- Advanced Materials

- Glass Ceramics Market

Glass Ceramics Market Size, Share, and Growth Forecast 2026 - 2033

Glass Ceramics Market by Material Type (Lithium Aluminosilicate [LAS], Zinc Aluminosilicate [ZAS], Magnesium Aluminosilicate [MAS], Others), Application (Household Appliances, Building & Construction, Electrical & Electronics, Healthcare & Medical, Industrial Equipment, Aerospace & Défense, Others), and Regional Analysis for 2026 - 2033

Glass Ceramics Market Size and Trend Analysis

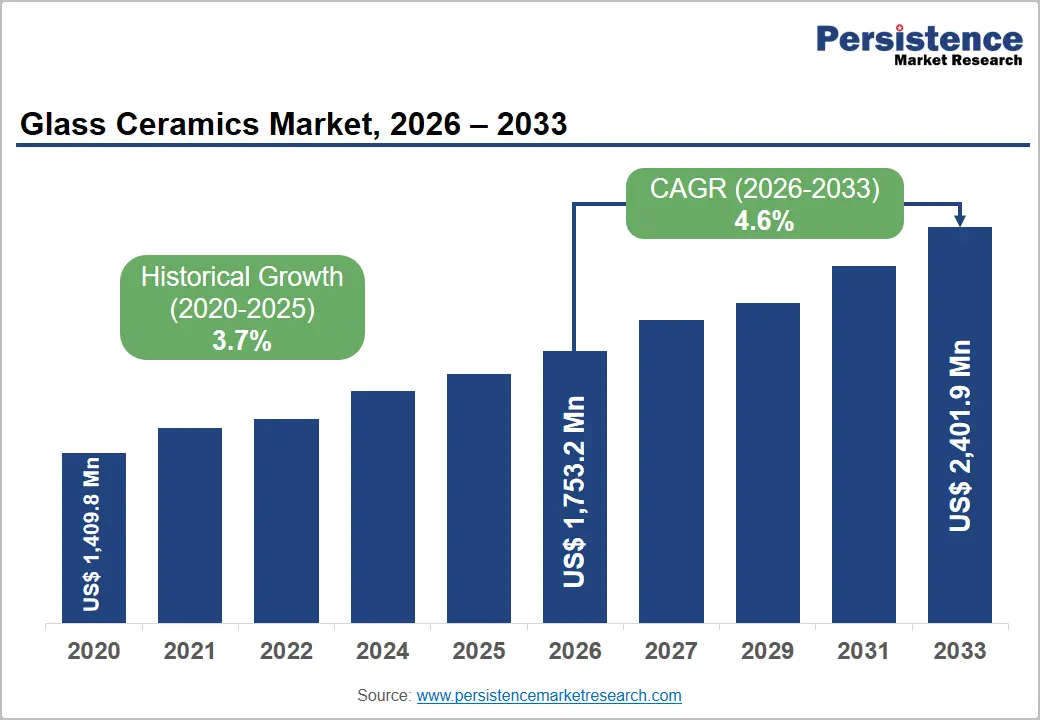

The global glass ceramics market size is valued at approximately US$ 1,753.2 Mn in 2026 and is projected to reach US$ 2,401.9 Mn by 2033, growing at a CAGR of 4.6% between 2026 and 2033. This steady expansion is driven by the material's unique combination of near-zero thermal expansion, mechanical strength, and chemical resistance properties that are irreplaceable across industrial, aerospace, and consumer applications.

Rising global investment in advanced manufacturing, the proliferation of energy-efficient induction cooktop technology in residential and commercial kitchens, growing demand for radiolucent and biocompatible materials in medical devices, and accelerating aerospace platform modernization are collectively reinforcing glass ceramics demand across all key end-use verticals.

