frequency cable jacketing, antenna sealing, printed circuit board encapsulation, and thermal interface materials. The International Telecommunication Union (ITU) projects that 5G connections will exceed 5.9 billion globally by 2027. Silicone's low dielectric loss tangent and stable electrical properties across wide temperature ranges make it the preferred encapsulant and insulator for high-frequency electronics.

Additionally, conductive silicone elastomers incorporating carbon black, silver, or nickel fillers are gaining traction for electromagnetic interference (EMI) shielding in smartphones, EVs, and industrial automation systems. Companies like Shin-Etsu Chemical and Elkem ASA are investing in specialty conductive silicone product development to capture this growing demand.

Growing Adoption of LSR in High-Precision Medical and Infant Care Products

Liquid Silicone Rubber (LSR) is the fastest-growing product type within the silicone elastomers market, driven by its precision injection molding capability, superior biocompatibility, and suitability for complex medical components. The global aging population, with the United Nations projecting the number of people aged 65+ to double to 1.6 billion by 2050, is increasing demand for implantable devices, prosthetics, and wearable health monitors, all of which rely on medical-grade LSR.

Additionally, the infant care products market, including pacifiers, feeding nipples, and teethers, exclusively uses food-grade LSR compliant with FDA 21 CFR and EU Regulation No. 10/2011 standards. Manufacturers investing in clean-room LSR injection molding capabilities, such as Momentive and Wacker Chemie, are well-positioned to capture premium margins in this high-growth, regulatory-driven segment.

Category-wise Analysis

By Product Type Insights

High Temperature Vulcanized (HTV) silicone rubber leads the product type segment with an estimated market share of approximately 45%. HTV silicone is the most mature and widely deployed product form, processed via compression, transfer, or extrusion molding and cured at elevated temperatures (typically 150–200°C).

Its dominance stems from widespread adoption in automotive sealing, industrial cable insulation, electrical connector boots, and construction profiles, applications demanding consistent mechanical performance under sustained thermal stress. The automotive sector, which accounts for a major share of silicone elastomer demand, prefers HTV grades for under-hood and powertrain sealing applications. Key HTV suppliers include Shin-Etsu Chemical, Wacker Chemie, and China National Bluestar, which dominate this high-volume segment through competitive pricing and broad product portfolios.

By Form Insights

Solid silicone elastomers represent the leading form segment with an estimated 40% share of the overall silicone elastomers market. Solid forms, including HTV sheet, extruded profiles, and calendered goods, are the most universally applicable format across sealing, insulation, gasket, and vibration-damping applications. Their mechanical robustness, ease of fabrication, and compatibility with standard rubber processing equipment make them the default material form for high-volume industrial and automotive applications.

ASTM International and ISO standards extensively cover the specifications for solid silicone rubber, providing buyers with clear performance benchmarks. Liquid silicone elastomers, while smaller in current volume share, represent the fastest growing form, driven by precision molding demand from the medical and electronics sectors.

By Function Insights

Heat-Resistant function leads the silicone elastomers market by function, with an estimated 30% share. Silicone elastomers' exceptional thermal stability, maintaining performance from -60°C to +230°C continuously, and up to 300°C for short-term exposures, is the primary driver of adoption across automotive, aerospace, and industrial machinery applications.

No other general-purpose elastomer matches silicone's breadth of thermal service range, making heat-resistant functionality the market's defining value proposition. The SAE International notes that silicone is the preferred elastomer for turbocharger hoses, exhaust system components, and oven door seals. As EV powertrains and industrial motors operate at higher sustained temperatures, demand for heat-resistant silicone elastomers continues to expand beyond traditional application boundaries.

By Application Insights

Sealing & gasketing is the leading application segment, capturing an estimated 28% of the silicone elastomers market. Silicone seals and gaskets are indispensable across automotive engines, EV battery packs, aerospace fuel systems, industrial process equipment, and building facades, where environments demand long-term dimensional stability, chemical resistance, and temperature performance that conventional elastomers cannot provide.

