- Industrial Machinery

- Steam Peeler Market

Steam Peeler Market Size, Share, and Growth Forecast 2026 - 2033

Steam Peeler Market by Product Type (Batch Steam Peelers, Continuous Steam Peelers), by Capacity (Low Capacity, Medium Capacity, High Capacity), by Application (Potato Peeling, Root Vegetables, Fruits, Others), End-Use (Food Processing Industry, Frozen Food Manufacturers, Snack & Chips Industry, Ready-to-Eat (RTE) Food Producers, Agro-processing Units), by Regional Analysis, 2026 - 2033

Steam Peeler Market Size and Trend Analysis

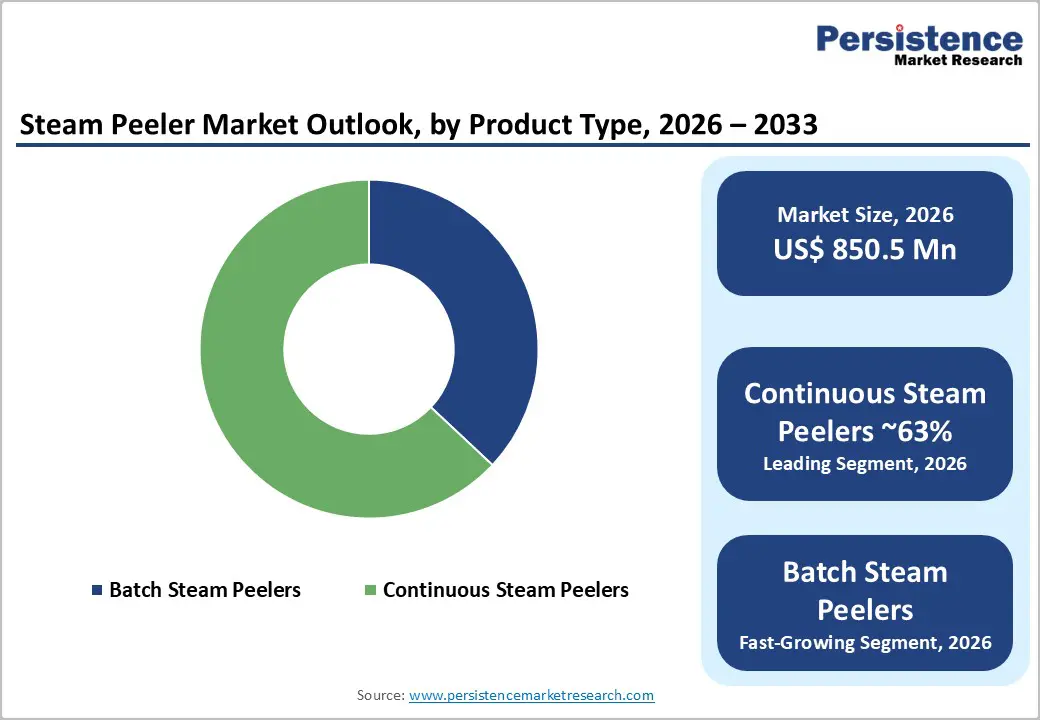

The global steam peeler market size is likely to be valued at US$ 850.5 Million in 2026 and is expected to reach US$ 1,356.8 Million by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033.

The steam peeler market is on a robust and accelerating growth trajectory, driven by the global expansion of industrial potato and vegetable processing, explosive demand for frozen foods and ready-to-eat products, and the food processing industry’s ongoing transition from labor-intensive manual peeling to energy-efficient, high-throughput automated steam peeling systems.

