- Electrical Equipment & Services

- Small Hydropower Market

Small Hydropower Market Size, Share, and Growth Forecast 2026 - 2033

Small Hydropower Market by Capacity (Pico Hydropower (Up to 5 kW), Micro Hydropower (5 kW - 100 kW), Mini Hydropower (100 kW - 1 MW), Small Hydropower (1 MW - 10 MW)), by Component (Electromechanical Equipment (Turbines, Generators, Control Systems), Civil Works, Electrical Infrastructure, Others), Plant Type, Application, and Regional Analysis, 2026 - 2033

Small Hydropower Market Size and Trend Analysis

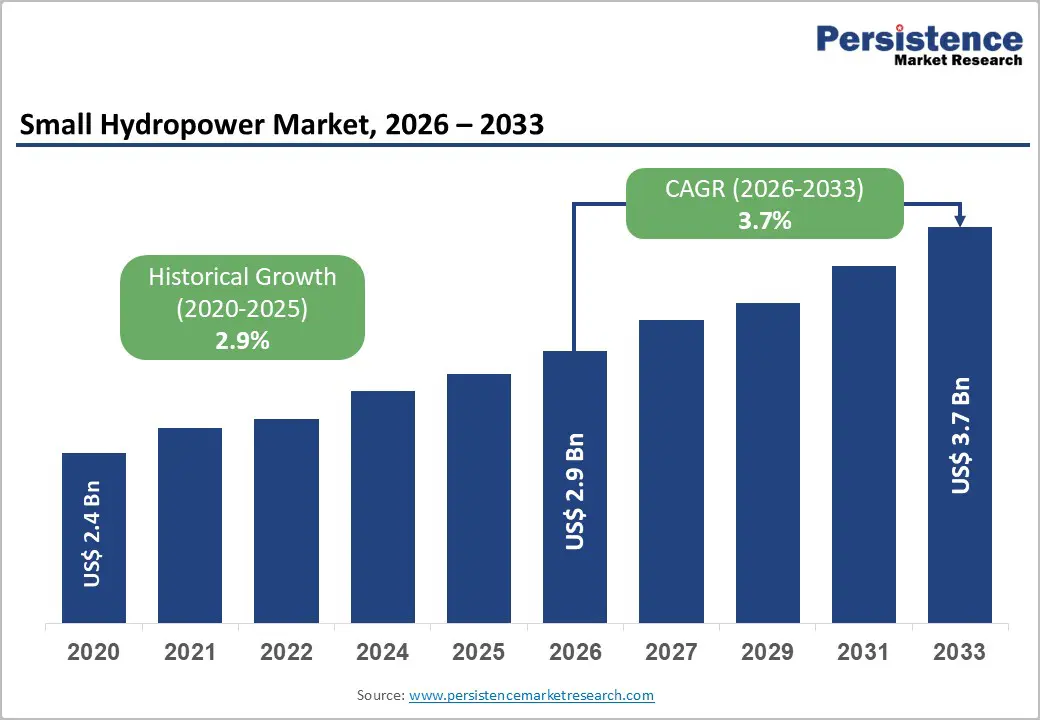

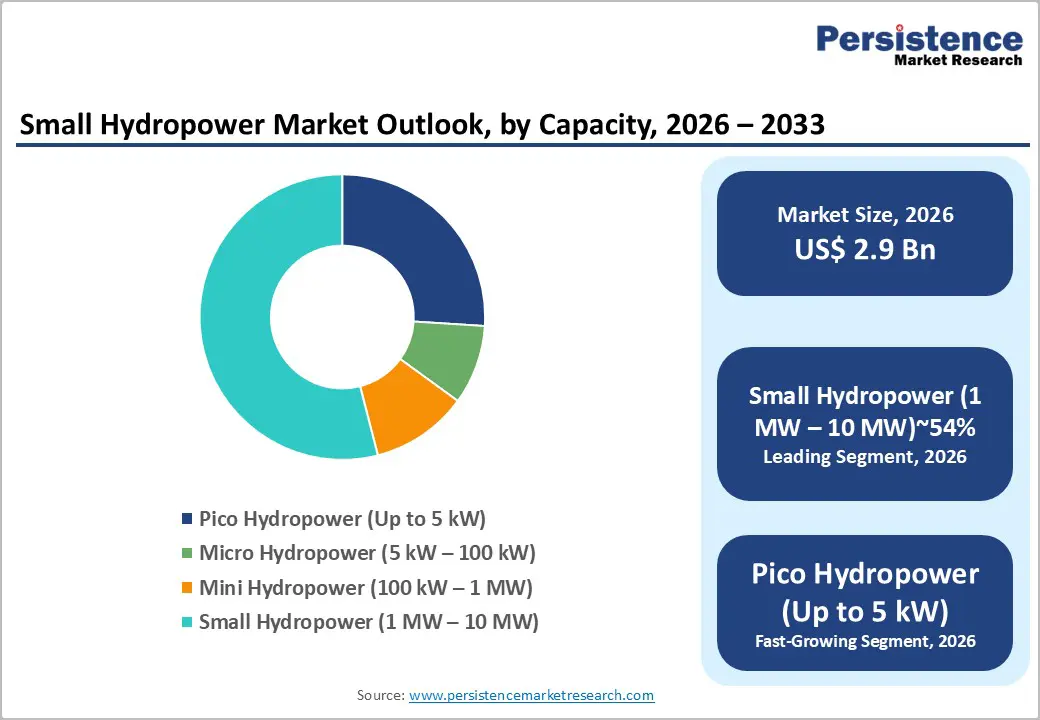

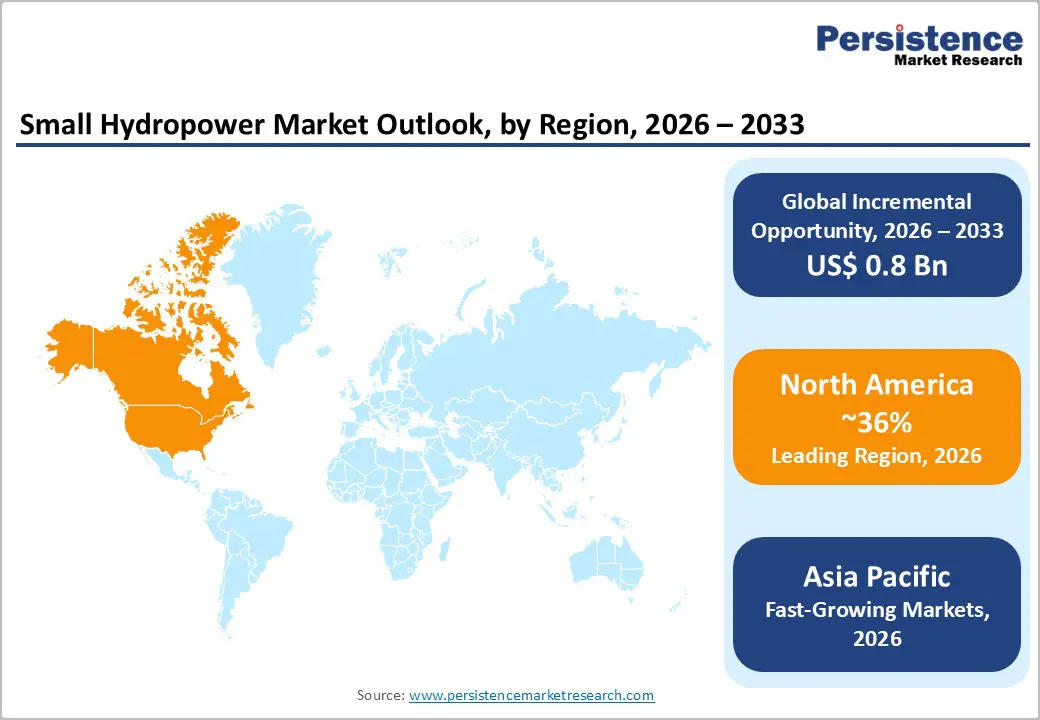

The global small hydropower market size is likely to be valued at US$ 2.9 Billion in 2026 and is expected to reach US$ 3.7 Billion by 2033, growing at a CAGR of 3.7% during the forecast period from 2026 and 2033.

