- Specialty & Fine Chemicals

- Specialty Carbon Black Market

Specialty Carbon Black Market Size, Share, and Growth Forecast 2026 - 2033

Specialty Carbon Black Market by Product Type (Conductive Carbon Black, Pigment Carbon Black, Fiber Carbon Black, Food Contact Carbon Black), by Form (Powder, Granules, Pellets, Other Forms), by Application (Plastics, Paints & Coatings, Printing Inks & Toners, Batteries, Cables & Wires, Adhesives & Sealants, Rubber, Others), by End-Use, by Regional Analysis, 2026 - 2033

Specialty Carbon Black Market Size and Trend Analysis

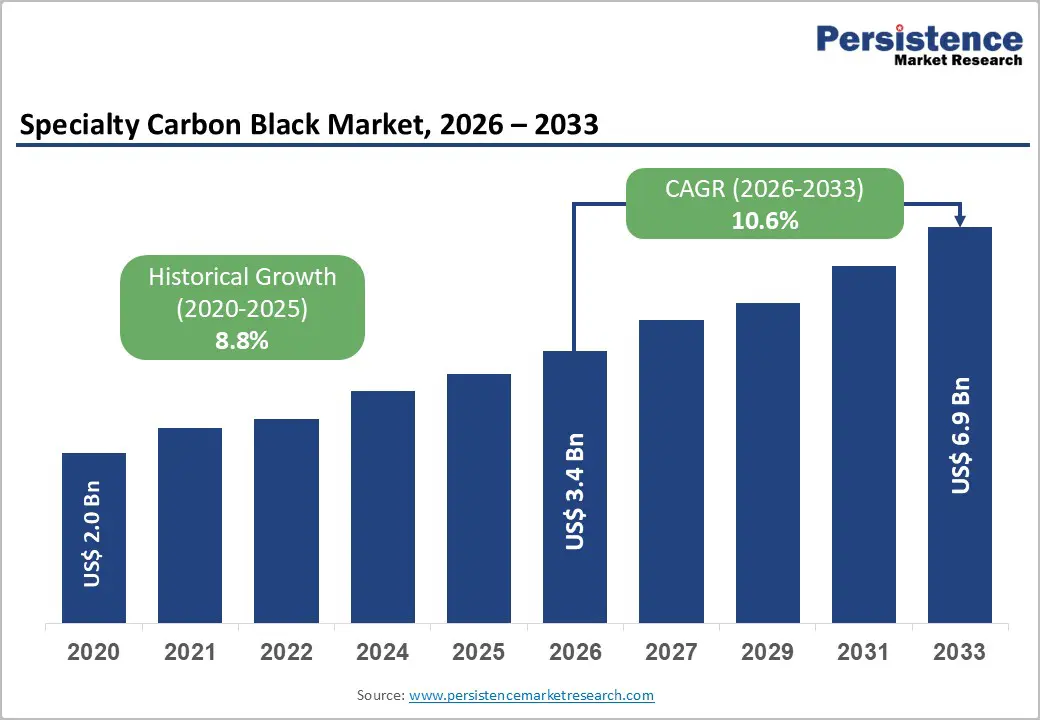

The global Specialty Carbon Black Market size is likely to be valued at US$ 3.4 Billion in 2026 and is expected to reach US$ 6.9 Billion by 2033, growing at a CAGR of 10.6% during the forecast period from 2026 to 2033. This accelerating growth is primarily driven by surging demand from the lithium-ion battery industry for conductive carbon black as an electrode material, rapid expansion in high-performance plastics and coatings applications, and escalating specialty chemical consumption across the automotive and electrical & electronics sectors globally.

