- Healthcare Services

- Telecardiology Market

Telecardiology Market Size, Share, and Growth Forecast 2026 - 2033

Telecardiology Market by Offering (Products, Services), by Modality (Store-And-Forward, Real-Time), by Application (Remote Patient Monitoring, Teleconsultation), by End-user (Healthcare Facilities, Homecare), and Regional Analysis, 2026 - 2033

Telecardiology Market Size and Trends Analysis

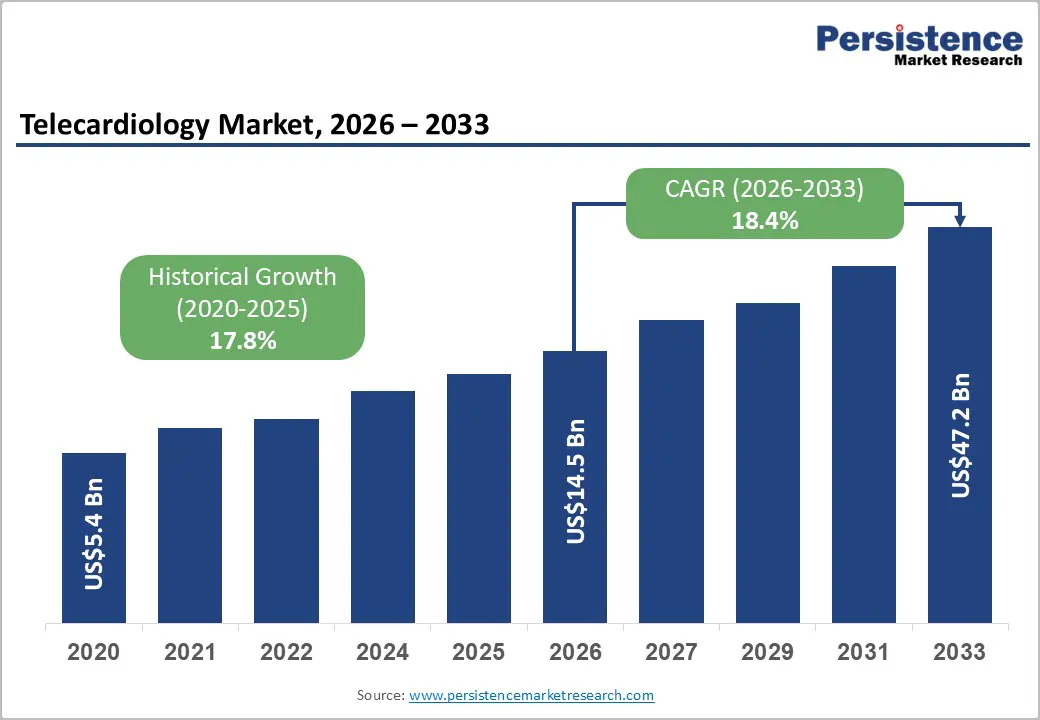

The global telecardiology market size is likely to be valued at US$14.5 billion in 2026 and is expected to reach US$47.2 billion by 2033, growing at a CAGR of 18.4% during the forecast period from 2026 to 2033, driven by the rising demand for quick cardiac diagnosis and continuous monitoring outside traditional hospital settings. Increasing pressure on hospitals to manage large volumes of heart patients is another key market driver.

Key Industry Highlights:

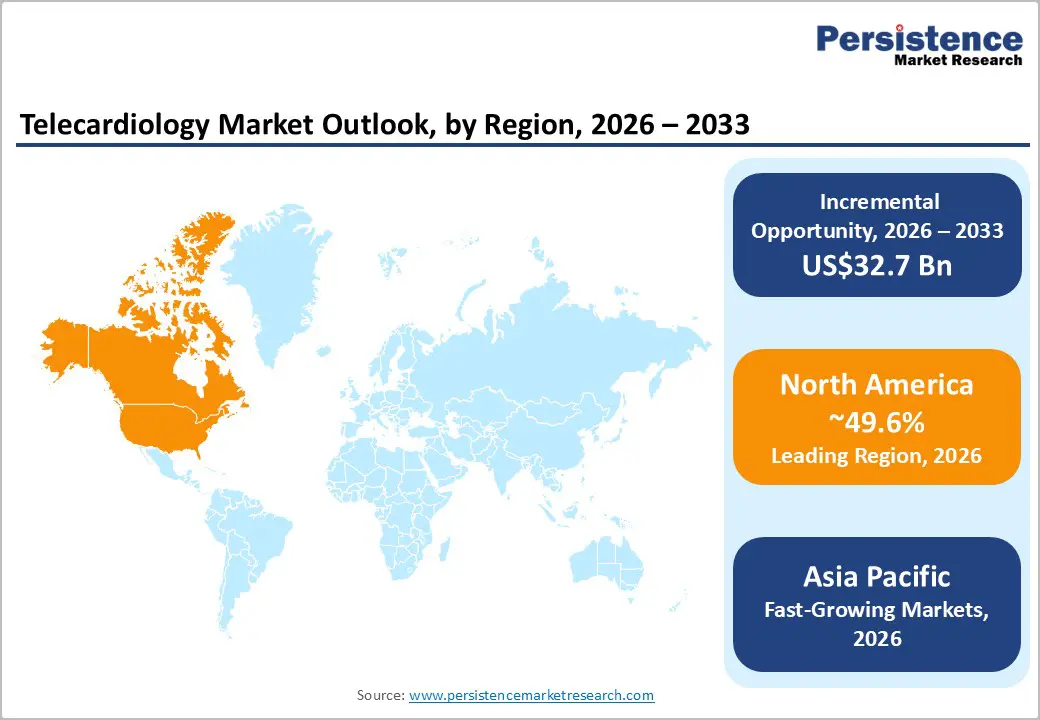

- Leading Region: North America, with about 49.6% share in 2026, owing to reimbursement support for remote cardiac monitoring.

- Fast-growing Region: Asia Pacific, backed by rising cardiovascular disease burden and expansion of digital health infrastructure.