Key Industry Highlights:

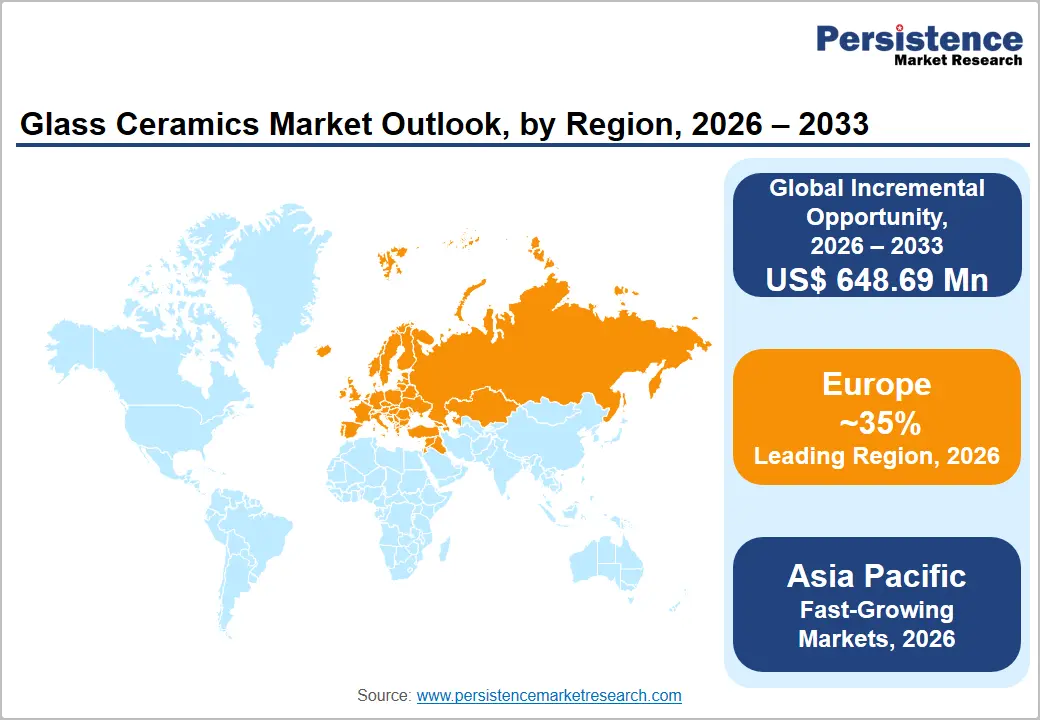

- Leading Region: Europe leads the global glass ceramics market with approximately 34% revenue share in 2026, anchored by SCHOTT AG and Eurokera's dominant cooktop panel production and the continent's world-leading induction cooking appliance adoption rates.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a CAGR exceeding 5.8% through 2033, propelled by China's vast appliance manufacturing base, India's rising induction cooking adoption, and Japan's advanced technical glass ceramics for semiconductors and precision optics.