Key Market Highlights

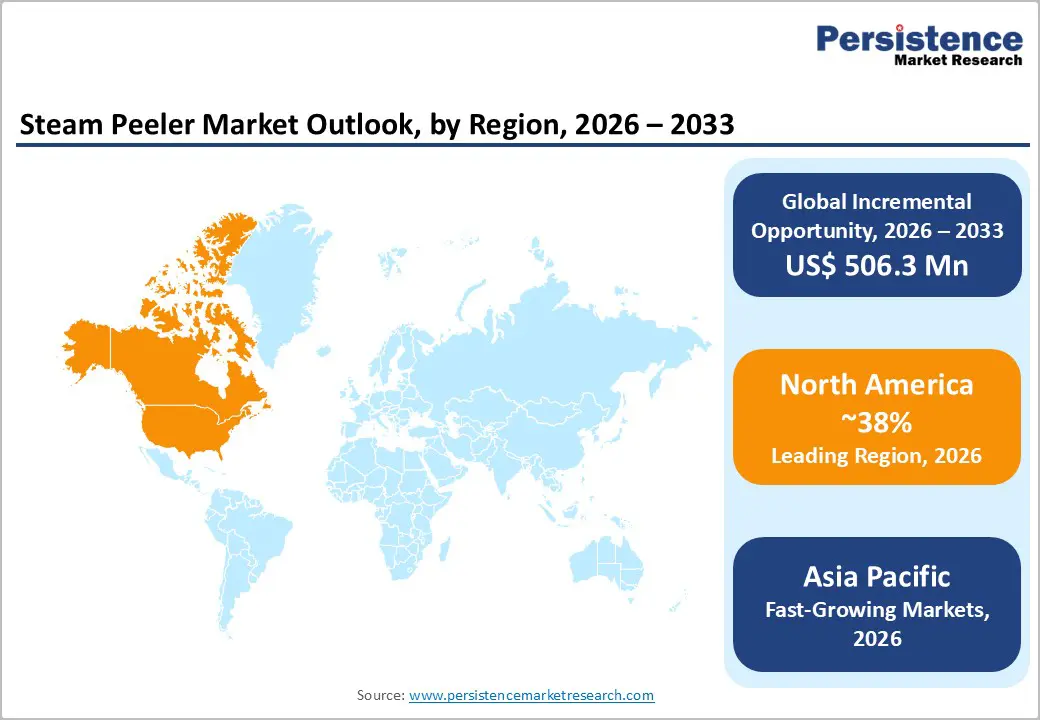

- Leading Region: North America leads the steam peeler market holding 38% share, anchored by the U.S.’s world-leading frozen potato processing sector where over 50% of the domestic potato crop is processed industrially, supported by FSMA food safety regulations and major processors including Lamb Weston and Simplot.

- Fastest Growing Region: Asia Pacific is the fastest growing region with rising CAGR of 9.7%, driven by China’s 90+ million tonne annual potato production with low industrial processing penetration, India’s PMKSY-funded food processing expansion, and rapidly growing ASEAN frozen food export manufacturing creating new steam peeler demand.

- Dominant Segment: Continuous Steam Peelers lead the By Product Type category with approximately 63% market share, preferred by large-scale frozen food, chip, and French fry processors for high-throughput operations of 5-40+ tonnes per hour with minimal labor and seamless production line integration.

- Fastest Growing Segment: Ready-to-Eat Food Producers within the By End-Use category are the fastest growing, driven by global urbanization pushing 68% of population to cities by 2050 and surging demand for pre-peeled, pre-cut convenience vegetable products across modern retail channels worldwide.

- Key Market Opportunity: Industrial potato processing expansion in India (50M+ tonne production, <10% industrially processed) and China, combined with smart steam peeling systems integrating IoT monitoring and AI process optimization for FSMA and EU food safety compliance, represent the highest-value growth opportunities.

Market Dynamics

Drivers - Explosive Global Growth of Frozen Potato and Snack Food Processing

The global frozen potato products and snack food sector is the single most powerful demand driver for industrial steam peeling equipment. According to the World Potato Congress, global potato processing into value-added products has grown consistently, with frozen potato products, including French fries, potato wedges, and hash browns, representing the largest and fastest-growing segment.

Major global frozen food producers, including McCain Foods, Lamb Weston Holdings, and Simplot Company, operate processing facilities each consuming hundreds of thousands of tonnes of potatoes annually, requiring high-capacity continuous steam peeling lines as foundational processing infrastructure. The Euromonitor International and USDA Economic Research Service both confirm sustained growth in global frozen food consumption, particularly in Asia Pacific and the Middle East where Western-style fast food culture and retail frozen food adoption are expanding rapidly, creating new processing facility investments that directly drive steam peeler procurement.

Rising Demand for Ready-to-Eat and Convenience Foods Across Emerging Markets

Rapid urbanization, expanding middle-class demographics, and the erosion of traditional home-cooking culture across Asia, Latin America, and Africa are generating powerful structural growth in demand for processed, ready-to-eat, and semi-prepared food products that depend on industrially peeled vegetables as primary inputs.

The United Nations projects that 68% of the global population will reside in urban areas by 2050, with urban consumers allocating a significantly higher share of food spending to processed and convenience categories. The ready-to-eat food sector, encompassing pre-peeled and pre-cut vegetable packs, meal kits, and cook-chill products, is among the food processing industry’s fastest-growing segments, requiring dedicated peeling infrastructure at fresh-cut and RTE food production facilities worldwide. Steam peelers, with their ability to deliver clean, uniform peeling with minimal product loss, are the technology of choice for these demanding food safety and yield-conscious applications.