Key Market Highlights

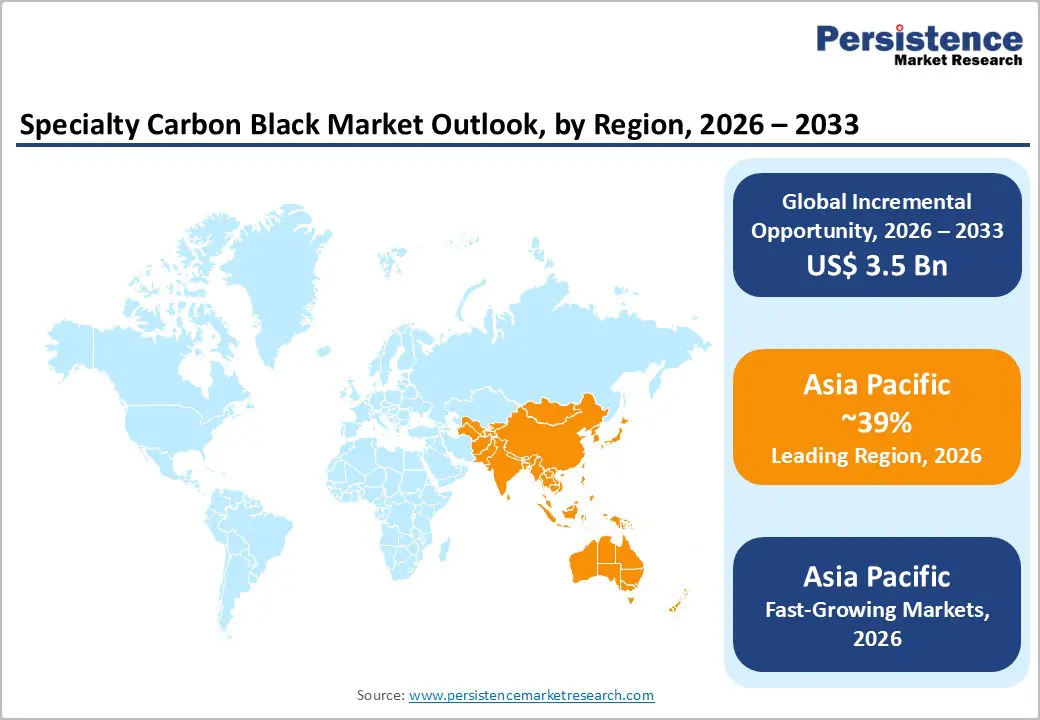

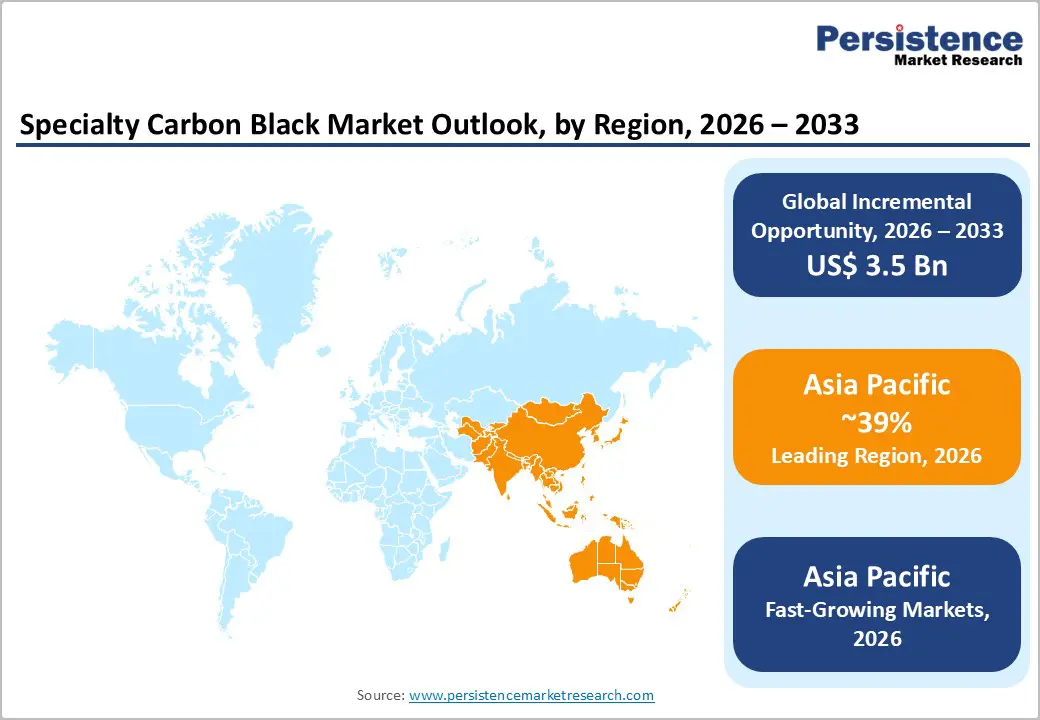

- Leading Region: Asia Pacific leads the global Specialty Carbon Black Market having 39% share, with China accounting for largest share in the global consumption driven by CATL's battery gigafactories, Japan's precision-grade producers Tokai Carbon and Mitsubishi Chemical, and India's scaling capacity from Himadri and Philips Carbon Black.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region with rising CAGR of 12.4%, propelled by India's PLI-scheme manufacturing expansion, China's 14th Five-Year Plan specialty chemical self-sufficiency targets, and surging battery-grade specialty carbon black demand from expanding EV and electronics manufacturing across ASEAN economies.

- Leading Segment: Conductive Carbon Black dominates with approximately 42% product type market share, driven by its indispensable role in lithium-ion battery electrode formulations, anti-static polymer compounds, and semiconducting cable insulation layers governed by IEC and ASTM International performance standards.

- Fastest-Growing Segment: The Batteries application segment is the fastest-growing category, with the IEA projecting global battery demand to surge from 950 GWh in 2023 to over 9,000 GWh by 2030, driving exponentially increasing procurement of battery-grade conductive specialty carbon black from producers globally.

- Key opportunity: The most significant market opportunity lies in sustainable and battery-grade specialty carbon black development, where the EU Battery Regulation (2023/1542) carbon footprint mandates and the US DOE's US$ 3 billion battery manufacturing investment are jointly compelling producers to deliver certified low-carbon, high-performance grades at commercial scale.

| Key Insights | Details |

|---|---|

|

Specialty Carbon Black Market Size (2026E) |

US$ 3.4 Billion |

|

Market Value Forecast (2033F) |

US$ 6.9 Billion |

|

Projected Growth CAGR (2026–2033) |

10.6% |

|

Historical Market Growth (2020–2025) |

8.8% |

Market Dynamics

Market Growth Drivers

Exponential Growth of Lithium-Ion Battery Manufacturing Driving Conductive Carbon Black Demand

