- Smart Packaging

- Printed Rigid Packaging Market

Printed Rigid Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Printed Rigid Packaging Market by Material (Paper & Paperboard, Bioplastics & Plant-Based Fibers, Others), Packaging Format (Folding Cartons, Rigid Boxes, Others), End-use Industry, Printing Technology, and Regional Analysis for 2026 - 2033

Printed Rigid Packaging Market Size and Trends Analysis

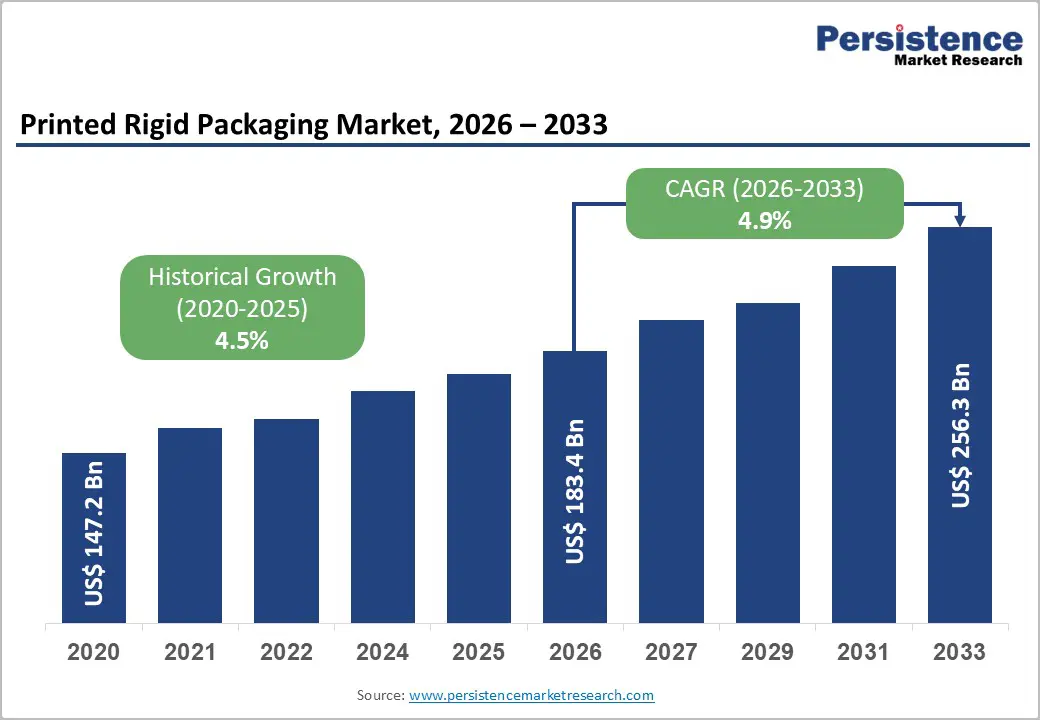

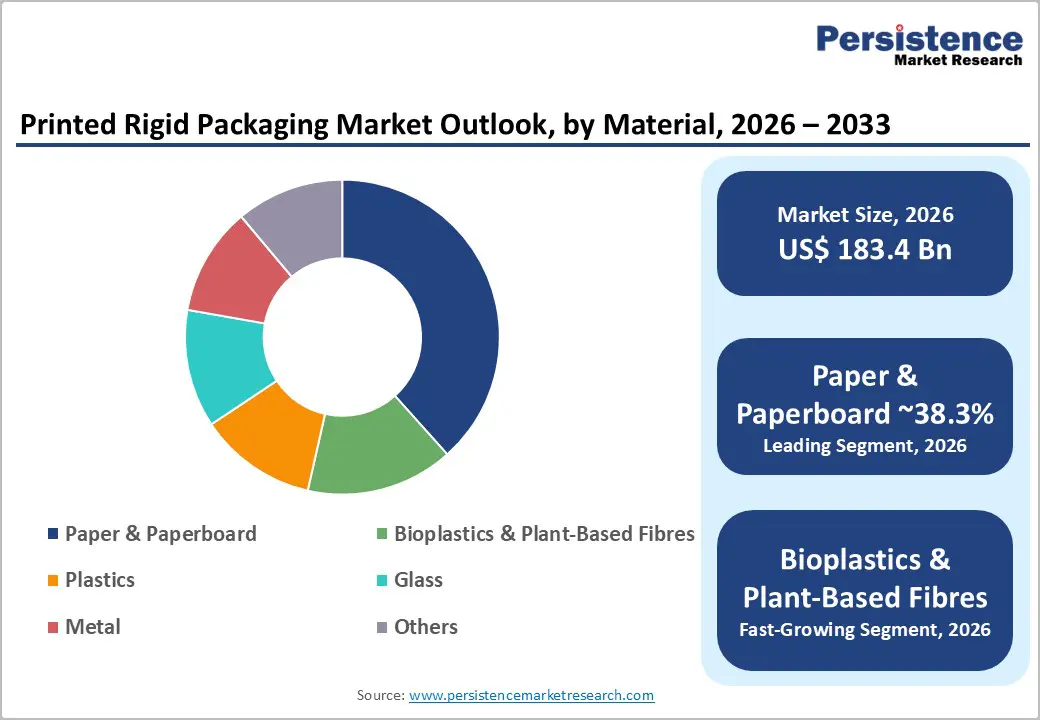

