- Hardware & Software IT Services

- SaaS-based Core Banking Software Market

SaaS-based Core Banking Software Market Size, Share, and Growth Forecast 2026 - 2033

SaaS-based Core Banking Software Market by Deployment (Public, Private, Hybrid Cloud), Banking Type (Large Banks, Midsize Banks, Small Banks, Community Banks, Credit Unions), End-user, and Regional Analysis, 2026 - 2033

SaaS-based Core Banking Software Market Size and Trends Analysis

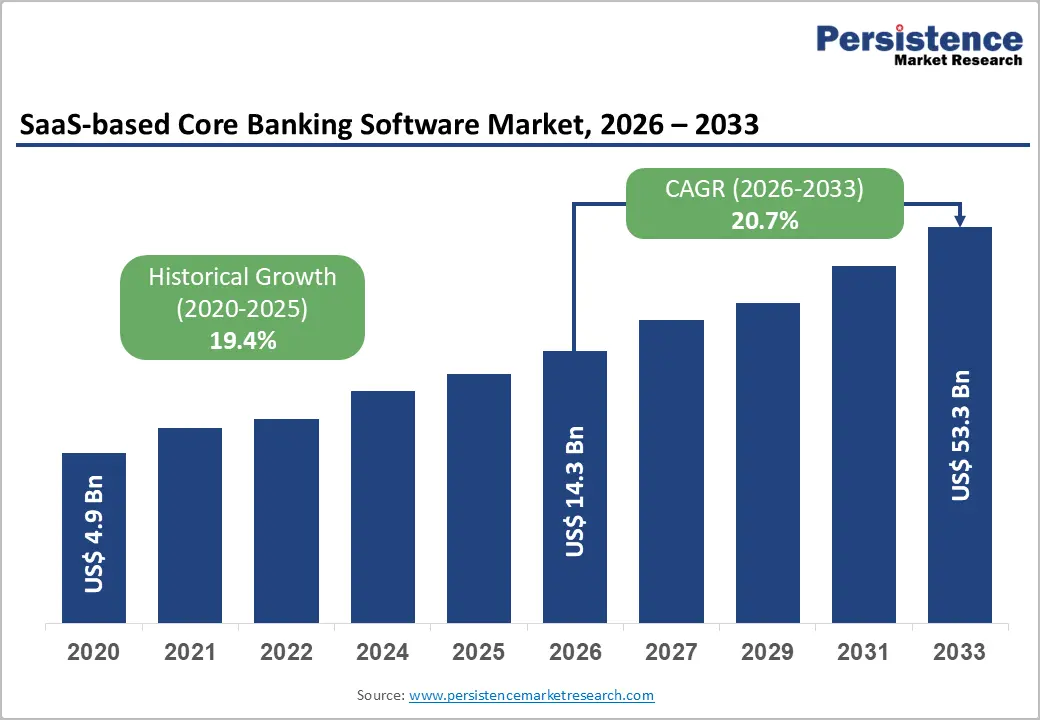

The global SaaS-based core banking software market size is likely to be valued at US$14.3 billion in 2026 and is expected to reach US$53.3 billion by 2033, growing at a CAGR of 20.7% during the forecast period from 2026 to 2033, driven by rising replacement of legacy banking systems with cloud-native and Application Programming Interface (API)-enabled platforms that support real-time processing and fast product launches. Increasing adoption of digital banking, embedded finance, and open banking frameworks is further spurring demand.

Key Industry Highlights:

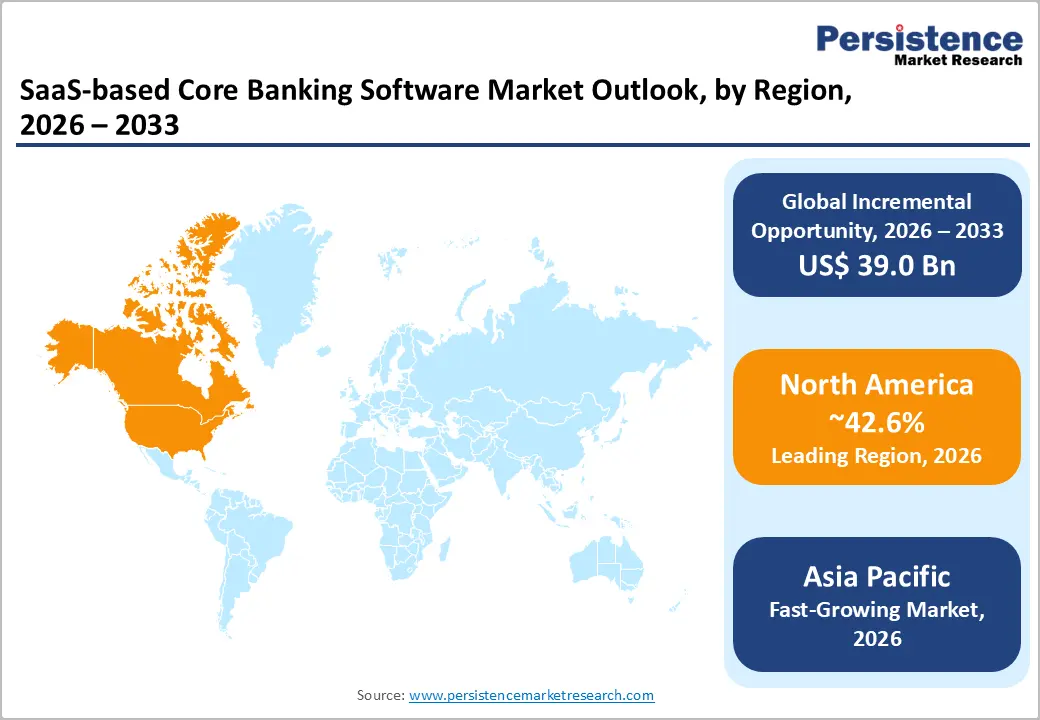

- Leading Region: North America, with about a 42.6% share in 2026, owing to large-scale core banking modernization and strong presence of leading vendors.

- Fast-growing Region: Asia Pacific, backed by expanding digital payments networks and government-backed financial digitization initiatives.

- New Launch: In October 2025, Mambu launched its composable banking framework for North America’s credit unions. The initiative was introduced to help credit unions replace legacy core banking systems with cloud-native SaaS architecture, enabling quick deployment of digital products and flexible integration with third-party fintech services.

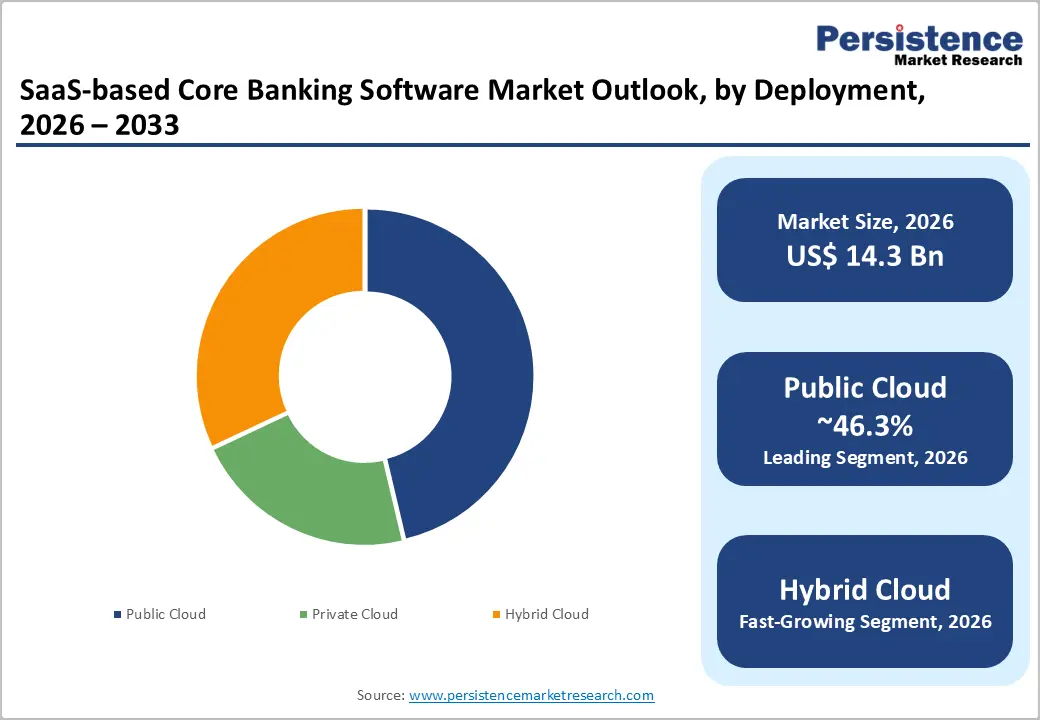

- Leading Deployment: Public cloud, approximately 46.3% share in 2026, as it enables fast deployment, expandability, and low upfront infrastructure costs.

