- Bulk Chemicals

- Rare Gases Market

Rare Gases Market Size, Share, and Growth Forecast 2026 - 2033

Rare Gases Market by Gas Type (Helium (He), Neon (Ne), Argon (Ar), Krypton (Kr), Xenon (Xe), Others), Mode of Supply (On-site Generation, Cylinders, Cryogenic Cylinders and Liquid Dewars), Application (Lighting, Welding & Metal Fabrication, Electronics & Semiconductors, Healthcare & Medical, Aerospace & Defense, Insulation, Others), and Regional Analysis, 2026 - 2033

Rare Gases Market Size and Trend Analysis

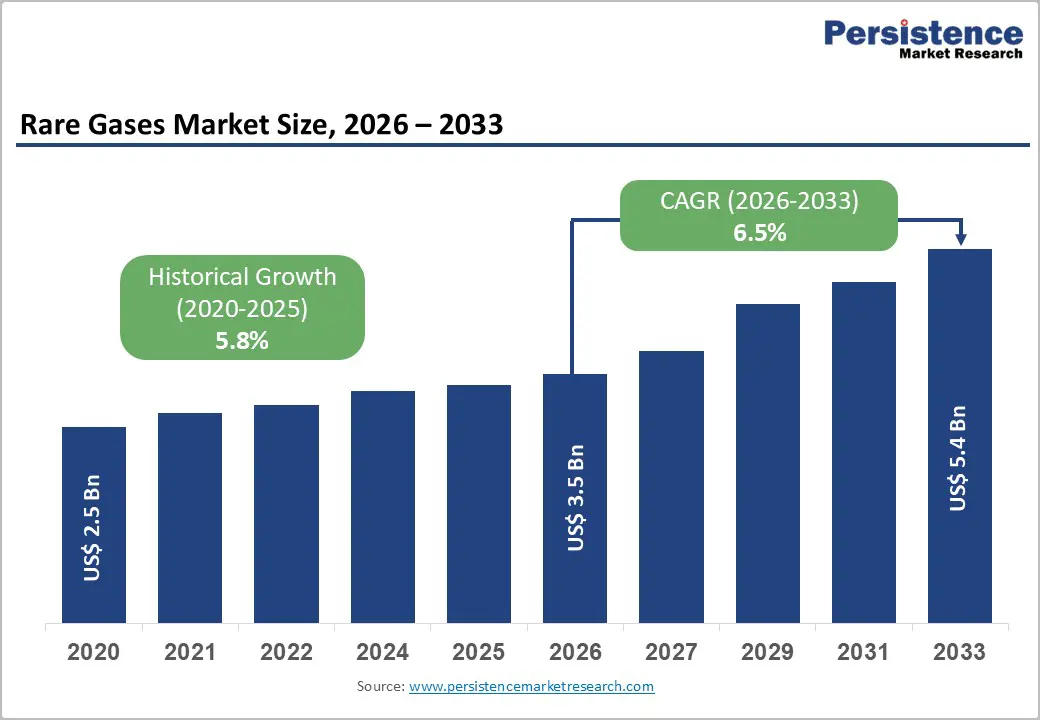

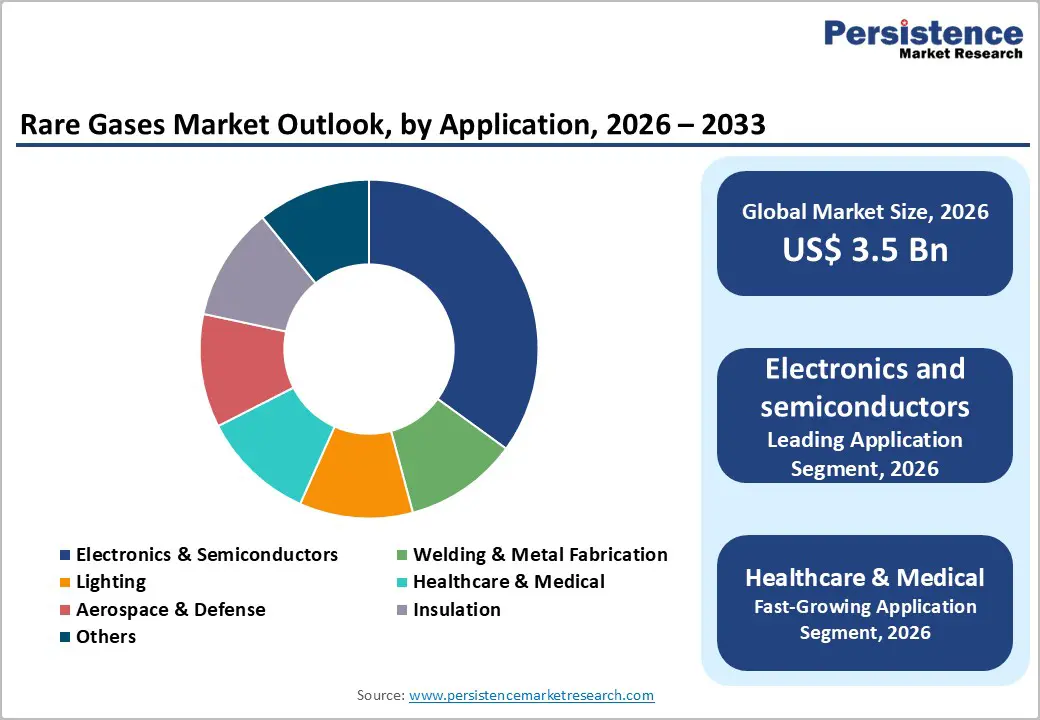

The global rare gases market size is expected to be valued at US$ 3.5 billion in 2026 and projected to reach US$ 5.4 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033. The market's sustained growth is fundamentally driven by surging demand for high-purity rare gases, helium, neon, argon, krypton, and xenon across the semiconductor, healthcare, and aerospace sectors.

The Semiconductor Industry Association (SIA) reported that global semiconductor sales surged 20.6% year-on-year between August 2023 and July 2024, directly amplifying neon, argon, and krypton consumption in chip fabrication. Simultaneously, global MRI installations exceeded 70,000 units in 2024, fueling helium consumption in cryogenic medical imaging at an annual rate of approximately 80 million cubic meters for healthcare alone. Expanding aerospace programs, advanced laser technologies, and quantum computing R&D further broaden the rare gases addressable market, ensuring structural demand momentum well into 2033.

Key Industry Highlights:

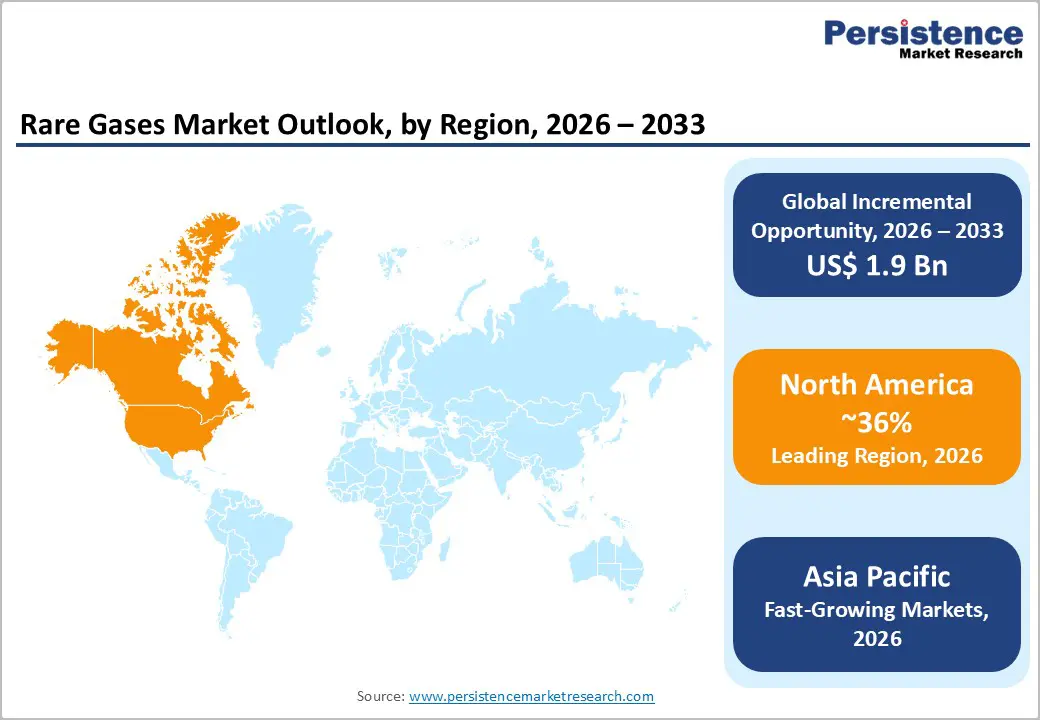

- Leading Region: North America leads the global rare gases market with approximately 36% share in 2025, driven by dominant U.S. helium production, major aerospace programs from NASA, SpaceX, and Planet Labs, and a surging semiconductor fab construction pipeline supported by the CHIPS and Science Act.

- Fastest Growing Region: Asia Pacific is the fastest growing rare gases market, projected at approximately 8.5% CAGR through 2033, underpinned by dense semiconductor fab concentrations across South Korea, Taiwan, Japan, and China, alongside rapid healthcare infrastructure expansion in India and ASEAN nations.

- Dominant Segment: Argon is the dominant gas type segment, commanding approximately 54% market share in 2025, owing to its abundant atmospheric availability, cost-efficient production via air separation, and critical role as a shielding gas in global welding, steel production, and semiconductor manufacturing operations.

- Fastest Growing Segment: Electronics and semiconductors is the fastest growing application segment, with neon demand for excimer laser lithography accelerating as TSMC, Samsung, and Intel expand 3 nm and 2 nm chip production lines, consuming significant neon volumes monthly and driving structural rare gas demand growth.

- Key Opportunity: Helium recovery and recycling technologies represent the most compelling market opportunity, enabling gas suppliers to offer long-term supply security contracts to MRI operators and semiconductor fabs, with Messer's MRI recycling unit achieving 85% helium recovery, a model set to scale industry-wide.

| Key Insights | Details |

|---|---|

| Rare Gases Market Size (2026E) | US$ 3.5 Billion |

| Market Value Forecast (2033F) | US$ 5.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.5% |

| Historical Market Growth (2020 - 2025) | 5.8% |

DRO Analysis

Drivers - Semiconductor Industry Expansion and Rising Demand for High-Purity Rare Gases

The explosive growth of the global semiconductor industry is the single most powerful demand catalyst for rare gases in the current decade. Neon is critical in excimer laser lithography, the dominant process for patterning advanced chips, with over 80% of global neon consumption directed toward chip manufacturing. Argon usage in the welding and semiconductor sector reached approximately 1.4 billion cubic meters in 2024, driven by surging manufacturing and electronics activity. The U.S. CHIPS and Science Act and parallel programs in the European Union, Japan, and South Korea are catalyzing over US$ 200 billion in semiconductor fab investments across Asia Pacific alone, each new fab requiring hundreds of millions of standard cubic feet of high-purity helium and neon over its lifecycle, directly propelling sustained rare gas demand.

Healthcare Sector Growth and Helium Demand in Medical Imaging

The global healthcare sector's accelerating adoption of advanced diagnostic imaging technologies is generating robust, long-term demand for medical-grade helium and xenon. Helium is the indispensable cryogenic coolant for superconducting magnets in MRI scanners, with over 70,000 MRI units globally as of 2024, consuming an estimated 80 million cubic meters of helium annually in the healthcare sector. In February 2024, Siemens Healthineers introduced the Magnetom Flow MRI featuring a closed-loop helium circuit, signaling a shift toward helium-efficient medical systems while simultaneously validating helium's irreplaceable role. Xenon is gaining traction in anesthesia and respiratory therapies, and healthcare infrastructure development in emerging economies such as India, Brazil, and Southeast Asia is set to structurally increase rare gas consumption over the forecast period.

