- LED & Lighting (Optoelectronics)

- Solid State Lighting Market

Solid State Lighting Market Size, Share, and Growth Forecast 2026 - 2033

Solid State Lighting Market by Technology (LED, OLED, PLED), Installation Type (Retrofit, New Installation), Application (Residential, Industrial & Commercial, Automotive & Transportation, Public Infrastructure, Other), and Regional Analysis for 2026 - 2033

Solid State Lighting Market Size and Trend Analysis

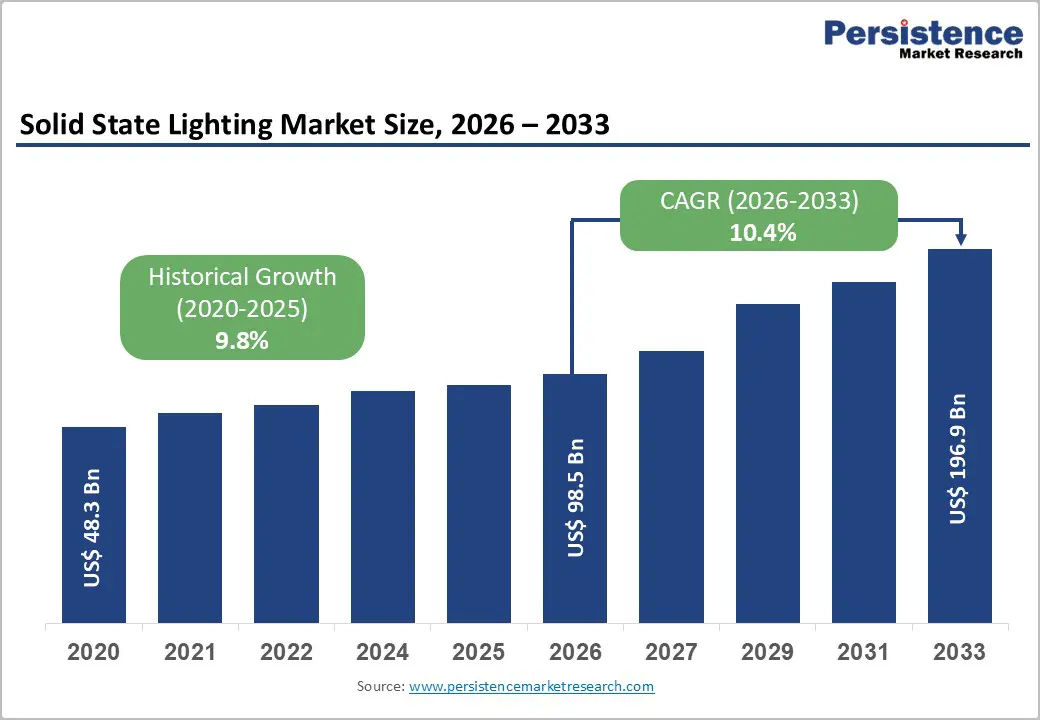

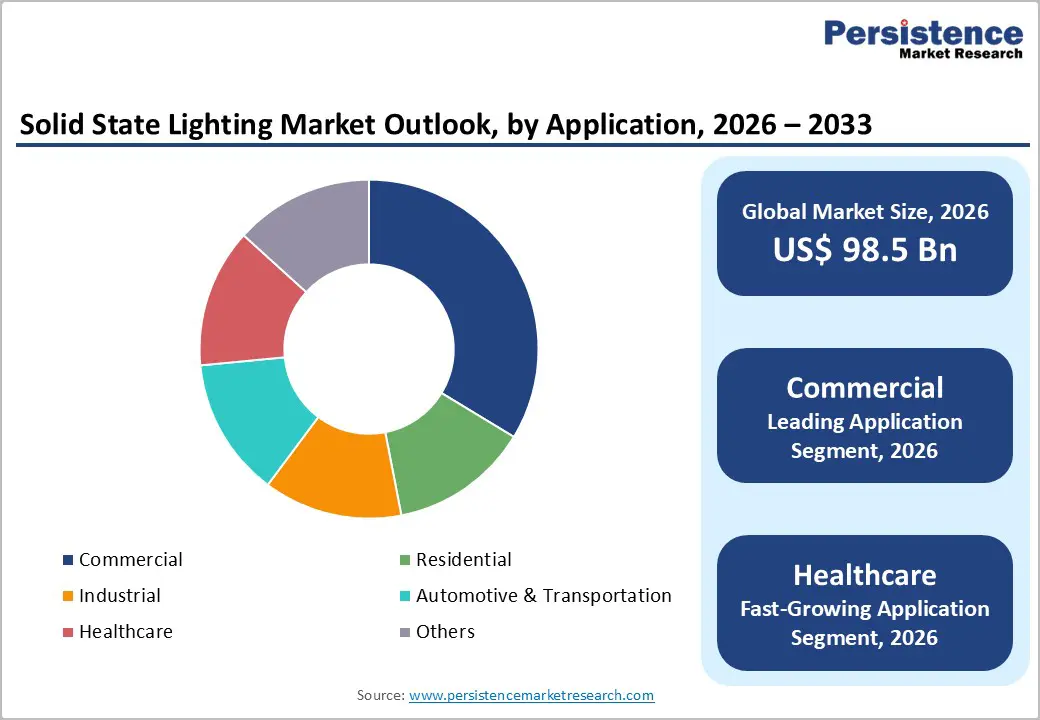

The global Solid State Lighting market is valued at US$ 98.5 Bn in 2026 and is projected to reach US$ 196.9 Bn by 2033, growing at a CAGR of 10.4% between 2026 and 2033.

This robust expansion is underpinned by a confluence of powerful demand drivers. Stringent energy efficiency mandates from governments across North America, Europe, and Asia-Pacific, coupled with the rapidly declining cost of LED and OLED components, have accelerated mainstream adoption. The International Energy Agency (IEA) has emphasized that all lighting sales must transition to LED technology by 2025 to meet Net Zero Emissions by 2050 targets. Additionally, the proliferation of smart city programs, Internet of Things (IoT)-enabled lighting infrastructure, and rising construction activity in developing economies are collectively amplifying market momentum through the forecast horizon.

Key Market Highlights

- Leading Region: North America is the leading revenue-generating region in the global Solid State Lighting market, capturing approximately 36% of global market share, supported by an advanced regulatory framework, mature commercial infrastructure, and high smart lighting adoption rates.