- Dominant End User: Retail banking, nearly 34.5% in 2026, due to high transaction volumes and surging digital customer expectations.

DRO Analysis

Driver- Low Total Cost of Ownership

Banks running on-premise core systems carry hidden costs that go well beyond server hardware, including floor space, power consumption, periodic hardware refreshes, and in-house IT teams to manage it all. On-premises Total Cost of Ownership (TCO) is significantly higher than cloud-based alternatives, once the fully loaded costs of hardware, storage, cooling, and periodic asset replacement are factored in.

Software as a Service (SaaS)-based core banking converts these unpredictable capital outlays into a fixed subscription fee. SaaS replaces high upfront costs with manageable and recurring payments, preserving cash flow for core growth activities. This shift also unlocks a tax advantage. Operating expenses are deductible in the year incurred, unlike capitalized assets that depreciate over years. For resource-constrained community banks and mid-tier lenders, this financial flexibility is a prominent growth enabler.

Speedy Adaptation to Regulatory Changes

Financial institutions face a relentless pace of regulatory change. In the first half of 2025 alone, global sanctions-related fines reached US$228.8 million, a sharp increase from US$3.7 million in the same period of 2024, thereby signaling intensifying regulatory scrutiny, as per Fenergo's KYC and AML Compliance Blog. With legacy systems, every new rule requires bespoke internal development. SaaS providers, by contrast, push compliance updates across their entire client base simultaneously.

Ideally, Anti-Money Laundering (AML) software is updated in real time as regulations change, perpetually protecting the institution. For instance, regulators in 2025 are actively encouraging AI-native transaction monitoring and automated KYC for real-time detection. These capabilities can be deployed platform-wide by SaaS vendors without each bank needing to commission custom builds.

Restraint - Dependency on a Single Vendor

Once a bank embeds its operations into a SaaS core banking platform, switching becomes a key undertaking- not just technically, but financially and operationally. The ABA's 2024 Core Platforms Survey found that 35% of banks are dissatisfied with their current core vendor, yet only 19% say they are likely to switch at their next renewal date. The gap between dissatisfaction and action is a migration risk.

For mid-market banks, the attached integration estate typically runs 50 to 150 active third-party connections, many partially or entirely undocumented. A full-platform migration typically takes 3 to 5 years, and decommissioning timelines frequently extend 12 to 24 months beyond original estimates. It further hampers the TCO benefit of modernization. This dependency means a bank's product roadmap, uptime reliability, and compliance readiness all hinge on a vendor's own priorities and execution pace.

Opportunity - Modular and Plug-and-Play Banking Architectures

Traditional core banking systems bundle every function, including deposits, loans, payments, and the ledger, into a single tightly coupled stack. Any change in one area risks breaking another. Composable architectures solve this by isolating functions as independent microservices. Institutions can now reduce their time-to-market by 80% using this modular approach, according to Backbase's guide to composable banking.

TCS BaNCS, for example, allows banks to add or replace specific loan or payment products without making any other changes to their existing systems landscape by selecting and connecting individual microservices. Low-code platforms enable financial institutions to develop applications 10 times faster than traditional methods, allowing business teams to configure new product capabilities. This dramatically lowers the cost and risk of deploying targeted upgrades.

API-Based Integration of Non-Banking Services

SaaS core banking platforms are increasingly built to function as open infrastructure, not closed systems. Banking-as-a-Service (BaaS) enables third-party businesses to build their own financial products without needing to become banks by accessing core banking functions through APIs. This opens a new opportunity for traditional banks to monetize their infrastructure. BaaS-enabled services have increased financial access for underserved U.K. consumers by approximately 22% since 2022, according to the FCA's Financial Services Market Review 2025.

Non-financial platforms are also entering the space. Approximately 64% of businesses plan to launch embedded finance solutions in 2025, with a few firms reporting 2 to 5x higher customer lifetime value for companies that implement these integrations. SaaS cores with pre-built API connectors, covering crypto wallets, real-time payments, and Buy Now, Pay Later (BNPL), let banks tap into these aspects without building from scratch.

