- Retail

- Specialty Cut Flower Market

Specialty Cut Flower Market Size, Share, and Growth Forecast 2026 - 2033

Specialty Cut Flower Market by Flower Type (Annual Specialty Flowers, Perennial Specialty Flowers, Bulb & Tuber Flowers, Woody & Foliage Stems, Exotic & Tropical Flowers, Fillers & Accent Flowers), Application (Household/Personal Use, Events & Occasions, Commercial Use, Hotels & Hospitality), Distribution Channel, and Regional Analysis, 2026 - 2033

Specialty Cut Flower Market Size and Trend Analysis

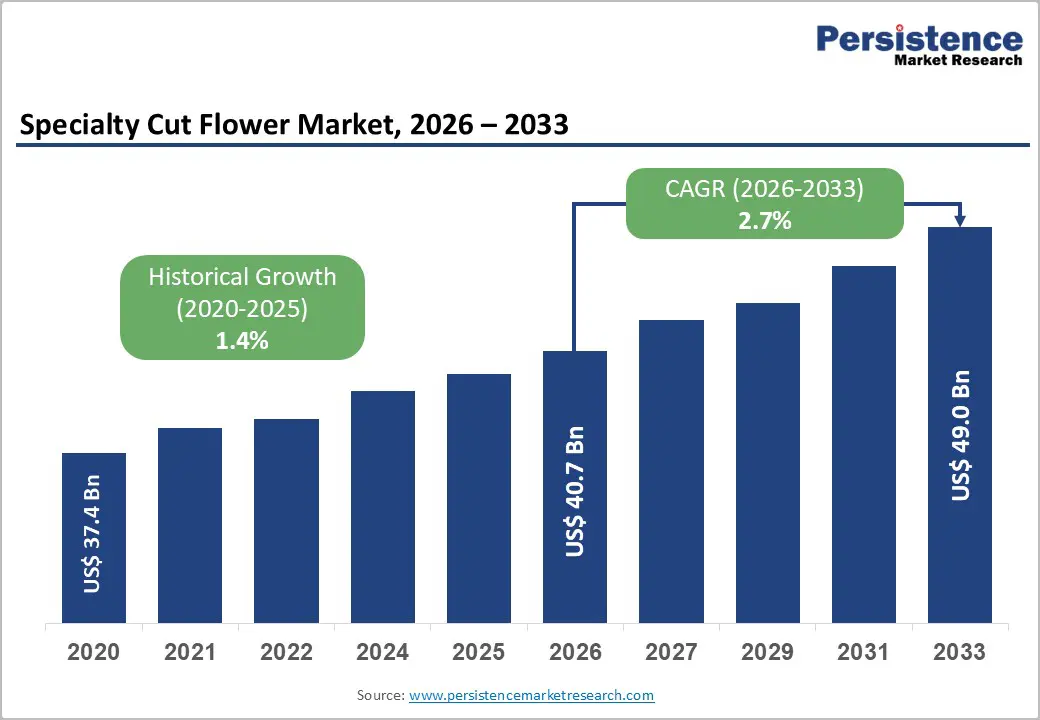

The global specialty cut flower market size is likely to be valued at US$ 40.7 Billion in 2026 and is expected to reach US$ 49.0 Billion by 2033, growing at a CAGR of 2.7% during the forecast period from 2026 to 2033. The specialty cut flower industry is advancing on a moderate but structurally durable growth trajectory, driven by expanding floral gifting culture, accelerating e-commerce adoption, enabling year-round consumer access, and rising demand from events, hospitality, and premium retail channels globally.

Key Industry Highlights:

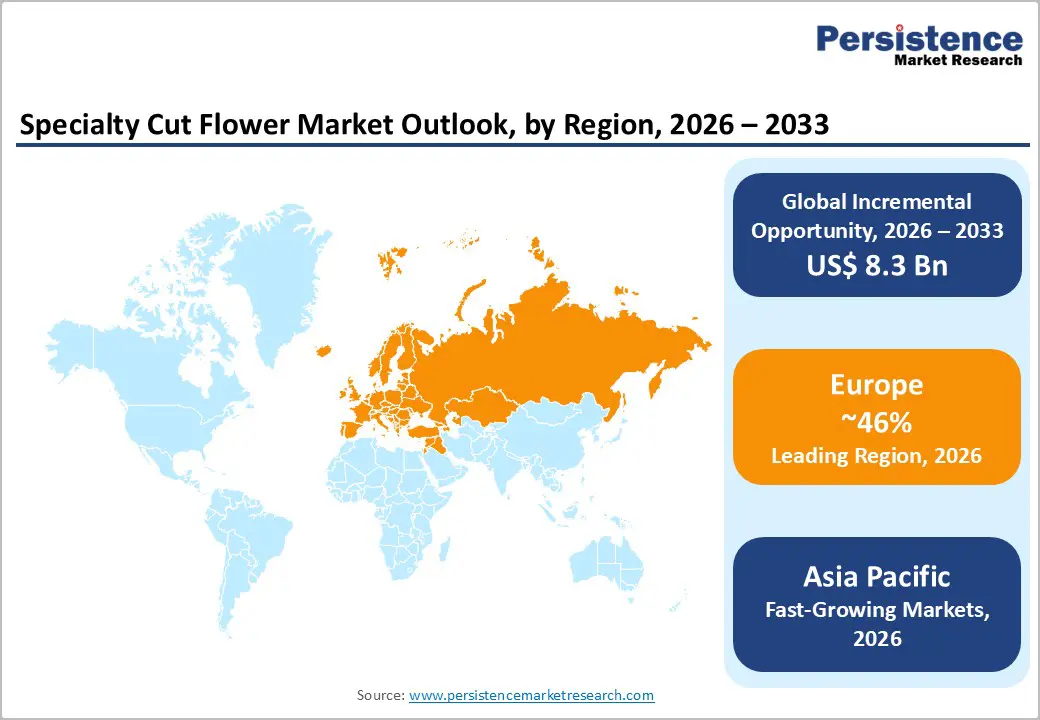

- Leading Region: Europe leads the global specialty cut flower market with approximately 46% of global value in 2024, anchored by the Netherlands' Royal FloraHolland auction processing EUR 5.2 billion annually, 50% of global flower exports, and 12 billion stems through Aalsmeer, the world's largest flower trading facility

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a positive CAGR, with China's rapidly expanding urban floral gifting and home décor demand, Yunnan Province's domestic production scale, and fast-growing specialty flower markets in Japan, India, and key ASEAN economies outpacing global market growth rates

