- Smart Packaging

- Thermal Transfer Ribbon Market

Thermal Transfer Ribbon Market Size, Share, and Growth Forecast, 2026 - 2033

Thermal Transfer Ribbon Market by Product Type (Wax Ribbon, Wax-Resin Ribbon, Others), Printing Head (Flat Head, Near Edge), Application, End-user Industry, and Regional Analysis for 2026 - 2033

Thermal Transfer Ribbon Market Size and Trends Analysis

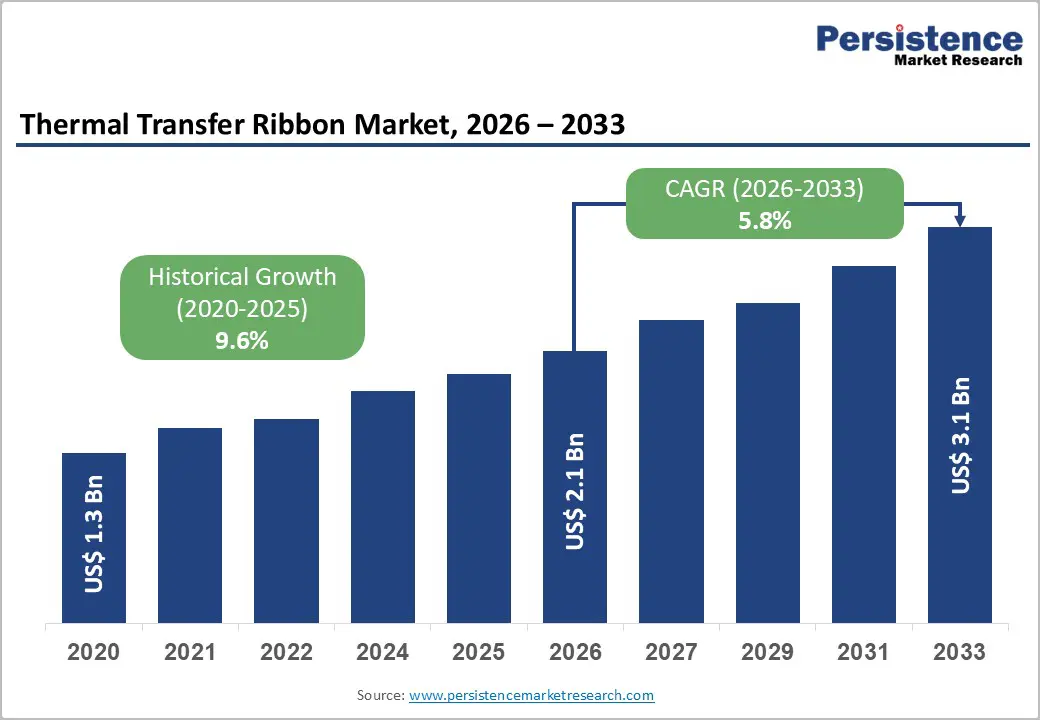

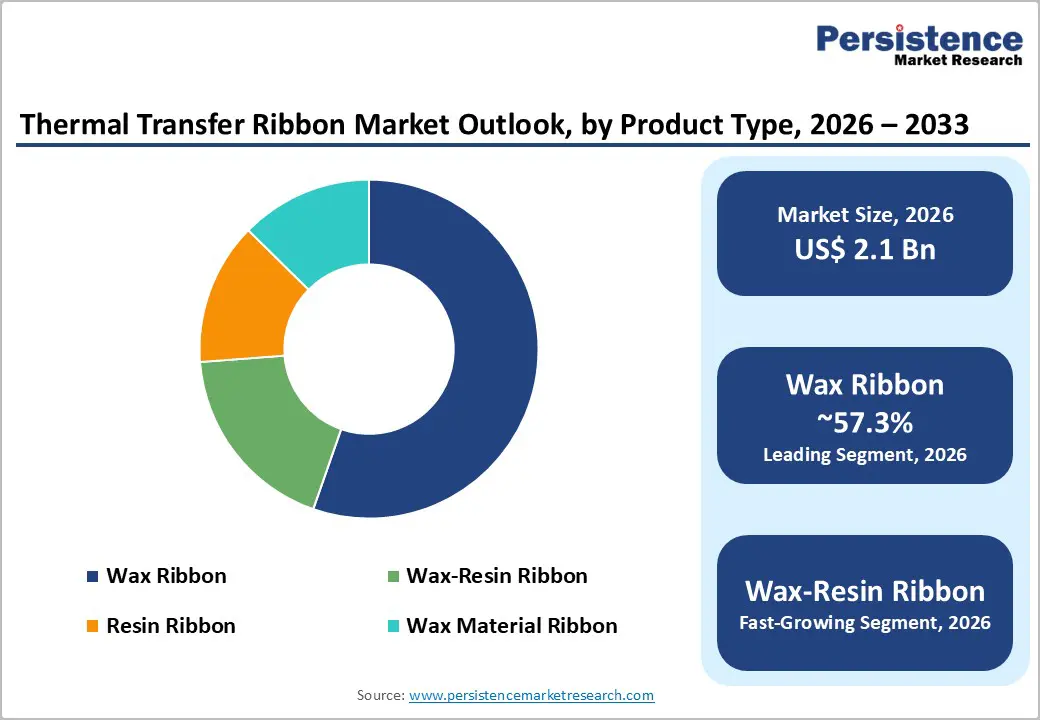

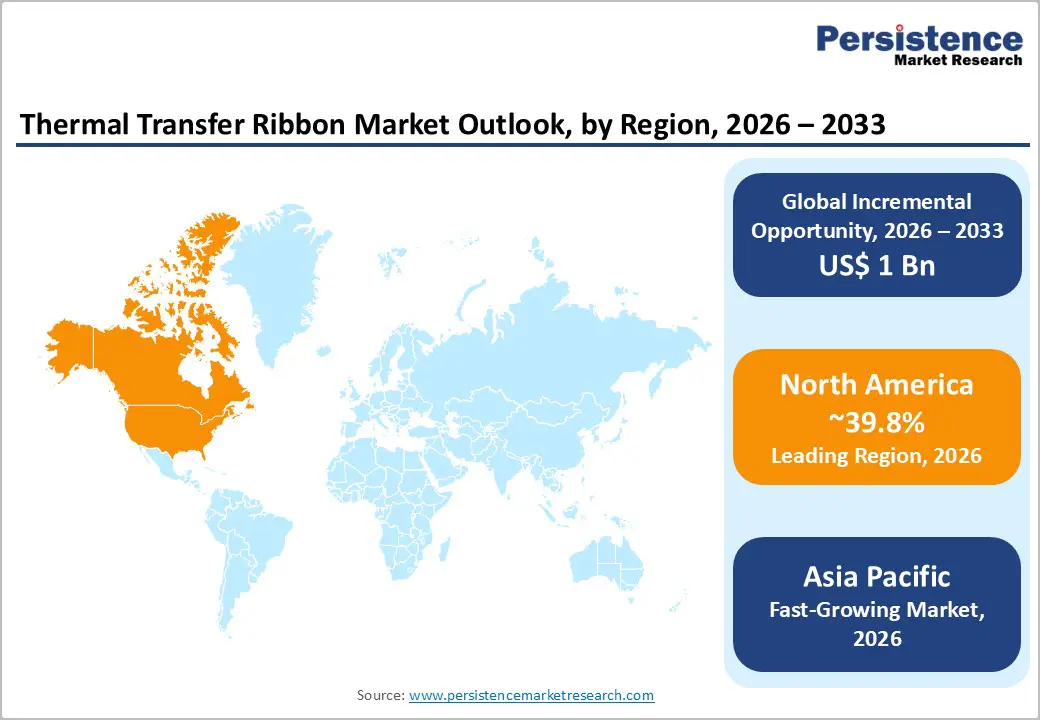

The global thermal transfer ribbon market size is likely to be valued at US$2.1 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033, driven by rising labeling volumes in global logistics and e-commerce operations, stronger regulatory requirements for durable product identification, and the rapid adoption of automated printing systems across manufacturing and supply chain operations.

Thermal transfer technology enables long-lasting barcode and product labels, making it essential for traceability across industries such as healthcare, chemicals, retail, and transportation. Increasing adoption of wax-resin and resin ribbons for high-durability applications is improving product performance and expanding industrial use cases.

Key Industry Highlights

- Leading Region: North America is projected to hold the leading position in the market, accounting for approximately 39.8% of market share, supported by advanced logistics infrastructure, strong adoption of automated warehouse systems, and widespread use of barcode labeling across e-commerce, healthcare, and retail supply chains.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, driven by rapid industrialization, expanding manufacturing activity, and the growth of e-commerce logistics networks in China, India, and Southeast Asia.