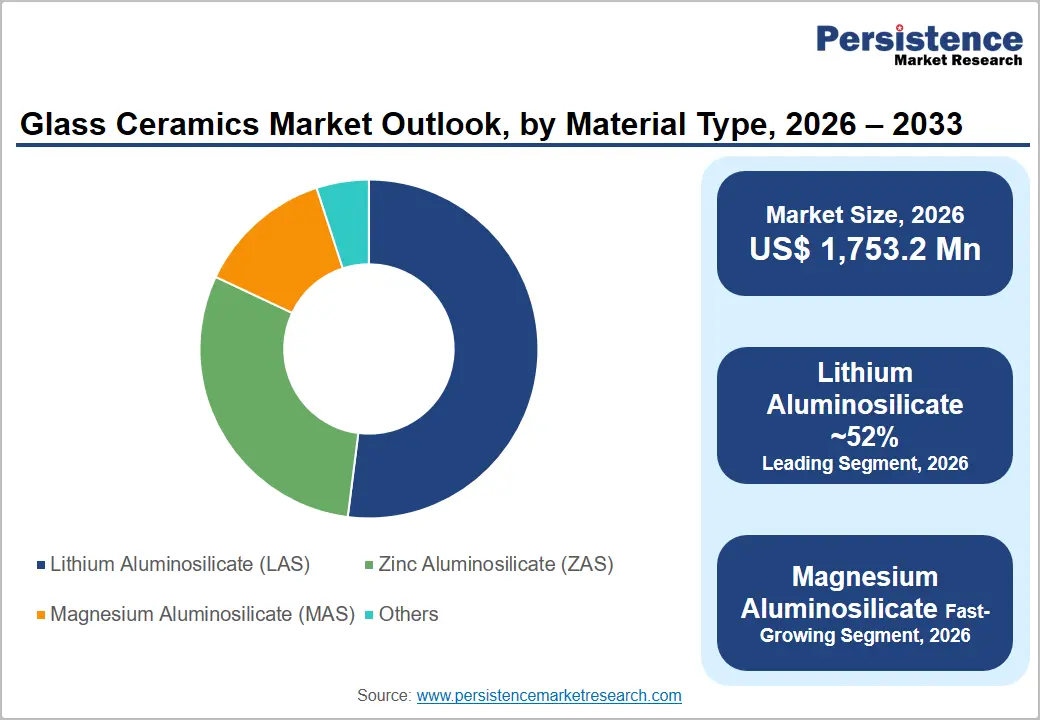

- Dominant Segment: Lithium Aluminosilicate (LAS) glass ceramics dominate the material type category with approximately 52% market share in 2026, driven by their irreplaceable role in induction and radiant cooktop panels, the highest-volume single application in the glass ceramics market.

- Fastest Growing Segment: Healthcare & medical is the fast-growing application segment, driven by rising global dental procedure volumes, CAD/CAM chairside dentistry adoption, and the WHO's estimate of 3.5 billion people affected by oral disease generating structural restorative care demand.

- Key Opportunity: The most actionable near-term opportunity is investing in glass ceramic formulations for 5G electronics and semiconductor applications: the ITU's projection of 4.4 billion 5G connections by 2027 is generating premium-priced demand for low-loss glass ceramic substrates and random components from leading telecom equipment OEMs.

DRO Analysis

Drivers - Rising Adoption of Glass Ceramic Cooktop Panels in Energy-Efficient Household Appliances

The global consumer appliances industry is generating sustained, high-volume demand for glass ceramics particularly Lithium Aluminosilicate (LAS) compositions as induction and radiant cooktop penetration accelerates across Europe, China, and North America. The International Energy Agency (IEA) reports that induction cooktops deliver 85-90% energy efficiency compared to 40-55% for traditional gas hobs, a performance gap that is translating directly into regulatory mandates and consumer preference shifts.

The European Commission's Ecodesign Directive and China's National Energy Conservation Standards (GB Standards) are actively incentivizing the replacement of gas cooking appliances with electric induction alternatives, each of which requires a precision-finished LAS glass ceramic panel engineered for thermal shock resistance exceeding 700°C differential.

Expanding Applications in Aerospace, Défense, and High-Performance Industrial Equipment

Glass ceramics' unique material profile, combining zero or near-zero thermal expansion coefficients, optical transparency in specific wavelength ranges, and superior dimensional stability under extreme temperature cycling, is driving accelerating specification adoption across aerospace randoms, infrared window systems, precision optical equipment, and industrial furnace observation ports.

The U.S. Department of Défense (DoD) and allied Défense establishments have increased procurement of glass ceramic-based random and infrared dome assemblies as next-generation missile, drone, and aircraft programs advance applications where no polymer or conventional glass material can match glass ceramic's combined performance envelope. According to the American Ceramic Society (ACerS), advanced glass ceramic materials are experiencing renewed R&D investment from Défense prime contractors and aerospace OEMs seeking materials capable of withstanding hypersonic flight thermal loads exceeding 1,000°C.

Restraints - High Manufacturing Complexity and Production Cost Relative to Alternative Materials

Glass ceramics' manufacturing process, which requires precise nucleation agent formulation, controlled crystallization heat treatment cycles, and stringent quality inspection protocols, imposes significantly higher production costs than conventional glass or technical ceramic alternatives, constraining market penetration in cost-sensitive application segments. The multistep thermal processing required to achieve the correct crystalline microstructure demands energy-intensive kiln operations and tight process control, with yield losses from microstructural defects adding further cost pressure.