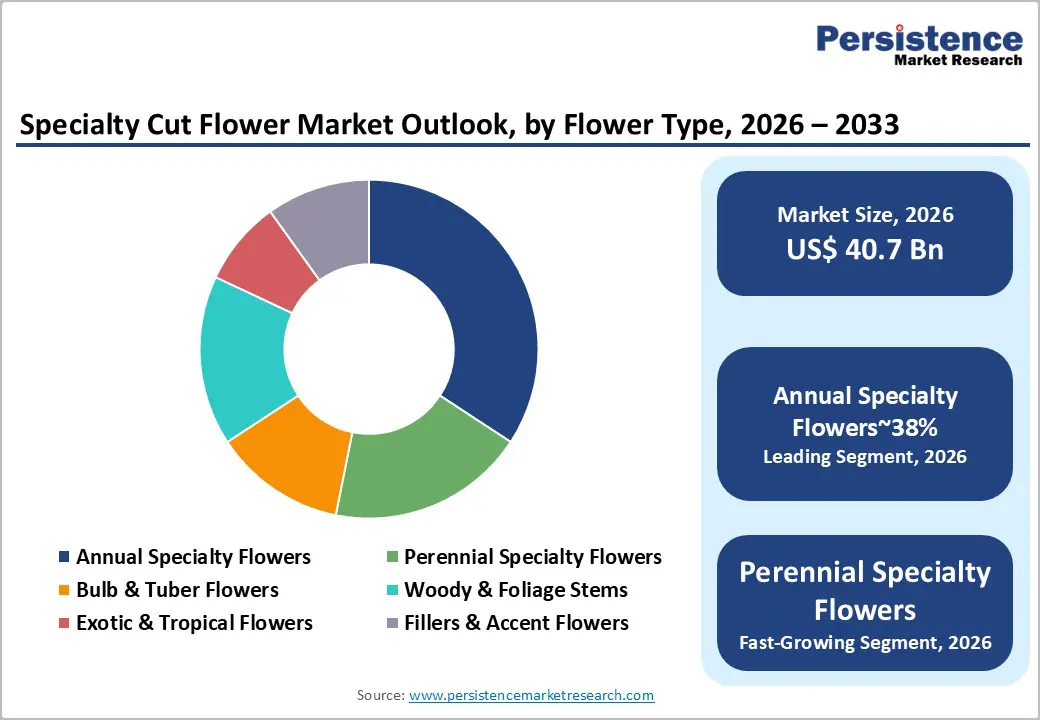

- Leading Flower Type: Annual Specialty Flowers, led by roses, gerberas, chrysanthemums, and seasonal cutting varieties, with approximately 38% market share, sustained by year-round demand across all application segments and confirmed high trade volumes through Royal FloraHolland's global auction infrastructure

- Fastest-Growing Segment: Online / E-commerce is the fastest-growing distribution channel, with subscription models accounting for 26% of online floral sales in the U.S. in 2025, driven by cold chain advances maintaining 2–8°C fulfillment and AI-powered inventory optimization reducing post-harvest losses across digital-native floral brands

- Key Opportunity: Sustainable and certified specialty flower production represents the most strategically significant opportunity, as Fairtrade, Rainforest Alliance, and MPS-certified stems command premium retail pricing and are increasingly required by major European and North American supermarket chains and hotel procurement programs.

| Key Insights | Details |

|---|---|

|

Specialty Cut Flower Market Size (2026E) |

US$ 40.7 Billion |

|

Market Value Forecast (2033F) |

US$ 49.0 Billion |

|

Projected Growth CAGR (2026–2033) |

2.7% |

|

Historical Market Growth (2020–2025) |

1.4% |

DRO Analysis

Drivers - Expanding Floral Gifting Culture and Non-Occasion Personal Use Driving Broadened Demand

One of the most important structural drivers in the specialty cut flower market is the steady shift in consumption patterns from traditional seasonal occasions, such as Valentine’s Day, Mother’s Day, Christmas, and Easter, toward everyday personal use. Consumers are increasingly purchasing flowers for home décor, wellness, and self-gifting, making flowers part of their regular lifestyle rather than occasional purchases.

Data from major U.S. floral retail platforms shows that subscription models account for 26% of online floral sales as of 2025, reflecting this behavioral shift. The U.S. cut flower market generated USD 7.6 billion in 2024 and is projected to grow at a CAGR of 6% through 2034, with personal use emerging as the leading demand category. At the same time, China is experiencing strong growth driven by rapid urbanization and higher consumer spending on floral décor and premium gifting. Together, these trends are transforming the market into a stable, year-round demand model.

E-commerce Expansion and Cold Chain Innovation: Unlocking New Consumer Markets

The rapid growth of online floral retail is transforming the specialty cut flower market by removing traditional geographic and seasonal limitations. E-commerce platforms, direct-to-consumer delivery services, and subscription bouquet models are making specialty flowers accessible to a wider audience. These platforms leverage digital marketing, social commerce, and same-day delivery to reach customers who previously had limited access to premium floral varieties.

Advancements in cold chain logistics, such as vacuum cooling, IoT-based temperature monitoring, blockchain traceability, and temperature-controlled last-mile delivery maintained at 2–8°C, are significantly reducing post-harvest losses, which typically range between 20–30%. Additionally, AI-driven inventory forecasting and route optimization are improving supply efficiency and minimizing waste. These technological advancements are enabling reliable product availability, expanding market reach, and increasing per-capita consumption in regions that previously had limited access to specialty flowers.

Restraints - High Perishability and Supply Chain Fragility Limiting Market Efficiency and Price Stability

Specialty cut flowers are among the most perishable agricultural products, with vase life ranging from as little as three days for delicate varieties to about two weeks for more durable blooms. This high perishability requires strict temperature-controlled handling throughout the entire supply chain, from the farm to the end consumer. Any disruption, such as flight delays, temperature fluctuations, port congestion, or regulatory inspection delays, can lead to significant product loss, directly impacting supplier revenues and retailer margins.

On average, post-harvest losses in conventional supply chains range up to 25%, representing a major structural inefficiency. These losses reduce the overall profitability and value realization across the supply chain, especially for smaller specialty flower producers who lack access to advanced logistics infrastructure. As a result, maintaining product quality and ensuring consistent supply remain critical challenges, limiting pricing stability and overall market efficiency.