- Investment Plans: Leading labeling technology companies and logistics operators are investing heavily in automated printing systems and supply chain digitization. Expansion of automated fulfillment centers and smart manufacturing facilities is increasing the installed base of thermal transfer printers, strengthening long-term demand for ribbon consumables across industrial and logistics applications.

- Dominant Product Type: Wax ribbons dominate the market with an anticipated share of approximately 57.3%, primarily due to their cost-effectiveness and suitability for high-volume paper label printing used in shipping labels, retail shelf tags, and warehouse inventory management.

- Leading Printing Head: Desktop printers are estimated to lead the market, accounting for approximately 42.1% of market share, supported by their widespread use in retail stores, offices, and small logistics operations for barcode labels, price tags, and inventory tracking.

| Key Insights | Details |

|---|---|

| Thermal Transfer Ribbon Market Size (2026E) | US$2.1 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of E-commerce and Logistics Infrastructure

Rapid growth in global e-commerce shipments is significantly increasing demand for barcode labeling and package identification. Logistics companies require high-quality labels that withstand handling, temperature changes, and friction during transportation. Thermal transfer ribbons provide the durability and print clarity required for high-volume parcel operations. Warehouses now process thousands of labels per hour using automated print-and-apply systems. Supply chain organizations are increasingly deploying thermal transfer printers integrated with warehouse management systems, leading to higher ribbon consumption per facility. The expansion of cross-border trade, omnichannel retail distribution, and fulfillment centers continues to increase label printing volumes. As a result, transportation and logistics remain the largest end-user segment, directly supporting sustained demand for ribbon consumables across distribution networks worldwide.

Rising Regulatory Requirements for Product Traceability

Regulatory frameworks across healthcare, chemicals, and food industries increasingly mandate long-term traceability and durable labeling. Pharmaceutical serialization programs require scannable barcodes and readable batch identification throughout product lifecycles. Chemical packaging regulations require hazard symbols and information labels that remain legible under exposure to moisture, abrasion, and solvents. Thermal transfer ribbons, particularly resin-based formulations, ensure label durability for these regulated applications. In medical environments, hospitals and laboratories rely on thermal transfer printing for patient identification wristbands, specimen labels, and medical device tracking. Compliance requirements have increased demand for validated printing systems that test printers, ribbons, and substrates together. This regulatory environment supports premium ribbon grades and increases the adoption of higher-performance formulations in compliance-driven sectors.

Advancements in Ribbon Formulation and Printing Technology

Technological developments in ribbon chemistry have improved print durability, substrate compatibility, and energy efficiency. Modern wax-resin and resin formulations enable printing on synthetic films, coated papers, textiles, and specialty materials. These advancements reduce printhead wear and enhance barcode readability across challenging environments. Industrial production lines and flexible packaging operations increasingly require ribbons that maintain high-speed printing accuracy. Printer manufacturers continue to optimize ribbon performance through integrated validation programs. Improved ribbon coatings allow lower transfer temperatures and higher printing speeds, reducing operational costs for manufacturers. Such technological innovation enables thermal transfer printing to expand beyond conventional labeling into packaging coding, asset tracking, and industrial identification, thereby strengthening the long-term growth potential of the market.

Barrier Analysis - Raw Material Price Volatility

Thermal transfer ribbons rely on polyester film bases and specialized wax and resin coatings derived from petrochemical feedstocks. Fluctuations in global oil prices influence the cost of these materials, creating pricing instability for ribbon manufacturers. Periodic increases in polyester film costs can significantly raise production expenses, forcing suppliers to adjust pricing strategies. Procurement contracts with industrial buyers often restrict rapid price adjustments, which can compress supplier margins. Raw-material volatility, therefore, creates financial risk across the supply chain and can delay investment in new production capacity.

Printer Compatibility and Equipment Fragmentation

The installed base of thermal transfer printers includes multiple architectures, primarily flat-head and near-edge systems. Each configuration requires specific ribbon formulations and dimensions, limiting interchangeability. Organizations deploying new labeling solutions must conduct compatibility testing between printers, ribbons, and substrates before implementation. This validation process increases procurement complexity and slows supplier switching. Compatibility constraints also create inventory management challenges because distributors must stock multiple ribbon specifications to support diverse printer fleets.

Opportunity Analysis - Growth of Flexible Packaging and Coding Applications

Flexible packaging has become one of the fastest-expanding segments in the global packaging industry. Consumer goods companies increasingly use thermal transfer overprinting to apply date codes, batch numbers, and regulatory information on packaging films. Near-edge thermal transfer printers for high-speed packaging lines require specialized ribbon formulations that can print on polymer substrates. This shift toward flexible packaging opens new opportunities for high-performance resin ribbons and color thermal transfer products. Suppliers that develop film-optimized ribbon systems and establish partnerships with packaging converters can capture higher-margin applications in this growing segment.

