- Home Appliances

- Refrigerator Market

Refrigerator Market Size, Share, and Growth Forecast, 2026 – 2033

Refrigerator Market by Product Type (Top Freezer, Bottom Freezer, Side-by-Side, French Door), Capacity (Less than 150 Liters, 150–250 Liters, 250–350 Liters, 350–500 Liters, More than 500 Liters), End-User (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Refrigerator Market Share and Trends Analysis

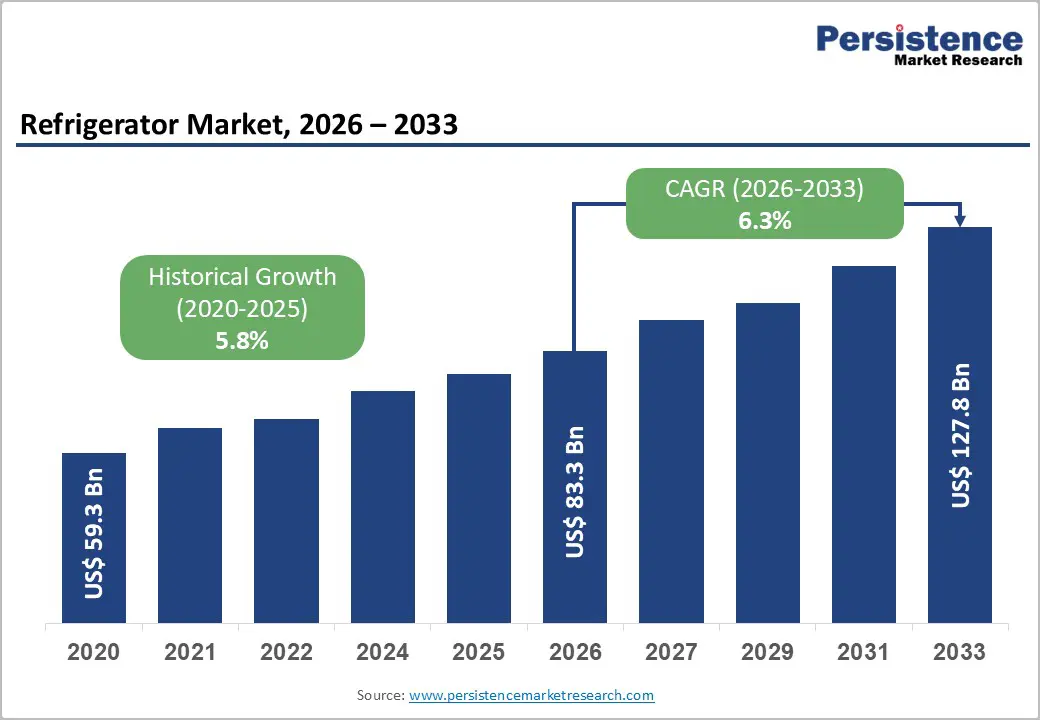

The global refrigerator market size is likely to be valued at US$ 83.3 billion in 2026, and is projected to reach US$ 127.8 billion by 2033, growing at a CAGR of 6.3% during the forecast period 2026−2033. Market expansion is driven by rising urbanization and household formation rates, which have increased the demand for energy-efficient and technologically advanced refrigerators, influencing consumer purchasing patterns. Technological integration, including smart and connected appliances, enhances product adoption and user experience, reinforcing market growth. Expansion of organized retail and e-commerce channels has widened product accessibility, improving distribution efficiency and fostering regional penetration. Regulatory emphasis on energy efficiency and environmental sustainability has guided product innovation, resulting in compliant, market-ready offerings. Demographic trends such as increased single-person households and nuclear families stimulate demand for diverse capacity options, while industrial and commercial adoption supports large-capacity and specialized refrigerators, complementing residential demand.