Restraints - High Energy Consumption and Steam Generation Costs

Steam peeling is inherently energy-intensive, requiring the generation and delivery of high-pressure steam at 3-8 bar to achieve flash peeling. Industrial steam generation costs are directly linked to natural gas and energy prices, which experienced extreme volatility between 2021 and 2023, with European gas prices increasing by over 400% at peak according to Eurostat.

For food processors operating on thin margins, elevated energy costs directly impact the operating economics of steam peeling versus alternative abrasive peeling methods, potentially deferring or downsizing steam peeling investments during periods of sustained energy price inflation, moderating market growth.

High Capital Investment and Long Equipment Payback Periods

Industrial-scale continuous steam peeling systems from premium manufacturers represent significant capital investments, typically ranging from US$ 200,000 to over US$ 1.5 million, depending on throughput capacity and level of automation. For emerging market food processors and smaller agro-processing units, which represent a substantial share of potential new market participants, these capital requirements present a significant barrier to entry. Access to food processing equipment financing in developing markets is frequently constrained, extending payback period uncertainty and contributing to delayed upgrade cycles among price-sensitive operators.

Opportunities - Expansion of Industrial Potato Processing in Emerging Economies

The establishment and expansion of industrial potato and vegetable processing infrastructure in high-growth emerging economies represents one of the most compelling near-term growth opportunities for steam peeler manufacturers. India, the world’s second-largest potato producer with annual output exceeding 50 million tonnes per the Indian Council of Agricultural Research (ICAR), has historically processed less than 10% of its potato crop industrially, creating an enormous untapped equipment market as domestic and multinational food processors invest in Indian processing capacity.

China, Indonesia, and Brazil are similarly investing in potato and vegetable processing infrastructure to reduce post-harvest losses and capture value in growing domestic frozen and snack food markets. Steam peeler manufacturers that establish local distribution partnerships, offer competitive financing, and develop region-specific throughput configurations can capture significant first-mover advantages in these rapidly developing processing markets.

Automation and Smart Peeling Systems Integration with Food Safety Technologies

The convergence of industrial steam peeling with automation, machine vision, and real-time process monitoring technologies is creating a significant product innovation and premium pricing opportunity for equipment manufacturers. Next-generation smart steam peeling systems incorporating automated defect detection, adaptive steam pressure control based on incoming product characteristics, automated CIP cycles, and IoT-connected process data logging are responding directly to food processors’ requirements for FSMA-compliant and HACCP-validated peeling operations.

Leading players including Tomra Food are integrating optical sorting with downstream peeling to create integrated product quality management lines. According to the International Society of Automation (ISA), food processing automation investment has been growing at over 7% annually, and manufacturers offering digitally integrated, validation-ready steam peeling systems can command significant premium pricing while addressing the growing compliance needs of globally exporting food processors.

Category-wise Analysis

By Product Type Insights

Continuous Steam Peelers dominate the product type segment, commanding approximately 63% of total market share. Continuous steam peelers are the preferred configuration for large-scale industrial food processing operations, particularly potato chip, French fry, and frozen vegetable production facilities, where uninterrupted, high-throughput peeling of 5 to 40+ tonnes per hour is required to match upstream harvesting and downstream processing line speeds.

The continuous configuration minimizes labor requirements, enables consistent steam pressure optimization across the processing cycle, and integrates seamlessly with automated conveyor and sorting systems. Leading manufacturers including Bühler Group, Kiremko B.V., and JBT Corporation offer premium continuous steam peeling lines that serve major global potato processors, reinforcing this segment’s dominant and growing market position.

By Capacity Insights

The High Capacity segment leads the capacity category, representing approximately 47% of total market share. High-capacity steam peelers, processing volumes exceeding 10 tonnes per hour, are the primary equipment specification for large-scale industrial food processors, frozen food manufacturers, and national-scale snack production facilities that require continuous, high-throughput peeling operations to maintain commercially viable processing economics.

The global consolidation of the potato processing industry, with major processors including McCain Foods, Lamb Weston, and Agrarfrost operating mega-facilities processing hundreds of thousands of tonnes annually, has driven procurement toward the highest-capacity peeling configurations. High-capacity systems also generate the highest per-unit revenue for equipment manufacturers, supporting disproportionate segment revenue share relative to unit volume.