- Fastest Growing Region: Asia-Pacific also registers the highest growth rate at a CAGR of approximately 12%, led by China's smart city programs, India's UJALA scheme, and ELCOMA Vision 2024, and expanding OLED adoption in Japan and South Korea.

- Dominant Segment: The LED segment commands approximately 69% of the global SSL market, underpinned by its unmatched energy efficiency, a lifespan of 25,000–50,000 hours, and regulatory support from the IEA, U.S. DOE, and EU Ecodesign Directive.

- Fastest Growing Segment: OLED technology is the fastest-growing SSL segment, with European panel production rising 35% as per the European Commission, driven by automotive lighting innovation, architectural applications, and the proliferation of flexible, thin-form display-grade illumination.

- Key Market Opportunity: The convergence of Solid State Lighting with IoT platforms and smart building automation represents the most significant market opportunity, with energy savings of 30–50% achievable through connected adaptive systems, positioning smart SSL as a critical enabler of global net-zero infrastructure commitments.

DRO Analysis

Market Growth Drivers

Stringent Government Regulations and Energy Efficiency Mandates Driving SSL Adoption

One of the key drivers for the Solid State Lighting market is the increasing number of regulatory mandates focused on energy consumption in the built environment. The U.S. Department of Energy (DOE) reported over 87 million LED installations in U.S. households and commercial buildings by 2023, largely influenced by initiatives under the Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007. In 2017 alone, LED lighting resulted in energy savings of 1.1 quads, translating to approximately $12 billion in cost savings.

