- Inks, Coatings, Adhesives & Sealants (ICAS)

- Pressure Sensitive Adhesives Market

Pressure Sensitive Adhesives Market Size, Share, and Growth Forecast 2026 - 2033

Pressure Sensitive Adhesives Market by Chemistry (Acrylic, Rubber, Silicone, Others), Product Type (Tapes, Labels, Graphic Films, Others), Adhesion Type (Permanent PSA, Removable PSA, Repositionable PSA), End-user (Automotive, Electrical & Electronics, Healthcare & Medical, Packaging, Building & Construction, Retail & E-commerce), and Regional Analysis, 2026 - 2033

Pressure Sensitive Adhesives Market Size and Trend Analysis

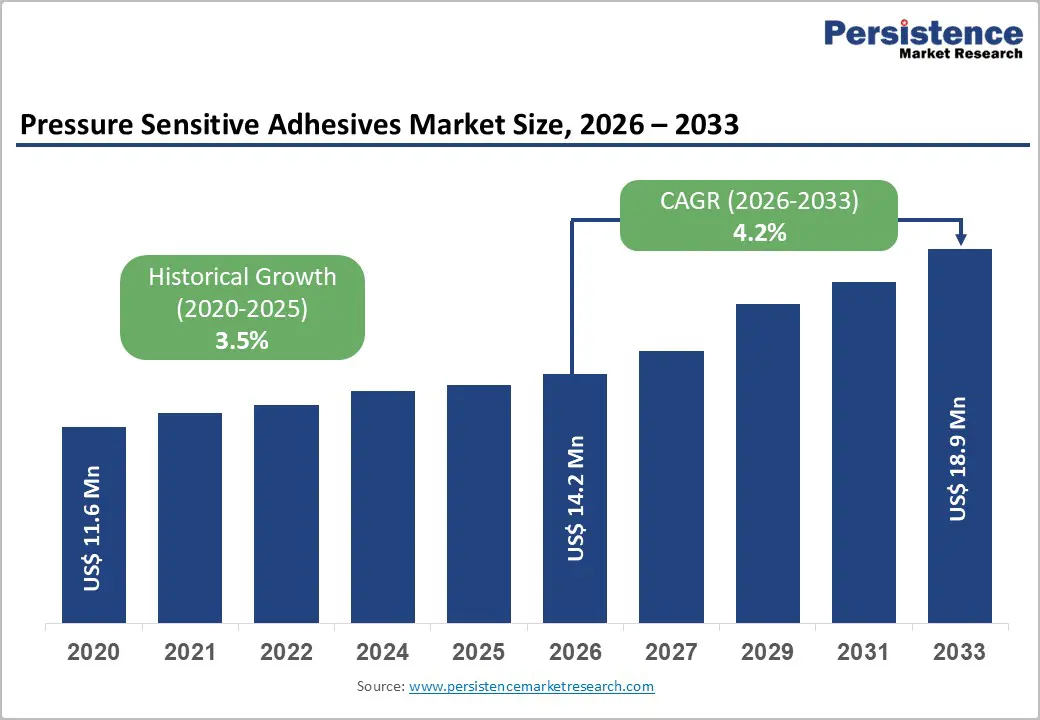

The global pressure sensitive adhesives market size is expected to be valued at US$ 14.2 billion in 2026 and projected to reach US$ 18.9 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

The pressure sensitive adhesives (PSA) market is set for consistent and broad-based expansion, driven by accelerating demand across e-commerce-led packaging, automotive lightweighting initiatives, medical device assembly, and electronics miniaturization, all of which increasingly rely on PSA solutions as mechanically and chemically superior alternatives to fasteners, rivets, and solvent-based adhesives. The market’s growth is further reinforced by sustainability-driven reformulation trends, particularly the shift from solvent-borne to water-based and UV-curable acrylic PSA systems in compliance with the U.S. EPA’s National Volatile Organic Compound Emission Standards and the European Union’s REACH regulation, as well as the exponential growth in self-adhesive label demand from the global retail, food & beverage, and pharmaceutical end-use sectors generating cumulative volume uplift throughout the forecast period.

