- Healthcare

- Spinal Cord Stimulation System Market

Spinal Cord Stimulation System Market Size, Share, and Growth Forecast, 2026 - 2033

Spinal Cord Stimulation System Market by Product Type (Conventional System, Radiofrequency System, Others), Application (Failed Back Syndrome (FBS), Complex Regional Pain Syndrome, Others), End-user, and Regional Analysis for 2026 - 2033

Spinal Cord Stimulation System Market Size and Trends Analysis

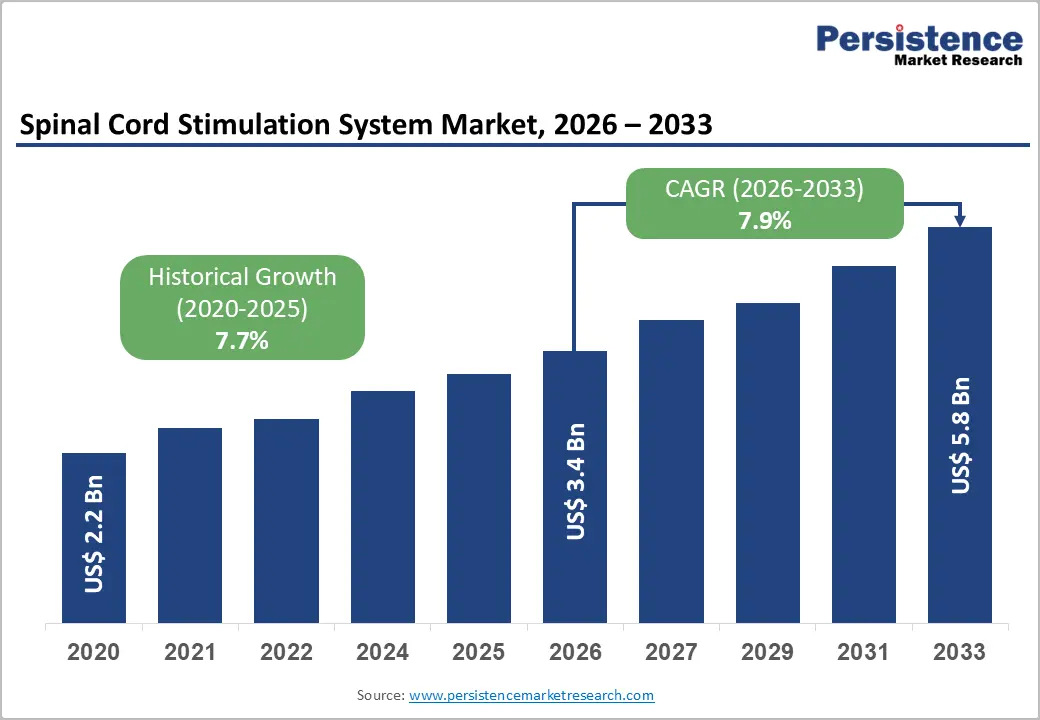

The global spinal cord stimulation system market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$5.8 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by increasing adoption of neuromodulation therapies for chronic pain management, particularly in patients who are unresponsive to conventional pharmacological treatments. Demand is strongly supported by the rising prevalence of neuropathic pain conditions, degenerative spinal disorders, failed back surgery syndrome, and age-related musculoskeletal diseases, which collectively expand the eligible patient pool for implantable pain management solutions.

The market is also benefiting from a broader healthcare shift toward non-opioid pain therapies due to concerns over opioid dependence and long-term side effects, encouraging physicians to adopt advanced implantable stimulation technologies. Technological innovation is a key growth pillar, with increasing integration of high-frequency stimulation, burst stimulation, and closed-loop feedback systems that improve pain relief outcomes and patient personalization.