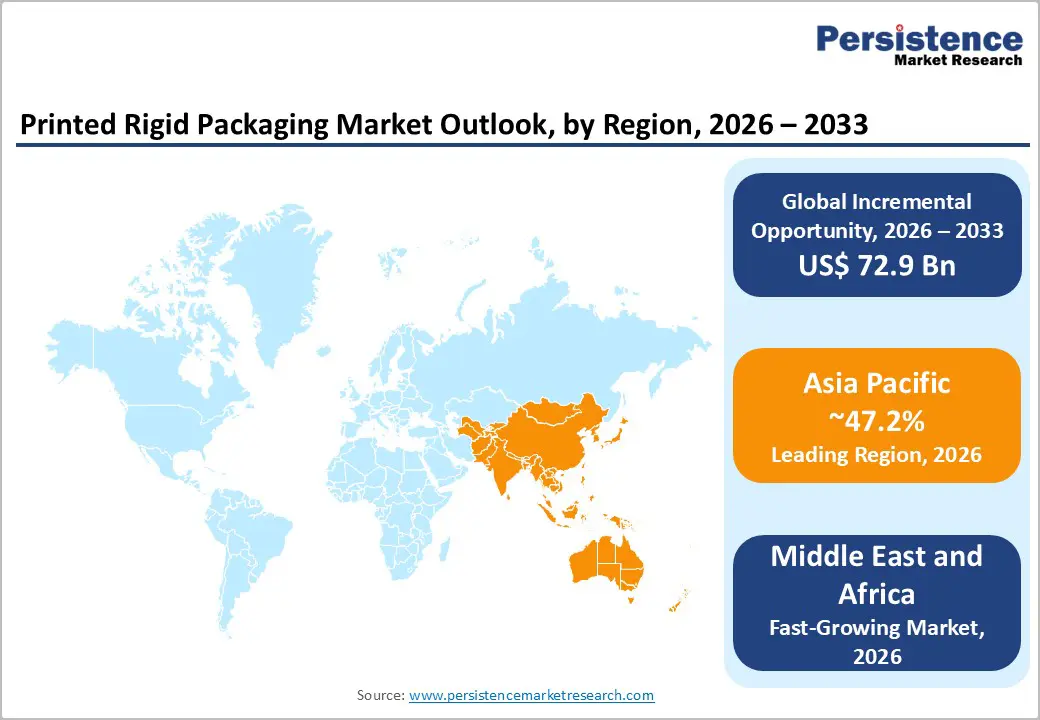

The global printed rigid packaging market size is likely to be valued at US$183.4 billion in 2026 and is expected to reach US$256.3 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven increasing consumer packaged goods branding requirements, rising demand for premium and protective packaging formats, and large-scale investments by packaging converters in advanced printing technologies and sustainable substrates.