Key Industry Highlights:

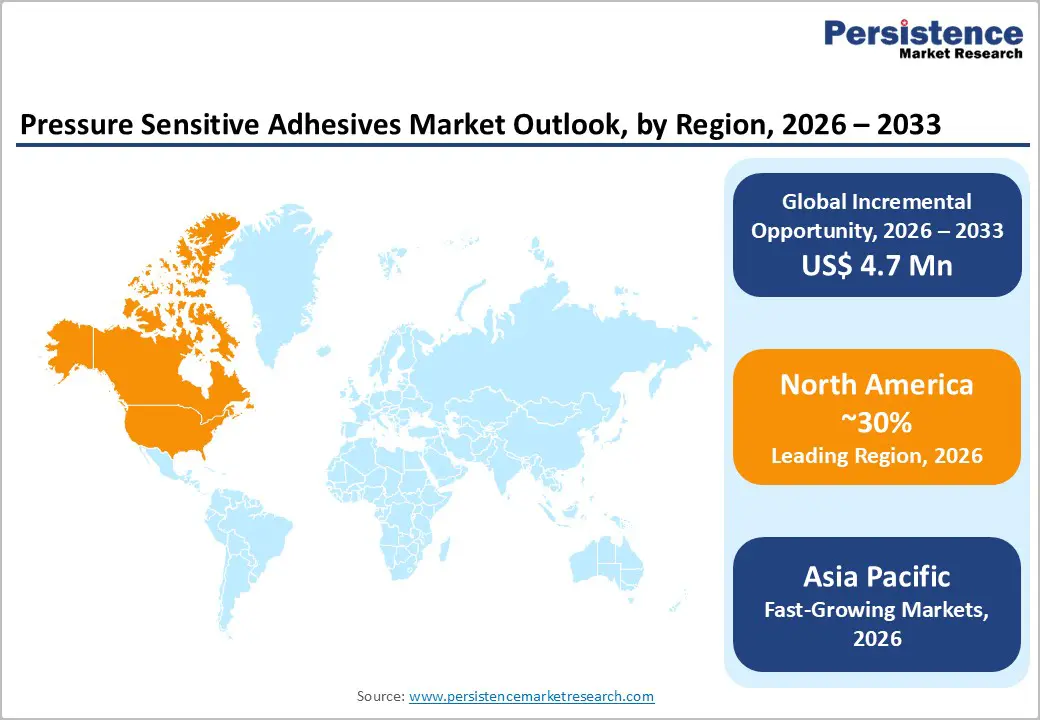

- Leading Region: North America leads the global Pressure Sensitive Adhesives market with approximately 30% revenue share in 2025, anchored by the U.S.’s dominant e-commerce packaging, medical device, and automotive manufacturing sectors, alongside the PSTC and EPA VOC regulatory framework driving sustained innovation investment in waterborne and UV-curable PSA chemistry.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market, projected to expand at approximately 5.5% CAGR through 2033, propelled by China’s 9.4 million-unit NEV production, Japan’s precision electronics PSA demand, India’s e-commerce packaging boom, and electronics manufacturing relocation driving PSA consumption across Vietnam, Thailand, and Indonesia.

- Dominant Segment: Acrylic-based PSAs dominate the chemistry segment with approximately 50% market share in 2025, preferred across packaging, automotive, graphic film, and healthcare applications for their UV stability, versatile performance tuning, waterborne formulation compatibility, and alignment with REACH and EPA VOC regulatory compliance requirements.

- Fastest Growing Segment: UV-curable and waterborne PSA chemistries represent the fastest-growing technology segments, driven by the EU Chemicals Strategy for Sustainability, EPA VOC standards, and converter investment in sustainable coating lines, with European new PSA product launches already exceeding 55% in low-VOC formats, according to European Coatings Journal data.

