- Automotive Components & Materials

- Automotive Crankshaft Market

Automotive Crankshaft Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Crankshaft Market by Crankshaft Type (Forged Crankshaft, Billet Crankshaft, Others), Material (Steel Alloy, Forged Steel, Others), Vehicle Type, Manufacturing Process, and Regional Analysis for 2026 - 2033

Automotive Crankshaft Market Size and Trends Analysis

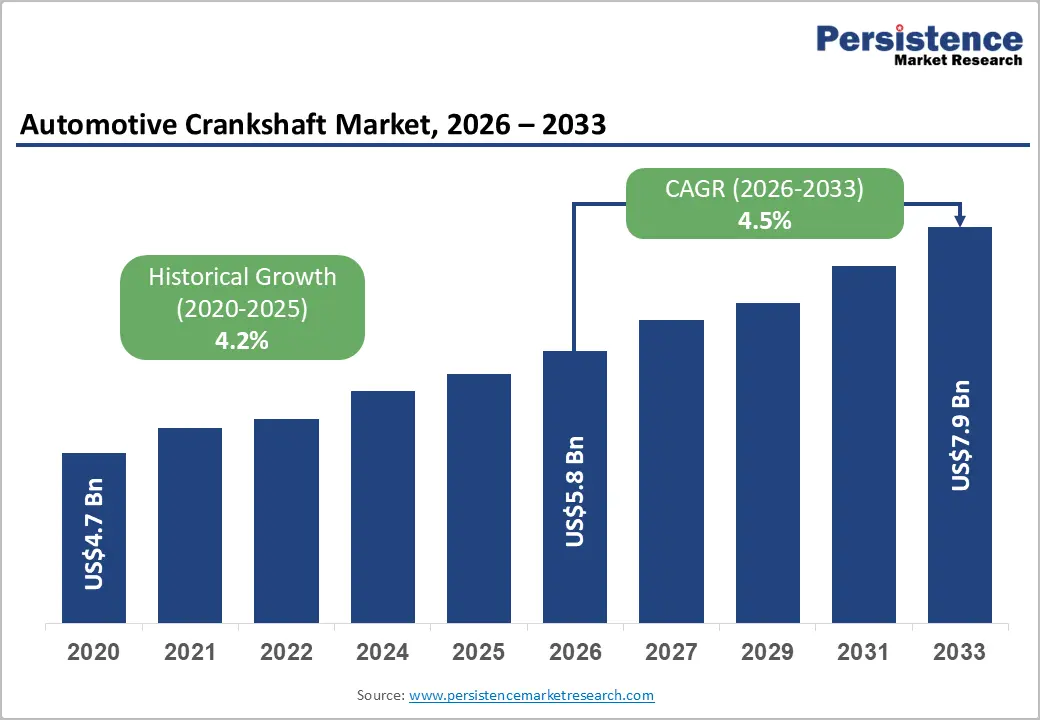

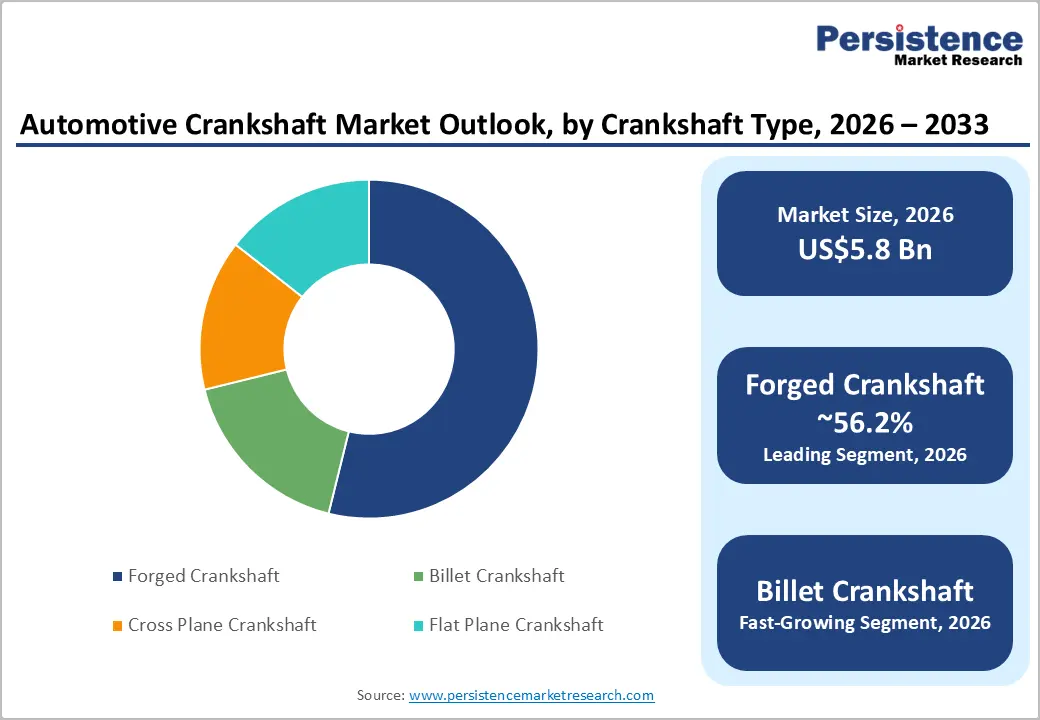

The global automotive crankshaft market size is likely to be valued at US$5.8 billion in 2026 and is expected to reach US$7.9 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033, driven by sustained internal combustion engine (ICE) and hybrid vehicle production, particularly in the Asia Pacific, where automotive manufacturing continues to be highly concentrated.