Paper and paperboard-based rigid packaging formats such as folding cartons and board boxes remain dominant, supported by strong recyclability credentials and cost efficiency. Meanwhile, digital printing adoption is accelerating in high-SKU production environments, enabling faster product launches and improved customization. Growth prospects remain strongest in markets where sustainability regulations drive recyclable packaging adoption and where e-commerce logistics demand durable, print-intensive packaging solutions.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to hold 47.2% of the market, driven by strong manufacturing capacity and rising packaged goods consumption.

- Fastest-growing Region: The Middle East & Africa is the fastest-growing region due to rapid urbanization, expanding retail infrastructure, and increasing demand for packaged food and personal care products.

- Investment Plans: Packaging manufacturers are investing heavily in digital printing technologies, recyclable paperboard packaging, and automated converting lines to improve sustainability and production efficiency.

- Dominant Material: The paper and paperboard segment is expected to lead the material segment with an anticipated market share of 38.3%, supported by recyclability, strong print compatibility, and widespread adoption in food and beverage packaging.

- Leading Packaging Format: Folding cartons dominate the packaging format segment with a 35.6% share, driven by cost efficiency, strong branding capabilities, and high adoption in FMCG packaging.

| Key Insights | Details |

|---|---|

| Printed Rigid Packaging Market Size (2026E) | US$183.4 Bn |

| Market Value Forecast (2033F) | US$256.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Transition toward Sustainable and Recyclable Packaging

Government regulations and environmental policies across major economies are reshaping packaging design and materials usage. Authorities are increasingly enforcing extended producer responsibility (EPR) programs, recycled-content mandates, and packaging waste reduction targets, compelling manufacturers to transition toward recyclable and fiber-based packaging formats. These policies encourage the use of mono-material rigid packaging structures and discourage complex multilayer plastic solutions. In response, brand owners are shifting toward paperboard-based rigid packaging with recyclable coatings and water-based inks, which can comply with circular economy guidelines. Packaging converters are investing in upgraded printing lines and sustainable barrier technologies capable of meeting these regulatory requirements while maintaining visual quality. As regulatory frameworks become more stringent, demand for certified recyclable rigid packaging formats is expected to rise steadily, creating long-term growth opportunities for manufacturers that develop environmentally compliant packaging solutions.

Printing Technology Advancement and SKU Proliferation

Technological advancements in packaging printing have significantly improved productivity and customization capabilities. Digital printing systems, hybrid flexographic presses, and UV-curing technologies are reducing production setup times and minimizing material waste. These developments allow packaging converters to produce smaller batch sizes at competitive costs while maintaining high print quality. Brands increasingly require short-run promotional packaging, regional product variants, and seasonal designs, which necessitate flexible printing capabilities. Digital printing enables variable data printing and rapid design changes without the need for expensive printing plates. As a result, converters can respond quickly to marketing campaigns and product launches. The increasing number of stock-keeping units (SKUs) across food, personal care, and consumer electronics categories is therefore driving the adoption of advanced printing technologies in the rigid packaging industry.

Expanding Demand from Food & Beverage and Personal Care Industries

The food & beverage industry remains the primary consumer of printed rigid packaging, driven by rising demand for packaged food products, convenience meals, and ready-to-eat products. Consumers increasingly prioritize product safety, hygiene, and shelf-life stability, which rigid packaging formats effectively provide. Premiumization in beverage and personal care products is driving demand for visually appealing packaging that enhances brand differentiation. High-quality printed rigid packaging helps brands communicate product information, nutritional content, and brand identity directly on the package. As retail environments become more competitive, manufacturers rely on visually striking packaging to attract consumer attention and strengthen brand loyalty, thereby expanding demand for printed rigid packaging solutions.

Barrier Analysis - Raw Material Price Volatility

The printed rigid packaging industry relies heavily on raw materials such as pulp, recycled paper fiber, plastics, and metal. Price fluctuations in these materials can significantly affect production costs and profit margins. For example, sudden increases in pulp prices or disruptions in recycled fiber supply can raise manufacturing costs for paperboard packaging. A 10-15% increase in key raw material prices can reduce converter margins by several percentage points, particularly in highly competitive market segments. Manufacturers often attempt to offset these costs through price adjustments, but intense competition may limit their ability to fully pass cost increases to customers. Consequently, raw material price volatility remains a critical risk factor for packaging producers.