The Fluid Sealing Association (FSA) identifies silicone as one of the most versatile sealing materials for extreme-environment applications. As EV manufacturing scales globally and semiconductor fab construction accelerates, the demand for precision-molded silicone seals and gaskets meeting increasingly stringent IP67/IP68 enclosure standards continues to drive this segment's dominant position.

By End-user Insights

Electrical & Electronics leads the silicone elastomers market by end use, with an estimated 27% share. The segment's dominance reflects silicone's unmatched electrical insulation properties, volume resistivity exceeding 10¹? Ω·cm, combined with thermal stability and flame retardancy meeting UL 94 V-0 standards. Applications span high-voltage cable insulation, transformer components, LED lighting seals, consumer electronics encapsulants, and semiconductor test sockets.

The Semiconductor Industry Association (SIA) reports that global semiconductor sales exceeded US$520 billion in 2023, driving consistent demand for electronic-grade silicone elastomers. Automotive & Transportation ranks as the second largest end-use, while Healthcare is the fastest growing end-use segment, driven by medical device and diagnostic equipment expansion.

Regional Insights

North America Silicone Elastomers Market Trends & Analysis

North America represents a mature, innovation-led silicone elastomers market driven by strong demand from automotive (especially EVs), aerospace, healthcare, and semiconductors. Policy support, such as the CHIPS and Science Act and the Inflation Reduction Act, is accelerating investments. High regulatory standards and advanced manufacturing ecosystems sustain premium product demand and technological advancement.

- U.S. Silicone Elastomers Market Size

The U.S. dominates the regional market, accounting for an estimated USD 2.6 billion in 2026, growing at ~7.0% CAGR. Growth is driven by EV production, semiconductor fabs, and stringent U.S. Food and Drug Administration standards, boosting medical-grade silicone adoption.

Europe Silicone Elastomers Market Trends, Drivers & Insights

Europe emphasizes high-performance and compliant silicone elastomers, supported by strong automotive electrification and aerospace manufacturing. Regulatory frameworks such as REACH and the Medical Device Regulation 2017/745 increase demand for traceable, high-quality materials. Renewable energy and sustainability initiatives further drive silicone applications.

- Germany Silicone Elastomers Market Size

Germany leads Europe with an estimated USD 1.2 billion market in 2026. Demand is fueled by EV manufacturing, industrial machinery, and strong OEM presence. Companies like Wacker Chemie AG reinforce innovation and supply chain leadership in silicone elastomers.

- U.K. Silicone Elastomers Market Size

The U.K. silicone elastomers market is valued at approximately USD 450 million in 2026, growing steadily due to aerospace, defense, and healthcare applications. Increasing investment in advanced manufacturing and medical technologies is driving demand for silicone elastomers, particularly for high-specification and specialty applications.

- France Silicone Elastomers Market Size

France accounts for around USD 0.6 billion in 2026, driven by the aerospace and industrial sectors. Strong ties with Airbus supply chains boost demand for flame-retardant and high-performance silicone elastomers used in aviation and defense applications.

Asia Pacific Silicone Elastomers Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing region, supported by expanding electronics, automotive, and industrial manufacturing. Government initiatives, cost advantages, and strong domestic production capabilities drive growth. The region benefits from rapid EV adoption, semiconductor expansion, and increasing healthcare investments.

- China Silicone Elastomers Market Size

China leads globally with an estimated USD 3.2 billion market size in 2026, growing above 7.5% CAGR. Domestic players such as Zhejiang Xinan Chemical Industrial Group Co., Ltd. and China National Bluestar (Group) Co., Ltd. drive large-scale production and exports, supported by industrial policies.

- India Silicone Elastomers Market Size

India’s market is valued at approximately USD 0.6 billion in 2026, expanding at ~8.9% CAGR. Growth is driven by automotive manufacturing under the Production-Linked Incentive Scheme and by increasing healthcare infrastructure investments, both of which are boosting silicon usage.

- Japan Silicone Elastomers Market Size

Japan's market size is around USD 1.0 billion in 2026, driven by high-end applications in electronics and healthcare. Companies like Shin-Etsu Chemical Co., Ltd. and Kaneka Corporation maintain global leadership in advanced silicone technologies.