Key Industry Highlights

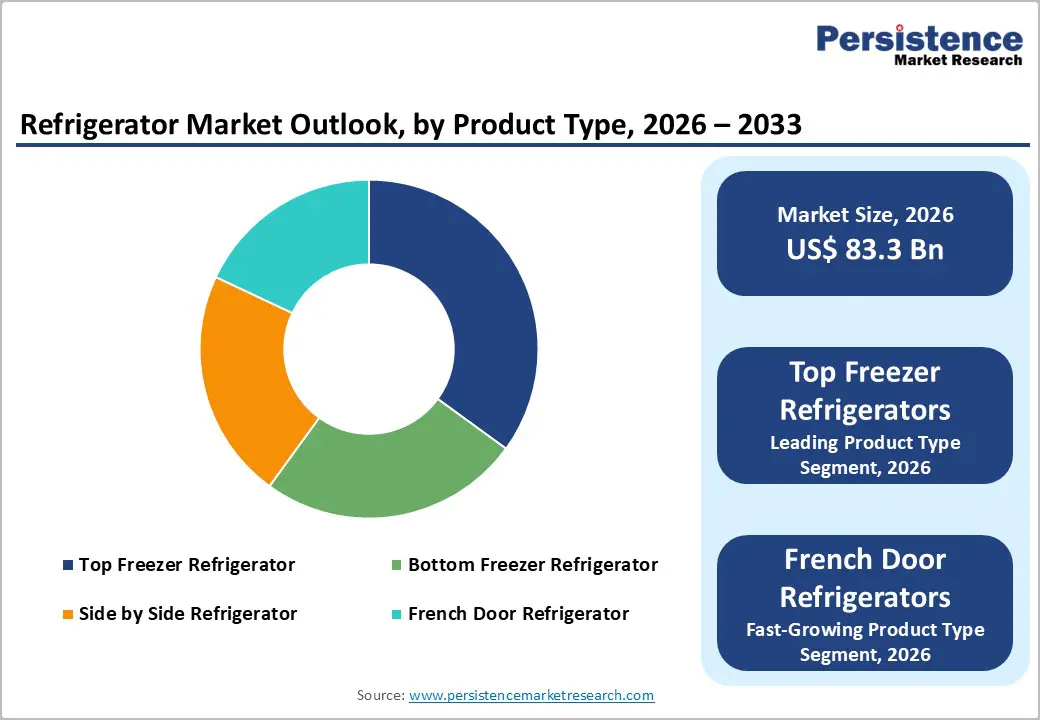

- Leading Product Type: Top freezer refrigerators are projected to hold a 35% market share by 2026, fueled by energy efficiency, affordability, compact design, and widespread retail availability.

- Fastest-growing Product Type: French door refrigerators are expected to be the fastest-growing segment by 2033, propelled by advanced storage options and expanded retail and digital availability.