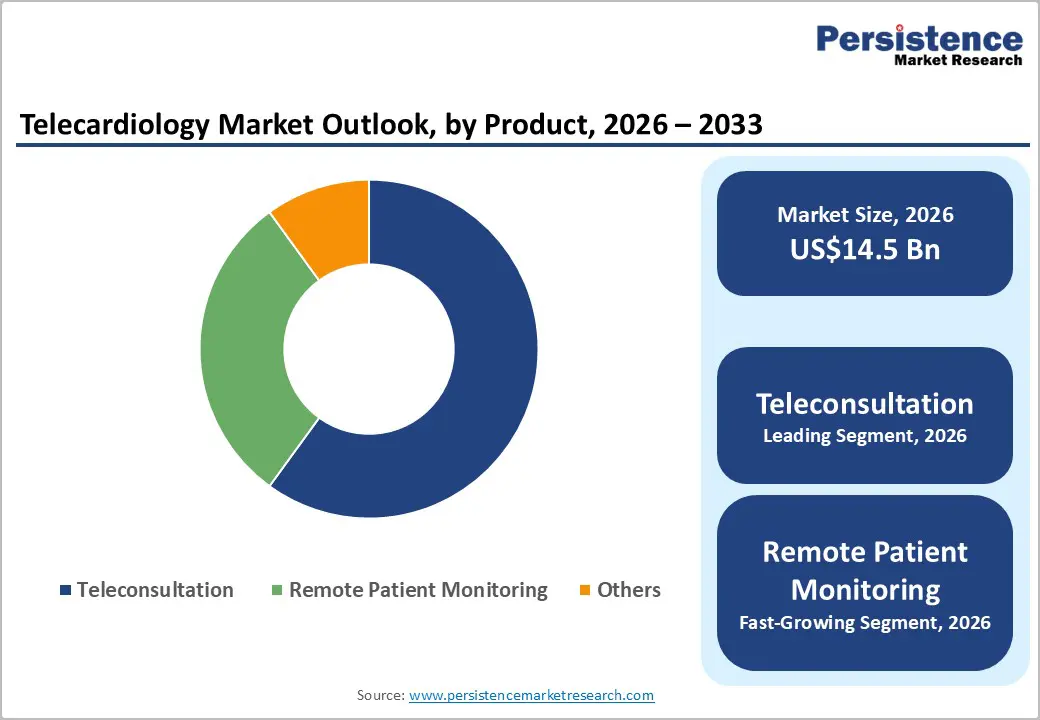

- Leading Offering: Services, with approximately 48.2% share in 2026, as hospitals prefer outsourced ECG interpretation, remote monitoring, and 24/7 cardiologist support rather than investing in standalone infrastructure.

- Dominant Application: Teleconsultation, nearly 40.1% in 2026, as it allows for immediate access to cardiologists for diagnosis, follow-ups, and emergency decision-making.

- Latest Project: In January 2026, the Interreg NEXT MED Program launched the SALAM telecardiology project in collaboration with healthcare and academic partners from Italy, Spain, Lebanon, and Jordan. The initiative aims to improve access to cardiac care in underserved Mediterranean regions through telecardiology platforms, mobile medical units, and hospital hubs in Beirut and Irbid.

DRO Analysis

Driver - Increasing Burden of Heart-related Disorders

The rising incidence of cardiovascular disease is a key growth driver for telecardiology worldwide. Healthcare systems are under constant pressure to monitor large cardiac patient populations outside hospitals. According to the World Health Organization (WHO), cardiovascular diseases caused nearly 19.8 million deaths globally in 2022, with heart attacks and strokes accounting for most fatalities. Low- and middle-income countries are witnessing particularly high cardiac mortality rates, creating demand for swift diagnosis and continuous monitoring solutions.

Telecardiology is increasingly being used for remote ECG interpretation, chronic heart disease monitoring, and early emergency intervention. Companies are now developing IoT-enabled and AI-assisted cardiac monitoring systems that allow physicians to track ECG, blood pressure, and oxygen levels in real time. For example, Heartnet India launched its ASAAN telecardiology platform to improve cardiac diagnostics in Tier II, Tier III, and rural regions through connected cardiac screening systems.

Surging Demand for Convenient and Remote Cardiac Care Services

Rising demand for accessible healthcare services is boosting telecardiology adoption, especially in rural and underserved regions where cardiologists remain scarce. Governments and healthcare providers are increasingly using telemedicine infrastructure to reduce travel burdens, minimize hospital overcrowding, and improve access to specialists. India’s Ministry of Health and Family Welfare has expanded digital healthcare delivery through the eSanjeevani platform, enabling remote consultations across thousands of health and wellness centers.

Several state-led initiatives now include telecardiology services as part of broad digital healthcare programs. In West Bengal, for instance, the Swasthya Ingit telemedicine initiative surpassed 7 crore (70 million) consultations and extended into cardiology, helping patients in remote regions access cardiac specialists without visiting urban hospitals. Also, Maharashtra’s public telemedicine network continues expanding specialist consultations across district and rural hospitals to improve healthcare reach in remote communities.

Restraint - Data Protection Risks and Infrastructure Gaps

Concerns around patient data privacy and the requirement for highly secure digital infrastructure continue to limit telecardiology expansion. It is especially evident when handling sensitive ECG data, imaging records, and real-time patient monitoring feeds. Cardiac data is long-term and highly identifiable, making it a prime target for cyberattacks. The World Health Organization (WHO) has highlighted cybersecurity as a key barrier to the adoption of digital health. It has been stated that weak safeguards in telemedicine systems can expose patient records and disrupt care delivery.