Competitive Landscape

The silicone elastomers market is moderately consolidated at the premium tier, with Dow Inc., Shin-Etsu Chemical, Wacker Chemie AG, and Momentive Performance Materials collectively commanding the majority of high-value specialty silicone volumes. The commodity HTV and RTV segments are more competitive, with Chinese producers including Zhejiang Xinan and China National Bluestar competing aggressively on price.

Market leaders differentiate through proprietary formulation expertise, regulatory certifications (FDA, MDR, REACH), application engineering support, and long-term supply agreements with OEM customers. R&D investment is concentrated on LSR grades for medical and electronics applications, sustainable silicone chemistries, and thermally conductive formulations for EV thermal management.

Key Market Developments

- March, 2025: Wacker Chemie AG launched a new range of self-adhesive LSR grades for two-component medical device assemblies, enabling direct bonding to thermoplastics without adhesion promoters, targeting wearable health monitors and insulin delivery systems.

- November, 2024: Dow Inc. announced expansion of its SILASTIC silicone elastomer production capacity in Asia Pacific to meet surging demand from EV battery thermal management and 5G electronics encapsulation applications across China, South Korea, and Japan.

- July, 2024: Shin-Etsu Chemical Co., Ltd. introduced a new series of thermally conductive liquid silicone rubber (TC-LSR) compounds for EV battery pack thermal interface applications, offering enhanced heat dissipation performance with improved processability in high-speed injection molding.

Companies Covered in Silicone Elastomers Market

- Dow Inc.

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- China National Bluestar (Group) Co., Ltd.

- Elkem ASA

- KCC Corporation

- Mesgo S.p.A.

- Reiss Manufacturing Inc.

- Specialty Silicone Products, Inc.

- Stockwell Elastomerics

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- NuSil Technology LLC

- Kaneka Corporation

- Cabot Corporation

- Rogers Corporation

- Trelleborg AB

- Primasil Silicones Ltd.

Frequently Asked Questions

The global silicone elastomers market is estimated to be valued at US$ 8.5 Billion in 2026, and it is projected to reach US$ 13.9 Billion by 2033, growing at a CAGR of 7.3% during the forecast period. Between 2020 and 2025, the market recorded a historical CAGR of 6.9%, reflecting sustained demand from automotive, electrical & electronics, and healthcare sectors.

The primary drivers are the accelerating global EV production surge, with IEA reporting over 14 million EV sales in 2023, creating demand for battery sealing and thermal management silicones, and the expanding medical device industry requiring biocompatible LSR for implantable and diagnostic applications validated by FDA and EU MDR regulatory frameworks.

High Temperature Vulcanized (HTV) silicone rubber leads the market by product type with an estimated 45% share. Its dominance is attributed to widespread adoption in automotive sealing, cable insulation, and industrial gaskets that require sustained performance at temperatures from -60°C to +230°C, a thermal range unmatched by conventional elastomers.

Asia Pacific leads the global silicone elastomers market, accounting for the largest share of production and consumption. China drives the region's dominance as the world's largest silicone producer, while Japan's Shin-Etsu Chemical and Kaneka Corporation lead in high-performance grades. India's PLI-backed manufacturing expansion further reinforces Asia Pacific's leadership position.

The fastest growing opportunity lies in the 5G infrastructure and advanced electronics segments, where LSR and conductive silicone elastomers are in high demand for antenna sealing, EMI shielding, and precision encapsulation. With the ITU projecting 5.9 billion global 5G connections by 2027, and semiconductor fab investments accelerating under the CHIPS Act, the demand for specialty silicone elastomers in electronics is set for significant expansion.

The leading global companies include Dow Inc., Wacker Chemie AG, Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd., China National Bluestar (Group) Co., Ltd., Elkem ASA, KCC Corporation, NuSil Technology LLC, Zhejiang Xinan Chemical Industrial Group, and Kaneka Corporation, among other regional and specialty silicone manufacturers.