- Biotechnology

- Rapid Microbiology Testing Market

Rapid Microbiology Testing Market Size, Share, and Growth Forecast 2026 - 2033

Rapid Microbiology Testing Market by Product (Instruments, Reagents & Kits, Consumables, Software & Services), by Technology (Nucleic acid-based, Growth-based, Immunoassays & biosensors, ATP bioluminescence, Flow cytometry), by Application (Clinical diagnostics, Pharmaceutical & biologics testing, Food & beverage safety, Environmental testing, Cosmetics & personal care, Research & academic use), End-user and Regional Analysis, 2026 - 2033

Rapid Microbiology Testing Market Share and Trends Analysis

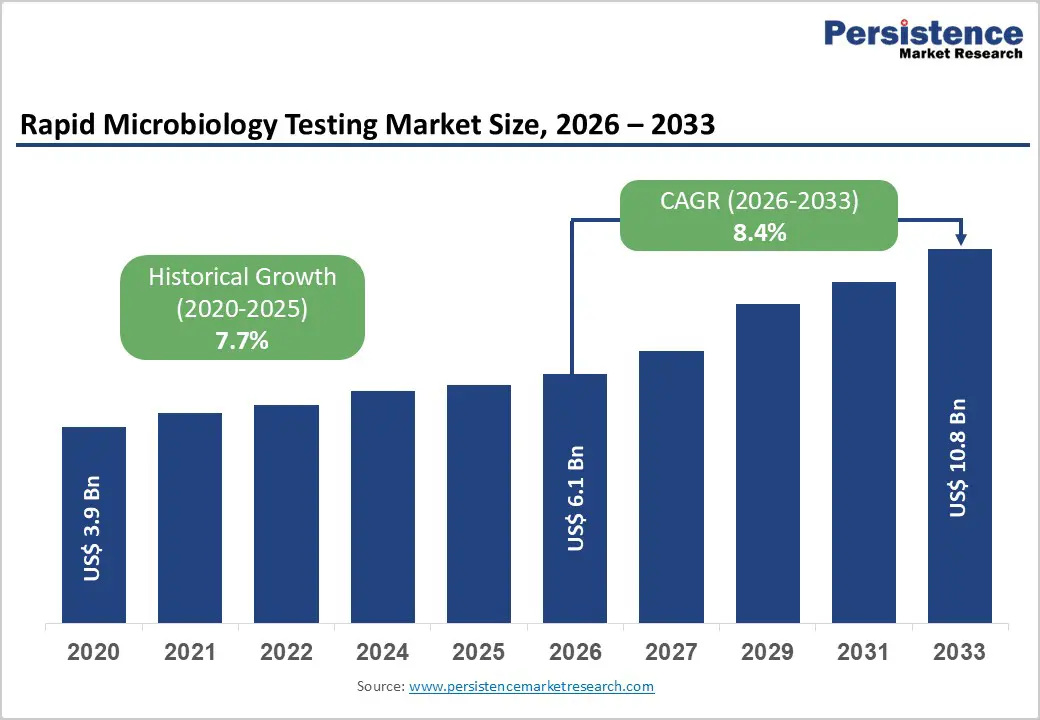

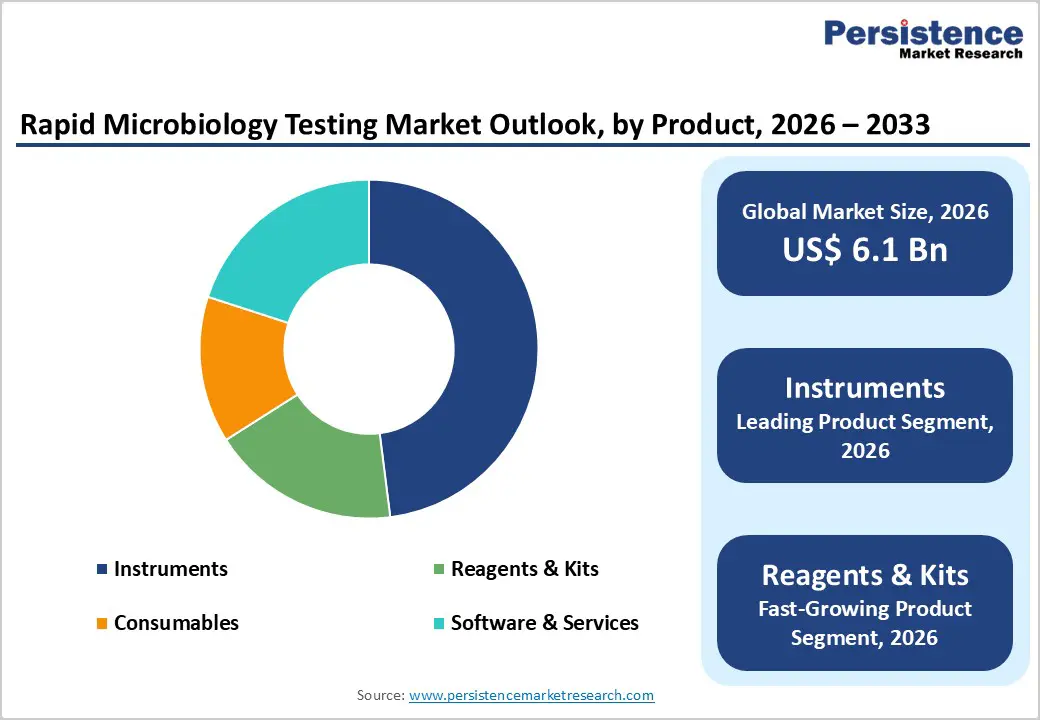

The global rapid microbiology testing market size is expected to be valued at US$ 6.1 billion in 2026 and projected to reach US$ 10.8 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033. Market growth is underpinned by rising infectious disease burden, sepsis, and antimicrobial resistance, which are compelling healthcare systems to adopt faster, more accurate microbiological methods to guide life-saving therapies.

At the same time, pharmaceutical and biopharmaceutical manufacturers face tightening regulatory expectations on sterility assurance and contamination control, pushing a shift from slow, traditional culture methods to automated rapid microbiological methods that shorten release cycles and enhance quality-by-design. Evolving regulations such as the In Vitro Diagnostic Medical Devices Regulation (EU) 2017/746 (IVDR) in Europe, along with increased focus on surveillance of healthcare-associated infections, further strengthen the business case for validated, high-throughput rapid microbiology platforms.

Key Industry Highlights:

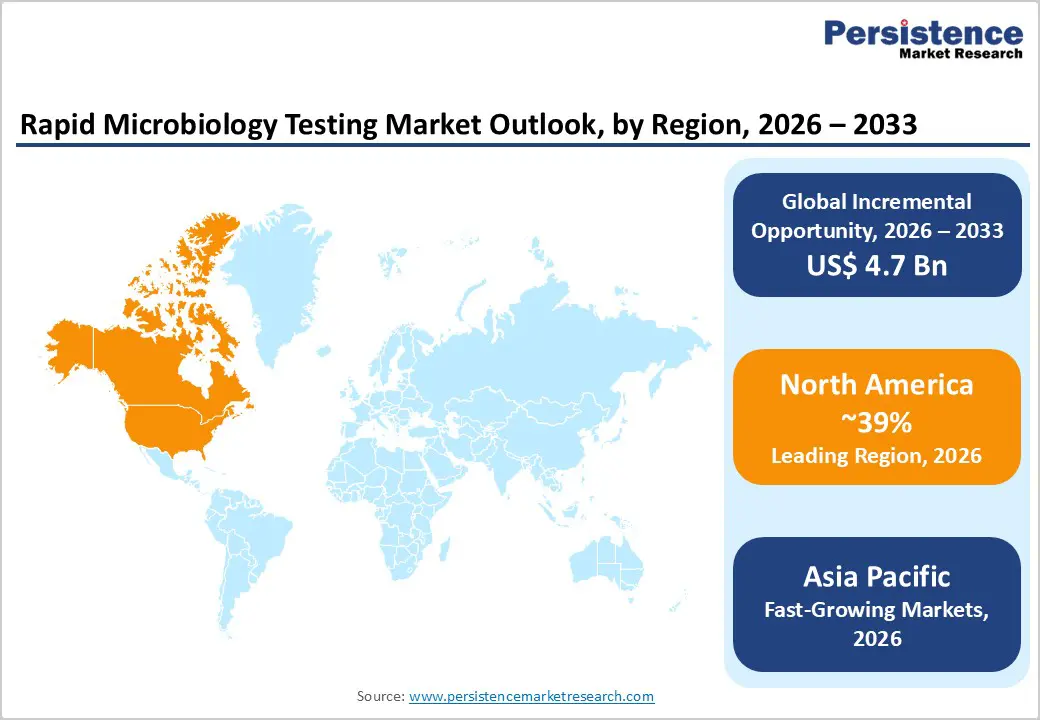

- North America is the leading region with around 39% share in 2025, supported by advanced hospital and reference lab infrastructure, strong regulatory oversight by the FDA, early adoption of MALDITOF and automated ID/AST platforms, and national initiatives focused on sepsis and AMR reduction that directly benefit the rapid microbiology testing market.

- Asia Pacific is the fastest-growing region, driven by large-scale pharmaceutical and biologics manufacturing investments in China and India, expanding healthcare access, rising food-safety expectations, and regulatory convergence toward global quality standards, which together create robust demand for modern rapid microbiology testing solutions in both clinical and industrial settings.

- Within products, Instruments are the dominant segment with about 48% share, reflecting widespread adoption of automated culture systems, MALDITOF MS, and integrated ID/AST analyzers that significantly reduce time-to-result and support high-throughput workflows across clinical, pharmaceutical, and food-safety laboratories worldwide.

- Reagents & Kits represent the fastest-growing product segment as laboratories expand their test menus with molecular panels, immunoassays, and specialized culture or confirmation kits, generating recurring consumables demand across the installed base of rapid microbiology instruments and enabling flexible, application-specific testing strategies.

| Key Insights | Details |

|---|---|

| Rapid Microbiology Testing Market Size (2026E) | US$ 6.1 billion |

| Market Value Forecast (2033F) | US$ 10.8 billion |

| Projected Growth CAGR (2026 - 2033) | 8.4% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Drivers - Rise in Sepsis Burden and Antimicrobial Resistance

The rapid microbiology testing market is strongly driven by the global effort to reduce deaths from sepsis and combat antimicrobial resistance (AMR). Data cited by the World Health Organization (WHO) and global sepsis collaborators indicate around 48.9 million sepsis cases and approximately 11 million related deaths in 2017, accounting for about 20% of annual global deaths. This burden has prompted initiatives such as the 2030 World Sepsis Declaration, which calls for earlier detection and optimized treatment pathways, directly supporting adoption of rapid diagnostic technologies that can deliver actionable microbiology results within hours rather than days. Rapid identification and antimicrobial susceptibility systems like VITEK® COMPACT PRO from bioMérieux, which has received FDA 510(k) clearance, are designed to provide faster organism ID/AST to guide targeted therapy and improve outcomes in both clinical and industrial settings. As AMR continues to complicate empiric treatment, hospitals and labs are investing in rapid microbiology platforms that enable antimicrobial stewardship teams to de-escalate or optimize antibiotics earlier in the patient journey.