Key Industry Highlights:

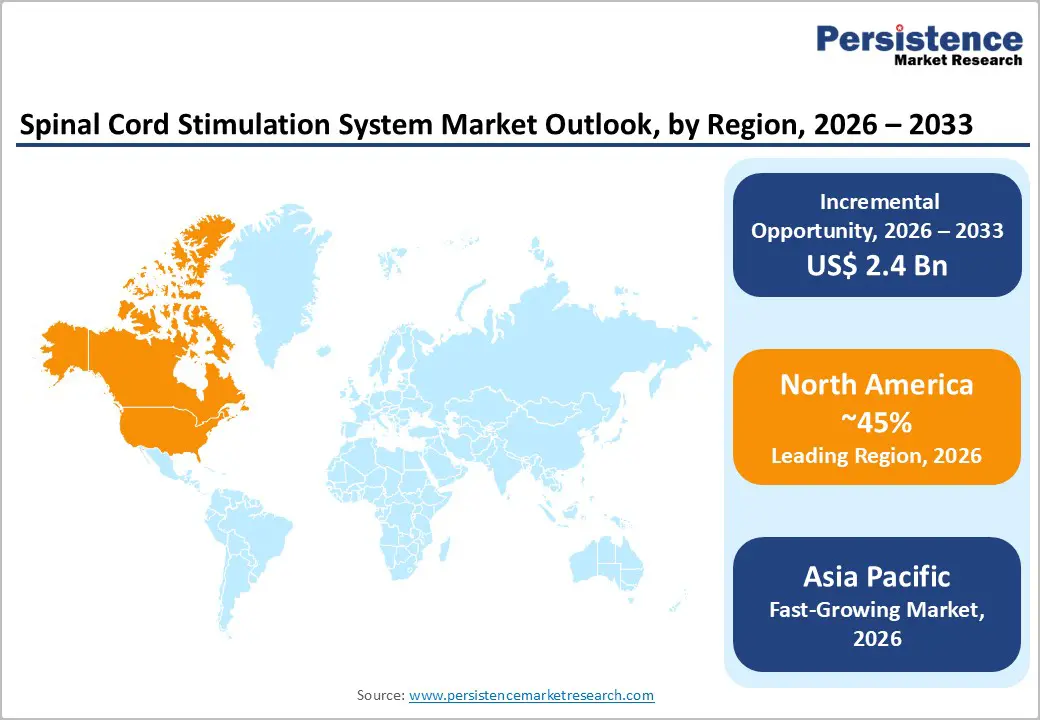

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by high chronic pain burden, strong reimbursement systems, advanced healthcare infrastructure, and early adoption of neuromodulation technologies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rising chronic diseases, an aging population, healthcare expansion, and increasing adoption of neuromodulation technologies.

- Leading Product Type: Rechargeable systems are projected to represent the leading product type in 2026, accounting for 60% of the revenue share, driven by longer battery life, fewer replacement surgeries, improved patient compliance, and compatibility with advanced stimulation technologies.