High Capital Investment Requirements

Advanced printing technologies and automated packaging production systems require substantial capital investment. High-resolution digital presses, hybrid printing lines, and precision finishing equipment represent high upfront costs for converters. Smaller regional packaging companies may struggle to finance these investments, particularly in markets where price competition is intense. Digital printing equipment requires high utilization rates to achieve profitability, often exceeding 60-70% operational capacity. Companies unable to achieve such volumes may face longer payback periods, which can delay technology adoption and widen the competitive gap between global packaging corporations and smaller converters.

Opportunity Analysis - Premium Packaging and Brand Differentiation

Brand owners increasingly recognize packaging as a strategic marketing tool rather than simply a protective container. High-quality printed rigid packaging enhances product visibility and reinforces brand identity, particularly in premium product categories such as cosmetics, electronics, and specialty foods. Digital printing technologies allow companies to create limited-edition packaging designs, personalized branding campaigns, and region-specific product packaging. These capabilities enable brands to strengthen customer engagement and improve shelf visibility. As a result, converters that provide integrated design, printing, and finishing services can capture higher-value contracts and establish long-term partnerships with consumer goods manufacturers.

Circular Packaging Solutions and Sustainable Materials

Sustainability initiatives across the packaging industry are creating new opportunities for innovation in rigid packaging materials. Companies are developing recyclable mono-material packaging formats, biodegradable coatings, and plant-based fiber substrates to reduce environmental impact. Packaging solutions made from agricultural residues, recycled fibers, and bio-based polymers are gaining attention as brands attempt to meet corporate sustainability targets. Manufacturers that successfully commercialize circular packaging solutions can secure long-term supply agreements with major consumer goods companies seeking to reduce their environmental footprint.

Category-wise Analysis

Material Insights

Paper and paperboard represent the largest material segment in the market and are anticipated to hold approximately 38.3% of the market share during the forecast period. Their dominance stems from strong recyclability credentials, cost efficiency, and excellent compatibility with multiple printing technologies. These materials are widely used in folding cartons, rigid boxes, and specialty packaging applications, particularly for food and beverage products where regulatory compliance and brand visibility are critical. Paperboard substrates provide a smooth printing surface that supports high-resolution graphics, vibrant colors, and complex branding elements. This makes them highly suitable for consumer packaged goods that rely heavily on shelf appeal.

The widespread availability of recycled fiber and well-established recycling infrastructure across North America and Europe further strengthens the adoption of paper-based packaging solutions. For example, major global beverage brands have increasingly adopted paperboard multipack cartons for bottled beverages, while confectionery manufacturers commonly use printed folding cartons for premium chocolate packaging. Many consumer goods companies are also transitioning toward fiber-based packaging alternatives to reduce plastic usage, reinforcing the leadership position of paper and paperboard materials in the printed rigid packaging market.

Bioplastics and plant-derived fiber materials represent the fastest-growing material category. These materials are gaining popularity as companies seek renewable and environmentally responsible alternatives to petroleum-based plastics while maintaining packaging durability and visual appeal. Plant-based packaging solutions derived from sources such as bagasse, bamboo fiber, wheat straw, and other agricultural residues offer promising sustainability benefits. These materials can be molded into rigid packaging formats while maintaining compatibility with modern printing technologies.

Advances in biodegradable coatings and compostable packaging structures allow manufacturers to preserve print clarity and color quality without compromising environmental performance. For instance, several personal care brands have introduced plant-fiber molded containers and rigid cosmetic boxes with biodegradable coatings, while organic food producers increasingly use bagasse-based rigid trays and cartons for sustainable product packaging. Growth in this segment is particularly strong in premium personal care, organic food products, and eco-focused consumer brands that emphasize sustainable packaging as a core element of their brand identity.