Sustainable Labeling and Recyclable Material Innovation

Environmental sustainability initiatives across the retail and consumer goods industries are driving demand for recyclable and environmentally responsible packaging materials. Labeling systems must be compatible with recycling processes and minimize environmental impact. Manufacturers are investing in low-emission ribbon coatings, recyclable polyester carriers, and reduced-waste manufacturing processes. Sustainable ribbon products provide a competitive advantage in procurement processes where companies prioritize environmental certifications and lifecycle transparency. The growing emphasis on circular packaging systems presents opportunities for ribbon suppliers to deliver validated solutions that support recyclable label structures.

Emerging Market Expansion

Emerging economies across Asia, Latin America, and the Middle East are rapidly modernizing logistics and manufacturing infrastructure. Growth of regional e-commerce platforms, retail chains, and export manufacturing is increasing the need for barcode labeling and product traceability. As companies adopt automated warehousing and inventory tracking systems, thermal transfer printers become standard equipment in supply chains. Rising industrialization and manufacturing exports create consistent demand for durable product labels. Expansion into these developing markets offers ribbon manufacturers opportunities to increase global distribution and establish new regional production facilities.

Category-wise Analysis

Product Type Insights

Wax ribbons represent the largest volume segment and are anticipated to account for approximately 57.3% of the market share during the forecast period in 2026, primarily due to their cost-effective performance for paper label printing. These ribbons are widely used for shipping labels, retail shelf tags, warehouse inventory labels, and courier tracking labels printed on uncoated or coated paper substrates. Wax ribbons offer adequate durability for short-term labeling applications while maintaining low printing temperatures, which helps reduce printer head wear and energy consumption. Their affordability makes them the preferred choice for high-volume operations in logistics centers, e-commerce fulfillment warehouses, and retail distribution facilities. Major logistics and retail operators, including companies managing large fulfillment networks, use wax ribbons extensively for barcode labels and shipping documentation where label longevity requirements are moderate. As paper labels remain widely used across global supply chains, wax ribbons continue to maintain a dominant share of total ribbon consumption.

Resin ribbons represent the fastest-growing product segment in the Thermal Transfer Ribbon market, driven by their superior resistance to abrasion, chemicals, moisture, and high temperatures. These ribbons are essential for demanding industrial environments, including chemical manufacturing, electronics production, and automotive component labeling. Resin ribbons enable high-resolution printing on synthetic films, including polypropylene, polyester, and vinyl materials used in long-life asset tags and durable industrial labels. For example, electronics manufacturers use resin ribbons to produce circuit board identification labels that withstand soldering processes, while automotive companies require durable barcode labels for engine components exposed to oil and heat. Their durability also ensures barcode readability in outdoor logistics operations and harsh manufacturing environments. The expansion of regulatory labeling requirements and traceability systems is increasing demand for resin ribbons in healthcare and pharmaceutical packaging. As manufacturers shift toward longer-lasting labels and high-performance substrates, resin ribbons are expected to experience the strongest revenue growth among all ribbon types.

Application Insights

Desktop printers represent the leading application segment and are anticipated to account for approximately 42.1% of the market share in 2026, largely due to their widespread use in office environments, retail stores, and small logistics operations. These printers are compact, cost-efficient, and capable of producing high-quality barcode labels for inventory management and shipping documentation. Businesses across the retail and service industries rely on desktop thermal transfer printers for daily labeling tasks, including price tags, product identification labels, and order tracking. For example, supermarkets, pharmacies, and small distribution hubs frequently deploy desktop printers for shelf labeling and product tagging. The high installed base of these printers globally creates consistent demand for ribbon consumables, making the desktop printer segment a major revenue contributor for ribbon manufacturers and distributors.

Industrial and mobile printing systems are the fastest-growing application categories in the Thermal Transfer Ribbon market, driven by expanding automation across manufacturing, warehousing, and logistics. Industrial printers are increasingly used in high-volume production environments such as automotive assembly plants, food processing facilities, and electronics manufacturing lines, where continuous printing of barcode labels, compliance labels, and packaging identifiers is required. These systems often integrate with enterprise resource planning (ERP) and warehouse management systems (WMS), enabling automated product identification and real-time tracking. Mobile printers are gaining rapid adoption in field operations, including last-mile delivery services, warehouse inspections, asset tracking, and utility maintenance work. For instance, courier companies use mobile printers to generate delivery receipts and shipping labels on-site, improving workflow efficiency and reducing processing time. The rapid expansion of e-commerce logistics networks and mobile workforce management systems is expected to significantly increase ribbon demand in these emerging application segments.