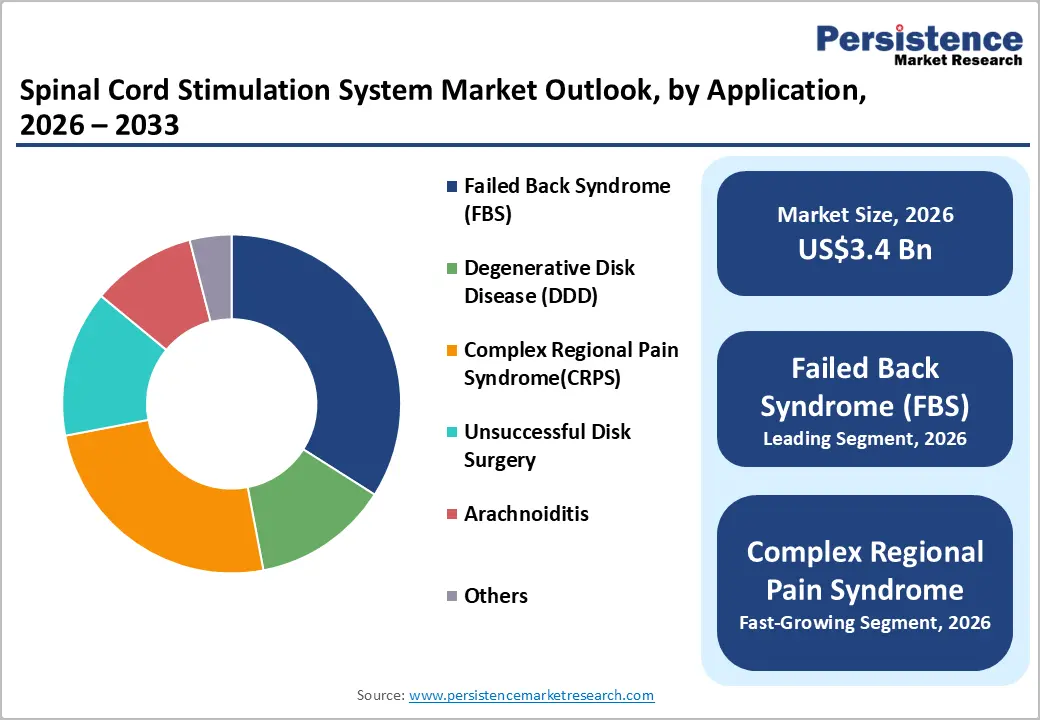

- Leading Application: Failed back syndrome (FBS) is anticipated to be the leading application, accounting for over 50% of the revenue share in 2026, supported by high incidence of post-lumbar surgery pain, strong clinical evidence base, and established reimbursement coverage.

| Key Insights | Details |

|---|---|

| Spinal Cord Stimulation System Market Size (2026E) | US$3.4 Bn |

| Market Value Forecast (2033F) | US$5.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.7% |

DRO Analysis

Driver - Rising Prevalence of Chronic Pain Conditions and Failed Back Surgery Syndrome

The increasing prevalence of chronic pain conditions such as failed back surgery syndrome, degenerative disk disease, and neuropathic pain is significantly driving demand for spinal cord stimulation systems. A growing aging population and a rising number of spinal surgeries are leading to higher post-surgical chronic pain cases. Many patients do not achieve adequate relief from conventional pharmacological treatments, increasing dependence on neuromodulation therapies.

Clinical adoption is supported by strong evidence demonstrating the effectiveness of spinal cord stimulation in reducing chronic pain intensity and improving quality of life. Physicians are increasingly recommending this therapy for refractory pain conditions where conservative treatments fail. Expanding reimbursement support in developed healthcare systems is improving accessibility for patients. Rising hospital admissions for spine-related disorders and improved referral networks are increasing procedure volumes.

Technological Advancements in Rechargeable and Closed-Loop Systems

Technological advancements in spinal cord stimulation systems, particularly rechargeable and closed-loop devices, are significantly enhancing treatment outcomes and driving market growth. Rechargeable systems provide extended device lifespan, reducing the need for repeated surgical replacement procedures and lowering long-term healthcare costs. These systems also improve patient convenience and compliance due to better battery efficiency. Closed-loop stimulation technology enables real-time adjustment of therapy based on patient feedback signals, resulting in more precise pain control.

The integration of advanced digital technologies into spinal cord stimulation devices is strengthening market adoption. Wireless connectivity and remote programming capabilities allow physicians to adjust therapy settings without requiring in-person visits, improving patient management efficiency. These innovations are increasing physician confidence in neuromodulation therapies and expanding their application across broader chronic pain indications.

Restraint - Reimbursement Variability and Healthcare Access Constraints

Reimbursement variability across different healthcare systems remains a major barrier to the adoption of spinal cord stimulation systems. While developed regions offer structured insurance coverage, strict eligibility criteria and prior authorization requirements often delay treatment initiation. In many developing countries, limited insurance penetration and high out-of-pocket expenses significantly restrict patient access to advanced neuromodulation therapies. The high cost of implantation procedures and devices increases the financial burden on patients.

Healthcare access constraints also play a critical role in limiting market penetration, especially in rural and underdeveloped regions. Limited availability of specialized pain management centers and trained neurosurgeons reduces treatment accessibility. Infrastructure gaps in advanced medical facilities restrict the adoption of complex implantable devices. Lengthy approval processes and administrative hurdles in insurance systems delay patient treatment pathways. These combined financial and structural limitations result in delayed or missed treatment opportunities for eligible patients.

Physician Training and Patient Selection Challenges

Physician training limitations significantly impact the effective adoption of spinal cord stimulation systems in clinical practice. Many general practitioners and even some pain specialists lack sufficient exposure to advanced neuromodulation techniques, leading to underutilization of this therapy. Proper implantation and programming of devices require specialized expertise, which is not uniformly available across healthcare systems. Inadequate training can also affect procedural outcomes and patient satisfaction.

Patient selection challenges restrict optimal market growth as successful outcomes depend heavily on identifying appropriate candidates. Accurate evaluation requires a detailed assessment of pain type, psychological readiness, and previous treatment responses. Misidentification of suitable patients can lead to poor outcomes and reduced therapy effectiveness. Limited awareness among referring physicians often delays appropriate patient referrals. Variability in clinical guidelines across regions creates inconsistencies in patient selection practices.