The rapid global expansion of energy storage technologies, primarily driven by the growing adoption of electric vehicles and large-scale battery installations, is creating strong and consistent demand for conductive specialty carbon black. This material plays a vital role as an electron-conducting additive in both cathode and anode formulations used across most lithium-ion battery chemistries. According to the Net Zero by 2050 roadmap by the International Energy Agency, the global electric vehicle fleet is expected to reach nearly 300 million vehicles by 2030. Each battery pack typically requires between 1 and 3 kilograms of conductive carbon black, depending on energy density requirements.

In addition, the U.S. Department of Energy has allocated more than US$3 billion for battery manufacturing through the Bipartisan Infrastructure Law, strengthening domestic production capacity. Major battery manufacturers including CATL, LG Energy Solution, Panasonic, and Samsung SDI are expanding gigafactory capacity significantly through 2028, creating substantial procurement demand for high-performance conductive carbon black grades that meet strict battery performance requirements.

Rising Demand for Electrically Conductive Polymers in Advanced Electronics and EV Components

The increasing adoption of lightweight and high-performance polymer composites is creating a strong secondary demand driver for specialty carbon black beyond its traditional use as a pigment or rubber reinforcement material. Electrically conductive plastics, produced by incorporating specialized grades of conductive carbon black, are increasingly replacing metal components in many electronic and automotive applications. These materials are widely used in electrostatic discharge protection systems, electronic device housings, anti-static packaging, and automotive fuel system components.

The European Chemicals Agency has established regulatory frameworks under REACH that define strict quality and performance requirements for conductive additives, encouraging the use of high-quality specialty carbon black products. In addition, standards developed by the International Electrotechnical Commission for cable shielding, including IEC 60502 and IEC 60840, specify resistivity limits that can only be achieved through carefully engineered carbon black dispersion in polymer insulation materials. These compliance-driven requirements are encouraging cable manufacturers and electronics producers to increasingly adopt premium specialty carbon black grades.