Regional Insights

North America Thermal Transfer Ribbon Market Trends - E-commerce Fulfillment Automation and Regulatory Healthcare Labeling Driving Ribbon Demand

North America is anticipated to account for approximately 39.8% of the market share in 2026. The region benefits from a highly developed logistics ecosystem, widespread adoption of automated labeling technologies, and strong demand for durable barcode identification systems across transportation, healthcare, retail, and manufacturing industries. The U.S. represents the dominant market within the region, supported by its large e-commerce sector, extensive warehouse infrastructure, and high penetration of barcode-based inventory management systems. One of the primary drivers of market growth in North America is the rapid expansion of automated e-commerce fulfillment networks.

Major logistics and retail companies, including Amazon, Walmart, and FedEx, operate highly automated distribution centers that require millions of barcode labels every day. Thermal transfer printing systems are integrated with warehouse management software and robotics systems to generate shipping labels, tracking codes, and inventory tags in real time. For example, Amazon’s continued investment in next-generation robotics and automated fulfillment facilities across the U.S. has expanded the installed base of industrial thermal transfer printers used for parcel labeling and package tracking. This large-scale infrastructure significantly increases recurring demand for ribbon consumables used in high-volume printing operations.

Another important factor supporting the regional market is the strict regulatory framework governing healthcare and pharmaceutical labeling. Institutions such as hospitals, diagnostic laboratories, and pharmaceutical manufacturers must comply with product identification standards established by organizations such as the U.S. Food and Drug Administration and the GS1 global barcode standards body. Regulations requiring unique device identification (UDI) for medical devices and serialized pharmaceutical packaging have significantly increased the need for durable and scannable labels.

Thermal transfer ribbons are widely used to produce high-resolution barcodes and compliance labels that remain readable throughout sterilization, storage, and transportation processes. Leading printer and labeling technology providers such as Zebra Technologies and Honeywell International continue to introduce advanced industrial printing platforms designed for automated supply chain environments. In 2024, Zebra Technologies expanded its portfolio of industrial barcode printers and intelligent labeling systems designed for high-volume warehouse operations. These innovations support improved printing durability, ribbon efficiency, and remote printer management capabilities.

Europe Thermal Transfer Ribbon Market Trends - Industrial Manufacturing Traceability and Sustainability-Focused Labeling Solutions

Europe represents a technologically advanced and mature market for thermal transfer ribbons, supported by strong industrial manufacturing, well-established logistics networks, and strict regulatory requirements governing product identification. Germany is the largest market within Europe, largely due to its extensive industrial ecosystem encompassing automotive production, machinery manufacturing, and chemical processing. Companies such as Volkswagen AG, BMW Group, and Siemens AG require reliable labeling systems for component identification, product traceability, and logistics management across complex manufacturing operations. Automotive assembly lines rely heavily on durable labels capable of withstanding oils, high temperatures, and mechanical stress. As a result, high-performance wax-resin and resin ribbons are widely used for printing component tracking labels and compliance identification tags.

The U.K. maintains a strong demand driven by large retail supply chains and expanding e-commerce logistics networks. Retailers and distribution companies depend on barcode labels for warehouse inventory management, order fulfillment, and shelf labeling. For example, major British retail organizations, including Tesco and Sainsbury's, operate large automated distribution centers that require continuous label printing for product identification and shipment tracking. The expansion of parcel delivery networks managed by logistics providers such as Royal Mail has also increased the demand for thermal transfer labeling systems used for package sorting and routing.

Packaging producers and labeling solution providers are focusing on environmentally responsible materials and manufacturing processes. Companies such as ARMOR-IIMAK, a major global thermal transfer ribbon manufacturer headquartered in France, have introduced lower-emission coating technologies and eco-designed ribbon formulations aimed at reducing environmental impact. These innovations align with broader European Union sustainability policies targeting waste reduction and circular packaging systems.