Climate Change and Extreme Weather Disrupting Production in Key Export Regions

Climate change is emerging as a major structural risk for the specialty cut flower market, as extreme weather conditions increasingly disrupt production in key growing regions. Events such as prolonged droughts, unexpected frost, flooding, and temperature fluctuations are affecting both the yield and the quality of flowers. Major exporters like Colombia and Kenya, which together account for approximately 35% of global cut flower exports, are particularly vulnerable to these environmental challenges.

Kenya’s flower industry, which generated around USD 835 million in export revenues in 2024, is highly dependent on stable water availability and consistent climatic conditions. Any disruption leads to supply shortages, quality inconsistencies, and increased production costs. These climate-related uncertainties create price volatility in global auction markets and reduce buyer confidence in consistent supply, ultimately slowing down the overall growth momentum of the market.

Opportunity - Sustainable and Certified Flower Production Meeting Growing Retailer and Consumer Demand for Ethical Sourcing

The increasing focus on sustainability, ethical sourcing, and environmental responsibility is creating a strong growth opportunity in the specialty cut flower market. Consumers and retailers are now prioritizing flowers that are produced using environmentally friendly and socially responsible practices. Certifications such as Fairtrade, Rainforest Alliance, MPS (Milieu Programma Sierteelt), and Florverde Sustainable Flowers are becoming essential for accessing premium market segments. These certifications are particularly valued by international retailers, hotels, and event planners who integrate sustainability into their procurement policies.

Data from Royal FloraHolland indicates that certified flowers often command premium prices in both European and North American markets. This trend is encouraging producers in regions such as East Africa and Latin America to invest in sustainable cultivation practices. As sustainability becomes a key purchasing criterion, certified producers gain a competitive advantage through improved market access, stronger brand positioning, and long-term supply contracts.

Online / E-commerce and Subscription Floral Services as a High-Growth Distribution Opportunity

The online and direct-to-consumer distribution channel is the fastest-growing segment in the specialty cut flower market, offering significant growth potential for producers and retailers. Subscription-based floral delivery services, which account for 26% of online floral sales in the U.S. as of 2025, are particularly attractive due to their ability to generate recurring revenue and predictable demand. These models provide better demand visibility for growers and increase customer lifetime value compared to one-time purchases.

Specialty flower varieties, including exotic blooms, seasonal arrangements, and sustainably sourced collections, are well-suited for subscription services because they offer variety and personalization. Additionally, platforms that use AI-driven personalization, source farm-direct from regions like Kenya, Ethiopia, Colombia, and the Netherlands, and offer flexible delivery options are enhancing customer engagement. These innovations are encouraging consumers to purchase flowers more frequently, expanding usage beyond gifting into everyday lifestyle and home décor applications.

Category-wise Analysis

By Flower Type Insights

Annual Specialty Flowers, including roses, chrysanthemums, gerberas, carnations, lisianthus, and seasonal cut varieties, lead the By Flower Type category, contributing approximately 38% of total market revenue. This strong position reflects consistent consumer preference for these well-known and versatile flowers across multiple applications such as personal gifting, home décor, events, hospitality, and commercial displays.

Among them, roses remain the most traded cut flower globally, with Royal FloraHolland’s auction data consistently ranking them as the highest-volume category at the Aalsmeer facility, which processes nearly 12 billion stems and potted plants annually. Additionally, lilies and gerberas recorded strong performance in Q1 2025, supported by supply constraints that drove prices to record levels. Their year-round availability, stable demand, and widespread cultivation across regions such as Kenya, Ecuador, Colombia, the Netherlands, and Japan continue to reinforce the segment’s dominant market position.

By Application Insights

The events & occasions segment dominates the By Application category, accounting for approximately 34% of total market revenue. This leadership is driven by consistently high spending on flowers for weddings, corporate gatherings, funerals, religious ceremonies, graduations, and major seasonal events such as Valentine’s Day and Mother’s Day. These occasions collectively contribute a substantial share of annual global cut flower demand.