This effectively limits glass ceramics to applications where performance requirements justify the premium, excluding broad mid-market consumer and construction segments where lower-cost alternatives such as tempered glass, alumina ceramics, or engineered polymers adequately serve functional requirements without the associated cost penalty.

Competition from Advanced Technical Ceramics and Engineered Glass Alternatives

The glass ceramics market faces intensifying substitution pressure from a range of advanced technical ceramics, including alumina, zirconia, and silicon nitride, and from high-performance engineered glass formulations that can replicate specific glass ceramic properties at lower material costs in select applications.

In the healthcare segment, zirconia-based dental ceramics are competing directly with glass ceramic dental restorations in certain aesthetic and structural applications, with some clinical studies published in the Journal of Dentistry reporting comparable longevity outcomes for well-sintered zirconia frameworks.

Market Opportunities

Rapid Growth in Glass Ceramic Applications for Healthcare and Dental Restorations

The healthcare and medical application segment represents one of the most strategically compelling growth opportunities for glass ceramic producers, as rising global dental procedure volumes, aging population demographics, and accelerating adoption of CAD/CAM (Computer-Aided Design/Computer-Aided Manufacturing) dental milling technology are collectively driving demand for lithium disilicate and leucite-reinforced glass ceramic dental blocks.

The World Health Organization (WHO) estimates that oral disease affects nearly 3.5 billion people globally, with demand for restorative dental procedures growing fastest in the Asia Pacific, Latin America, and the Middle East as middle-class populations gain access to dental care. Lithium disilicate glass ceramics used in dental crowns, veneers, and bridges offer a clinically proven combination of translucency, flexural strength (360-400 MPa), and ease of machinability that makes them the preferred material for CAD/CAM chairside and laboratory milling systems.

Emerging Opportunities in Electrical & Electronics: 5G Infrastructure and Semiconductor Applications

The global rollout of 5G telecommunications infrastructure and accelerating semiconductor manufacturing investment are creating a new, high-value demand corridor for specialized glass ceramic substrates, microwave-transparent enclosures, and precision MEMS (Micro-Electro-Mechanical Systems) carrier materials applications, where glass ceramics' combination of low dielectric loss, dimensional stability, and hermetic sealing capability is technically superior to competing materials.

The International Telecommunication Union (ITU) projects that global 5G connections will surpass 4.4 billion by 2027, driving the construction of hundreds of thousands of new base stations that require glass ceramic components in antenna random and filter assemblies.

Category-wise Analysis

Material Type Insights

Lithium Aluminosilicate (LAS) glass ceramics command the dominant position in the material type category, accounting for approximately 52% of the total global glass ceramics market revenue in 2026. LAS glass ceramics' market leadership is rooted in their exceptional combination of near-zero to slightly negative thermal expansion coefficients (typically -0.5 to +0.5 × 10??/°C), outstanding thermal shock resistance, and optical translucency, a property profile that makes them essentially irreplaceable in the cooktop panel application, the market's single highest-volume end use.

Major producers, including SCHOTT AG (with its CERAN brand) and Eurokera, have invested decades in LAS composition refinement and large-format melting and crystallization technology, establishing manufacturing scale advantages and brand recognition with appliance OEMs that function as durable structural barriers to entry for new competitors.

Application Insights

Household appliances is the leading application segment in the glass ceramics market, accounting for approximately 46% of total revenue in 2026, a position anchored almost entirely by the induction and radiant cooktop segment, where glass ceramic panels manufactured from LAS compositions represent the only commercially viable surface material meeting the combined requirements of thermal shock resistance, mechanical load-bearing, and smooth cleanability.

This application segment's leadership is reinforced by the global installed base of over 200 million glass ceramic cooktop surfaces in active use, according to appliance industry association estimates, and by the ongoing replacement cycle as aging units are upgraded.