- Key Opportunity: The medical-grade PSA segment offers the highest-value growth opportunity, driven by FDA-cleared wearable CGMs, cardiac patches, and the proliferation of transdermal drug delivery devices, targeting a global population of over 1.4 billion people aged 60+ by 2030 per WHO projections, and commanding significant price premiums over industrial PSA grades.

| Key Insights | Details |

|---|---|

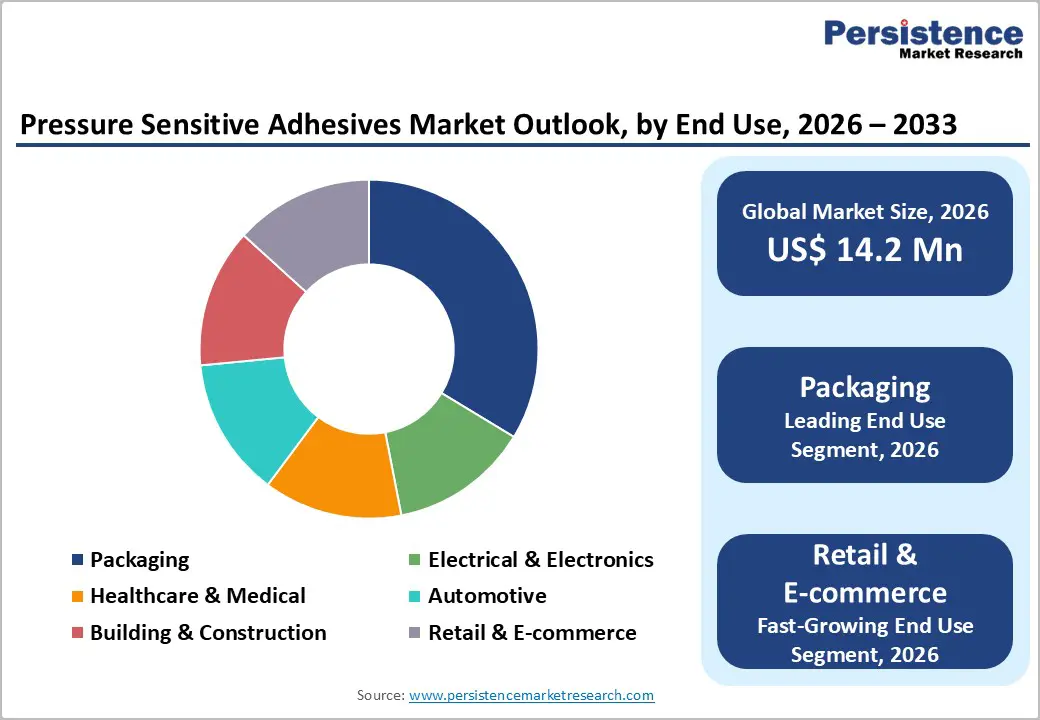

| Pressure Sensitive Adhesives Market Size (2026E) | US$ 14.2 Billion |

| Market Value Forecast (2033F) | US$ 18.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.2% |

| Historical Market Growth (2020 - 2025) | 3.5% |

DRO Analysis

Drivers - E-commerce Boom and Flexible Packaging Demand Driving PSA Tape and Label Consumption

The explosive growth of global e-commerce is among the most powerful demand catalysts for PSA tapes and self-adhesive labels, generating structural and recurring volume requirements across packaging, logistics, and retail supply chains. According to UNCTAD (United Nations Conference on Trade and Development), global e-commerce sales surpassed US$ 5.8 trillion in 2023 and are forecast to continue expanding at high single-digit annual rates through the decade, each transaction requiring carton sealing tapes, tamper-evident labels, and shipping labels that depend on high-performance PSA formulations. The Flexible Packaging Association (FPA) reports that flexible packaging, a major PSA end-use substrate, is the fastest growing U.S. packaging format, with acrylic PSA laminates enabling resealable pouch functionality critical to consumer convenience. Brand owners’ increasing adoption of pressure sensitive labels as the preferred primary and secondary packaging labeling format, displacing glue-applied and sleeve labels for their design flexibility and decoration speed, further concentrates volume growth in PSA label substrates globally, reinforcing the packaging end-use segment’s structural demand leadership.