The market continues to benefit from material innovation, precision manufacturing technologies, and strong aftermarket demand, which collectively reinforce crankshaft relevance across passenger vehicles, commercial vehicles, and hybrid powertrains. However, long-term demand visibility is gradually being reshaped by electrification trends, requiring suppliers to adapt their product and investment strategies.

Key Industry Highlights:

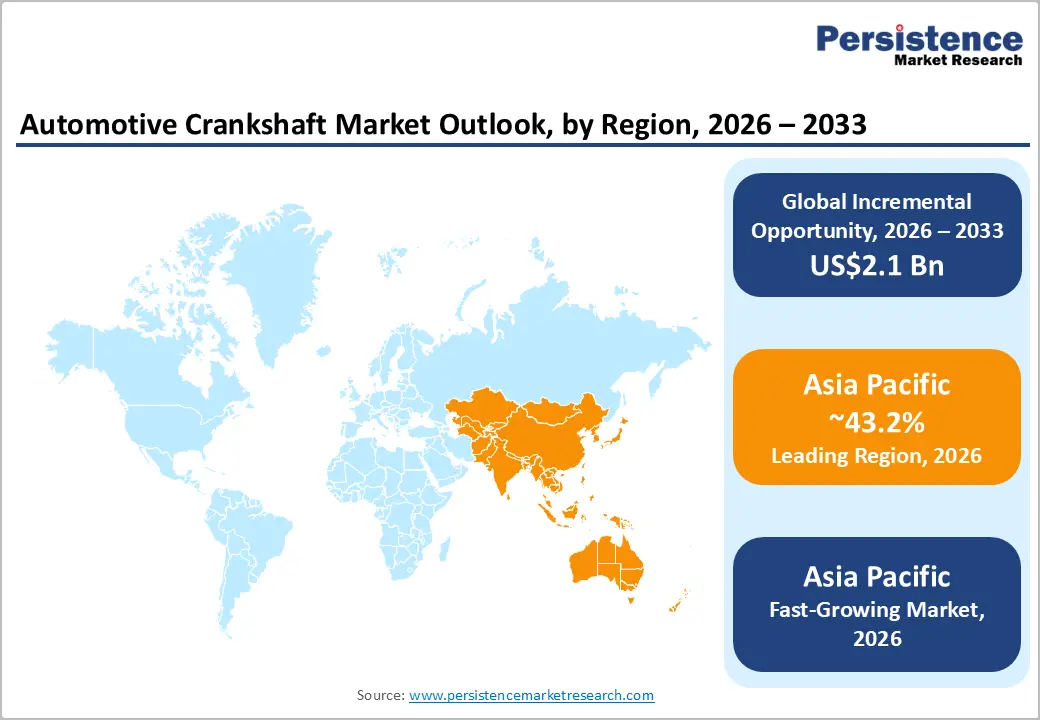

- Leading Region: Asia Pacific is projected to account for approximately 43.2% of market share, supported by high vehicle production volumes in China, India, Japan, and South Korea.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by increasing domestic demand, expanding manufacturing capacity, and strong localization strategies.