Market Restraints

Stringent Environmental and Emission Regulations on Carbon Black Manufacturing

The production of specialty carbon black, which primarily uses the oil furnace process, generates emissions such as particulate matter, polycyclic aromatic hydrocarbons, and carbon dioxide. As environmental concerns increase, regulatory authorities across major production regions are imposing stricter emission standards on manufacturers. In Europe, the European Commission enforces regulations through the Industrial Emissions Directive (IED 2010/75/EU), which is currently being updated under Industrial Emissions Directive 2.0.

These rules require carbon black manufacturers to meet tighter emission limits and invest in advanced pollution control technologies such as filtration systems, tail-gas recovery units, and continuous emission monitoring equipment. In addition, the European Chemicals Agency is reviewing the classification of carbon black under REACH and the Classification, Labelling and Packaging regulation. These regulatory reviews create uncertainty for producers and may increase compliance costs. As a result, manufacturers must allocate significant capital toward environmental upgrades, which can slow new investment and impact the expansion plans of specialty carbon black production facilities across highly regulated markets.

Raw Material Price Volatility and Feedstock Dependency on Petroleum Derivatives

The production of specialty carbon black relies heavily on petroleum-based feedstocks such as coal tar, ethylene cracker residue, and fluid catalytic cracking decant oil. Since these raw materials are closely linked to global crude oil markets, price fluctuations in oil directly influence feedstock costs for carbon black manufacturers. According to the U.S. Energy Information Administration, crude oil prices have historically shown significant volatility, sometimes changing by more than 50 percent within a single year.

Such fluctuations can quickly affect the cost structure of specialty carbon black production. For high-performance grades, manufacturers also require feedstocks with consistent chemical composition to maintain precise surface characteristics and particle morphology. Variations in petroleum by-product quality can therefore require costly production adjustments and quality control measures. This strong dependency on petroleum-derived feedstocks exposes producers to margin pressure during periods of high oil prices and can reduce their pricing flexibility compared with alternative conductive additives used in cost-sensitive industrial applications.

Market Opportunities

Battery-Grade and Supercapacitor-Grade Specialty Carbon Black for Energy Storage Systems

The rapid global expansion of electrochemical energy storage systems is creating one of the largest growth opportunities for specialty carbon black manufacturers. Demand is rising across multiple applications, including electric vehicle batteries, stationary grid storage systems, and supercapacitors used in regenerative braking and industrial backup power systems. The International Energy Agency reported that global battery energy storage installations reached approximately 42 GWh in 2023, representing a 130 percent increase compared with the previous year. The agency expects this growth to continue as renewable energy generation expands and grid operators invest in energy storage solutions.

Battery manufacturers require conductive carbon black materials with precisely engineered properties, including controlled surface area, particle size, and low impurity levels. Companies such as Cabot Corporation and Orion S.A. are investing heavily in research and development to produce advanced battery-grade carbon black products. These innovations are expected to support the large-scale expansion of battery manufacturing capacity across North America, Europe, and Asia over the coming decade.

Sustainable and Bio-Based Specialty Carbon Black for Regulatory-Compliant Applications

Increasing environmental regulations and strong corporate sustainability commitments are creating new opportunities for specialty carbon black manufacturers that can offer low-carbon and renewable alternatives. Governments and regulatory bodies are encouraging industries to reduce reliance on fossil-based materials and adopt more sustainable chemical products. Under the European Green Deal, the European Commission introduced the Sustainable Chemicals Strategy, which promotes the development of environmentally friendly production technologies and materials.

In response, companies such as Orion S.A. and Cabot Corporation are investing in carbon black produced from renewable or recycled feedstocks and are working to lower the carbon intensity of their manufacturing processes. Industry organizations such as the Carbon Black Forum are also developing standardized life-cycle assessment methodologies to measure the environmental impact of carbon black products. Manufacturers that successfully commercialize certified low-carbon specialty grades can gain strong competitive advantages and attract sustainability-focused customers in the automotive, packaging, and consumer goods industries.