Furthermore, the European Union's Ecodesign Directive, implemented in 2009, initiated a phase-out of incandescent lamps. The International Energy Agency's 4E Solid State Lighting (SSL) Annex continues to enforce rigorous LED quality and performance standards, compelling manufacturers and end users to adopt compliant, high-efficacy systems. This ongoing regulatory pressure is a significant, long-term catalyst for the global demand for Solid State Lighting.

Rapid Urbanization and Smart City Initiatives Creating Large-Scale SSL Demand

Accelerating urbanization, particularly across Asia-Pacific, Latin America, and Sub-Saharan Africa, is generating substantial infrastructure investment that directly benefits the Solid State Lighting market. The IEA reported that urban LED street lighting coverage expanded to 56% globally by the end of 2023, driven by cities investing in smart, sustainable infrastructure to meet decarbonization goals. IoT-enabled SSL systems facilitate adaptive controls, occupancy sensing, and remote management, enabling energy savings of 30–50% compared to conventional systems.

In India, the government's bulk procurement programs under initiatives such as the ELCOMA Vision 2024 roadmap have driven down LED lamp costs and accelerated market penetration in lower-income households. In China, eight new lighting standards were implemented in 2024, raising efficacy thresholds and compelling domestic manufacturers to scale smart product lines, further reinforcing smart city lighting demand across the Asia-Pacific corridor.

Market Restraints

High Initial Capital Investment Limiting Adoption Among Cost-Sensitive Buyers

Despite the compelling long-term economics of Solid State Lighting, the upfront cost of LED luminaires, OLED panels, and associated smart control systems remains a significant barrier, particularly for residential consumers and small businesses in emerging markets. Although LED lamp prices have declined substantially, high-performance commercial-grade systems and OLED installations continue to carry premium price tags.

According to the DOE, the payback period for LED retrofit tubes replacing linear fluorescent lamps can be as short as four months in some applications; however, integrated smart lighting systems with sensors, wireless controls, and data analytics platforms require substantially higher capital outlay. In markets where upfront cost sensitivity is high and financing mechanisms are underdeveloped, this barrier continues to slow the penetration of advanced SSL solutions and moderate overall market growth rates.

Technological Complexity and Interoperability Challenges Hindering Mass Deployment

The increasing integration of SSL systems with smart building management platforms, IoT networks, and energy management systems introduces substantial technical complexity that can impede large-scale deployment. Interoperability between products using different wireless protocols, such as Zigbee, Wi-Fi, Z-Wave, and Matter, remains a persistent challenge, raising integration costs and discouraging standardization-averse procurement. The IEA's 4E SSL Annex has explicitly noted the need for improved policy measures and better quality metrics to protect markets from substandard products that can erode consumer confidence.

Furthermore, maintaining adequate power density in OLED and polymer LED (PLED) systems, where the semiconductor conductivity is inherently lower, poses ongoing engineering hurdles. These technological and interoperability constraints add layers of complexity to adoption and increase the total cost of ownership for operators seeking fully connected lighting ecosystems.

Market Opportunities

Emergence of OLED Technology as a High-Growth, High-Margin Segment

Organic Light Emitting Diode (OLED) technology represents one of the most compelling growth opportunities within the broader SSL landscape. OLED panels, characterized by their thin form factor, design flexibility, superior color rendering, and suitability for curved and transparent surfaces, are gaining rapid traction in automotive interior and exterior lighting, high-end architectural applications, and premium consumer electronics displays.

According to the European Commission's Energy Efficient Lighting Report (2023), OLED lighting panel production in Europe increased by 35%, driven by demand in automotive, architectural, and residential sectors, prioritizing thin and flexible lighting solutions. The automotive sector, in particular, is experiencing a convergence of OLED and Micro-LED technologies. ams OSRAM and Nichia Corporation have both developed dedicated micro-LED solutions that deliver a more than 100-fold increase in resolution compared to existing matrix LED systems, unlocking significant premium-pricing power for manufacturers.