- Investment Plans: The market is witnessing significant investments in forging and machining capacity, with companies such as Bharat Forge Limited and Balu Forge Industries Limited expanding facilities, including projects with capacity additions exceeding 70,000 TPA, to support precision manufacturing and export growth.

- Dominant Crankshaft Type: Forged crankshafts dominate the market, holding an estimated 56.2% share, due to their superior strength, durability, and suitability for high-volume automotive applications.

- Leading Material: Steel alloy remains the leading material segment, accounting for approximately 63.2% of the market share, driven by its optimal balance of strength, fatigue resistance, and cost efficiency across passenger and commercial vehicles.

DRO Analysis

Driver - Rising Vehicle Production in Asia-Led Automotive Ecosystems

Crankshaft demand is directly correlated with global vehicle production volumes, particularly in regions with strong ICE and hybrid penetration. Global motor vehicle production reached 92.5 million units in 2024, with Asia-Oceania contributing 54.9 million units, significantly outpacing other regions. Within this, China accounted for 31.3 million units, India 6.0 million, Japan 8.2 million, and South Korea 4.1 million. This geographic concentration creates high-volume demand for crankshaft manufacturing, machining, and aftermarket replacement, supported by localized supplier ecosystems and export-oriented OEM operations.

The clustering of automotive manufacturing in Asia-Pacific enables cost efficiencies, supply chain integration, and economies of scale, which are critical for forged and machined components. From a strategic standpoint, this production concentration ensures stable, medium-term demand visibility for crankshaft manufacturers, particularly those integrated into regional OEM supply chains and capable of supporting high-volume production while maintaining consistent quality standards.

Increasing Powertrain Efficiency and Emission Compliance Requirements

Stringent emissions regulations and fuel-efficiency standards are increasing the technical complexity of crankshaft design and manufacturing. Modern engines demand crankshafts capable of handling higher torque loads, tighter dimensional tolerances, and reduced vibration, while also contributing to overall engine efficiency. Regulatory frameworks in major markets are accelerating this shift. In the United States, Phase 3 greenhouse gas standards for heavy-duty vehicles, beginning in 2027, are pushing manufacturers toward higher efficiency engines. Similarly, updated fuel economy standards for light and heavy-duty vehicles require improved combustion efficiency and reduced energy losses.

In Europe, tightening CO2 emission targets and broader automotive transition policies are driving demand for high-performance, lightweight, and precision-engineered crankshafts. These regulatory pressures do not eliminate crankshaft demand but instead elevate product specifications, favoring manufacturers with advanced forging, machining, and metallurgical capabilities. The net impact is a shift from volume-driven to value-driven growth, with technical differentiation becoming a key competitive advantage.

Restraint - Electrification Is Structurally Reducing Long-Term ICE Demand

The global transition toward electric vehicles represents the most significant structural restraint for the crankshaft market. Electric vehicles do not require crankshafts, which directly reduces the long-term addressable market. Electric vehicle sales exceeded 17 million units in 2024, accounting for more than 20% of global passenger car sales, with higher penetration in Europe and China. This trend is supported by government incentives, regulatory mandates, and investments in charging infrastructure.

While ICE and hybrid vehicles will continue to dominate in the near-to-medium term, particularly in emerging markets, long-term demand is expected to gradually decline, especially in passenger vehicle segments within developed economies. For crankshaft manufacturers, the key risk lies in shrinking OEM program pipelines and increasing dependence on fewer ICE platforms. This necessitates strategic diversification into hybrid applications, commercial vehicles, and adjacent precision-engineered components to mitigate demand erosion.