In 2024, for instance, a ransomware attack on Ascension Health disrupted clinical operations across multiple hospitals, underlining the vulnerability of connected health systems. Various low-resource regions also lack stable internet, cloud infrastructure, and secure data storage systems. This makes real-time telecardiology deployment unreliable and limits its expandability beyond urban centers.

Opportunity - Expansion of Smartphone-linked Cardiac Monitoring Platforms

Increasing use of smartphone-connected cardiac monitoring apps is creating new opportunities in telecardiology by enabling real-time ECG transmission, remote diagnosis, and continuous patient engagement outside hospitals. Companies are now developing portable and wearable ECG systems that connect directly to mobile applications, enabling physicians to receive live cardiac data from patients at home or in rural areas. In 2025, for example, Octagos Health launched the OctaLink mobile platform to provide clinicians with instant access to real-time cardiac monitoring alerts and remote patient data through smartphones.

ASUS, on the other hand, received Thailand FDA certification for its VivoWatch ECG application. It enables ECG monitoring through wearable devices integrated with mobile systems. The increasing consumer adoption of smartwatches and portable ECG devices is expected to accelerate this trend, particularly in regions with limited access to cardiologists.

Emergence of Artificial Intelligence-Enabled Cardiac Diagnostics

AI-based ECG interpretation and cardiac imaging analysis are creating novel growth opportunities in telecardiology by improving diagnostic speed and identifying abnormalities that are often missed during manual review. Healthcare providers are continually adopting AI tools that accurately detect subtle heart conditions from ECGs, CT scans, and cardiac MRI images. In 2025, for example, researchers presented an AI model at the American College of Cardiology scientific session. It showed high accuracy in detecting blocked coronary arteries using ECG readings, comparable to troponin testing in emergency settings.

The opportunity is expanding beyond arrhythmia detection into structural heart disease screening and predictive diagnostics. Tempus AI received Food and Drug Administration (FDA) clearance in 2025 for its ECG-Low EF software. It uses AI to identify patients at risk of low left ventricular ejection fraction from ECG data. Recent research presented by the American Heart Association also demonstrated that smartwatch-based AI algorithms could detect structural heart disease using single-lead ECG sensors, pointing to the future potential of AI-supported remote cardiac diagnostics.

Category-wise Analysis

Offering Insights

The services segment is set to lead with nearly 48.2% of the market share in 2026, as hospitals and healthcare systems mainly prefer end-to-end cardiac care support instead of purchasing standalone devices. Modern telecardiology services now include remote ECG interpretation, teleconsultation, AI-assisted diagnostics, physician reporting, cloud data management, and continuous patient monitoring, all delivered under subscription-based models. This approach reduces the burden on hospitals that lack dedicated cardiologists or 24/7 cardiac monitoring teams.

Products are anticipated to be the fastest-growing segment in 2026, spurred by increasing adoption of wearable ECG monitors, mobile cardiac telemetry systems, AI-enabled diagnostic tools, and connected biosensors designed for continuous cardiac monitoring. Healthcare providers are continually investing in portable and home-based cardiac devices that enable early diagnosis and long-term monitoring without the need for repeated hospital visits.

Application Insights

The teleconsultation segment is projected to dominate, with approximately 40.1% share in 2026, as it addresses one of the most prominent challenges in cardiac care: limited access to cardiologists, especially in rural and underserved regions. Hospitals and governments are using virtual cardiac consultations to reduce patient travel time, accelerate access to specialists, and support quick decision-making during emergencies. Teleconsultation is particularly valuable for follow-up care, medication management, post-surgical monitoring, and interpretation of ECG and imaging reports. The ongoing expansion of telemedicine infrastructure after the pandemic significantly strengthened the adoption of remote cardiology consultations.

The remote patient monitoring segment is expected to remain in second place. This is owing to a shift in healthcare systems toward preventive and continuous cardiac care rather than episodic treatment. Cardiovascular diseases require long-term monitoring of heart rhythm, blood pressure, oxygen levels, and other vital signs. This makes remote monitoring highly valuable for reducing hospital readmissions and identifying complications early. Developments in wearable sensors, AI analytics, IoT connectivity, and cloud platforms are further improving the effectiveness of remote cardiac monitoring systems.