Category-wise Insights

Product Type Analysis

Conductive Carbon Black leads the product type segment, accounting for an estimated 42% of total specialty carbon black market revenues. Its strong position is driven by the wide range of critical applications it supports, including lithium-ion battery electrodes, anti-static plastic compounds, electrically conductive coatings, semiconducting cable shields, and fuel cell components. These materials are engineered with a high-structure morphology, large surface area, and optimized aggregate design, which allow efficient electron movement even at low loading levels in polymer matrices.

This enables manufacturers to achieve the desired electrical conductivity without affecting the mechanical strength or processing characteristics of the host material. Industry standards defined by organizations such as International Electrotechnical Commission and ASTM International set strict resistivity specifications for applications like cable insulation and anti-static packaging. Only high-quality conductive carbon black grades can meet these requirements. The rapid growth of electric vehicle and battery manufacturing worldwide remains the most important factor supporting the continued dominance of this segment.

Form Analysis

The Powder form segment leads the Specialty Carbon Black Market by form, accounting for nearly 47% of total form-segment revenues. Powdered specialty carbon black is widely preferred in applications that require precise and uniform dispersion into liquid or melt-phase systems. These applications include battery electrode slurries, conductive coating formulations, ink grinding processes, and plastic masterbatch compounding. In battery electrode manufacturing, especially in wet slurry coating processes for current collectors, powdered carbon black with controlled bulk density and excellent dispersibility is essential.

It helps create homogeneous electrode structures that directly influence battery cycle life and performance efficiency. Industry standards such as ASTM D1618 and ISO 787-17, developed by organizations like ASTM International and International Organization for Standardization, define key testing parameters including surface area and pH for powdered carbon black. Although granulated and pelleted forms offer advantages in handling and dust reduction for rubber and plastics manufacturing, high-value specialty applications in batteries, inks, and coatings largely depend on powdered grades, which supports this segment’s leading market position.

Application Analysis

The Batteries application segment has become the largest and fastest-growing application for specialty carbon black, accounting for an estimated 28% of total application-segment revenues. Lithium-ion battery manufacturing for electric vehicles, consumer electronics, and grid energy storage requires conductive carbon black additives in both cathode and anode formulations. These additives improve electron transport within the electrode, support structural stability during charge and discharge cycles, and help manage volume expansion of active materials.

Typically, battery formulations include around 1–4% conductive carbon black by weight. According to the International Energy Agency, global lithium-ion battery demand reached approximately 950 GWh in 2023 and is projected to exceed 9,000 GWh by 2030. Each gigawatt-hour of battery manufacturing capacity requires significant volumes of specialty carbon black, creating a large and sustained demand pipeline. Expansion plans announced by companies such as Contemporary Amperex Technology Co., Limited, Panasonic Corporation, LG Energy Solution, and Samsung SDI further highlight the scale of future procurement demand for battery-grade carbon black.

End-Use Analysis

The Electrical & Electronics segment holds the leading position in the Specialty Carbon Black Market by end use, representing approximately 31% of total market demand. This segment covers a wide range of high-value applications such as conductive polymer housings for electronic devices, electrostatic discharge (ESD) protective packaging materials, semiconducting cable insulation layers, printed circuit board substrates, and electrode materials used in rechargeable batteries and supercapacitors. Compliance standards established by organizations like the International Electrotechnical Commission define strict requirements for electromagnetic compatibility, anti-static safety, and cable performance.

These standards create a compliance-driven purchasing environment that requires certified specialty carbon black grades for electronics manufacturing. The rapid expansion of global data centers, telecommunications infrastructure, consumer electronics production, and EV power electronics continues to drive strong demand from this sector. Major producers such as Birla Carbon and Cabot Corporation have developed specialized Electrical & Electronics-grade carbon black product lines with tightly controlled surface area, structure, and impurity levels to meet IEC and ASTM compliance requirements.