The push for decentralized renewable energy to achieve net-zero targets is the overriding force propelling this market. Governments worldwide are prioritizing small hydro for its low environmental footprint and rapid deployment, particularly in remote areas lacking grid access.

Key Market highlights

- Leading region: North America leads the small hydropower market holding 36% share, due to abundant river systems and strong renewable policies, driving continuous capacity additions and technology deployment across rural and mountainous regions.

- Fastest Growing Region: Asia Pacific is the fastest growing region with a CAGR of 5.1%, as countries increasingly retrofit irrigation canals and promote rural electrification programs, creating strong demand for decentralized small hydropower systems across agricultural and remote communities.

- Dominant Segment: The 1-10 MW capacity segment dominates the market, with a 54% share, because it offers an ideal balance between power output and investment cost, making it highly suitable for grid integration and utility-scale renewable energy projects.

- Fastest Growing Segment: Pumped storage hydropower is emerging as the fastest-growing segment as utilities integrate more solar and wind energy, using pumped storage systems to balance electricity supply and stabilize renewable-heavy power grids.

- Key Market Opportunity: Canal-based hydropower retrofits across global irrigation networks present strong opportunities, as developers can install turbines in existing water infrastructure, enabling low-cost renewable power generation with faster permitting and attractive returns.

| Key Insights | Details |

|---|---|

| Small Hydropower Market Size (2026E) | US$ 2.9 Billion |

| Market Value Forecast (2033F) | US$ 3.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 3.7% |

| Historical Market Growth (2020 - 2025) | 2.9% |

Market Dynamics - Market Growth Drivers

Government Policies Driving Small Hydropower Expansion through Renewable Decentralization and Rural Electrification Programs Worldwide

Government policies supporting renewable energy and rural electrification are strongly driving the growth of small hydropower projects worldwide. National renewable energy targets and decentralized power programs are encouraging the development of small hydro systems, especially in remote and off-grid regions. According to the International Renewable Energy Agency (IRENA), small hydropower plays a crucial role in delivering reliable baseload power without requiring large-scale storage systems, making it highly suitable for rural energy access initiatives.

In many developing countries, governments offer financial incentives and subsidies that cover up to 70% of the capital investment, significantly lowering project costs and encouraging local developers to initiate projects. As a result, thousands of micro- and mini-hydro installations have been built, providing reliable electricity to more than 100 million off-grid users worldwide. Policy support is also helping simplify permitting processes and encouraging the integration of small hydropower with solar and wind systems in hybrid microgrids. This combination improves energy reliability and protects communities from fossil fuel price fluctuations and climate-related energy disruptions.

Technological Advancements in Low-Head Turbine Systems Expanding Small Hydropower Potential Across Previously Unviable Water Sites

Technological innovation in low-head turbine systems is opening new opportunities for small hydropower development at sites that were previously considered economically unviable. Modern turbine designs, such as crossflow and axial-flow turbines, are capable of operating efficiently even at very low water heads. Today’s advanced systems can achieve efficiency levels of nearly 85-90% with water heads as low as two meters, making it possible to generate power from irrigation canals, small rivers, and existing water infrastructure.

The International Hydropower Association reports that the introduction of standardized and containerized turbine-generator systems has significantly reduced installation time by nearly 50%, lowering overall project costs and complexity. These innovations are particularly beneficial for pico- and micro-hydropower projects in rural communities where large infrastructure investments are not feasible. With simpler installation processes and improved operational efficiency, local communities are now able to implement their own energy solutions. This progress also supports local economic development by creating jobs and reducing reliance on costly diesel-based power generation.

Market Restraints

Lengthy Regulatory Approvals and Environmental Permitting Processes Delaying Small Hydropower Project Development and Investor Participation

Regulatory approvals and permitting requirements remain a major challenge for the development of small hydropower projects in many regions. Environmental impact assessments, water usage permissions, and stakeholder consultations often extend the project approval process significantly. In many cases, these procedures can delay project timelines by two to three years, creating uncertainty for investors and developers. In the United States, for example, licensing approvals from the Federal Energy Regulatory Commission (FERC) for small and low-impact hydropower facilities can take between 18 and 24 months.