Stricter Pharmaceutical Quality Control and Sterility Requirements

Another major growth driver is the tightening of sterility and contamination-control expectations in pharmaceutical and biologics manufacturing. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) require manufacturers to implement robust microbiological control strategies under current Good Manufacturing Practice (cGMP), emphasizing validated test methods, environmental monitoring, and rapid detection of contaminants to protect patient safety. Traditional sterility tests can require up to 14 days of incubation before batch release, whereas modern rapid microbiological methods and automated growth-based systems can substantially reduce this window, supporting faster time-to-market for high-value biologics and sterile injectables. In parallel, the EU IVDR 2017/746 raises expectations for performance evidence, traceability, and post-market surveillance for diagnostic systems, encouraging wider deployment of scientifically validated and automated rapid microbiology technologies in both in-house and commercial labs across Europe. Collectively, these regulatory and quality imperatives are driving investment in advanced rapid microbiology instruments, reagents, and software that support continuous process verification and real-time release strategies.

Restraints - High Upfront Capital Costs and Validation Burden

Despite clear benefits, the adoption of rapid microbiology methods is constrained by the significant upfront capital investment required for advanced instruments, automation, and lab-information system integration. Smaller hospitals, contract labs, and manufacturers in emerging markets may struggle to justify these expenditures without high test volumes or strong reimbursement mechanisms. In addition, regulatory frameworks require extensive method validation demonstrating equivalence or superiority to compendial culture-based methods across parameters such as specificity, sensitivity, accuracy, and robustness, which can be both time and resource-intensive. This validation complexity is amplified in pharmaceutical and biologics applications, where product-specific validations are often required due to differing formulations and matrices, limiting the speed with which organizations can switch from legacy methods to new rapid platforms.

Limited Replacement of Conventional Culture Methods

Many rapid microbiology technologies still function as complements rather than full replacements for traditional culture-based tests, particularly where pharmacopoeias or internal quality standards mandate viable cell counts, broad environmental monitoring, or confirmatory testing. Molecular and phenotypic rapid tests may quickly flag the presence of particular pathogens or resistance markers, but final product release decisions may still rely on classical sterility or bioburden tests in certain regulated workflows. Additionally, technology limitations such as challenges in detecting very low-level contamination without enrichment, or incomplete coverage of rare or emerging organisms in identification databases mean that laboratories must often maintain dual workflows, adding operational complexity. This complementary role, combined with the need to retrain staff and re-engineer standard operating procedures, can slow full-scale transition to rapid microbiology testing, especially in cost-sensitive environments.

Opportunity - Advancement of Nucleic Acid-Based and Syndromic Testing Platforms

Nucleic acid-based technologies present a major opportunity for rapid microbiology testing vendors and end users. Polymerase chain reaction (PCR), isothermal amplification methods, and next-generation sequencing-based workflows enable highly sensitive and specific detection of pathogens and resistance genes directly from clinical specimens, food samples, or environmental matrices, often within a few hours. Molecular pathogen panels for bloodstream infections, respiratory diseases, gastrointestinal infections, and meningitis are gaining traction because they can simultaneously detect dozens of targets in a single run and provide faster guidance than stepwise culture. For example, commercially available molecular food-pathogen systems can complete enrichment, amplification, and detection within a single working shift, dramatically compressing the decision window for release, rework, or recall in food and beverage operations. As laboratories increasingly seek consolidated “syndromic” solutions, vendors that offer comprehensive test menus, validated sample-to-answer workflows, and connectivity into antimicrobial stewardship or quality systems are well positioned to capture growing demand.

Regulatory and Manufacturing Tailwinds in Asia Pacific

Asia Pacific offers strong medium- to long-term opportunities due to the rapid expansion of pharmaceutical, biologics, and vaccines manufacturing, along with intensifying food-safety and public-health initiatives in countries such as China, India, Japan, and members of the ASEAN bloc. Governments and regulators in the region are increasingly aligning with international quality standards and good manufacturing practices, pushing local producers to adopt more sophisticated microbiological testing and environmental monitoring tools to retain export market access for drugs, medical devices, and food products. In parallel, rising healthcare expenditure and the growing burden of infectious diseases in populous economies are spurring investments in modern clinical microbiology laboratories and rapid diagnostic technologies. As large biopharma clusters and contract manufacturing organizations scale up in the Asia Pacific, demand for rapid microbiology instruments, reagents, and software especially those integrated with automation and digital quality-management systems is expected to accelerate faster than in mature markets, making the region a focal point for strategic partnerships, technology transfers, and localized manufacturing by leading global players.