Restraints - Supply Concentration and Geopolitical Vulnerabilities

The rare gases market is acutely exposed to supply chain fragility stemming from the geographic concentration of production. The U.S. holds approximately 40% of the world's helium reserves, exceeding 20 billion cubic feet, while neon production was historically concentrated in Ukraine, which at one point supplied over 40% of global neon. The Russia-Ukraine conflict triggered sharp neon price spikes, compelling semiconductor manufacturers to scramble for alternative supply. The 2024 privatization of the U.S. Federal Helium Reserve further shifted procurement dynamics, compelling end-users to negotiate directly with private suppliers. Fewer than 15 producers dominate global helium output, creating structural vulnerabilities that limit market responsiveness and introduce persistent pricing volatility.

High Production Costs and Capital-Intensive Extraction Infrastructure

The extraction, purification, and liquefaction of rare gases require sophisticated cryogenic air separation units and energy-intensive multi-stage distillation processes. Producing one liter of liquid helium alone consumes approximately 5.5 kWh of energy, making it significantly more expensive than conventional industrial gases. Neon and krypton purification involves multiple compression and distillation cycles, further inflating operational costs. European producers face a compounding challenge from soaring electricity tariffs, with German industrial power prices among the highest in the developed world, which have squeezed merchant gas margins and deterred greenfield investments in rare gas production. These cost barriers limit supply scalability and can translate into price volatility that constrains end-user adoption, particularly among budget-sensitive small and medium-sized manufacturers.

Opportunities - Quantum Computing and Advanced Aerospace Applications

The emergence of quantum computing represents one of the most significant new demand vectors for the rare gases market over the forecast period. Quantum processors operate at temperatures near absolute zero and require ultra-pure liquid helium for cryogenic cooling of superconducting qubits. Emerging applications in quantum systems are forecast to boost global helium demand by over 10 million cubic meters by 2025. Additionally, xenon-based ion propulsion systems have been adopted aboard over 120 satellites launched between 2020 and 2024 for deep-space and commercial missions. In September 2022, NASA selected Air Products and Chemicals Inc., Messer LLC, and Linde Inc. to supply over 1.4 million liters of liquid helium and 87.7 million standard cubic feet of gaseous helium for agency facilities, illustrating the scale of aerospace-driven rare gas demand expected through 2033.

Helium Recovery and Recycling Technologies for Semiconductor Fabs

With helium's non-renewable nature and geopolitical supply risks, helium recovery and recycling technologies are emerging as a high-value commercial opportunity for gas companies and equipment manufacturers. Messer Group developed and commercialized a portable helium recovery unit for MRI facilities capable of recycling 85% of helium used during MRI scans, significantly reducing operating costs for hospital operators. In the semiconductor sector, Samsung has implemented on-site neon recycling, capturing a significant share of its feedstock and reducing exposure to volatile import markets. Market participants who invest in gas reclamation systems, including on-site helium liquefiers, neon scrubbers, and xenon recovery units, are well-positioned to offer differentiated, long-term supply security contracts to semiconductor fabs, MRI operators, and aerospace manufacturers, creating a premium revenue stream that conventional bulk gas suppliers cannot replicate.

Category-wise Analysis

Gas Type Insights

Argon (Ar) leads the global rare gases market by gas type, commanding approximately 54% market share in 2025. Argon's dominance is rooted in its status as the most abundant rare gas in the Earth's atmosphere (approximately 0.93% by volume), making it the most cost-efficiently produced noble gas via cryogenic air separation. Argon is indispensable as a shielding gas in welding and metal fabrication, argon usage in the welding sector reached approximately 1.4 billion cubic meters in 2024, and as an inert atmosphere provider in semiconductor manufacturing, steel production, and solar panel fabrication.