Automotive Lightweighting and Electric Vehicle Assembly Fueling High-Performance PSA Adoption

The global automotive industry’s accelerating transition toward lightweight body structures and battery electric vehicle (BEV) platforms is creating substantial incremental demand for high-performance structural and bonding PSA tapes. The European Automobile Manufacturers’ Association (ACEA) reported that BEV registrations in Europe reached 1.5 million units in 2023, with each electric vehicle incorporating significantly greater quantities of adhesive tape than conventional internal combustion engine vehicles, for battery cell assembly, thermal management pad bonding, exterior body panel attachment, and interior trim fixing. According to the Society of Automotive Engineers (SAE), adhesive bonding displaces approximately 1.5 kg of fasteners per vehicle on average, delivering weight savings critical to BEV range optimization. 3M’s VHB® (Very High Bond) tape family and Henkel’s TEROSON® structural bonding tapes are widely specified across premium automotive OEM programs, demonstrating PSA’s technical readiness to serve the highest-demand automotive structural bonding applications.

Restraints - Volatile Raw Material Costs and Dependency on Petrochemical Feedstocks

Pressure sensitive adhesive formulations, particularly acrylic and rubber-based systems, rely on petrochemical-derived monomers, tackifying resins, and plasticizers whose prices exhibit significant cyclicality tied to crude oil market dynamics. Acrylate monomer prices surged by over 50% in 2021 due to feedstock shortages and logistics disruptions, severely compressing manufacturer margins and limiting the ability of PSA producers to offer stable long-term pricing to downstream converters and end-users. The American Chemistry Council (ACC) has flagged recurring feedstock supply chain vulnerabilities in the specialty chemicals sector, impacting PSA producers’ ability to maintain cost competitiveness while simultaneously investing in sustainable chemistry reformulation programs required by evolving environmental regulations.

Regulatory Pressure on Solvent-Borne PSA Systems and VOC Emissions Compliance Costs

Stringent and increasingly harmonized global regulations on volatile organic compound (VOC) emissions from solvent-borne adhesive manufacturing and coating operations impose substantial compliance investment burdens on PSA producers. The U.S. EPA’s 40 CFR Part 63 NESHAP standards for adhesive and sealant manufacturing facilities and the EU’s Industrial Emissions Directive (IED 2010/75/EU) set progressively tighter VOC emission limits, requiring significant capital investment in thermal oxidizers, solvent recovery systems, or transitions to waterborne and UV-curable PSA chemistries. These compliance costs are particularly burdensome for small and medium-sized PSA manufacturers operating legacy solvent-coating lines, creating consolidation pressure within the industry and reducing the competitive flexibility of incumbents during technology transition periods.

Opportunities - Healthcare and Medical Device Sector: A High-Value Growth Frontier for Specialty PSAs

The healthcare and medical device sector represents one of the highest-value and fastest-growing application frontiers for specialty pressure sensitive adhesives, driven by the global expansion of wearable medical devices, wound care product innovation, and transdermal drug delivery systems. The U.S. Food and Drug Administration (FDA) reports a significant increase in clearances for wearable continuous glucose monitors (CGMs), cardiac monitoring patches, and wearable drug delivery devices, each requiring skin-compatible, hypoallergenic PSA systems that must meet ISO 10993 biocompatibility standards. Avery Dennison’s medical PSA platform and Scapa Group’s healthcare tape solutions exemplify the commercial attractiveness of this segment, where PSA performance requirements, encompassing moisture vapor transmission rate, skin adhesion consistency, and residue-free removal, command significant price premiums over industrial-grade PSA products. The World Health Organization (WHO)’s projections of an aging global population exceeding 1.4 billion people aged 60 and above by 2030 will structurally expand demand for chronic disease management wearables and wound care products, creating a durable, multi-decade demand runway for medical-grade PSA solutions.