Smart SSL Integration with IoT and Building Automation Systems

The confluence of Solid State Lighting with Internet of Things (IoT) technology and intelligent building management systems presents a transformative opportunity for market participants. Smart SSL solutions enable real-time monitoring, remote operation, occupancy-based dimming, and predictive maintenance, features increasingly mandated by green building standards and net-zero construction codes. The global smart lighting market, a direct adjacency of the SSL market, is growing rapidly, driven by large-scale deployments across commercial, public infrastructure, and industrial sectors.

The IoT-enabled lighting solutions became increasingly mainstream in commercial spaces in 2025, with energy savings of 30–50% achievable through protocols such as Zigbee and Wi-Fi. In Canada, the city of Toronto launched a $25 million renovation to replace municipal lights with IoT-capable smart systems in 2024. Such deployments underscore the systemic shift toward lighting-as-a-platform, creating recurring revenue streams for connected SSL solution providers.

Category-wise Insights

Technology Analysis

The LED (Light Emitting Diode) segment dominates the global Solid State Lighting market, accounting for approximately 69% of total market revenue. This dominant share is rooted in LED technology's unmatched combination of energy efficiency, longevity, and cost competitiveness relative to legacy lighting alternatives. Compared to incandescent lamps, LEDs offer 80–90% energy savings, and compared to fluorescent lamps, savings of 50–60% are achievable, as documented by the IEA.

The U.S. DOE projects that LED lamps and luminaires will comprise 84% of all U.S. lighting installations by 2035, with cumulative energy savings of 78 quads possible by that date if program efficiency targets are met. The DOE's 349 competitively selected R&D projects funded under its SSL Program have yielded 483 patents and a portfolio of 364 directly traceable commercial products. The IEA's 4E SSL Annex further reinforces LED dominance by setting efficacy standards that smaller-format alternatives, such as PLED and non-integrated OLED panels, are not yet fully equipped to meet at scale.

Installation Type Analysis

The Retrofit segment is a significant leader in the Installation Type category, comprising approximately 58% of the Solid-State Lighting (SSL) market revenue. Retrofit solutions allow businesses, municipalities, and homeowners to upgrade to energy-efficient SSL systems without extensive electrical renovations, providing immediate energy savings and regulatory compliance at lower upfront costs compared to new construction. This segment remains robust due to the aging global building stock, with the European Union's Ecodesign and Energy Efficiency Directives mandating compliance timelines that make retrofitting a legal necessity.

In North America, utility rebate programs, along with European subsidies like Germany's KfW276 and various government incentives in the Asia-Pacific region, further enhance the financial viability of retrofits. The International Energy Agency (IEA) highlights that direct drop-in LED replacement products minimize the need for fixture changes, thereby lowering installation barriers and solidifying retrofitting as the most practical and scalable approach to global lighting modernization.

Application Analysis

The Industrial & Commercial segment is the leading application category in the Solid State Lighting market, accounting for approximately 42% of global application revenue. Non-residential spaces like offices, warehouses, and factories have the highest demand for lumens and the greatest incentive for energy-efficient LED upgrades. The U.S. DOE forecasts that energy savings from LED lighting in these sectors will contribute significantly to the estimated 569 TWh in annual savings by 2035.

The DOE SSL Program estimates that $710 billion in avoided energy costs and 2.1 billion metric tons of avoided CO? emissions are achievable through advanced lighting systems by 2035, with commercial and industrial applications contributing the largest share. The Illuminating Engineering Society (IES) and ENERGY STAR Program of the U.S. Environmental Protection Agency (EPA) continue to set performance benchmarks that channel commercial procurement toward premium SSL systems, reinforcing this segment's leadership.

Regional Insights

North America Solid State Lighting Market Trends & Analysis

North America is the leading revenue-generating region in the global Solid State Lighting market, capturing approximately 36% of global market share, supported by an advanced regulatory framework, mature commercial infrastructure, and high smart lighting adoption rates. The DOE's Connected Communities program and ENERGY STAR labeling initiative continue to drive commercial adoption of smart SSL systems. Commercial building smart lighting installation increased by 28% in 2024 across North America.