Category-wise Analysis

Deployment Insights

Public cloud is predicted to lead with a share of approximately 46.3% in 2026, as it allows banks to launch and expand services much faster than traditional infrastructure. Banks no longer need to maintain physical data centers. They can deploy core banking systems in weeks instead of years. This is important for digital banks and fintech-led offerings. Also, hyperscalers are heavily investing in banking-specific solutions. Amazon Web Services reported that thousands of financial institutions globally use its cloud.

The hybrid cloud segment is estimated to be the fastest-growing segment over the forecast period, as banks are not ready to move everything to the public cloud at once. Several institutions still run critical workloads on legacy systems. They prefer a gradual transition. Hybrid setups allow them to modernize step by step without disrupting operations. Hybrid cloud also helps in data localization. India and Germany have strict data rules. Banks can store sensitive customer data locally while using the public cloud for analytics and digital services. Reserve Bank of India has emphasized data storage and control requirements, which indirectly support hybrid adoption.

End-user Insights

Retail banking is anticipated to dominate with a share of nearly 34.5% in 2026, as it deals with a very large customer base and high transaction volumes. Everyday services such as payments, deposits, loans, and mobile banking require real-time processing. SaaS-based core systems are better suited for handling such expansion and speed. Digital payments growth is a key driver. For example, National Payments Corporation of India reported that UPI processed over 100 billion transactions annually by 2025. Such volumes require extensible and cloud-ready core systems, which push retail banks to upgrade their infrastructure.

The wealth management segment is expected to remain in the second position in 2026, fueled by increasing demand for personalized financial services. High-net-worth individuals expect real-time portfolio insights, digital onboarding, and smooth advisory services. SaaS-based platforms make this possible through data analytics and AI integration. Another factor is the shift to digital advisory models. Robo-advisors and hybrid advisory platforms are becoming common.

Regional Insights

North America SaaS-based Core Banking Software Market Trends

North America is predicted to dominate in 2026 with a share of approximately 42.6%, as banks in the region have been investing in core modernization for much longer than most other regions. Several financial institutions are replacing decades-old legacy systems with cloud-native platforms that support real-time processing, open APIs, embedded finance, and AI-enabled banking services. Large technology providers such as FIS, Fiserv, Finxact, and Jack Henry have also created a mature network for digital transformation. In 2025, FIS was recognized as a leader in retail core banking systems in North America, highlighting the region's superior concentration of advanced banking technology vendors.

U.S. SaaS-based Core Banking Software Market Trends

A share of nearly 56.8% is expected to be held by the U.S. in 2026, as thousands of community banks, regional banks, and credit unions still operate on legacy core systems that are becoming expensive to maintain. These institutions are now migrating to cloud-native platforms to improve operational efficiency and compete with digital-first financial providers. In 2025, for example, PeoplesBank became the largest U.S. community bank to fully migrate to a modern cloud-native core platform from Nymbus. It demonstrates that even traditional banks are now embracing SaaS-based banking infrastructure.

Asia Pacific SaaS-based Core Banking Software Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 31.7%, as several countries are broadening financial inclusion, digital banking, and real-time payment networks simultaneously. Unlike mature banking markets that must replace old systems, multiple institutions in Asia Pacific can build cloud-native infrastructure from the beginning. Governments across the region are also promoting digital transformation through fintech regulations and open banking initiatives. Financial institutions are also choosing SaaS-based core banking platforms as they can launch products in months rather than years.

China SaaS-based Core Banking Software Market Trends

China will likely lead in Asia Pacific in 2026 with a share of around 39.6%, as banks are investing heavily in digital banking infrastructure, AI integration, and cloud-based financial services. The country has one of the world's largest digital payment networks, and financial institutions require expandable core banking platforms to support massive transaction volumes. Digital banking and mobile financial services have become deeply integrated into everyday consumer activity, encouraging banks to modernize their backend systems.

India SaaS-based Core Banking Software Market Trends

In 2026, India is projected to account for a share of approximately 18.9%. The country is supported by one of the world's most advanced digital public infrastructure networks. Platforms such as UPI, Aadhaar-enabled verification, and digital onboarding have encouraged banks to invest in modern cloud-based banking systems. As customer expectations shift toward instant digital services, banks are now replacing rigid legacy infrastructure with SaaS-based platforms that support fast innovation. India is also becoming a prominent cloud and data center hub. In 2025, the country became the second-largest data center market in Asia Pacific, propelled by hyperscale cloud expansion and AI adoption.