UV-Curable and Waterborne PSA Innovation Capitalizing on Sustainability Mandates

The transition from solvent-borne to waterborne and UV-curable PSA chemistries, driven by tightening VOC regulations and brand owner sustainability commitments, represents a significant opportunity for PSA manufacturers with advanced formulation capabilities to differentiate their portfolios and capture premium margins. Arkema’s Sartomer UV-curable resin platform and Ashland’s waterborne acrylic PSA emulsions have been recognized as technically leading products in sustainability-driven reformulation programs by leading tape and label converters globally. The European Coatings Journal reports that waterborne and UV-curable adhesive technologies collectively accounted for over 55% of new adhesive product launches in Europe in 2022, confirming the industry’s accelerating transition trajectory. Waterborne PSAs deliver comparable performance to solvent-borne systems in most packaging and label applications while eliminating costly solvent recovery infrastructure, creating a compelling total cost of ownership argument that accelerates converter adoption. The EU’s Green Deal and Chemicals Strategy for Sustainability (CSS) further reinforce regulatory tailwinds supporting low-VOC PSA technology investment through the forecast period.

Category-wise Analysis

Chemistry Insights

Acrylic-based pressure sensitive adhesives dominate the chemistry segment with approximately 50% of total market revenue in 2025, reflecting their unmatched combination of performance versatility, environmental resistance, UV stability, and compatibility with waterborne and UV-curable formulation platforms. Acrylic PSAs, available in both solvent-borne and waterborne emulsion forms, can be precisely tailored through monomer selection and crosslinker systems to deliver application-specific peel strength, tack, and cohesive strength profiles across virtually the full range of PSA end-use applications. Their superior UV and oxidative resistance compared to rubber-based systems makes acrylic PSAs the specification of choice for outdoor graphic films, automotive exterior tapes, and long-lifecycle label applications. Leading producers including Arkema, Ashland, and H.B. Fuller Company continue to invest in expanding their acrylic PSA emulsion portfolios to meet converter demands for low-VOC, high-performance waterborne systems compliant with evolving REACH and EPA VOC regulatory frameworks.

Product Type Insights

Tapes represent the leading product type segment in the PSA market, capturing approximately 45% of total market revenue in 2025. PSA tapes, encompassing packaging tapes, masking tapes, double-coated tapes, structural bonding tapes, and specialty functional tapes, address the broadest range of end-use applications of any PSA product format, spanning industrial assembly, automotive manufacturing, construction, healthcare, and consumer applications. The Pressure Sensitive Tape Council (PSTC), the North American industry association for PSA tape manufacturers, reports sustained volume growth across virtually all tape sub-categories, with double-coated and foam-core structural bonding tapes demonstrating above-average growth driven by automotive assembly and electronics manufacturing demand. 3M’s industry-leading tape portfolio, comprising over 1,000 individual tape products, and Nitto Denko Corporation’s precision functional tape range exemplify the technical breadth of the PSA tape segment and its capacity to address highly specialized industrial bonding, sealing, and insulating requirements across diverse end-use industries.

Adhesion Type Insights

Permanent PSA is the dominant adhesion type segment, accounting for approximately 62% of total market revenue in 2025. Permanent PSAs, engineered to form irreversible bonds to a wide variety of substrate materials upon initial contact, address the largest volume applications across packaging sealing, industrial bonding, automotive assembly, and healthcare product manufacturing, where bond integrity throughout the product’s service life is the primary performance specification. The packaging segment, itself the largest end-use for PSA products globally, relies almost exclusively on permanent PSA formulations for carton sealing tapes and primary self-adhesive labels where label removal or repositioning is not an intended feature. The FINAT (International Federation of Self-Adhesive Label Manufacturers), representing the global self-adhesive label industry, reported global self-adhesive label volume exceeding 68 billion square meters in 2022, the overwhelming majority of which utilizes permanent PSA, confirming the segment’s structural volume dominance and its tight linkage to packaging and consumer goods label end-use growth drivers.