Event floristry is particularly attractive due to its high-margin nature and strong customization requirements, where specialty flowers, including exotic tropical varieties, premium garden roses, and decorative foliage, command premium pricing compared to standard retail offerings. Furthermore, the global events industry, generating hundreds of billions in revenue annually, provides a stable and predictable demand base tied to recurring seasonal and cultural calendars. Meanwhile, the Household / Personal Use segment is emerging as the fastest-growing category, driven by rising consumer interest in everyday floral décor and the rapid expansion of subscription-based flower delivery services.

By Distribution Channel Insights

The Wholesale / Auctions channel is the largest distribution segment in the Specialty Cut Flower Market, accounting for approximately 42% of total revenue. This channel remains the foundation of the global flower trade, supported by well-established wholesale networks and auction systems. A key example is Royal FloraHolland’s auction complex in Aalsmeer, Netherlands, which facilitates the daily trade of around 34 million flowers and connects approximately 4,800 suppliers with 2,300 buyers.

The auction model plays a critical role by ensuring transparent price discovery, standardized quality grading, origin verification, and seamless logistics integration, enabling efficient large-scale international trade across diverse flower varieties. In 2025, Royal FloraHolland reported total turnover close to EUR 5 billion, with a year-on-year growth of about 4.5% in Q1 and record average prices across several specialty categories. At the same time, the Online / E-commerce channel is the fastest-growing segment, driven by digital platforms, direct-to-consumer models, and subscription-based delivery services.

Regional Insights

North America Specialty Cut Flower Market Trends

North America represents a significant demand hub for specialty cut flowers, led by the United States, which generated USD 7.6 billion in revenue in 2024 and is expected to grow at a CAGR of 6% through 2034, outpacing the global average. Domestic production is largely concentrated in California, which accounts for around 70% of locally grown flowers, while a substantial portion of demand is met through imports from Colombia, Ecuador, Kenya, and the Netherlands.

The U.S. market stands out for its innovation in distribution channels, particularly in subscription-based delivery services, which accounted for approximately 26% of online flower sales in 2025. These platforms combine cold-chain logistics with AI-driven personalization to enhance customer experience. Additionally, evolving regulatory frameworks such as MoCRA have increased transparency expectations, aligning with rising consumer demand for sustainably sourced and certified flowers, further supporting premiumization trends in the market.

Europe Specialty Cut Flower Market Trends

Europe remains the largest regional market for specialty cut flowers, accounting for approximately 48% of the global market value in 2025. This dominance is driven by key markets including the Netherlands, Germany, the United Kingdom, France, and Spain. The Netherlands serves as the central hub of global flower trade, managing nearly 50% of global exports through advanced greenhouse production, highly efficient cold-chain logistics, and the Royal FloraHolland auction system.

The Aalsmeer facility alone handles around 12 billion stems annually, setting global standards for pricing, quality, and traceability. Meanwhile, Germany, the U.K., and France are the largest consumption markets, supported by strong retail florist networks, supermarket sales, and online delivery services. Spain is emerging as a high-growth market, driven by tourism and hospitality demand. Across Europe, sustainability is becoming increasingly important, with certifications such as MPS, Fairtrade, and Rainforest Alliance influencing purchasing decisions and shaping future production practices.

Asia Pacific Specialty Cut Flower Market Trends

Asia Pacific is the fastest-growing region in the specialty cut flower market, supported by rapid urbanization, rising incomes, and increasing adoption of floral gifting and décor across China, Japan, India, and ASEAN countries. China leads regional growth, driven by expanding middle-class consumption, urban lifestyle trends, and strong e-commerce platforms such as JD.com and Tmall, which facilitate efficient farm-to-consumer delivery from Yunnan Province, the country’s primary production hub.

Japan represents a mature and high-value market, characterized by strong demand for premium flowers and deep-rooted cultural practices such as ikebana, which emphasize quality and presentation. In India, the market is growing rapidly due to rising disposable income, a large and expanding wedding industry, and increasing penetration of organized retail channels. Domestic production in regions such as Karnataka, Maharashtra, and Andhra Pradesh is further supported by government initiatives to strengthen floriculture infrastructure and improve supply chain efficiency.

Competitive Landscape

The global specialty cut flower market is highly fragmented, with a diverse structure spanning growers, breeders, trading intermediaries, and retail distribution channels. Leading companies such as Ball Horticultural Company, Dümmen Orange, Syngenta Flowers, Selecta One, and Sakata Seed Corporation maintain competitive advantage through advanced breeding programs, proprietary plant genetics, and global licensing systems. These innovations focus on improving vase life, developing unique flower varieties, and enhancing disease resistance.