Regional Analysis

North America Glass Ceramics Market Trends & Analysis

North America accounts for approximately 22% of the global glass ceramics market revenue in 2026, driven by a mature household appliances sector, strong demand from aerospace and Défense prime contractors, and a growing dental restoration market supported by widespread adoption of CAD/CAM chairside dentistry systems.

The U.S. market benefits from a strong Défense and aerospace procurement base, with glass ceramic radomes and infrared windows widely utilized in multiple active development programs. Additionally, the commercial kitchen sector is increasingly adopting induction cooking technologies to improve energy efficiency and operational safety. The residential appliance market is also gradually shifting toward induction cooking, supported by natural gas appliance restrictions implemented in California and several other states.

U.S. Glass Ceramics Market Size

The United States accounts for approximately 78% of North America's glass ceramics market in 2025, underpinned by the country's globally significant Défense and aerospace procurement base, a highly developed dental technology market, and an appliance sector undergoing structural transition toward induction cooking. Federal investment in next-generation aircraft, hypersonic weapons programs, and satellite systems is sustaining demand for high-specification glass ceramic components certified to MIL-SPEC standards.

Europe Glass Ceramics Market Trends, Drivers, & Insights

Europe is the world's largest and most mature glass ceramics market, representing approximately 34% of global market revenue in 2025, anchored by the continent's dominant position in glass ceramic cooktop panel production with SCHOTT AG (Germany) and Eurokera (France, a joint venture of Saint-Gobain and Corning) collectively supplying a substantial share of global LAS glass ceramic panels.

The region's demand is structurally supported by strong induction cooktop penetration in France, Germany, and the Netherlands, which rank among the world's highest induction cooking adoption markets, and by a sophisticated dental and medical device sector that extensively specifies glass ceramic restorations and implant components. The European Commission's Ecodesign and Energy Labelling regulations are accelerating the replacement of conventional gas and resistive electric cooktops with induction alternatives, directly driving glass ceramic panel demand.

Germany Glass Ceramics Market Size

Germany accounts for approximately 25% of Europe's glass ceramics market in 2025, reflecting the country's status as both the global production headquarters of SCHOTT AG the world's leading glass ceramics manufacturer, and as a major consumer market for glass ceramic cooktop panels, precision optics, and dental materials. Germany's advanced manufacturing industrial base sustains demand for glass ceramic components in metrology, laser technology, and industrial furnace equipment.

U.K. Glass Ceramics Market Size

The U.K. represents approximately 13% of Europe's glass ceramics market in 2026, with demand driven by a substantial household appliances replacement market, a well-developed dental technology sector, and growing procurement of glass ceramic components for Défense and aerospace applications through the country's advanced manufacturing supply chain. UK Research and Innovation (UKRI) has funded multiple glass ceramic R&D programs targeting photonic and quantum technology applications.

France Glass Ceramics Market Size

France accounts for approximately 16% of Europe's glass ceramics market in 2026, supported by the country's role as co-host to Eurokera, the world's second-largest glass ceramic cooktop panel producer, and by France's high induction cooking penetration rate, estimated at over 60% of new kitchen appliance installations. The French government's energy efficiency incentives under the MaPrimeRenov scheme and broader EU Ecodesign compliance requirements are sustaining residential appliance upgrade demand.

Asia Pacific Glass Ceramics Market Drivers & Analysis

Asia Pacific is the fast-growing regional market for glass ceramics, accounting for approximately 31% of global revenue in 2026 and projected to expand at a CAGR exceeding 5.8% through 2033. China dominates regional volume, operating significant glass ceramic production capacity for both domestic consumption and export, with state-supported investment in appliance manufacturing, advanced materials, and semiconductor production sustaining robust procurement.

Japan is the regional leader in advanced glass ceramic technology applications, particularly in precision optics, MEMS substrates, and dental CAD/CAM materials, while India is the fastest-growing national market, propelled by rapidly expanding household appliance penetration and a growing domestic dental technology sector.

China Glass Ceramics Market Size

China accounts for approximately 48% of the Asia Pacific's glass ceramics market in 2026, supported by the world's largest household appliance manufacturing base. China's domestic cooktop production encompasses millions of induction units annually and by government investment in advanced ceramics under the Made in China 2025 and 14th Five-Year Plan industrial strategies.