End-user Insights

The packaging end-use segment leads the PSA market with approximately 35% of total market revenue in 2025, driven by the unparalleled breadth and volume of PSA tape and label applications across consumer goods, food & beverage, e-commerce, pharmaceutical, and industrial packaging supply chains globally. Self-adhesive labels, the primary packaging labeling format for food, beverage, personal care, and pharmaceutical products, represent one of the largest single volume consumers of PSA formulations worldwide. The FINAT’s annual market data confirm self-adhesive label volumes growing consistently at 4-6% annually across global markets, propelled by product proliferation, SKU complexity, and the shift from wet-glue to PSA labeling in food and beverage filling lines. E-commerce growth generates additional carton sealing tape and shipping label demand, creating a dual growth vector for PSA packaging applications spanning both physical retail and online distribution channels simultaneously.

Regional Insights

North America Pressure Sensitive Adhesives Market Trends and Insights

North America is the leading regional market for pressure sensitive adhesives, commanding approximately 30% of global revenue in 2025, with the United States representing the dominant national market driven by its world-class e-commerce infrastructure, automotive manufacturing sector, advanced medical device industry, and sophisticated packaging converting industry. The U.S. EPA’s National Volatile Organic Compound Emission Standards for adhesive and sealant products continue to drive converter investment in waterborne and UV-curable PSA coating lines, benefiting formulation leaders including Henkel Corporation, H.B. Fuller Company, and Ashland who have prioritized low-VOC product development. The Pressure Sensitive Tape Council (PSTC) actively promotes technical standards and testing methodologies that underpin product specification quality across North American converting and end-use industries.

Canada’s growing e-commerce and food packaging sectors contribute additional PSA demand, while Mexico’s expanding automotive assembly base, particularly in the Bajío and Monterrey manufacturing corridors, is generating rising demand for automotive-grade PSA tapes and films as international OEMs expand capacity under the reshoring and nearshoring supply chain diversification trend post-COVID-19. The U.S. medical device industry, accounting for approximately 40% of global medical device output per AdvaMed, represents the world’s largest single demand center for medical-grade PSA in wearable device, wound care, and transdermal drug delivery applications, further reinforcing North America’s leadership position across the highest-value PSA end-use segments.

Europe Pressure Sensitive Adhesives Market Trends and Insights

Europe is a major and technically mature PSA market, holding approximately 25% of global revenue share in 2025, characterized by strong regulatory-driven innovation, premium automotive manufacturing demand, and sophisticated self-adhesive label converting industry infrastructure. Germany, Europe’s largest industrial economy, anchors regional PSA demand through its world-class automotive OEM and Tier-1 supplier base (Volkswagen Group, BMW, Mercedes-Benz, Bosch, Continental) requiring structural bonding tapes, noise-dampening PSA foams, and exterior protection films for premium vehicle assembly. The EU’s REACH regulation and the Chemicals Strategy for Sustainability (CSS) are compelling European PSA manufacturers to systematically phase out substances of very high concern (SVHC) from formulations and transition to bio-based and waterborne chemistries, driving significant R&D investment at companies including Bostik, Arkema, and Jowat SE.

France and the UK contribute significant PSA demand through their respective healthcare, cosmetics packaging, and food & beverage sectors, where premium self-adhesive label applications and specialty medical device tape requirements generate above-average revenue per unit. Spain’s expanding food & beverage export sector and Italy’s luxury goods and fashion packaging industry are growing secondary demand centers for decorative and specialty PSA label formats. The FINAT, headquartered in The Hague, Netherlands, serves as the European hub for self-adhesive label industry standards, market data, and sustainability benchmarking, with its members driving adoption of linerless label technologies and PSA liner recycling programs that are reshaping European PSA label material specifications and reducing total system waste.