Packaging Format Analysis

Folding cartons dominate the market and are anticipated to account for approximately 35.6% of the market share during the forecast period. Their leadership position is supported by a combination of versatility, cost efficiency, and excellent printability. Folding cartons are widely used for packaging food products, pharmaceuticals, cosmetics, and consumer goods because they provide both product protection and effective brand communication. These cartons offer extensive surface area for product branding, ingredient information, regulatory labeling, and promotional messaging. They are also highly efficient in terms of logistics since they can be shipped flat to packaging facilities and assembled during the product filling process. This feature significantly reduces transportation and storage costs for manufacturers.

For example, breakfast cereal packaging, frozen food cartons, pharmaceutical medicine boxes, and cosmetic skincare packaging commonly rely on folding carton formats. Retail-ready packaging solutions and shelf-display cartons used by snack food manufacturers further highlight the widespread use of folding cartons. Their adaptability to both high-volume flexographic printing and premium offset printing techniques continues to reinforce their leading position in the printed rigid packaging market.

Rigid boxes represent the fastest-growing packaging format in the printed rigid packaging market. These packaging formats are typically associated with premium and luxury product segments where presentation and brand experience play a significant role in consumer purchasing decisions. Rigid boxes provide superior structural strength and are capable of supporting sophisticated finishing techniques such as embossing, foil stamping, magnetic closures, soft-touch coatings, and custom inserts.

These features make them particularly suitable for high-value products, including luxury cosmetics, smartphones, designer fashion accessories, and premium jewelry packaging. For instance, leading consumer electronics brands commonly use rigid boxes with multi-layer inserts to package smartphones and wearable devices, while luxury perfume manufacturers rely on high-end rigid packaging to enhance brand perception. The rising demand for premium packaging experiences, combined with the growth of luxury retail and e-commerce gift packaging, is expected to drive continued expansion in the rigid box segment.

Regional Insights

North America Printed Rigid Packaging Market Trends - Sustainability Initiatives, Digital Printing Adoption, and E-Commerce Driven Demand

North America represents a mature yet technologically advanced market for printed rigid packaging, supported by strong consumer packaged goods (CPG) industries, sophisticated retail channels, and a well-developed logistics infrastructure. The U.S. leads regional demand due to its large food, beverage, pharmaceutical, and personal care sectors. Packaging converters across the region continue to adopt advanced printing technologies, automated converting lines, and digital printing solutions to enhance production efficiency and improve packaging customization capabilities.

The presence of large packaging manufacturers and integrated supply chains further strengthens North America’s role as a major innovation hub in packaging technologies. Growth in North America is driven by increasing demand for sustainable packaging solutions, rapid expansion of e-commerce, and rising investments in digital printing capabilities. Regulatory frameworks emphasizing food safety and environmental sustainability are encouraging the adoption of recyclable and fiber-based packaging materials. For instance, several major consumer brands have committed to reducing plastic packaging and increasing the use of recyclable paperboard. Companies such as PepsiCo and Coca-Cola have expanded the use of paperboard multipack cartons for beverage packaging in North America as part of broader sustainability goals.

Packaging manufacturers such as Graphic Packaging Holding Company have invested in new paperboard converting and printing facilities to support growing demand for recyclable carton packaging. Amazon’s ongoing packaging optimization programs, including the use of recyclable paper-based packaging and improved shipping cartons, have increased demand for durable printed rigid packaging solutions capable of withstanding complex distribution networks.

Middle East and Africa Printed Rigid Packaging Market Trends - Urbanization, Retail Expansion, and Local Manufacturing Investments

The Middle East & Africa represent the fastest-growing regional market for printed rigid packaging. Rapid urbanization, expanding retail infrastructure, and increasing disposable incomes are supporting growth in packaged consumer goods markets across the region. Modern retail formats such as supermarkets, hypermarkets, and convenience stores are expanding rapidly, particularly in Gulf Cooperation Council (GCC) countries. As consumer demand for packaged food and branded personal care products rises, manufacturers are increasingly investing in rigid packaging solutions that enhance product protection and shelf visibility.

Countries such as the UAE, Saudi Arabia, Egypt, and South Africa are witnessing growing demand for packaged food, beverages, and cosmetics. Government initiatives aimed at strengthening local manufacturing capabilities are also encouraging investment in packaging production facilities. For example, several multinational packaging companies have expanded operations in the Gulf region to serve the growing FMCG market.