Opportunity - Expansion into Non-Surgical Back Pain and Peripheral Neuropathies

Expansion into non-surgical back pain represents a major growth opportunity for spinal cord stimulation systems, as clinical evidence increasingly supports its effectiveness even in patients who have not undergone prior spinal surgery. This significantly expands the potential patient pool beyond traditional indications such as failed back surgery syndrome. The rising prevalence of chronic lower back pain due to sedentary lifestyles and occupational stress is increasing the demand for advanced pain management solutions.

Peripheral neuropathies, including diabetic neuropathy and nerve injury-related pain, are emerging as important new indications for spinal cord stimulation therapy. These conditions are becoming more common due to the rise in diabetes and metabolic disorders. Neuromodulation is showing promising outcomes in reducing pain intensity and improving patient mobility in these cases. Increasing physician awareness and supportive clinical evidence are accelerating adoption in these expanded indications.

Technological Convergence with AI and Remote Monitoring

The integration of artificial intelligence into spinal cord stimulation systems is creating significant opportunities for personalized and adaptive pain management. AI-driven algorithms can analyze patient response patterns and automatically optimize stimulation parameters for improved therapeutic outcomes. This reduces the need for frequent manual adjustments and enhances treatment precision. Machine learning models are also helping predict patient responsiveness, enabling better patient selection.

Remote monitoring technologies are transforming the management of spinal cord stimulation patients by enabling real-time tracking of device performance and patient outcomes. Physicians can adjust stimulation settings remotely, reducing the need for hospital visits and improving long-term care efficiency. Integration with digital health platforms enhances patient engagement and therapy adherence. These technologies support value-based healthcare models by reducing overall treatment costs while improving clinical outcomes.

Category-wise Analysis

Product Type Insights

Rechargeable spinal cord simulation systems are expected to lead the spinal cord stimulation system market, accounting for approximately 60% of revenue in 2026, driven by extended device lifespan, reduced need for replacement surgeries, and improved cost efficiency over time. These systems are widely preferred by both physicians and patients due to their compatibility with advanced stimulation waveforms and better long-term reliability. For example, in patients with chronic failed back surgery syndrome, rechargeable implants are often selected to minimize repeat surgical interventions and improve treatment continuity, making them the standard choice in advanced neuromodulation practice.

Non-rechargeable systems are likely to represent the fastest-growing segment, supported by increasing use in elderly patients and those with limited ability to manage recharging requirements. These systems are gaining attention due to simpler usage, lower upfront procedural complexity, and suitability for short to medium-term pain management. For example, in elderly patients suffering from degenerative disk disease with limited mobility, non-rechargeable implants are preferred due to ease of use and reduced maintenance requirements.

Application Insights

Failed back syndrome (FBS) is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by the high prevalence of chronic pain following spinal surgeries and strong clinical validation of spinal cord stimulation in managing post-laminectomy pain. It remains the most commonly treated indication due to consistent reimbursement support and well-established treatment protocols. For example, patients experiencing persistent pain after lumbar decompression surgery are often referred for spinal cord stimulation implantation, as it provides significant long-term pain relief and improved functional outcomes.

Complex regional pain syndrome (CRPS) is likely to be the fastest-growing application, driven by increasing awareness of early neuromodulation intervention and expanding clinical evidence demonstrating its effectiveness in neuropathic pain control. Growth is driven by improved diagnostic accuracy and the adoption of high-frequency and burst stimulation technologies. For example, in post-traumatic limb pain cases associated with CRPS, early implantation of spinal cord stimulators has shown significant improvement in pain reduction and functional recovery.

Regional Insights

North America Spinal Cord Stimulation System Market Trends

North America is anticipated to be the leading region, accounting for a market share of 45%, driven by high adoption of advanced neuromodulation therapies, strong reimbursement frameworks, and a large patient base suffering from chronic pain conditions such as failed back surgery syndrome and neuropathic disorders. For example, Medtronic has expanded its Intellis rechargeable neurostimulator adoption across the U.S., supporting broader use of advanced neuromodulation technologies in chronic pain management and strengthening its leadership position in the region.