Such long approval cycles can discourage investment, particularly when interest rates and project financing costs are rising. Similar regulatory challenges are observed across Europe, where strict environmental protection policies under the European Union Water Framework Directive require developers to prioritize ecological water flows and river conservation. While these measures are important for environmental protection, they can restrict approvals for new run-of-river hydropower installations. As a result, developers often face increased project risk, longer planning phases, and higher administrative costs.

High Initial Capital Investment and Infrastructure Costs Limiting Small Hydropower Adoption Compared to Rapidly Declining Solar Energy Prices

High initial capital requirements represent another key challenge for the small hydropower market. Although advancements in modular equipment have improved cost efficiency, civil construction activities still account for approximately 60-70% of total project expenditure. Infrastructure components such as intake weirs, diversion channels, penstocks, and powerhouses require significant engineering work and specialized construction.

Projects in remote, mountainous regions often face additional logistical challenges, which increase transportation and labor costs. Financing can also be difficult, particularly for independent power producers in emerging markets that lack strong credit support or stable regulatory frameworks. According to the World Bank, the levelized cost of electricity (LCOE) for small hydropower remains around 30% higher than solar photovoltaic power in regions with strong sunlight availability. This cost gap makes it harder for developers to compete with rapidly expanding solar energy projects, especially in markets where financial incentives for hydropower are limited.

Market Opportunities

Growing Opportunities for Small Hydropower Integration with Hybrid Renewable Microgrids to Improve Grid Stability and Energy Access

The integration of small hydropower with solar and wind technologies in hybrid renewable microgrids presents a major growth opportunity for the industry. Unlike intermittent renewable sources, hydropower can provide stable and dispatchable electricity, making it an ideal complementary energy source. When combined with solar or wind power, small hydro systems can significantly improve overall grid reliability and energy availability. According to the International Renewable Energy Agency, hybrid renewable microgrids could potentially provide electricity access to more than 500 million additional people worldwide by 2030.

In these systems, small hydropower can also support pumped-storage operations, helping store surplus renewable energy and release it during peak demand periods. Several technology providers, including Voith Group, are developing advanced digital control systems that allow seamless switching between renewable energy sources within microgrids. This capability is particularly valuable in emerging markets across Africa and Southeast Asia, where diesel-based electricity generation costs often exceed US$0.30 per kilowatt-hour.

Retrofitting Existing Irrigation Canals and Water Infrastructure Creating Cost-Effective Expansion Opportunities for Small Hydropower Generation

Retrofitting existing irrigation canals and water conveyance systems with hydropower technology represents another promising opportunity for the small hydropower market. Across the world, more than 2 million kilometers of irrigation channels already provide water that can be used for electricity generation. These installations, often referred to as “non-powered dams,” offer natural water head and flow without requiring the construction of new reservoirs or large dams.

The U.S. Department of Energy estimates that the United States alone has nearly 12 gigawatts of untapped hydropower potential in existing water infrastructure. Similar opportunities are emerging in countries such as India, where the Ministry of Jal Shakti is promoting the integration of small hydro turbines into canal systems. With operational efficiencies exceeding 80% and average payback periods of less than seven years, these retrofit projects offer stable returns. Engineering, procurement, and construction companies can benefit significantly by upgrading irrigation networks using advanced Francis and Kaplan turbine technologies.

Category-wise Insights

Capacity Analysis

Small Hydropower (1 MW - 10 MW) leads the Capacity category with an estimated 54% share of the market. This dominance is mainly due to its optimal project size, which allows easier integration into utility grids while maintaining cost efficiency in electromechanical equipment. According to the U.S. Department of Energy, mini-to-small hydropower plants ranging from 101 kW to 10 MW accounted for about 63.9% of revenue in recent years, highlighting strong industry preference for this capacity range. These systems provide a balanced combination of reliable power generation and manageable infrastructure requirements, making them attractive for both public utilities and private developers.