Regional Insights

North America Telecardiology Market Trends

In 2026, North America is estimated to lead with around 49.6% of the share, owing to its novel digital health infrastructure, favorable reimbursement structure, and early adoption of remote cardiac monitoring technologies. The U.S. healthcare system already supports reimbursement for remote physiologic monitoring, remote therapeutic monitoring, and AI-enabled cardiac care through Medicare and private insurers, which has spurred hospital investments in telecardiology platforms.

The U.S. Department of Health and Human Services has continued to expand guidance on remote patient monitoring and connected care services, helping providers integrate telecardiology into routine cardiac management.

U.S. Telecardiology Market Trends

The U.S. is witnessing steady growth driven by superior Medicare reimbursement, rising use of wearable cardiac devices, and increasing adoption of AI-assisted diagnostics. Remote patient monitoring is now widely reimbursed under multiple Medicare billing codes, encouraging healthcare providers to expand virtual cardiac care programs.

The country is also becoming a key innovation hub for AI-assisted cardiac diagnostics. Hospitals are deploying AI systems capable of detecting arrhythmias, coronary artery disease, and heart failure risks from ECG data and imaging scans. Companies such as AliveCor and HeartFlow are extending AI-enabled cardiology tools across healthcare networks. Consumer adoption of smartwatches and wearable ECG devices has also increased substantially, creating high demand for continuous remote cardiac monitoring services in home care settings.

Asia Pacific Telecardiology Market Trends

Asia Pacific is predicted to be the fastest-growing market over the forecast period, driven by its rapidly aging population, rising cardiovascular disease burden, and a large underserved rural population with limited access to cardiologists. Governments across India, China, Japan, and Southeast Asia are investing heavily in digital healthcare infrastructure to improve specialist access outside major urban centers. Telecardiology is increasingly being used to bridge gaps between tertiary hospitals and remote clinics through cloud-connected ECG systems and virtual consultations.

Japan Telecardiology Market Trends

Japan is witnessing decent growth primarily due to its aging population and strong national focus on digital medicine. Nearly one-third of the country’s population is aged 65 or older, creating surging demand for long-term cardiac monitoring and home-based healthcare services. The country has been actively promoting digital therapeutics, AI-assisted healthcare, and remote monitoring solutions to reduce hospital burden and manage chronic diseases more efficiently.

Japan is also becoming an important market for AI-supported ECG monitoring technologies. In 2025, for instance, iRhythm Technologies launched its Zio ECG recording and analysis system in the country, delivering up to 14 days of uninterrupted ECG monitoring supported by PMDA-approved AI algorithms. Compared with conventional Holter monitors, which typically record only 24 to 48 hours, these long-duration wearable systems are improving arrhythmia detection and expanding the country’s telecardiology capabilities.

China Telecardiology Market Trends

China’s market is expanding through AI integration, large-scale hospital digitization, and government-backed healthcare modernization. Key hospitals are now using AI-assisted cardiac diagnostic systems to handle rising patient volumes and physician shortages. In 2025, for example, Shanghai’s Zhongshan Hospital introduced CardioMind. It is described as China’s first AI cardiologist system designed to assist physicians in diagnosing cardiovascular diseases using large-scale patient datasets and clinical guidelines.

Europe Telecardiology Market Trends

Europe is witnessing steady growth driven by increased investments in digital healthcare infrastructure, an aging population, and a rising focus on chronic disease management. Several countries in the region are expanding remote monitoring programs to reduce hospital overcrowding and improve long-term cardiac care delivery. The region is particularly superior in integrated telehealth systems that connect hospitals, primary care centers, and remote diagnostic platforms through unified electronic health networks.