At the same time, large-scale producers in Africa, including Karen Roses, Carzan Flowers Kenya Ltd, and the Rosebud Ltd. group, compete through operational scale, sustainability certifications, and strong access to European markets. A key emerging trend is the shift toward direct farm-to-retailer supply models, which allow growers to capture higher margins by bypassing traditional auction channels. Additionally, increasing digital integration and hybrid auction-direct systems continue to reshape market dynamics, with Royal FloraHolland remaining a benchmark for global trading infrastructure.

Key Developments:

- In April, 2025, Royal FloraHolland reported strong financial performance in 2024, with total product sales reaching approximately EUR 5.2 billion. Auction turnover for homegrown cut flowers rose by 4.5% year-on-year in Q1 2025, supported by record pricing in lilies, gerberas, and tulips amid tight supply conditions.

- In March 2025, Schiphol Airport announced a 15% expansion in chilled perishables handling capacity for 2025, strengthening the Netherlands’ leadership in global flower logistics by enabling efficient distribution of specialty cut flowers sourced from Africa, Latin America, and domestic greenhouse production.

- In February 2025, Kenya recorded USD 835 million in flower export revenues in 2024, with its global market share rising significantly from 8.6% in 2003 to 16.1% in 2024, highlighting its growing importance as a major supplier of roses and mixed cut flowers globally.

Companies Covered in Specialty Cut Flower Market

- Ball Horticultural Company

- Carzan Flowers Kenya Ltd

- Karen Roses

- Syngenta Flowers, Inc.

- Sher Holland BV

- The Queen's Flowers Corp

- Dümmen Orange

- Multiflora Group

- Danziger Group

- Rosebud Ltd.

- Karuturi Global Ltd.

- Selecta One

- Beekenkamp Group

- Florensis

- Sakata Seed Corporation

- Royal FloraHolland

Frequently Asked Questions

The global Specialty Cut Flower Market is estimated at US$ 40.7 Billion in 2026 and projected to reach US$ 49.0 Billion by 2033, growing at a CAGR of 2.7%. This aligns with broader cut flower industry trade data showing Royal FloraHolland processing EUR 5.2 billion annually and the U.S. cut flower market projected to grow at 6% CAGR through 2034.

The key growth drivers are the broadening of cut flower consumption into everyday personal and home décor use, with subscription models accounting for 26% of U.S. online floral sales, and e-commerce expansion supported by cold chain advances reducing post-harvest losses upto 25% in conventional supply chains, enabling year-round access to specialty varieties for wider consumer populations globally.

Annual Specialty Flowers lead with approximately 38% market share, anchored by roses as the globally dominant variety. Royal FloraHolland's Aalsmeer auction processes approximately 12 billion stems annually, with roses consistently achieving the highest trade volumes. Q1 2025 auction data confirmed record average prices in lilies, gerberas, and tulips, validating sustained strong professional demand for this segment.

Europe leads with approximately 46% of global market value, anchored by the Netherlands' Royal FloraHolland, processing EUR 5.2 billion in annual transactions and connecting 4,800 suppliers with 2,300 buyers daily. The Netherlands controls approximately 50% of global flower exports, and Schiphol Airport increased chilled flower handling capacity by 15% in 2025 to meet growing global distribution demand.

Sustainable and certified specialty flower production is the most strategically significant opportunity, with Fairtrade, Rainforest Alliance, and MPS-certified stems commanding premium pricing and increasingly required by major European and North American supermarket chains and hotel procurement programs, rewarding East African and Latin American growers who invest in verified sustainability credentials with durable premium market access.

Key players include Ball Horticultural Company, Dümmen Orange, Syngenta Flowers, Selecta One, Sakata Seed Corporation, Karen Roses, Carzan Flowers Kenya Ltd, Rosebud Ltd., Sher Holland BV, Beekenkamp Group, Florensis, Danziger Group, The Queen's Flowers Corp, Multiflora Group, and Karuturi Global Ltd., with Dümmen Orange and Syngenta Flowers holding strong positions in proprietary specialty variety breeding and global licensing.