Standardized turbine technologies developed by companies such as ANDRITZ and GE Renewable Energy have also contributed to the segment’s growth by reducing equipment costs by nearly 20% compared to smaller micro-hydropower units. As a result, small hydropower projects are widely adopted by industrial power consumers while also qualifying for renewable energy incentives and sustainability programs in multiple countries.

Component Analysis

Electromechanical Equipment accounts for approximately 45% of the Component category, making it the most valuable part of small hydropower installations. Core equipment, such as turbines, generators, and governors, represents the technological backbone of these projects and largely determines their efficiency and performance. Modern developments, including permanent magnet generators, have significantly improved energy conversion efficiency, especially in low-head and variable-flow conditions.

Companies like Hydrosyst have recently introduced advanced turbine-generator solutions designed to perform efficiently under fluctuating water levels. While civil construction often represents a large portion of the overall project cost, electromechanical components remain the key differentiator in project competitiveness. The integration of digital technologies, including IoT-based monitoring systems and predictive maintenance platforms, is further enhancing equipment performance. These innovations help operators detect potential issues early, reduce maintenance downtime, and extend the operational life of hydropower assets by up to 25%, ultimately improving long-term project profitability.

Plant Type Analysis

Run-of-River (RoR) hydropower plants hold the leading position in the Plant Type category, accounting for around 60% of the market share. Their popularity largely stems from their environmentally friendly design, as these systems generate electricity using natural river flow without requiring large reservoirs or extensive water storage infrastructure. This approach minimizes ecological disruption and simplifies the environmental approval process under regulatory frameworks such as those implemented by the Federal Energy Regulatory Commission and European energy authorities.

Data from the International Hydropower Association highlights the widespread adoption of run-of-river systems in Asia, where many rivers offer suitable gradients and consistent water flow for reliable electricity generation. These plants typically achieve plant factors of 50-60%, allowing them to maintain steady output with relatively lower operational complexity. In addition, their shorter construction timelines and lower infrastructure requirements enable faster project deployment and quicker return on investment, further strengthening their leadership within the small hydropower sector.

Application Analysis

Rural Electrification represents the largest Application segment in the small hydropower market, contributing approximately 40% of the overall share. Small and micro hydropower plants play a crucial role in delivering reliable electricity to remote and off-grid communities where large power infrastructure is difficult to build. These systems are particularly effective in mountainous or river-rich regions where natural water flow can be easily harnessed for local power generation. Such initiatives strongly support global sustainability targets, including the energy access goals established under United Nations Sustainable Development Goal 7.

India has announced plans to significantly expand its small hydropower capacity to nearly 10 GW, focusing on canal-based and decentralized hydro projects. These projects provide electricity to thousands of villages while supporting local economic development. With relatively low operating and maintenance costs and a levelized cost of electricity below US$0.05 per kWh, small hydropower remains a preferred energy solution for rural electrification programs funded by governments and international development organizations.

Regional Insights

North America Small Hydropower Trends

The United States leads the North American small hydropower market due to supportive regulatory policies and increasing investments in renewable infrastructure. The Federal Energy Regulatory Commission has introduced streamlined licensing processes for low-impact hydropower projects under 10 MW, which has significantly accelerated project approvals and encouraged private sector participation. Additionally, the U.S. Department of Energy has provided strong financial backing for innovation in small hydropower technologies.

The agency allocated US$16.6 million in funding for a 3 MW project in Kentucky, highlighting government commitment to expanding distributed renewable power systems. Technology innovation is also supported through initiatives such as Manufacturing USA, which focuses on the development of modular and flexible turbine technologies suitable for retrofitting existing dams. In the Pacific Northwest region, companies like Canyon Hydro are modernizing older hydropower facilities by installing advanced cross-flow turbines that achieve nearly 90% operational uptime even under fluctuating water flow conditions.

Europe Small Hydropower Trends

Europe remains an important region for small hydropower development, supported by strong renewable energy policies and modernization initiatives. Germany has been particularly active in upgrading run-of-river hydropower plants through incentives provided under the Renewable Energy Sources Act (EEG), which encourages efficient renewable power generation below the 1 MW threshold. Meanwhile, the United Kingdom is integrating hydropower into broader clean-energy systems that support its long-term net-zero emissions strategy.