Asia Pacific Pressure Sensitive Adhesives Market Trends and Insights

Asia Pacific is the fastest growing regional market for pressure sensitive adhesives, projected to expand at a CAGR of approximately 5.5% through 2033, driven by the region’s unparalleled manufacturing scale, rapidly expanding consumer markets, and accelerating electronics and automotive sector growth across China, Japan, South Korea, India, and ASEAN. China is both the largest PSA producer and consumer in Asia Pacific, hosting a deep and vertically integrated adhesive tape manufacturing ecosystem in provinces including Guangdong, Zhejiang, and Jiangsu, collectively accounting for the majority of global PSA tape production capacity. China’s New Energy Vehicle (NEV) market, which produced over 9.4 million electric vehicles in 2023 per the China Association of Automobile Manufacturers (CAAM), is a major and rapidly expanding end-market for automotive-grade PSA structural tapes, battery insulation films, and thermal management adhesives.

Japan’s precision electronics industry, anchored by companies including Sony, Panasonic, TDK, and Murata Manufacturing, demands ultra-thin, high-precision PSA optical films and electronic component tapes, a segment dominated by domestic producer Nitto Denko Corporation and Lintec Corporation. India’s PSA market is growing rapidly, supported by expanding domestic e-commerce (Flipkart, Amazon India), pharmaceutical packaging sector growth, and the government’s Production-Linked Incentive (PLI) scheme for advanced chemistry cell battery manufacturing, generating downstream demand for battery assembly PSA tapes. ASEAN markets, particularly Vietnam, Thailand, and Indonesia, are emerging as high-growth PSA demand centers driven by electronics manufacturing relocation from China and rapidly growing modern retail and FMCG packaging sectors.

Competitive Landscape

The global pressure sensitive adhesives market exhibits a moderately consolidated structure at the top tier, with large multinational specialty chemical companies holding significant shares across diverse product categories and regions. However, the broader market remains fragmented, with numerous regional manufacturers catering to localized demand, particularly in packaging, labeling, and industrial applications.

Competition is driven by formulation expertise, product portfolio breadth across multiple chemistries and substrates, and the ability to offer consistent performance across varied end uses. Leading players focus on expanding global manufacturing footprints and strengthening technical service capabilities to support converter customers. Strategic priorities include increased investment in sustainable technologies such as water-based and UV-curable adhesives, along with efforts to reduce VOC emissions. Additionally, companies are pursuing targeted acquisitions to enhance technology portfolios and adopting digital tools to streamline product selection and customization, enabling stronger customer engagement and long-term competitive positioning.

Key Developments

- November 2025: BioBond Adhesives launched its BioMelt™ plant-based hot melt pressure sensitive adhesives for labels and tapes, offering PFAS-free, microplastic-free formulations with competitive performance, with product samples made available for industry evaluation in Q4 2025.

- September 2025: Ahlstrom expanded its range of sustainable release and label papers for pressure-sensitive adhesive applications, introducing fiber-based materials with reduced environmental impact and circularity benefits, showcased at Labelexpo Europe 2025 to support eco-friendly labeling solutions.

- June 2024: Avery Dennison launched new pressure-sensitive adhesive tape solutions for EV battery cell wrapping, designed to improve electrical insulation, corrosion resistance, and durability while addressing arcing challenges and enhancing safety and performance in battery pack applications.

Companies Covered in Pressure Sensitive Adhesives Market

- Henkel Corporation

- Bostik (Total Energies Group)

- Momentive Performance Materials

- 3M

- Avery Dennison Corp.

- Cosmo Specialty Chemicals

- Illinois Tool Works

- Scapa Group

- Nitto Denko Corporation

- Ashland

- H.B. Fuller Company

- Arkema

- Jowat SE

- Wacker Chemie AG

- Sika AG

- Tesa SE (Beiersdorf Group)

- Lintec Corporation

- Intertape Polymer Group (IPG)

- Biobond Adhesives

Frequently Asked Questions

The pressure sensitive adhesives market is estimated to reach US$ 14.2 billion in 2026.

Demand is driven by e-commerce growth and increasing use in automotive and electronics.

North America leads the market with the highest revenue share.

Opportunities lie in medical applications and sustainable adhesive technologies.

Leading companies in the global Pressure Sensitive Adhesives market include 3M, Henkel Corporation, Avery Dennison Corp., H.B. Fuller Company, Nitto Denko Corporation, Bostik, Arkema, Ashland, Illinois Tool Works, etc.