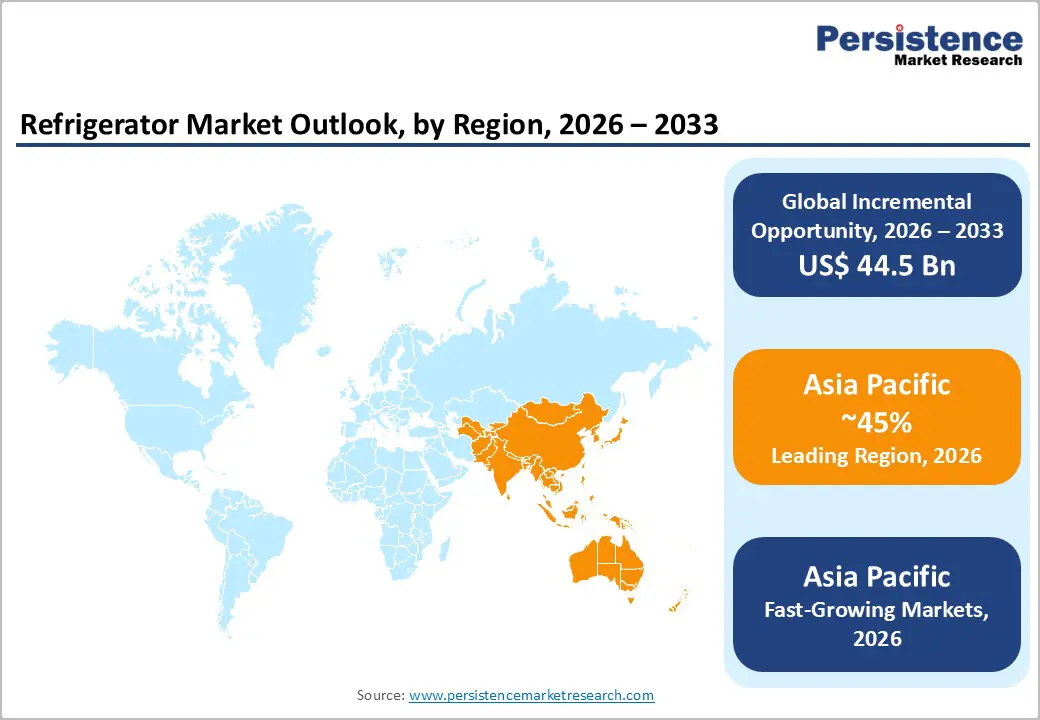

- Dominant Region: Asia Pacific is projected to hold a 45% market share by 2026, driven by evolving spending habits and proliferation of urban clusters.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing refrigerator market, supported by cold-chain expansion and increasing adoption of smart, energy-efficient appliances.

- January 2026: Haier launched its Frost Free 5252 refrigerator series in India with advanced 360° cooling, solar power compatibility, and enhanced freshness features.

| Insights |

Details |

|---|---|

|

Refrigerator Market Size (2026E) |

US$ 83.3 Bn |

|

Market Value Forecast (2033F) |

US$ 127.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancement and Smart Integration

Integration of smart technologies such as artificial intelligence (AI) and Internet of Things (IoT) in refrigerators serves as a primary driver for market growth due to the increasing demand for appliances that offer enhanced convenience, connectivity, and operational efficiency. Smart refrigerators have evolved beyond basic cooling functions to provide features such as real-time inventory tracking, remote access via mobile applications, and predictive maintenance alerts. These capabilities streamline household management, reduce food waste, and improve energy utilization. The embedding of AI and IoT allows appliances to adjust temperatures automatically, generate shopping lists, and provide expiration notifications, positioning refrigerators as central hubs in modern kitchens and elevating user experience across residential and commercial environments.

Smart technologies also enable efficiency improvements and alignment with sustainability objectives. Adaptive cooling systems optimize energy consumption, lowering operational costs while adhering to environmental standards. Compatibility with home automation platforms and voice-controlled interfaces further enhances convenience and user engagement, supporting differentiated offerings in competitive markets. Manufacturers leverage these technological features to deliver premium value propositions, stimulating demand for advanced models and influencing purchasing decisions.

High Upfront Costs of Advanced Models

Advanced refrigerator models entail a hefty price, which acts as a key restraint for the market, since elevated prices influence consumer purchasing decisions and limit adoption rates. Sophisticated models with smart features, connected systems, and enhanced energy efficiency require expensive components and significant research and development investment. Consumers face the full financial impact at the point of purchase, while benefits such as energy savings or improved convenience are realized over time. This timing mismatch reduces appeal among households with limited disposable income or short-term budgeting priorities. High purchase costs also encourage comparison with conventional models, leading many buyers to delay upgrades or select basic alternatives.

The effect of elevated prices is more pronounced in regions where discretionary spending is constrained or economic conditions limit affordability. Premium models are often perceived as luxuries rather than essential items, narrowing the target customer base and slowing adoption. Higher initial costs can also increase total cost of ownership, as advanced units may require specialized maintenance or repairs. Retailers may need to offer discounts or promotions to stimulate demand, which can pressure margins and complicate inventory management. In emerging economies, affordability challenges restrict penetration of technologically advanced units, reinforcing reliance on conventional alternatives.