Regional Insights

North America Specialty Carbon Black Market Trends

The United States serves as the central hub of the North American Specialty Carbon Black Market, driven by the rapid expansion of domestic battery manufacturing, strong demand from advanced plastics and coatings industries, and a strict regulatory framework that emphasizes the procurement of certified high-performance specialty grades. Government initiatives are significantly strengthening this ecosystem. The U.S. Department of Energy has committed more than US$3 billion to domestic battery manufacturing through the Bipartisan Infrastructure Law, while the Inflation Reduction Act offers advanced manufacturing tax incentives such as the 45X credit.

These programs are accelerating the development of a localized battery supply chain, generating long-term demand for battery-grade specialty carbon black produced within the U.S. or Free Trade Agreement partner countries. Cabot Corporation, headquartered in Boston, operates major specialty carbon black facilities across the region and is investing in next-generation battery carbon black technologies. Meanwhile, Canada is emerging as a growing demand center, supported by EV battery gigafactory investments from Stellantis–LG Energy Solution, Volkswagen PowerCo, and Honda–LG. Environmental oversight from the U.S. Environmental Protection Agency under the NESHAP program and product standards set by ASTM International further strengthen quality-driven procurement practices across the region.

Europe Specialty Carbon Black Market Trends

Europe represents one of the most technologically advanced and highly regulated specialty carbon black markets in the world. The market operates under strict regulatory frameworks such as the European Chemicals Agency’s REACH regulations and the Industrial Emissions Directive, which ensure high environmental and product safety standards. Demand is also increasing due to the region’s expanding battery manufacturing ecosystem. Germany acts as the key regional market, supported by its strong automotive manufacturing base with companies such as Volkswagen Group, BMW, and Mercedes-Benz.

The European Battery Alliance is promoting large-scale gigafactory investments across the region. Orion S.A., headquartered in Luxembourg, is a leading producer with production facilities in Germany and Belgium and is actively developing sustainable low-PAH and bio-based specialty grades aligned with the EU’s Sustainable Chemicals Strategy. Countries such as France and Spain are expanding battery production through the Important Projects of Common European Interest initiative. In addition, the United Kingdom is strengthening its battery supply chain under its Critical Minerals Strategy. The European Battery Regulation (EU 2023/1542) will further increase demand for low-carbon specialty carbon black.

Asia Pacific Specialty Carbon Black Market Trends

Asia Pacific leads the global Specialty Carbon Black Market in both production capacity and consumption. China alone accounts for more than 50% of global demand, supported by its massive battery manufacturing capacity, large automotive sector, electronics production, and advanced specialty chemical processing industries. The country’s 14th Five-Year Plan and long-term Made in China 2035 strategy emphasize domestic self-sufficiency in specialty chemicals, encouraging large investments in high-performance specialty carbon black manufacturing.

Major domestic players, including International CSRC Investment Holdings Co., Ltd., are expanding capacity to meet rising demand. CATL, the world’s largest battery manufacturer, holds a global market share exceeding 37% and is one of the largest consumers of battery-grade specialty carbon black as its gigafactory network expands. Japan also plays an important role with advanced producers such as Tokai Carbon Co., Ltd. and Mitsubishi Chemical Group Corporation, which focus on ultra-high-purity grades for electronics and printing inks. Meanwhile, India is emerging as a high-growth market, supported by Himadri Specialty Chemical Ltd and Philips Carbon Black Limited expanding capacity under the Production-Linked Incentive Scheme.

Competitive Landscape

The global Specialty Carbon Black Market shows a moderately consolidated competitive structure, where a limited number of multinational specialty chemical producers hold a significant share of industry revenue. Leading companies such as Cabot Corporation, Orion S.A., Birla Carbon, Tokai Carbon Co., Ltd., and Himadri Specialty Chemical Ltd form the core leadership group of the market. These companies differentiate themselves through advanced furnace process technologies, diverse application-specific product portfolios, and well-established global production networks. Key competitive advantages include precise surface area engineering, advanced particle morphology control, and the production of low-impurity grades required for high-performance applications such as batteries and food-contact materials.

Companies are also focusing on strict regulatory compliance across major global markets to maintain credibility and customer trust. Strategic priorities include acquiring niche specialty producers, expanding manufacturing capacity near EV battery gigafactories, and increasing investment in research and development. In addition, many players are exploring sustainable and bio-based carbon black production technologies and entering long-term supply partnerships with battery manufacturers and EV original equipment manufacturers to co-develop application-specific specialty grades.