Opportunity - Hybrid Powertrains and Engine Downsizing Extend Component Relevance

Hybrid vehicles continue to rely on crankshafts, creating a critical bridge between traditional ICE systems and full electrification. Engine downsizing trends, aimed at improving fuel efficiency, place greater mechanical stress on crankshafts, increasing the need for high-strength, fatigue-resistant designs. This creates opportunities for forged and billet crankshafts in premium, high-performance, and hybrid applications, where precision engineering and durability are essential.

The focus is shifting toward high-specification components rather than mass-volume production, enabling suppliers to capture higher margins through technical differentiation. As hybrid adoption grows across passenger and commercial vehicle segments, crankshaft demand remains structurally supported, particularly in markets where full electrification faces infrastructure or cost barriers.

Localization Trends and Manufacturing Expansion in Emerging Markets

The ongoing shift toward localized manufacturing and diversified supply chains is creating new growth opportunities, particularly in India and Southeast Asia. India’s auto-component industry reached Rs. 6.73 lakh crore (USD 80.2 billion) in FY25, reflecting strong domestic demand and export momentum. Significant investments in forging and machining capacity are reinforcing this trend.

For instance, leading manufacturers are expanding production capabilities through greenfield facilities, advanced CNC machining, and increased forging capacity, enabling higher precision and scalability. These developments support shorter supply chains, reduced lead times, and improved cost competitiveness, making emerging markets increasingly attractive for global OEM sourcing. For crankshaft suppliers, this translates into opportunities to expand market share through localization, strategic partnerships, and export-oriented manufacturing models.

Category-wise Analysis

Crankshaft Type Insights

Forged crankshafts are anticipated to account for approximately 56.2% of the market share in 2026, driven by their superior mechanical properties, including high fatigue strength, durability, and load-bearing capacity. These characteristics make them the preferred choice across passenger vehicles, commercial vehicles, and heavy-duty applications, where operational reliability and long service life are critical. For instance, major OEMs such as Toyota Motor Corporation and Ford Motor Company extensively utilize forged crankshafts in high-volume engine platforms to ensure durability under continuous load cycles.

The widespread adoption of precision forging and controlled heat-treatment processes further reinforces their dominance in mass production environments. Cross-plane crankshafts are anticipated to hold 68% share in engine architecture, primarily due to their ability to deliver smoother engine operation, reduced vibration, and improved torque balance, particularly in larger displacement engines. These designs are widely used in V6 and V8 engines, including those found in premium vehicles and light trucks. From an OEM perspective, forged crankshafts remain the default configuration for high-volume manufacturing, supported by established supply chains, cost efficiency at scale, and consistent performance outcomes.

In contrast, billet crankshafts are likely to be the fastest-growing segment, driven by demand in high-performance, motorsport, and specialized engine applications. Billet crankshafts offer greater design flexibility and precision, as they are machined from solid metal blocks using advanced CNC technology.

For example, performance-focused manufacturers such as Ferrari N.V. and aftermarket specialists such as Crower Cams & Equipment Company utilize billet crankshafts in racing and high-performance engines to achieve custom stroke configurations and enhanced rotational balance. Although billet crankshafts have higher production costs, their ability to support customization, rapid prototyping, and performance optimization is accelerating adoption in niche but high-value segments.

Material Insights

Steel alloy is anticipated to account for approximately 63.2% of the market share in 2026, owing to its optimal balance of strength, durability, machinability, and cost efficiency. Steel alloys are widely used in crankshafts for both passenger and commercial vehicles, as they can withstand high cyclic stresses, thermal loads, and torsional forces over extended operating lifecycles. Leading automotive manufacturers such as Volkswagen AG and General Motors Company rely heavily on alloy steel crankshafts in their ICE and hybrid engine platforms to ensure consistent performance and compliance with durability standards.

Forged steel remains critical for high-performance and heavy-duty applications, particularly in diesel engines and commercial vehicles, where structural integrity and fatigue resistance are essential. For example, heavy-duty engine manufacturers like Cummins Inc. use forged steel crankshafts in truck and industrial engines to handle high torque loads and extended duty cycles.