Category-wise Analysis

Product Insights

Within the product category, instruments form the leading segment, accounting for about 48% of the rapid microbiology testing market in 2025, reflecting the central role of high-performance analyzers in modern microbiology workflows. Instruments such as MALDI-TOF mass spectrometry platforms for microbial identification and automated ID/AST systems like VITEK® COMPACT PRO deliver rapid, standardized results that significantly shorten time-to-answer compared with manual methods. Evidence from clinical practice shows that MALDI-TOF MS can reduce identification times from 24-48 hours to minutes while also lowering per-test costs, supporting its widespread adoption as a new standard in many microbiology labs. At the same time, Reagents & Kits are the fastest-growing product segment, supported by recurring consumables demand and the expansion of molecular and immunoassay test menus across clinical, pharmaceutical, and food-safety applications. As installed instrument bases grow in North America, Europe, and Asia Pacific, ongoing purchase of panels, cartridges, culture media, and verification kits creates robust, annuity such as revenue streams for suppliers.

End-user Insights

In terms of End-user, hospitals & labs form the largest segment, underpinned by the high volume of clinical microbiology testing and the critical importance of turnaround time for patient management. Academic medical centers, reference laboratories, and integrated delivery networks have been pioneers in adopting MALDI-TOF MS, rapid ID/AST platforms, and multi-pathogen molecular panels, often demonstrating reductions in time-to-effective therapy and improvements in antimicrobial stewardship metrics compared with legacy workflows.

Pharma & biotech companies represent the fastest-growing end-user segment, particularly those engaged in sterile manufacturing, cell and gene therapy, and large-scale biologics production. As biopharmaceutical pipelines expand and more facilities seek global regulatory approvals, rapid microbiology testing becomes a strategic enabler of manufacturing flexibility, supporting faster scale-up, technology transfers, and real-time quality monitoring. Contract research organizations (CROs) and specialized contract testing labs also play a growing role, offering outsourced rapid microbiology services to smaller manufacturers and healthcare institutions that may not initially be able to justify investment in advanced instrumentation.

Regional Insights

North America Rapid Microbiology Testing Market Trends and Insights

North America holds a leading position in the Rapid Microbiology Testing Market due to its advanced healthcare infrastructure, strong pharmaceutical and biotechnology industries, and strict regulatory standards for product safety and quality. Regulatory authorities such as the U.S. Food and Drug Administration emphasize rapid and accurate microbial detection in pharmaceuticals, biologics, and food products, encouraging the adoption of rapid testing technologies. The region also benefits from the strong presence of major biotechnology and diagnostics companies such as Thermo Fisher Scientific and Danaher Corporation, which continuously invest in innovative testing platforms and automation systems. Growing concerns about hospital-acquired infections and antimicrobial resistance further increase the demand for rapid microbial diagnostics in clinical laboratories. Additionally, pharmaceutical manufacturers are increasingly adopting rapid sterility and contamination testing methods to improve production efficiency and regulatory compliance. The expansion of biopharmaceutical manufacturing and increasing investments in research and development are expected to further strengthen market growth in North America.

Asia Pacific Rapid Microbiology Testing Market Trends and Insights

The Asia Pacific Rapid Microbiology Testing Market is emerging as a significant growth region due to expanding pharmaceutical manufacturing, increasing healthcare investments, and rising awareness regarding microbial contamination control. Countries such as China, India, Japan, and South Korea are witnessing rapid growth in biotechnology and biopharmaceutical production, which is increasing the demand for advanced microbial testing technologies. Governments in the region are strengthening regulatory frameworks and quality standards for pharmaceuticals, food safety, and environmental monitoring, encouraging industries to adopt rapid microbiology testing solutions. In addition, the expansion of hospital laboratories, diagnostic centers, and research institutes is supporting the use of faster and more accurate microbial detection methods. Rising concerns about infectious diseases and hospital-acquired infections are also promoting the adoption of molecular and automated testing systems. Furthermore, growing investments by global and regional diagnostic companies in manufacturing facilities and research collaborations are expected to accelerate technological adoption, making Asia Pacific one of the fastest-growing regions in the rapid microbiology testing market.