U.S. Solid State Lighting Market Size: The United States accounts for the dominant share of North American SSL revenues, estimated at approximately US$ 30 Bn in 2026, supported by federal efficiency mandates, widespread commercial retrofit activity, and strong smart home penetration in residential segments. Recent U.S. tariff escalations on imported electronic components and semiconductors, particularly those originating from China, are creating supply chain realignment pressures, encouraging domestic LED component manufacturing investment while potentially elevating near-term product costs for end users.

Europe Solid State Lighting Market Trends, Drivers, & Insights

Europe is holding approximately 28% of the global market share, underpinned by the European Union's comprehensive regulatory architecture. The EU Ecodesign Directive, Energy Efficiency Directive, and Energy Performance of Buildings Directive (EPBD) collectively mandate progressive transitions to efficient lighting across residential, commercial, and public-sector applications. However, U.S. tariff actions and related geopolitical tensions, including U.S.-European trade frictions over semiconductor supply chains, are creating procurement uncertainty for European manufacturers reliant on North American component suppliers. Countries like Germany, the U.K., and France remain the largest national contributors.

Germany Solid State Lighting Market Size: Germany is the largest SSL market in Europe, estimated at approximately US$ 8 Bn in 2026, driven by robust industrial LED adoption, KfW276 energy retrofit subsidies, and smart city deployments in Berlin, Munich, and Hamburg.

U.K. Solid State Lighting Market Size: The United Kingdom SSL market is estimated at approximately US$ 6 Bn in 2026, supported by MEPS (Minimum Energy Performance Standards) for lamps, government net-zero commitments, and accelerating commercial building retrofits across London and other major urban centers.

France Solid State Lighting Market Size: France's SSL market is estimated at approximately US$ 5 Bn in 2026, with growth driven by the French government's energy renovation plan for public buildings, the widespread replacement of sodium street lamps with LED systems, and incentives under the MaPrimeRénov' residential energy efficiency scheme.

Asia Pacific Solid State Lighting Market Drivers & Analysis

Asia-Pacific is the fastest-growing regional market, accounting for approximately 32% of global revenues, owing to its dual role as the world's dominant SSL manufacturing hub and its massive, urbanization-driven consumption base. Geopolitical factors, including U.S.-China trade tensions, semiconductor export restrictions, and supply chain diversification initiatives, are reshaping regional sourcing strategies, accelerating investment in Southeast Asia, Vietnam, and India as alternative manufacturing locations.

China Solid State Lighting Market Size: China is the single largest national SSL market globally, estimated at approximately US$ 22 Bn in 2026, driven by massive government-backed smart city programs, large-scale infrastructure construction, and the domestic scaling of LED manufacturing under the China Solid State Lighting Alliance (CSA).

India Solid State Lighting Market Size: India's SSL market is estimated at approximately US$ 6 Bn in 2026, propelled by the government's Bright Road program, the UJALA scheme, which has already distributed over 360 million LED bulbs nationally, and rapidly expanding urban infrastructure development.

Japan Solid State Lighting Market Size: Japan is estimated at approximately US$ 5 Bn in 2026, with demand anchored by premium automotive OLED and Micro-LED applications, the Japan LED Lighting Association (JLEDS) promoting energy efficiency standards, and large-scale commercial LED retrofits supported by METI energy policies.

Competitive Landscape

The global solid state lighting market exhibits a moderately consolidated structure, with a small cohort of multinational corporations, including Signify, ams OSRAM, Samsung Electronics, Nichia Corporation, and Seoul Semiconductor, controlling a significant share of global revenues and intellectual property. These leaders differentiate through vertical integration, proprietary phosphor formulations, patent portfolios, and ecosystem partnerships. Mid-tier manufacturers increasingly pursue niche specialization, such as horticultural LED, medical lighting, or UV-C disinfection, to avoid direct commoditization pressure in the mainstream segment. Moderate merger and acquisition activity is reshaping the landscape, with companies targeting portfolio expansion and supply chain localization.