India Glass Ceramics Market Size

India represents approximately 14% of the Asia Pacific's glass ceramics market in 2026, with demand driven by rapidly rising induction cooktop adoption, supported by the Pradhan Mantri Ujjwala Yojana clean cooking initiative and urban middle-class lifestyle preferences, and by a growing private dental clinic sector investing in CAD/CAM glass ceramic restoration technology. India's market is among the region's fastest growing, with domestic appliance manufacturers sourcing glass ceramic panels increasingly from both import and nascent domestic supply.

Japan Glass Ceramics Market Size

Japan accounts for approximately 18% of the Asia Pacific's glass ceramics market in 2026, reflecting the country's globally advanced position in precision optical glass ceramics, semiconductor equipment components, and dental materials sectors, where Japanese manufacturers, including Nippon Electric Glass and AGC Inc., maintain world-class material science and process engineering capabilities.

Competitive Landscape

The global glass ceramics market is moderately consolidated at the premium technical product tier, where a small number of highly capital-intensive producers led by SCHOTT AG, Corning Incorporated, Nippon Electric Glass, and AGC Inc. command dominant shares through proprietary composition intellectual property, large-scale precision melting infrastructure, and decades of application engineering relationships with leading OEMs.

Key Developments:

- In March 2025, SCHOTT announced serial production of the CERAN matte line for glass-ceramic cooktops, signalling commercial scale-up of matte “design trend” surfaces with functional benefits such as reduced visible scratches/fingerprints.

- In March 2025, Corning launched Corning Gorilla Glass Ceramic as a transparent, strengthen able glass-ceramic cover material for mobile devices, signalling new growth headroom for glass-ceramics beyond cooktops into consumer electronics durability applications.

Companies Covered in Glass Ceramics Market

- SCHOTT AG

- Corning Incorporated

- Nippon Electric Glass Co., Ltd.

- AGC Inc. (Asahi Glass Co.)

- Eurokera S.N.C. (Saint-Gobain / Corning Joint Venture)

- Ivoclar AG

- Vita Zahnfabrik

- Dentsply Sirona

- Kyocera Corporation

- Noritake Co., Limited

- Murata Manufacturing Co., Ltd.

- Advanced Ceramics Manufacturing

- Ceramic Data Solution GmbH

- Beijing Kaitai Bearing Co., Ltd.

- Zhengzhou Litong Refractory Co., Ltd.

Frequently Asked Questions

The global glass ceramics market is valued at approximately US$ 1,753.2 Mn in 2026 and is projected to reach US$ 2,401.9 Mn by 2033, expanding at a CAGR of 4.6% during the forecast period.

The primary demand driver is accelerating global adoption of induction and radiant cooktop technology, driven by energy efficiency mandates from the IEA, the European Commission's Ecodesign Directive, and China's GB Standards, which creates high-volume, structurally durable demand for LAS glass ceramic cooktop panels.

Lithium Aluminosilicate (LAS) glass ceramics are the leading material type segment, commanding approximately 52% of global market revenue in 2025. LAS glass ceramics' dominance is rooted in their near-zero thermal expansion coefficients and exceptional thermal shock resistance properties that make them the only commercially viable surface material for induction and radiant cooktop panels.

Europe is the global leader in the Glass Ceramics market with approximately 34% of total market revenue in 2025. The region's leadership reflects its hosting of the world's two largest glass ceramic producers, SCHOTT AG (Germany) and Eurokera (France), combined with the highest global induction cooking penetration rates, a sophisticated dental materials industry, and substantial aerospace and optical glass ceramics demand from European Défense and research institutions.

Leading companies in the global Glass Ceramics market include SCHOTT AG, Corning Incorporated, Nippon Electric Glass Co., Ltd., AGC Inc., Eurokera S.N.C., Ivoclar AG, Vita Zahnfabrik, Dentsply Sirona, Kyocera Corporation, Noritake Co., Limited, and Murata Manufacturing Co., Ltd., among others.