Asia Pacific Thermal Transfer Ribbon Market Trends - Manufacturing Expansion and High-Volume E-commerce Logistics Fueling Market Growth

Asia Pacific represents the fastest-growing regional market for thermal transfer ribbons, driven by rapid industrialization, large-scale manufacturing activity, and expanding e-commerce logistics networks. China represents the largest market in the region due to its position as a global manufacturing hub and leading exporter of consumer electronics, machinery, and packaged goods. Manufacturing companies rely heavily on barcode labels for product identification, shipping documentation, and inventory tracking throughout large production facilities. Major Chinese logistics and e-commerce companies such as Alibaba Group and JD.com operate vast fulfillment networks that process millions of parcels daily. These operations depend on high-volume label printing systems integrated with automated sorting and warehouse management technologies, significantly increasing demand for thermal transfer ribbons used in shipping labels and tracking documentation. Japan plays a significant role in the regional market due to its advanced electronics and automotive manufacturing sectors. Companies such as Toyota Motor Corporation and Sony Group Corporation require durable product identification labels capable of withstanding high temperatures, chemical exposure, and mechanical stress during production processes. These requirements drive strong demand for resin-based ribbons used to print durable labels on polyester and polypropylene substrates commonly applied to electronic components and industrial equipment.

India is experiencing rapid growth in logistics infrastructure and warehouse automation. The expansion of organized retail and the growth of domestic e-commerce platforms have increased demand for barcode labeling technologies across distribution networks. Logistics companies, including Delhivery and Blue Dart Express, have significantly expanded automated sorting hubs and parcel distribution centers across the country. These facilities rely on thermal transfer printers to generate shipping labels, routing tags, and inventory identifiers, creating sustained demand for ribbon consumables. Investment in regional distribution networks and manufacturing facilities by ribbon suppliers is improving product availability throughout Asia Pacific. The rapid expansion of industrial production, export-oriented manufacturing, and e-commerce logistics infrastructure will continue to drive strong growth in thermal transfer ribbon demand across the region during the forecast period.

Competitive Landscape

The global thermal transfer ribbon market demonstrates moderate concentration, with several global suppliers controlling significant portions of industry revenue while numerous regional manufacturers serve local markets. Major companies compete through product innovation, printer compatibility, and supply chain partnerships with labeling system providers. Premium segments such as resin ribbons and specialty formulations are dominated by technologically advanced manufacturers, while commodity wax ribbons face stronger price competition.

Leading manufacturers focus on product innovation, compatibility validation with printer systems, global distribution expansion, and development of high-performance ribbon formulations. Companies are investing in advanced coating technologies and sustainable materials to strengthen differentiation and capture premium industrial labeling applications.

Key Industry Developments:

- In December 2025, ARMOR-IIMAK announced the launch of its AWR XL thermal transfer ribbon, a new wax ribbon designed with an ultra-thin PET film and a 100% solvent-free formulation. The innovation enables longer ribbon rolls that reduce roll changes and improve printer uptime, while also lowering plastic waste and logistics costs, supporting the company’s sustainability strategy.

Companies Covered in Thermal Transfer Ribbon Market

- Zebra Technologies Corporation

- Avery Dennison Corporation

- Dai Nippon Printing Co., Ltd.

- ARMOR-IIMAK

- Ricoh Company, Ltd.

- Honeywell International Inc.

- SATO Holdings Corporation

- TSC Auto ID Technology Co., Ltd.

- ITW Thermal Films

- Dynic Corporation

- Brady Corporation

- Toshiba Tec Corporation

- General Data Company, Inc.

- Fujicopian Co., Ltd.

- Hangzhou Todaytec Digital Technology Co., Ltd.

- Inkstar Office Automation Co., Ltd.

- Sony Chemicals & Information Device Corporation

- Koehler Paper Group

Frequently Asked Questions

The global thermal transfer ribbon market is estimated to be valued at US$2.1 billion in 2026.

The thermal transfer ribbon market is projected to reach US$3.1 billion by 2033.

Key market trends include the expansion of e-commerce and warehouse automation, increasing use of resin-based ribbons for durable industrial labeling, adoption of mobile printing solutions for field operations, and growing demand for high-performance labels in regulated industries such as healthcare and chemicals. Sustainability initiatives in packaging and labeling materials are also influencing ribbon formulation innovations.

Wax ribbons represent the leading segment, accounting for approximately 57.3% of market share, primarily due to their cost-effectiveness and suitability for high-volume paper label printing used in logistics, retail shelf labeling, and warehouse inventory tracking.

The thermal transfer ribbon market is expected to grow at a CAGR of 5.8% between 2026 and 2033.

Major companies with strong product portfolios include Zebra Technologies Corporation, Avery Dennison Corporation, Dai Nippon Printing Co., Ltd. (DNP), ARMOR-IIMAK, and SATO Holdings Corporation.