Key Market Developments

- October 2025: Nichia Corporation and ams OSRAM signed a comprehensive broad patent cross-license agreement covering thousands of patent-protected innovations in LED and laser technologies, signaling deepened IP collaboration and reducing litigation risk across the industry.

- June 2024: OSRAM launched a new generation of high-power LEDs with improved luminous efficacy, supporting sophisticated lighting controls designed to reduce energy consumption across commercial, industrial, and municipal applications while maintaining superior light quality.

- January 2024: Philips Lighting (Signify) announced a new range of smart LED bulbs with enhanced connectivity, integrating with voice-activated assistants and mobile applications to enable dynamic lighting control, occupancy sensing, and predictive maintenance for residential and commercial buildings.

Top Companies in Solid State Lighting Market

Signify (Netherlands) is the world's largest lighting company. The company operates across the full SSL value chain, from LED components through smart system integration under its Philips and Interact brands, and has consistently invested in connected lighting platforms, IoT ecosystem development, and sustainability-linked business models.

ams OSRAM (Austria/Germany) is a global leader in sensing and illumination, with approximately 19,700 employees and over 13,000 patents granted or applied. The company differentiates through a vertically integrated portfolio spanning LED emitters, drivers, optics, and sensors. Its pioneering work in automotive micro-LED adaptive driving beam systems and UV-C LED disinfection represents its highest-growth verticals.

Nichia Corporation (Japan), as the inventor of high-brightness blue LEDs and white LED lamps, commands an unparalleled position in the global SSL market through its phosphor technology, patent strength, and product quality. Nichia recently developed mass-transfer micro-LED technology for automotive adaptive driving beams, achieving a 100-fold improvement in resolution over conventional matrix LED systems. The company's focus on medical, horticultural, and high-CRI lighting applications positions it at the premium end of the SSL value chain.

Companies Covered in Solid State Lighting Market

- Signify

- ams OSRAM

- Samsung Electronics

- Nichia Corporation

- Seoul Semiconductor

- LG Innotek

- General Electric

- Acuity Brands

- Panasonic Holdings

- Mitsubishi Electric

- Eaton Corporation

- Lumileds

- Everlight Electronics

Frequently Asked Questions

The global Solid State Lighting market is valued at US$ 98.5 Bn in 2026 and is projected to reach US$ 196.9 Bn by 2033, growing at a CAGR of 10.4%. This growth reflects the rapid displacement of conventional lighting by energy-efficient LED and OLED technologies driven by regulatory mandates and declining component costs.

The primary demand drivers include stringent government energy-efficiency regulations, such as the U.S. DOE Solid-State Lighting Program, the EU Ecodesign Directive, and IEA SSL Annex standards, as well as rapid urbanization, smart-city investments, the proliferation of IoT-enabled connected lighting, and significant reductions in LED manufacturing costs over the past decade.

The LED (Light Emitting Diode) segment dominates the global SSL market with approximately 69% revenue share. Its supremacy is driven by 80–90% energy savings versus incandescent lamps, operational lifespans of 25,000–50,000 hours, broad application coverage, and robust support from global regulatory bodies including the IEA, DOE, and European Commission.

North America is the leading revenue-generating region in the global Solid State Lighting market, capturing approximately 36% of global market share, supported by an advanced regulatory framework, mature commercial infrastructure, and high smart lighting adoption rates.

The integration of Solid State Lighting with Internet of Things (IoT) platforms and smart building automation systems represents the most compelling opportunity. IoT-enabled adaptive SSL solutions deliver energy savings of 30–50%, support real-time monitoring and predictive maintenance, and align directly with global net-zero building mandates, creating a growing addressable market for connected lighting solution providers.

The leading companies operating in the global Solid State Lighting market include Signify, ams OSRAM, Samsung Electronics, Nichia Corporation, Seoul Semiconductor, LG Innotek, Acuity Brands, General Electric / GE Lighting, Panasonic Holdings, Lumileds, Eaton Corporation, Mitsubishi Electric, and Everlight Electronics.