Steel production and welding applications collectively account for more than half of total argon sales globally. Neon (Ne) is the fastest-growing gas type through 2033, driven by its irreplaceable role in excimer laser lithography for advanced semiconductor nodes, with global neon consumption in chip fabs anticipated to grow strongly as TSMC, Samsung, and Intel expand their next-generation production lines.

Mode of Supply Insights

Cryogenic cylinders and liquid dewars represent the dominant mode of supply in the rare gases market, capturing approximately 52% market share in 2025. The preference for cryogenic liquid supply is driven by the inherent thermodynamic efficiency of delivering gases in liquid form, enabling higher volume transfer, lower per-unit logistics costs, and on-demand vaporization at the point of use.

Large-scale semiconductor fabs, steel plants, MRI-equipped hospitals, and industrial welding facilities all rely on cryogenic liquid delivery for consistent, high-volume rare gas supply. Linde plc's commissioning of one of the world's largest helium storage caverns in Beaumont, Texas (capacity: 3 billion cubic feet) in July 2025 underscores the strategic importance of cryogenic infrastructure. On-site generation is the fastest-growing supply mode, particularly for argon and neon at semiconductor fabs, as manufacturers seek supply security and eliminate logistics vulnerabilities amid geopolitical disruptions.

Application Insights

Electronics and semiconductors is the leading application segment for rare gases, accounting for approximately 34% market share in 2025. Semiconductor fabrication is among the most gas-intensive industrial processes in the world, consuming neon for excimer laser lithography, argon for plasma etching and sputtering, helium for wafer cooling and leak detection, and xenon for ion implantation. The global electronics sector consumed more than 10,000 metric tons of rare gases, including neon, xenon, and argon, in 2024, driven by fabs operating in Taiwan, South Korea, Japan, China, and the United States.

The SIA confirmed global semiconductor sales surged 20.6% year-on-year through July 2024, directly amplifying rare gas demand. Healthcare and medical is the fastest growing application through 2033, sustained by MRI expansion, xenon anesthesia adoption, and emerging helium use in quantum computing and next-generation particle accelerator systems.

Regional Insights

North America Rare Gases Market Trends and Insights

North America is the leading region in the global rare gases market, accounting for approximately 36% market share in 2025, anchored by the United States' dominant helium production and the region's large-scale semiconductor and aerospace sectors. The U.S. holds approximately 40% of proven global helium reserves, and North American markets consumed over 80 million cubic meters of helium in 2024.

The region's aerospace sector, anchored by programs from NASA and commercial entities such as SpaceX and Planet Labs, generates significant xenon and helium demand for satellite propulsion and launch vehicle purging. The 2024 privatization of the U.S. Federal Helium Reserve has structurally reshaped helium procurement, compelling end-users to pivot to private long-term supply contracts.

In July 2025, Linde plc commissioned one of the world's largest helium storage caverns in Beaumont, Texas, with a capacity exceeding 3 billion cubic feet, reinforcing the region's supply infrastructure. Air Products & Chemicals has committed US$ 500 million in Louisiana for helium recovery from Gulf Coast gas streams, ensuring long-term supply for downstream customers. The U.S. CHIPS and Science Act is accelerating domestic semiconductor fab construction, structurally increasing neon and argon demand across the region through 2033.

Europe Rare Gases Market Trends and Insights

Europe is a significant consumer and technology hub in the global rare gases market, with Germany, the United Kingdom, France, and Spain forming the demand core. Germany and France maintain strong industrial welding and metal fabrication sectors that are among Europe's largest consumers of argon, including laser-arc hybrid welding processes that co-consume helium to deepen weld penetration, a trend that expanded across European automotive manufacturers in 2024.

The CERN Large Hadron Collider in Switzerland is one of Europe's highest-profile helium consumers, having contracted Linde Kryotechnik for two helium cryogenic refrigeration systems in December 2022. However, European producers face persistent headwinds from high energy costs, with German industrial power tariffs among the world's highest, squeezing cryogenic production margins. In response, Linde has undertaken waste-heat recovery retrofitting at its Leuna complex to mitigate energy cost pressures.