By Application Insights

Potato Peeling is the overwhelmingly dominant application segment, accounting for approximately 68% of total market share. Potato is the world’s most widely processed vegetable, with global industrial potato processing consuming tens of millions of tonnes annually for French fry, chip, dehydrated, and frozen product manufacturing. The scale and consistency requirements of industrial potato processing, where peeling loss percentage directly impacts profitability, make high-performance steam peeling the industry-standard technology.

FAO data confirms potatoes as the fourth most important global food crop by production volume, with the proportion destined for industrial processing growing each year as new processing facilities come online across Europe, North America, and emerging markets. The development of purpose-optimized potato steam peeler configurations by manufacturers ensures this application retains its dominant market position.

By End-user Insights

The Food Processing Industry is the dominant end-use segment, representing approximately 36% of total market share. This broad category encompasses the full range of industrial food manufacturers, from large-scale starch and dehydrated potato producers to fresh-cut vegetable processors and canned vegetable manufacturers, all of which require reliable, high-throughput steam peeling as an essential primary processing step.

The segment’s leadership reflects the fundamental role of steam peeling in the industrial food production value chain: virtually every processed potato and root vegetable product begins with a peeling operation, making steam peelers a non-discretionary capital investment for food processors. Industry associations including the European Snacks Association (ESA) and Snack Food Association (SFA) in the U.S. report consistent growth in processed potato and snack volumes, directly underpinning equipment demand.

Regional Insights

North America Steam Peeler Market Trends

North America is the largest and most technologically advanced steam peeler market, anchored by the United States’ world-leading potato processing industry. The U.S. is the world’s largest producer of frozen potato products, with the United States Potato Board (USPB) reporting that over 50% of the domestic potato crop is processed industrially. Major processors including Lamb Weston Holdings, McCain Foods’ North American operations, and Simplot Company operate multiple large-scale processing facilities each requiring continuous high-capacity steam peeling lines. The FDA Food Safety Modernization Act (FSMA) mandates documented preventive controls for food processing operations, driving demand for validated, traceable peeling systems.

Canada contributes significant regional demand, particularly from New Brunswick and Prince Edward Island, major potato-growing provinces supporting both domestic processing and export-oriented frozen food production. The U.S. snack food industry, represented by the Snack Food Association (SFA), generates over US$ 37 billion in annual retail sales, with potato chips constituting the largest category. This scale of snack production requires continuous, high-throughput steam peeling infrastructure. North American equipment innovation ecosystems, including Key Technology Inc., Urschel Laboratories Inc., and JBT Corporation, continuously advance steam peeling technology toward higher efficiency and reduced waste.

Europe Steam Peeler Market Trends

Europe is one of the most established steam peeler market, home to the highest concentration of industrial potato processors and the leading global steam peeler equipment manufacturers. The Netherlands is particularly significant, housing global steam peeling technology leaders including Kiremko B.V., alongside major potato processing operations. Belgium hosts Aviko, Farm Frites, and Clarebout Potatoes, among Europe’s largest frozen potato producers, operating continuous high-capacity steam peeling lines. Germany and Poland are major European potato-producing and processing nations with substantial installed equipment bases.

The United Kingdom and France are significant markets driven by their large frozen and chilled prepared food industries. The EU Farm to Fork Strategy and food waste reduction targets, aiming for a 50% reduction in food waste by 2030 per the European Commission, are providing regulatory tailwinds for steam peeling adoption, as steam peeling achieves significantly lower peeling losses (8-12%) compared to abrasive peeling (15-25%), making it the preferred technology under food waste minimization policies. Spain’s growing frozen vegetable export industry contributes additional regional demand.

Asia Pacific Steam Peeler Market Trends

Asia Pacific is the fastest-growing regional market for steam peelers, driven by expanding potato and vegetable processing capacity across China, India, Japan, and ASEAN markets. China is the world’s largest potato producer with annual output exceeding 90 million tonnes per FAO data, yet industrial processing penetration remains relatively low, creating a massive growth opportunity as domestic and multinational food processors invest in new facilities targeting China’s rapidly growing frozen food and snack markets. Chinese equipment manufacturers including Shandong Tinwing Machinery Manufacturing Co. Ltd. and Yangzhou Carota Automation Machinery Co. Ltd. supply cost-competitive steam peelers for both domestic and export markets.