Fusion with Renewable Energy Systems

Renewable energy systems can create strategic opportunities for the refrigerator ecosystem as they enhance value by aligning product capabilities with global energy trends and operational realities faced by consumers and businesses. Refrigeration devices powered or supported by renewable sources such as solar photovoltaic systems and energy storage reduce dependence on conventional grid electricity, leading to lower lifetime energy expenditure and increased operational resilience in regions with unstable power supply. By offering refrigerators that can pair with distributed energy resources, manufacturers position their products as cost-effective, future-ready solutions that deliver energy savings and uninterrupted performance. In 2025, distributed solar photovoltaic applications accounted for 42% of overall solar capacity expansion, reflecting widespread adoption of decentralized renewable power systems that can directly support connected appliances. This broader renewable energy penetration strengthens business cases for energy-integrated appliances, attracting environmentally conscious consumers, corporate buyers seeking lower total cost of ownership, and institutional clients focused on sustainability metrics.

Renewable-integrated refrigeration unlocks new revenue streams in rural and off-grid markets where lack of reliable electricity has constrained appliance adoption and cold-chain infrastructure. Systems that couple renewable generation with battery storage or smart energy management can ensure temperature stability for critical applications in healthcare, agriculture, and retail, improving service reliability and reducing spoilage costs. Offering energy-adaptive features can also support value-added services such as demand response participation or integration with microgrid solutions, enhancing utility partnerships and opening aftermarket opportunities. From a brand positioning perspective, renewable integration strengthens environmental commitments, enabling companies to meet corporate sustainability goals and improving appeal among stakeholders prioritizing clean energy transitions and resilient infrastructure deployments.

Category-wise Analysis

Product Type Insights

Top freezer refrigerators are likely to be the leading segment with approximately 35% revenue share in 2026, due to energy efficiency, affordability, and widespread retail availability. These models remain popular among consumers and households because they balance compact storage capacity with consistent performance, making them ideal for small and medium-sized kitchens. Compliance with energy standards adds further appeal, lowering electricity costs and supporting sustainability goals. Incremental innovations such as frost-free operation, antimicrobial coatings, and improved insulation enhance convenience and hygiene, reinforcing user confidence. Strong distribution networks and extensive retail penetration ensure easy access, while proven reliability sustains steady demand, particularly in urban and semi-urban households seeking practical and cost-effective refrigeration solutions.

French door refrigerators are expected to witness the fastest growth between 2026 and 2033, as enhanced storage flexibility, smart features, and aesthetic appeal drive adoption. Multi-door access, customizable temperature zones, and digital integration allow precise control over food preservation, catering to diverse household and commercial requirements. Lifestyle trends emphasizing premium and feature-rich appliances, along with rising disposable income, encourage greater adoption of these refrigerators. Expansion of e-commerce platforms and modern retail stores increases product visibility and availability. Continuous technological enhancements, including energy optimization and connectivity features, improve convenience and performance, supporting accelerated uptake across both residential and commercial segments seeking high-end refrigeration solutions.

Capacity Insights

The 250–350 liters segment is poised to lead with a forecasted 40% market share in 2026, owing to optimal suitability for small to medium households, energy efficiency, and adaptability to urban living spaces. This capacity meets the average daily food storage needs of families and individuals, balancing convenience with manageable electricity consumption. Compact dimensions allow placement in kitchens with limited space while maintaining adequate interior organization. Retail availability through modern outlets and standardization across brands ensures consistent access, and online platforms simplify the purchase process. Trusted performance, after-sales support, and easy maintenance strengthen consumer confidence, making this segment a stable and reliable revenue contributor across urban and semi-urban households.

The 350–500 liters segment is anticipated to be the fastest-growing segment between 2026 and 2033, driven by an increasing demand for large-capacity refrigerators in multi-person households and small commercial establishments. Changing lifestyles, including bulk grocery purchases, home meal preparation, and entertainment at home, require expanded storage solutions. Technological upgrades such as advanced cooling zones, energy optimization, and frost-free operation enhance reliability and efficiency. Rising awareness about long-term cost benefits, combined with preventive maintenance services, improves consumer trust. Growth of digital commerce and modern retail chains provides greater accessibility, ensuring faster adoption of high-capacity models in both residential and small commercial environments.