The EU's harmonized gas purity regulatory framework and strategic autonomy policies are prompting investment in domestic rare gas production capacity, reducing dependence on imports from geopolitically sensitive supply regions, particularly following Ukraine-related neon supply disruptions.

Asia Pacific Rare Gases Market Trends and Insights

Asia Pacific is the fastest growing region, projected to expand at a CAGR of approximately 8.5% between 2026 and 2033, underpinned by semiconductor fab proliferation and healthcare modernization across China, Japan, South Korea, and India. The region's semiconductor ecosystem, anchored by TSMC, Samsung, and SK Hynix, is a dominant driver of neon, argon, and helium demand. TSMC allocated substantial budgets in 2024-2025 to expand its 3 nm and 2 nm production lines, each of which requires significant monthly neon volumes for excimer laser lithography.

In April 2024, Air Liquide announced the construction of a new state-of-the-art krypton and xenon production plant in South Korea to supply the semiconductor and space industries, signaling strong regional commitment to rare gas infrastructure. India witnessed significant volume growth as Air Liquide launched new air separation units in Gujarat in 2024, expanding domestic rare gas availability. Across the ASEAN region, growing semiconductor assembly operations, solar panel manufacturing, and healthcare modernization programs are expected to sustain the Asia Pacific's position as the highest-growth rare gases market through 2033.

Competitive Landscape

The global rare gases market is characterized by a highly consolidated structure, with a limited number of multinational industrial gas companies controlling a significant share of production, refining, and distribution capacities. Strong entry barriers, including capital-intensive air separation units, limited helium reserves, and stringent purity requirements, reinforce market concentration and long-term dominance of established players.

From a strategic perspective, companies compete through secure sourcing and diversified supply portfolios, particularly for helium, alongside long-term supply contracts with semiconductor manufacturers, healthcare institutions, and aerospace clients. Increasing investments in gas recovery and recycling technologies are improving supply efficiency and sustainability. Market participants are also expanding into high-growth regions such as the Asia Pacific and the Middle East while enhancing capabilities in specialty gas purification and on-site generation systems. Additionally, a growing focus on high-purity applications in semiconductors and emerging technologies is shaping innovation and value-added service offerings.

Key Developments:

- September 2025: Messer North America, Inc. signed a long-term helium supply agreement with QatarEnergy for 3 million m³ of high-purity helium annually from Ras Laffan, diversifying its supply base and strengthening security of supply for downstream rare gas customers.

- July 2025: Linde plc commissioned one of the world's largest helium storage caverns in Beaumont, Texas, with a capacity exceeding 3 billion cubic feet, bolstering supply reliability for semiconductor, aerospace, and medical customers globally amid cyclical supply disruptions.

- April 2024: Air Liquide S.A. announced the construction of a new state-of-the-art krypton and xenon production plant in South Korea, specifically targeting the fast-growing semiconductor fabrication and satellite propulsion market, with operations expected to support leading chipmakers in the region.

Companies Covered in Rare Gases Market

- Linde plc

- Air Liquide S.A.

- Air Products & Chemicals, Inc.

- Messer Group

- Matheson Tri-Gas

- Iwatani Corporation

- American Gas Products

- Axcel Gases

- Nova Gas Technologies Inc.

- Air Water Inc.

- Ellenbarrie Industrial Gases

- Praxair Technology Inc.

- Amico Group

- GCE Group

- Rotarex

- Dakota Gasification Company

- Renergen Limited

Frequently Asked Questions

The global rare gases market is valued at US$ 3.5 billion in 2026 and is projected to reach US$ 5.4 billion by 2033 at a CAGR of 6.5%.

Demand is driven by semiconductor industry expansion, increased use of neon and argon in chipmaking, and rising MRI adoption requiring helium.

North America leads the market with around 36% share, supported by strong helium production and demand from semiconductor, aerospace, and healthcare sectors.

The key opportunity lies in helium recovery and recycling technologies that improve supply security, reduce costs, and support sustainability.

Key players include Linde plc, Air Liquide S.A., Air Products & Chemicals, Inc., Messer Group, Matheson Tri-Gas, and others competing on supply and technology.