India’s industrial potato processing sector is expanding rapidly, supported by government post-harvest infrastructure investment under the Pradhan Mantri Kisan Sampada Yojana (PMKSY) scheme allocating over INR 6,000 crore to food processing infrastructure. Japan represents a mature, high-specification market for precision steam peeling equipment used in premium frozen and chilled food production. ASEAN nations, particularly Thailand, Vietnam, and Malaysia, are experiencing rapid growth in processed food manufacturing, creating new steam peeler demand from food export processors targeting Japan, the Middle East, and European retail markets. Asia Pacific’s manufacturing cost advantages support a growing regional equipment supply base alongside premium international machine imports.

Competitive Landscape

The global steam peeler market is moderately consolidated, led by a core group of European and North American technology specialists that command premium market positions through decades of food processing engineering expertise and global service infrastructure. Companies such as Bühler Group, Kiremko B.V., JBT Corporation, and Marel hold strong positions through comprehensive potato processing line integration capabilities that include steam peeling as a key component.

Key competitive differentiators include throughput capacity, peeling loss percentage, energy efficiency, CIP compatibility, and food safety validation support. Emerging trends include the integration of steam peeling with optical sorting and AI-assisted process optimization. Asian manufacturers are increasing competition in mid-range capacity segments through cost-competitive offerings, particularly in emerging market geographies.

Key Developments:

- January 2025: Kiremko B.V. launched an enhanced continuous steam peeler series featuring integrated IoT process monitoring, automated steam pressure optimization, and energy recovery heat exchangers, targeting large-scale European and North American frozen potato processing facilities.

- August 2024: Marel announced integration of its steam peeling product line with its Innova food processing intelligence platform, enabling real-time OEE monitoring, peeling loss analytics, and predictive maintenance alerts for potato and vegetable processing operations globally.

- March 2024: Bühler Group expanded its food processing equipment portfolio for the Asian market by establishing a dedicated application center in China, offering steam peeling system demonstrations and process optimization services for Chinese potato and vegetable processors.

Companies Covered in Steam Peeler Market

- Bühler Group

- Key Technology Inc.

- Urschel Laboratories Inc.

- Grote Company

- Bigtem Makine

- VegTech Systems

- Shandong Tinwing Machinery Manufacturing Co. Ltd.

- Yangzhou Carota Automation Machinery Co. Ltd.

- LONKIA Machinery

- Envitro Technomech

- Marel

- Tomra Food

- JBT Corporation

- Turatti Group

- Kiremko B.V.

- Allround Vegetable Processing B.V.

- KRONEN GmbH

- TOMRA Systems ASA

Frequently Asked Questions

The global Steam Peeler Market is projected to reach US$ 1,356.8 Million by 2033, expanding from US$ 850.5 Million in 2026 at a CAGR of 6.9% during the 2026-2033 forecast period. This represents a significant acceleration from the historical CAGR of 5.1% recorded between 2020 and 2025, driven by frozen food processing expansion and emerging market industrialization.

The primary growth drivers are the global frozen potato product industry’s expansion, with FAO ranking potato as the world’s fourth most important food crop at 370+ million tonnes annual production, and rising urbanization driving RTE food consumption, with the UN projecting 68% of global population in urban areas by 2050 requiring mass-produced convenience foods dependent on industrial peeling infrastructure.

Continuous Steam Peelers lead the By Product Type category with approximately 63% of total market share. Their dominance reflects the operational requirements of large-scale industrial food processors, particularly frozen French fry, chip, and frozen vegetable manufacturers, requiring uninterrupted high-throughput peeling at 5-40+ tonnes per hour, seamless production line integration, and minimal labor inputs at scale.

North America leads the global Steam Peeler Market, anchored by the United States’ world-leading potato processing sector where over 50% of the domestic potato crop is industrially processed. Major processors including Lamb Weston Holdings, McCain Foods, and Simplot Company operate large-scale continuous steam peeling lines, while FDA FSMA food safety regulations maintain high equipment standard requirements.

The highest-value opportunities are industrial potato processing expansion in India (50M+ tonne production, less than 10% industrially processed, supported by PMKSY funding) and China (90M+ tonnes, low processing penetration), and smart steam peeling systems integrating IoT monitoring, AI process optimization, and CIP validation responding to FSMA and EU food safety compliance requirements.

The key market participants include Bühler Group, Key Technology Inc., Urschel Laboratories Inc., Grote Company, Bigtem Makine, VegTech Systems, Shandong Tinwing Machinery Manufacturing Co. Ltd., Yangzhou Carota Automation Machinery Co. Ltd., LONKIA Machinery, Envitro Technomech, Marel, Tomra Food, JBT Corporation, Turatti Group, and Kiremko B.V.