End-User Insights

Residential is positioned as the leading segment with nearly 60% of the refrigerator market revenue share in 2026, supported by rising household formation, urban apartment expansion, and demand for energy-efficient appliances. Consumers increasingly prioritize refrigerators that combine affordability with modern features, such as frost-free technology, digital controls, and optimized energy consumption. Brand reputation and after-sales support reinforce trust and influence purchasing decisions. Availability across modern retail stores and online platforms ensures convenient access, while seasonal promotions and warranty programs encourage adoption.

Commercial is expected to emerge as the fastest-growing segment between 2026 and 2033, driven by increasing adoption in hospitality, retail, and healthcare facilities. High-capacity units with advanced temperature management, specialized compartments, and remote monitoring address operational needs for bulk storage and product safety. Organizations focus on reducing operational costs and minimizing energy consumption through technology-enabled solutions. Policy initiatives supporting sustainable practices and energy-efficient procurement encourage investment. Integration with predictive maintenance, IoT-enabled tracking, and data analytics improves reliability, reduces downtime, and enhances asset management.

Regional Insights

North America Refrigerator Market Trends

North America is slated to hold a significant position in the market for refrigerators through 2033, fueled by high household penetration, urbanized population clusters, and strong consumer preference for energy-efficient and technologically advanced appliances. Adoption is driven by a focus on smart home integration, digital temperature controls, and appliances with connected features that enable remote monitoring and maintenance. Multi-door and French-door models gain popularity due to lifestyle trends favoring bulk grocery storage, home cooking, and organized food preservation. Extensive retail networks, online platforms, and home improvement chains enhance accessibility, while manufacturers leverage local production and distribution efficiency to maintain competitive pricing. Brand recognition, warranty programs, and reliable service infrastructure strengthen consumer trust, sustaining steady adoption across both urban and suburban households.

Market growth is further stimulated by commercial and industrial adoption, particularly in healthcare, hospitality, and food service sectors. Demand for high-capacity and specialized refrigeration units with energy optimization and predictive monitoring aligns with operational efficiency objectives. Sustainability initiatives and incentive programs promoting energy-efficient appliances encourage both residential and commercial procurement. Technological innovation, including frost-free systems, adaptive cooling zones, and antimicrobial features, enhances product differentiation and performance reliability. Collaboration between manufacturers, distributors, and digital commerce platforms facilitates rapid market penetration, while emerging trends in smart energy management and renewable energy integration create long-term growth opportunities.

Europe Refrigerator Market Trends

Europe maintains a steady position in the refrigerator market, driven by high consumer awareness of energy efficiency, advanced appliance standards, and sustainability compliance. Urban households and multi-person families increasingly prioritize compact yet technologically advanced models that deliver low energy consumption and consistent performance. Premium adoption is supported by a preference for feature-rich appliances, including frost-free systems, multi-temperature zones, and digital controls. Widespread availability through modern retail networks and e-commerce channels ensures efficient distribution and convenient purchase. Manufacturers leverage technological differentiation, local production capabilities, and standardized compliance with energy labeling regulations to strengthen market positioning.

Growth momentum is further enhanced by increasing investment in commercial refrigeration for sectors such as hospitality, healthcare, and retail. Rising focus on sustainable cold-chain solutions, including integration with renewable energy and smart monitoring systems, supports operational efficiency and long-term cost savings for business clients. Lifestyle trends favoring home-cooking, bulk grocery storage, and meal planning contribute to adoption of larger-capacity and multi-door models in residential segments. Policy frameworks promoting carbon reduction, eco-friendly appliance adoption, and energy conservation accelerate the introduction of compliant, high-performance refrigerators.

Asia Pacific Refrigerator Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 45% of the refrigerator market share, propelled by rising disposable incomes, expanding middle-class populations, and rapid urbanization. Increasing nuclear households and compact apartment living favor demand for energy-efficient, smart, and multi-functional refrigeration units. Expansion of modern retail networks and digital commerce platforms ensures wide product availability, while local manufacturing hubs provide cost-efficient solutions that strengthen competitiveness. High population density in urban clusters drives consistent appliance demand, enabling economies of scale. Investments in localized supply chains, targeted marketing, and product customization further reinforce leadership, attracting both global and domestic players to focus strategic operations in this area.