Key Market Developments

- In January 2025: Cabot Corporation introduced its LITX HP specialty conductive carbon black product line designed for advanced lithium-ion batteries. The material improves conductivity, cycle life, and electrode performance, supporting high-energy-density battery technologies including silicon-anode and next-generation energy storage systems.

- In September 2024: Orion S.A. expanded its specialty carbon black production line at the Ravenna facility in Italy, increasing capacity for premium conductive and battery-grade materials. The expansion helps regional battery manufacturers comply with the European Battery Regulation carbon-footprint reporting requirements.

- In March 2023: Himadri Specialty Chemical Ltd announced a US$120 million investment to expand specialty carbon black and anode material production capacity in India. The initiative aims to strengthen the domestic EV battery supply chain while increasing exports to Southeast Asia and Europe.

Companies Covered in Specialty Carbon Black Market

- Omsk Carbon Group

- Tokai Carbon Co., Ltd.

- Atlas Organics Private Limited

- Continental Carbon Company

- Birla Carbon

- Cabot Corporation

- Oak Investment Partners

- Himadri Specialty Chemical Ltd

- Philips Carbon Black Limited

- Orion S.A.

- Ralson Carbon Black Limited

- Mitsubishi Chemical Group Corporation

- International CSRC Investment Holdings Co., Ltd.

- Imerys

- Aditya Birla Chemicals

- Sid Richardson Carbon & Energy Co.

- Jiangxi Black Cat Carbon Black Co., Ltd.

- Evonik Industries AG

- Columbian Chemicals Company

Frequently Asked Questions

The global Specialty Carbon Black Market is valued at US$ 3.4 Billion in 2026 and is projected to reach US$ 6.9 Billion by 2033, advancing at a CAGR of 10.6% through the forecast period. The market recorded a historical CAGR of 8.8% between 2020 and 2025, underpinned by accelerating battery manufacturing investment and high-performance plastics demand globally.

The foremost demand drivers are the exponential scale-up of global lithium-ion battery manufacturing, with the IEA projecting capacity to exceed 9,000 GWh by 2030, combined with the growing adoption of electrically conductive polymer composites in EV components, electronics, and cable systems. The U.S. DOE's US$ 3 billion battery manufacturing investment and the EU Battery Regulation (2023/1542) are jointly accelerating domestic procurement of battery-grade specialty carbon black.

Conductive Carbon Black leads the product type segment with approximately 42% market share, driven by its indispensable role as an electron-pathway additive in lithium-ion battery cathode and anode formulations, anti-static polymer compounds, and semiconducting cable insulation layers certified to IEC 60502 and IEC 60840 standards. Its performance advantages across high-growth applications establish durable demand leadership through 2033.

Asia Pacific holds the leading regional position, with China consuming over 50% of global specialty carbon black volumes, anchored by CATL's globally dominant battery manufacturing operations. Japan's precision-grade producers Tokai Carbon Co., Ltd. and Mitsubishi Chemical Group Corporation, and India's expanding capacity at Himadri Specialty Chemical Ltd and Philips Carbon Black Limited, further reinforce the region's market leadership.

The greatest opportunity lies in commercializing sustainable and battery-grade specialty carbon black that simultaneously meets the EU Battery Regulation (2023/1542) carbon footprint declaration requirements and the performance specifications of next-generation battery chemistries. With the IEA projecting battery demand to grow tenfold by 2030, producers delivering certified low-carbon, high-surface-area specialty grades at commercial scale will capture disproportionate market share.

Leading companies include Cabot Corporation, Orion S.A., Birla Carbon, Tokai Carbon Co., Ltd., Himadri Specialty Chemical Ltd, Philips Carbon Black Limited, Omsk Carbon Group, Mitsubishi Chemical Group Corporation, Continental Carbon Company, International CSRC Investment Holdings Co., Ltd., Imerys, Evonik Industries AG, Ralson Carbon Black Limited, and Sid Richardson Carbon & Energy Co., among other regional specialty producers and emerging sustainable carbon black developers.