The fastest-growing material segment is expected to be billet steel, driven by increasing demand for high-performance and customized crankshaft designs. Billet steel enables precise machining, consistent grain structure, and enhanced dimensional accuracy, making it ideal for performance-oriented and specialized applications.

The broader material trend reflects a shift toward lightweight, high-strength materials, as OEMs aim to improve fuel efficiency, reduce emissions, and enhance engine performance, particularly in hybrid and next-generation ICE platforms.

Regional Insights

North America Automotive Crankshaft Market Trends

North America represents a mature but high-value automotive crankshaft market, supported by a large vehicle fleet, strong aftermarket demand, and a high concentration of pickup trucks and commercial vehicles, which rely heavily on durable ICE powertrains.

U. S. Automotive Crankshaft Market Trends

The U.S. leads regional demand, with vehicle production exceeding 10.5 million units in 2024, supported by strong domestic consumption and export activity. Major OEMs such as Ford Motor Company and General Motors Company continue to invest in next-generation ICE and hybrid engines, particularly for trucks and SUVs, which require high-strength forged crankshafts.

Recent developments reflect sustained ICE relevance. For example, Ford Motor Company has committed investments toward hybrid truck platforms, including the F-150 hybrid lineup, reinforcing demand for precision-engineered crankshafts. Similarly, Cummins Inc. continues to advance clean-diesel and hydrogen-compatible ICE technologies that still rely on robust crankshaft systems. Regulatory frameworks play a critical role.

Stringent emission standards and fuel-economy requirements are pushing OEMs toward lighter, more efficient engine components, thereby increasing the adoption of advanced forging and machining techniques. This trend benefits suppliers capable of delivering high-performance, low-friction crankshaft designs.

Investment activity is also notable. Bharat Forge Limited has expanded operations in North America through its aluminum forging subsidiary, strengthening localized production and supporting OEM supply chains. This localization reduces lead times and improves supply chain resilience. The aftermarket remains a key growth driver, supported by the region’s aging vehicle fleet, which increases demand for replacement crankshafts and engine rebuild components.

Mexico Automotive Crankshaft Market Trends

Mexico serves as a critical manufacturing hub, with strong integration into U.S. supply chains. OEMs such as Stellantis N.V. and Nissan Motor Co., Ltd. operate large-scale production facilities, driving demand for locally sourced forged components, including crankshafts.

Europe Automotive Crankshaft Market Trends

Europe is characterized by high engineering standards, premium vehicle production, and a stringent regulatory environment, making it a key region for high-value crankshaft applications.

Germany Automotive Crankshaft Market Trends

Germany remains the largest automotive manufacturing hub in Europe, producing over 4 million vehicles annually. Leading OEMs such as Volkswagen AG, BMW AG, and Mercedes-Benz Group AG continue to invest in high-efficiency ICE and hybrid engines, particularly in premium and performance segments. For example, BMW AG has expanded its plug-in hybrid lineup, requiring advanced crankshaft systems capable of handling dual powertrain loads. This reinforces demand for precision-forged and lightweight crankshafts.

U.K. Automotive Crankshaft Market Trends

The U.K. supports high-performance and specialty vehicle manufacturing, with companies like Jaguar Land Rover Automotive PLC focusing on hybrid SUVs and performance engines, sustaining demand for advanced crankshaft designs.

Spain Automotive Crankshaft Market Trends

Spain acts as a major production base for European OEMs, with facilities operated by SEAT S.A. and other global manufacturers. The country’s role in high-volume vehicle assembly supports steady demand for cost-efficient forged crankshafts.

Regulatory pressure remains the primary market driver. Tightening CO2 emission targets are pushing OEMs toward downsizing, hybridization, and efficiency optimization, increasing the need for high-performance crankshaft materials and designs. Despite rapid electrification, ICE and hybrid vehicles still dominate the installed base.

This ensures ongoing demand for crankshafts in both OEM production and the aftermarket, particularly for premium and performance vehicles. European suppliers are increasingly focusing on lightweight materials, advanced metallurgy, and precision machining, positioning the region as a leader in technologically advanced crankshaft solutions.

Asia Pacific Automotive Crankshaft Market Trends

Asia Pacific is the largest and fastest-growing automotive crankshaft market, driven by high vehicle production volumes, cost-efficient manufacturing, and strong domestic demand.