Competitive Landscape

The rapid microbiology testing market is characterized by intense competition with the presence of several global and regional participants offering advanced microbial detection technologies. Companies compete primarily through technological innovation, product portfolio expansion, and continuous investment in research and development to deliver faster, accurate, and automated testing solutions. The market is moderately consolidated, where a few major players hold significant revenue share while smaller and emerging companies focus on niche technologies and specialized applications. Strategic activities such as mergers, acquisitions, collaborations, and new product launches are commonly adopted to strengthen market presence and expand geographic reach.

Key Developments:

- In November 2025, Lonza Group signed an agreement to acquire Redberry SAS, a company specializing in rapid microbiology testing solutions based on solid-phase cytometry technology. The acquisition added Redberry’s Red One platform to Lonza’s portfolio, enabling rapid sterility and bioburden testing for pharmaceutical quality control laboratories.

- In April 2025, Karius, Inc. launched Karius Focus | BAL, a rapid microbial cell-free DNA diagnostic test designed to improve the detection of pathogens responsible for pneumonia and other lung infections. The test utilizes metagenomic sequencing technology to identify and classify more than 500 pathogens using just 1 mL of bronchoalveolar lavage (BAL) fluid, delivering results within one day of sample receipt.

- In May 2025, LEX Diagnostics collaborated with ZeptoMetrix to enable the development of an ultra-fast thermocycling PCR device designed for rapid detection of respiratory viruses, including SARS-CoV-2, at the point of care.

Companies Covered in Rapid Microbiology Testing Market

- bioMérieux S.A.

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Abbott Laboratories

- Becton

- Dickinson and Company (BD)

- Bruker Corporation

- Charles River Laboratories International, Inc.

- Merck KGaA

- Quidel Corporation

- Rapid Micro Biosystems, Inc.

- NEOGEN Corporation

- Don Whitley Scientific Limited

- 3M Company

- Sartorius AG

- Accelerate Diagnostics, Inc.

- BioControl Systems, Inc.

- Other relevant regional participants

Frequently Asked Questions

The global Rapid Microbiology Testing Market is expected to reach around US$ 6.1 billion in 2026, supported by increasing adoption of rapid diagnostics in clinical care, pharmaceutical sterility testing, and food-safety applications where shorter turnaround times and higher testing throughput are becoming essential.

Key demand drivers include the high global burden of sepsis about 48.9 million cases and 11 million deaths annually alongside rising antimicrobial resistance, stricter pharmaceutical and food-safety regulations, and the need for faster, more sensitive microbiological methods than traditional culture to guide timely clinical and manufacturing decisions.

North America is the leading region, with an estimated 39% share in 2025, driven by sophisticated hospital and reference-lab networks, a strong base of pharmaceutical manufacturers, proactive FDA regulatory activity, and extensive adoption of advanced technologies such as MALDI-TOF MS and automated ID/AST platforms.

One of the most attractive opportunities lies in expanding nucleic acid-based and syndromic rapid testing platforms, including PCR and isothermal systems, to address AMR and complex infectious diseases while also serving stringent sterility and contamination-control needs in Asia Pacific’s rapidly expanding pharmaceutical and biologics manufacturing ecosystem.

Major participants include bioMérieux S.A., Thermo Fisher Scientific Inc., Danaher Corporation (with Beckman Coulter and Cepheid), Abbott Laboratories, Becton, Dickinson and Company (BD), Bruker Corporation, Charles River Laboratories International, Inc., Merck KGaA, Quidel Corporation, Rapid Micro Biosystems, Inc., NEOGEN Corporation, and Don Whitley Scientific Limited, among others, all of which offer specialized rapid microbiology instruments, reagents, and services across clinical, industrial, and research applications.