Europe SaaS-based Core Banking Software Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 14.9% in 2026, as banks are balancing modernization with strict regulatory compliance requirements. The region has been at the forefront of open banking and Revised Payment Services Directive (PSD2) regulations, which require banks to create more interoperable and API-supported systems. Hence, multiple financial institutions are modernizing their core banking infrastructure in phases rather than through complete replacements. This creates a consistent flow of SaaS implementation projects.

Germany SaaS-based Core Banking Software Market Trends

Germany will likely register a substantial share of approximately 37.7% in 2026, as banks focus on efficiency, automation, and digital customer engagement. The country has a large number of regional and cooperative banks, many of which are gradually upgrading legacy infrastructure to support digital banking services. Local financial institutions are constantly exploring cloud technologies, although adoption is generally more cautious than in the U.S. owing to regulatory and data governance considerations. The country also benefits from its superior enterprise software network and advanced industrial digitalization initiatives.

U.K. SaaS-based Core Banking Software Market Trends

A share of around 22.4% is predicted to be held by the U.K. in 2026, as it is home to a highly developed fintech sector and several globally recognized digital banks. Financial institutions in the country are under constant pressure to deliver fast digital experiences, which is encouraging investment in cloud-native core banking platforms. Open banking adoption in the U.K. is among the highest globally, creating rising demand for API-centric banking infrastructure. The market is also benefiting from the presence of leading core banking innovators such as Thought Machine and 10x Banking.

Competitive Landscape

The global SaaS-based core banking software market is moderately fragmented with the presence of established banking technology vendors, cloud-native challengers, and regional specialists. Traditional banking software leaders such as Temenos, FIS, Finastra, Oracle, Infosys, and Tata Consultancy Services utilize decades of banking expertise, regulatory compliance capabilities, and extensive customer bases. Cloud-native SaaS disruptors, including Mambu, Thought Machine, 10x Banking, and Finxact, compete primarily on agility, API-first architecture, and speedy deployment timelines.

A key competitive trend is the shift from monolithic banking systems to composable banking architectures. Banks now prefer SaaS platforms that can integrate easily with fintech ecosystems, embedded finance applications, and open banking frameworks. Vendors are hence investing heavily in microservices, low-code product configuration, and AI-based automation rather than competing solely on transaction-processing capabilities. AI integration, ecosystem partnerships, and implementation expertise have become key differentiators in recent vendor evaluations.

Key Industry Developments:

- In June 2026, Temenos announced a definitive agreement to acquire Swiss fintech additiv. The acquisition is intended to strengthen Temenos’ wealth management capabilities by combining additiv’s AI-enabled financial services orchestration platform with Temenos’ core banking and digital banking portfolio, enabling banks to launch new wealth portfolios quickly and improve advisor productivity.

- In May 2026, Temenos launched a suite of embedded AI capabilities, including AI Agents, Copilots, and Conversational Studio, across its SaaS core banking and digital banking platforms. The company stated that these tools are designed to automate banking operations, boost product development, and improve customer interactions while maintaining governance and compliance controls.

- In March 2026, Temenos received Microsoft’s Solutions Partner with Certified Software designation for its Core Banking SaaS platform running on Azure. The certification validated the platform’s interoperability, security, and cloud-native capabilities, strengthening Temenos’ strategy of extending SaaS core banking deployments on public cloud infrastructure.

Companies Covered in SaaS-based Core Banking Software Market

- Mambu

- nCino

- Skaleet

- Backbase

- Avaloq

- Ohpen

- FIS

- TCS BaNCS

- Oracle FLEXCUBE

- Temenos

- EdgeVerve

- SDK Finance

- United Bank

- Finastra

Frequently Asked Questions

The global SaaS-based core banking software market is projected to be valued at US$14.3 billion in 2026.

The SaaS-based core banking software market is expected to reach US$53.3 billion by 2033.

Key market trends include the shift toward composable banking and increasing use of AI in core systems.

Public cloud is expected to be the leading deployment with a share of nearly 46.3% in 2026, as it supports API integration, AI capabilities, and fintech partnerships.

The SaaS-based core banking software market is expected to grow at a CAGR of 20.7% from 2026 to 2033.

Mambu, nCino, Skaleet, and Backbase are a few key market players.