U.K. Telecardiology Market Trends

The U.K. is seeing satisfactory growth as the National Health Service (NHS) is integrating remote monitoring and virtual consultations into cardiovascular care pathways. NHS hospitals are adopting wearable ECG devices, smartphone-linked cardiac monitoring systems, and cloud-based remote diagnostic tools to reduce outpatient pressure and improve specialist accessibility. Remote cardiac monitoring became significantly more common after the pandemic, especially for arrhythmia management and post-operative follow-up care.

The country is also actively testing AI-based cardiac diagnostics through partnerships between NHS trusts and digital health companies. Remote monitoring of implantable cardiac devices has expanded across several NHS facilities, helping clinicians identify abnormal heart rhythms earlier while reducing unnecessary hospital visits. The implementation of public healthcare digitization policies and rising patient acceptance of virtual consultations continue to support telecardiology expansion in the U.K.

Germany Telecardiology Market Trends

Germany’s market is expanding steadily due to national digital health reforms, well-established hospital infrastructure, and increasing use of remote monitoring for chronic cardiac conditions. The country has been actively promoting the adoption of digital healthcare through reimbursement support for telemedicine services and electronic health integration initiatives. Local hospitals are using telecardiology for heart failure management, arrhythmia monitoring, and rehabilitation support.

Competitive Landscape

The global telecardiology market is moderately fragmented, but a handful of large medtech companies dominate through integrated platforms. GE HealthCare, Philips, Medtronic, Abbott, and Siemens Healthineers are leading the competitive race by integrating telecardiology into broad digital health and hospital workflow systems. Their strength lies less in standalone teleconsultation and more in connected cardiac care interfaces involving remote ECG interpretation, wearable monitoring, implantable devices, and AI-assisted diagnostics.

Competition has shifted toward AI-backed cardiac analytics. Large firms are acquiring or partnering with AI start-ups to improve arrhythmia detection, predictive analysis, and workflow automation. Philips strengthened its AI capabilities through Cardiologs integration, while GE HealthCare continues expanding cloud-first cardiology solutions and AI-enabled imaging workflows. Companies such as AliveCor, iRhythm Technologies, VitalConnect, and Heartflow compete through wearable ECG patches, smartphone-based monitoring, and AI-supported interpretation platforms.

Key Industry Developments:

- In May 2026, MedStar Health introduced Auxira, a telecardiology company backed by investments from Abundant Health Ventures. Auxira uses fully remote Advanced Practice Providers (APPs) to handle low-complexity cases while also easing physicians’ administrative workload, including managing inbox communications.

- In March 2025, Circadian Health partnered with Tenovi to integrate cellular-connected remote patient monitoring devices into virtual cardiometabolic care platforms for real-time chronic cardiac disease management.

- In January 2025, Myant Corp. acquired mmHg Inc. to strengthen its AI-enabled remote cardiovascular monitoring capabilities and expand precision medicine solutions for chronic cardiac care.

Companies Covered in Telecardiology Market

- McKesson Corporation

- BioTelemetry Inc.

- BIOTRONIK SE & Co. KG

- Honeywell Life Care Solutions

- Philips

- AMD Global Telemedicine, Inc.

- Aerotel Medical Systems Ltd.

- GE Healthcare

- Meddiff Technologies Pvt. Ltd.

- Siemens Healthineers AG

- Telemed Solution

Frequently Asked Questions

The global telecardiology market is projected to be valued at US$14.5 billion in 2026.

The telecardiology market is expected to reach US$47.2 billion by 2033.

Key trends include the surging adoption of wearable cardiac monitoring devices and the shift of healthcare providers toward continuous remote patient monitoring.

Services are expected to be the leading offering segment with around 48.2% share in 2026, as subscription-based models bundle devices, analytics, and physician review into a single integrated care solution.

The telecardiology market is expected to grow at a CAGR of 18.4% from 2026 to 2033.

McKesson Corporation, BioTelemetry Inc., BIOTRONIK SE & Co. KG, and Honeywell Life Care Solutions are a few key market players.