Other European countries, including France and Spain, are working under coordinated EU renewable energy frameworks that promote environmentally responsible hydropower development, including fish-friendly turbine technologies. The European Renewable Network also highlights how different European countries define small hydropower capacity limits differently, sometimes extending up to 10 MW. This diversity has encouraged cross-border collaboration and technology transfer across the region. Additionally, companies such as Voith are modernizing older Alpine hydropower plants with upgraded turbines that improve operational efficiency by nearly 20%.

Asia Pacific Small Hydropower Trends

The Asia Pacific region represents one of the fastest-growing markets for small hydropower, driven by strong manufacturing capabilities and expanding renewable energy demand. China plays a dominant role as a global manufacturing hub for small hydropower turbines and related equipment, exporting these technologies to multiple developing markets through infrastructure programs such as the Belt and Road Initiative. In India, both government and private sector investments are accelerating capacity expansion. For example, JSW Neo Energy acquired the 150 MW Tidong hydropower project in September 2025, increasing its private hydropower portfolio to around 1.8 GW.

Countries like Japan are also focusing on developing advanced low-head turbine technologies designed for smaller rivers and irrigation channels. Across Southeast Asia, several nations are deploying small hydropower systems along irrigation canals to support decentralized energy generation. Additionally, India’s Arunachal Pradesh state has announced investments exceeding INR 1 lakh crore to harness the hydropower potential of Himalayan rivers through multiple small and micro hydropower projects.

Competitive Landscape

The small hydropower market is moderately consolidated among major turbine manufacturers but remains fragmented in engineering, procurement, and construction (EPC) services. Leading companies such as Voith, ANDRITZ, and GE Renewable Energy collectively account for more than 50% of the global market share due to their advanced turbine designs, proprietary hydrodynamic technologies, and digital monitoring solutions. These companies are increasingly focusing on modular hydropower systems that simplify installation and reduce project costs for small-scale plants.

Another major strategy involves combining small hydropower with pumped storage or hybrid renewable systems to improve grid flexibility and energy storage capabilities. Many equipment manufacturers are also investing in environmentally friendly innovations, such as integrated fish-pass technologies, which help projects meet strict environmental regulations. At the same time, market players are expanding into retrofit and modernization projects for aging dams and water infrastructure. Emerging service models, including AI-enabled operations and maintenance platforms, are helping operators achieve plant availability levels approaching 99%.

Key Market Developments

- In September, 2025: JSW Neo Energy signed an agreement to acquire the 150 MW Tidong run-of-river hydropower project in Himachal Pradesh from Statkraft for around INR 1,728 crore. The transaction expanded JSW’s hydro portfolio to nearly 1.8 GW and strengthened its renewable expansion strategy within India’s growing small hydropower sector.

- In October, 2025: Water Weco introduced compact mini-hydro generation systems designed for low-flow and distributed energy sites. The solution enables rapid installation and flexible grid integration, allowing utilities and rural developers to harness small water resources for decentralized renewable electricity production

Companies Covered in Small Hydropower Market

- Voith

- ANDRITZ

- GE Renewable Energy

- Siemens

- Toshiba

- BHEL

- SNC-Lavalin

- HNAC Technology

- Gilbert Gilkes & Gordon Ltd

- Mavel

- HM Hydro

- Ganz EEM

- Kolektor Turboinstitut

- Canyon Hydro

- CKD Blansko

Frequently Asked Questions

The market is forecasted to reach US$ 3.7 Billion by 2033, driven by renewable decentralization.

Government subsidies for rural electrification and low-head turbine innovations enable deployment in untapped sites.

1-10 MW leads with 54% share, balancing scale, efficiency, and regulatory feasibility.

Asia Pacific dominates via policy support in China and India's Himalayan resources.

Retrofitting irrigation canals worldwide for conduit hydro with quick paybacks under 7 years.

Key firms include Voith, ANDRITZ, GE Renewable Energy, Siemens, and BHEL.