Beverage companies such as Nestlé and PepsiCo have increased regional production capacity, which in turn supports demand for printed cartons, trays, and rigid boxes used in retail distribution. Saudi Arabia’s industrial development initiatives under Vision 2030 are also encouraging local manufacturing of packaging materials and improving supply chain infrastructure. These developments are contributing to the growth of regional packaging converters and creating new opportunities for printed rigid packaging providers.

Asia Pacific Printed Rigid Packaging Market Trends - Manufacturing Strength, Expanding Consumer Markets, and E-Commerce Growth

Asia Pacific is projected to dominate the market, accounting for 47.2% of the market share in 2026. The region benefits from strong manufacturing capabilities, large consumer markets, and competitive production costs. Rapid economic development and expanding middle-class populations have significantly increased demand for packaged consumer goods, particularly in food, beverages, electronics, and personal care products. As a result, many global packaging companies have established production facilities across the region to support both domestic consumption and export-oriented manufacturing.

China remains the largest contributor due to its extensive manufacturing base and growing domestic consumer market. Major consumer electronics companies, including Apple and Xiaomi, rely heavily on high-quality printed rigid boxes produced by Chinese packaging manufacturers for smartphone and accessory packaging. Japan, meanwhile, leads in high-precision packaging technologies and premium packaging design, with cosmetic brands such as Shiseido utilizing sophisticated printed rigid packaging to reinforce luxury brand positioning. India and Southeast Asian countries are experiencing rapid growth in packaged consumer goods demand due to urbanization, rising disposable incomes, and expanding organized retail sectors. Companies such as Unilever and Procter & Gamble continue to expand manufacturing and packaging operations in India and ASEAN markets, which increases demand for printed folding cartons and rigid packaging formats. The rapid expansion of e-commerce platforms such as Alibaba and Flipkart has accelerated demand for durable and visually appealing printed rigid packaging solutions capable of protecting products during shipping while maintaining brand presentation.

Competitive Landscape

The global printed rigid packaging market consists of a mix of global packaging corporations and numerous regional converters. While several multinational companies maintain significant market influence, the industry remains moderately fragmented due to the presence of many specialized packaging producers serving local markets. Large companies typically maintain competitive advantages through vertical integration, advanced printing technology, and global supply chain capabilities, while smaller firms focus on niche applications and regional customer relationships. Leading companies in the printed rigid packaging market focus on technological innovation, sustainable material development, strategic acquisitions, and global market expansion. Firms differentiate themselves through integrated packaging design services, advanced printing capabilities, and strong partnerships with consumer goods manufacturers.

Key Industry Developments:

- In April 2025, Mondi Group announced the completion of its acquisition of Schumacher Packaging’s Western Europe operations, significantly expanding its corrugated and solid board packaging network across Germany, the U.K., and the Benelux region.

- In April 2025, Amcor plc announced the successful completion of its all-stock combination with Berry Global, creating a larger global packaging company with expanded capabilities in consumer, healthcare, and rigid packaging solutions.

Companies Covered in Printed Rigid Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Westrock

- Graphic Packaging Holding Company

- International Paper Company

- Sonoco Products Company

- DS Smith plc

- Stora Enso Oyj

- WestRock Company

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

- Oji Holdings Corporation

- Rengo Co., Ltd.

- UFlex Limited

- Parksons Packaging Ltd.

- Sealed Air Corporation

Frequently Asked Questions

The global printed rigid packaging market is estimated to reach US$183.4 billion in 2026.

The printed rigid packaging market is projected to reach US$256.3 billion by 2033.

Key trends include growing adoption of recyclable paperboard packaging, increasing investments in digital printing technologies, expansion of e-commerce packaging solutions, and rising demand for premium packaging formats in cosmetics and electronics.

Paper and paperboard are the leading material segment, accounting for 38.3% of the market share, driven by strong recyclability and widespread use in folding cartons and rigid boxes.

The printed rigid packaging market is projected to grow at a CAGR of 4.9% between 2026 and 2033.

Major companies include Amcor plc, Mondi Group, Smurfit Westrock, Graphic Packaging Holding Company, and Sonoco Products Company.