China Automotive Crankshaft Market Trends

China is the dominant force in the region, producing over 31 million vehicles annually and accounting for approximately 20.8% of the market. Domestic OEMs such as BYD Company Limited and Geely Automobile Holdings Limited continue to expand hybrid and ICE production alongside EVs.

While China leads in EV adoption, hybrid and ICE vehicles remain critical, particularly in export markets. This dual-track strategy sustains significant demand for crankshaft manufacturing, especially for mid-range and commercial vehicles.

India Automotive Crankshaft Market Trends

India is emerging as a key growth engine, supported by rising vehicle demand, infrastructure development, and strong policy support for domestic manufacturing. Leading suppliers such as Bharat Forge Limited and Ramkrishna Forgings Limited are expanding forging and machining capabilities to meet both domestic and export demand.

Recent developments include capacity-expansion projects and investments in advanced CNC machining, enabling Indian manufacturers to move up the value chain. Additionally, global OEMs such as Hyundai Motor Company and Suzuki Motor Corporation continue to scale production in India, reinforcing demand for localized crankshaft supply.

Japan Automotive Crankshaft Market Trends

Japan remains a leader in precision engineering, with companies such as Toyota Motor Corporation and Honda Motor Co., Ltd. focusing on hybrid technology, which continues to rely on high-performance crankshafts.

Asia-Pacific benefits from low-cost manufacturing, strong supplier ecosystems, and increasing investments in forging and machining technologies. These factors enable high-volume production and global competitiveness.

The region is also seeing significant investments in advanced manufacturing facilities and localization strategies, reinforcing its role as the global hub for crankshaft production.

Despite rising EV adoption, the continued dominance of ICE and hybrid vehicles ensures strong medium-term demand growth, making Asia-Pacific the most critical region for market expansion.

Competitive Landscape

The global automotive crankshaft market is moderately consolidated at the top and fragmented at the regional level. Leading players collectively account for a significant share, supported by scale, long-term OEM relationships, and advanced manufacturing capabilities. Smaller and regional players compete on cost efficiency, localization, and niche applications, creating a competitive but diverse landscape.

Key players are focusing on precision manufacturing, vertical integration, localization, and diversification into high-growth segments. Emphasis is placed on advanced machining, material innovation, and hybrid-compatible component development to maintain competitiveness in a transitioning automotive landscape.

Key Industry Developments:

- In March 2025, Bharat Forge Limited announced continued expansion of its global forging and machining capabilities, including upgrades to its crankshaft manufacturing facilities, aimed at strengthening its position as a leading supplier of high-performance crankshafts for commercial and export markets, while improving production efficiency and scalability.

Companies Covered in Automotive Crankshaft Market

- thyssenkrupp AG

- Bharat Forge Limited

- Nippon Steel Corporation

- NSI Crankshaft LLC

- Maschinenfabrik Alfing Kessler GmbH

- Tianrun Industrial Technology Co., Ltd.

- CIE Automotive S.A.

- Crower Cams & Equipment Company

- Arrow Precision Engineering Ltd.

- Kellogg Crankshaft Company

- Sandvik AB

- Aichi Steel Corporation

- Musashi Seimitsu Industry Co., Ltd.

- Balu Forge Industries Limited

- Ramkrishna Forgings Limited

- MAHLE GmbH

Frequently Asked Questions

The global automotive crankshaft market is expected to be valued at US$5.8 billion in 2026.

The automotive crankshaft market is projected to reach US$7.9 billion by 2033.

Key trends include increasing adoption of forged crankshafts, growing demand for lightweight and high-strength materials, expansion of hybrid powertrains, and rising investments in precision forging and CNC machining technologies.

Forged crankshafts lead the market, accounting for approximately 56.2% share, driven by their superior strength and durability in high-volume automotive applications.

The automotive crankshaft market is expected to grow at a CAGR of 4.5% between 2026 and 2033.

Some of the major players include thyssenkrupp AG, Bharat Forge Limited, Aichi Steel Corporation, Musashi Seimitsu Industry Co., Ltd., and MAHLE GmbH.