Rapid market growth in Asia Pacific makes it the fastest-growing market for refrigerators, driven by evolving consumption patterns, industrial adoption, and infrastructure development. Rising cold-chain requirements for food and pharmaceuticals generate demand for high-capacity and specialized units. Integration of renewable energy-ready solutions and IoT-enabled smart appliances aligns with sustainability and operational efficiency objectives, appealing to residential and commercial customers. Continuous technological innovation, including frost-free systems, advanced temperature management, and antimicrobial features, enhances product differentiation. Policy support for energy-efficient appliances and strategic collaboration between manufacturers, distributors, and digital commerce platforms accelerate penetration, ensuring strong growth across urban, semi-urban, and emerging locations.

Competitive Landscape

The global refrigerator market exhibits a moderately consolidated structure, with leading players capturing approximately 40% of total revenue, reflecting a balance between scale-driven leaders and competitive fragmentation. Major participants such as Godrej Enterprises, Panasonic, GE Appliances, Videocon International Ltd., AB Electrolux, and Haier Group Corporation anchor competitive intensity through broad product portfolios, strong distribution coverage, and sustained investment in research and development. These companies leverage manufacturing scale, supply chain efficiency, and brand recognition to maintain stable revenue positions across residential and commercial segments. Technological advancement, particularly in energy efficiency, smart connectivity, and product reliability, serves as a primary differentiator.

Competitive dynamics remain favorable for emerging and mid-sized participants due to evolving consumer preferences and regulatory emphasis on sustainability. Regional producers compete effectively by offering localized designs, cost-optimized models, and faster responsiveness to market demand. Innovation focused on differentiated features such as advanced cooling systems, antimicrobial interiors, and renewable energy compatibility enables newer entrants to gain visibility without direct scale competition. Energy efficiency compliance and digital retail penetration further reduce entry barriers by improving market access and consumer reach. Strategic partnerships with retailers and e-commerce platforms support faster penetration, while after-sales service quality strengthens long-term positioning.

Key Industry Developments

- In December 2025, Xiaomi launched the new Mijia Refrigerator Pro, a smart 560 L appliance with dual cooling, intelligent temperature control and remote management via the Mi Home app, designed to keep food fresher longer while enhancing hygiene and connected home convenience.

- In September 2025, Samsung unveiled a new range of 183 L single-door refrigerators in India with stylish Begonia and Wild Lily floral designs, featuring energy-efficient compressors, stabilizer-free operation, and durable interiors to blend aesthetics with everyday performance for modern households.

- In August 2025, Toshiba unveiled a premium glass-door refrigerator range in India, featuring large-capacity frost-free models with sleek black glass finishes, advanced freshness technologies like Pure BIO Deodorizer and Cool Air Wrap System, automatic ice maker, ultra-fresh storage zones, and energy-efficient inverter compressors to appeal to style- and performance-focused consumers.

Companies Covered in Refrigerator Market

- Godrej Enterprises.

- Panasonic.

- GE Appliances

- Videocon International Ltd.

- AB Electrolux

- Haier Group Corporation

- LG Electronics

- Samsung Electronics Co. Ltd.

- BPL Refrigeration

- Whirlpool Corporation

- Siemens AG

- Hisense Co. Ltd.

- Midea Group

Frequently Asked Questions

The global refrigerator market is projected to reach US$ 83.3 billion in 2026.

The market is driven by urbanization, rising household formation, demand for energy-efficient and smart appliances, expanding retail and e-commerce access, and growing residential and commercial cold-storage needs.

The market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Key market opportunities include expansion of energy-efficient and smart refrigerators, integration with renewable energy systems, growth of e-commerce distribution, rising demand for premium and large-capacity models, and increasing adoption across commercial and cold-chain applications.

Some of the key market players include Godrej Enterprises, Panasonic, GE Appliances, Videocon International Ltd., AB Electrolux, and Haier Group Corporation.