The market is also characterized by rapid technological innovation and strong clinical research activity, with continuous FDA approvals expanding indications for spinal cord stimulation use. Growth in outpatient and ambulatory surgical centers is improving procedural accessibility and reducing healthcare costs. Physicians in North America demonstrate high awareness and training levels in neuromodulation therapies, enabling faster adoption compared to other regions.

Europe Spinal Cord Stimulation System Market Trends

Europe is likely to be a significant market for spinal cord stimulation systems, due to the increasing prevalence of chronic pain conditions, aging population demographics, and strong public healthcare systems. The region demonstrates consistent adoption of neuromodulation therapies, particularly in countries such as Germany, the U.K., and France, where advanced pain management protocols are well established. Demand is rising for rechargeable and minimally invasive stimulation systems due to their improved safety profiles and long-term cost-effectiveness.

The increasing integration of evidence-based clinical guidelines supports early use of spinal cord stimulation for refractory pain conditions. Clinical research and multicenter studies are actively contributing to broader acceptance among physicians. For example, Abbott’s Proclaim XR spinal cord stimulation system has seen strong adoption across European pain clinics, particularly in Germany, where healthcare providers emphasize advanced neuromodulation for chronic back pain management.

Asia Pacific Spinal Cord Stimulation System Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by increasing healthcare investments, rising prevalence of chronic pain disorders, and improving access to advanced medical technologies. Countries such as China and India are witnessing rapid expansion in neuromodulation adoption due to growing awareness of minimally invasive pain management solutions. The region shows increasing demand for cost-effective and rechargeable systems, particularly in urban hospitals and specialty pain clinics.

The gradual improvement in regulatory frameworks and healthcare infrastructure is enabling faster approval and adoption of advanced medical devices. International companies are increasingly entering partnerships with local distributors to strengthen market penetration. For example, Boston Scientific has expanded its WaveWriter Alpha spinal cord stimulation system presence in Japan, supporting advanced pain therapy adoption in high-tech healthcare settings. Growing medical tourism in countries such as India and Thailand is contributing to increased procedural volumes.

Competitive Landscape

The global spinal cord stimulation system market exhibits a moderately fragmented structure, driven by the strong dominance of a few multinational medical device companies with advanced neuromodulation portfolios, high R&D investments, and continuous product innovation in chronic pain management technologies. The market is characterized by strong competition in rechargeable, closed-loop, and high-frequency stimulation systems, which are increasingly replacing conventional implantable devices due to improved clinical outcomes and longer device life.

With key leaders including Medtronic, Abbott Laboratories, Boston Scientific Corporation, and Nevro Corp, the competitive landscape is shaped by companies focusing on technological differentiation, strategic acquisitions, and expansion. Medtronic maintains a strong position with its broad neuromodulation portfolio and deep clinical research capabilities, while Abbott strengthens its presence through advanced rechargeable systems and patient-centric innovations.

Key Industry Developments:

- In July 2025, Saluda Medical announced the commercial launch of its EVA sensing technology, designed for integration with the Evoke SmartLoop closed-loop spinal cord stimulation (SCS) system. The technology uses real-time detection of evoked compound action potentials (ECAPs) to monitor spinal cord neural responses and automatically adjust stimulation levels.

- In August 2025, Boston Scientific announced the launch of its Precision Plus™ Spinal Cord Stimulation (SCS) System, a next-generation rechargeable neuromodulation device designed for the treatment of chronic pain affecting the trunk, back, and limbs. The system is positioned as one of the smallest rechargeable SCS implantable pulse generators, offering enhanced patient comfort along with improved therapy control.

Companies Covered in Spinal Cord Stimulation System Market

- Boston Scientific Corporation

- Medtronic

- NeuroSigma, Inc.

- Nevro Corp.

- Synapse Biomedical Inc.

- Abbott

- GIMER MEDICAL

- Bluewind Medical

Frequently Asked Questions

The global spinal cord stimulation system market is projected to reach US$3.4 billion in 2026.

The spinal cord stimulation system market is driven by rising chronic pain prevalence, growing preference for non-opioid therapies, and advancements in neuromodulation technologies.

The spinal cord stimulation system market is expected to grow at a CAGR of 7.9% from 2026 to 2033.

Key market opportunities include expanding use in non-surgical chronic pain and neuropathies, adoption of AI-enabled closed-loop systems, and growth in emerging healthcare markets.

Boston Scientific Corporation, Medtronic, NeuroSigma, Inc., Nevro Corp., and Synapse Biomedical Inc are the leading players.