- Automation & Robotics

- Precision Agriculture Drone Market

Precision Agriculture Drone Market Size, Share, and Growth Forecast 2026 - 2033

Precision Agriculture Drone Market by Product Type (Fixed Wing, Rotary Wing), by Component (Hardware: Frames, Flight Control Systems, Navigation Systems, Propulsion Systems, Cameras, Sensors; Software; Services: Professional Services, Managed Services), Farming Environment (Indoor Farming, Outdoor Farming), Application, and Regional Analysis for 2026 - 2033

Precision Agriculture Drone Market Size and Trend Analysis

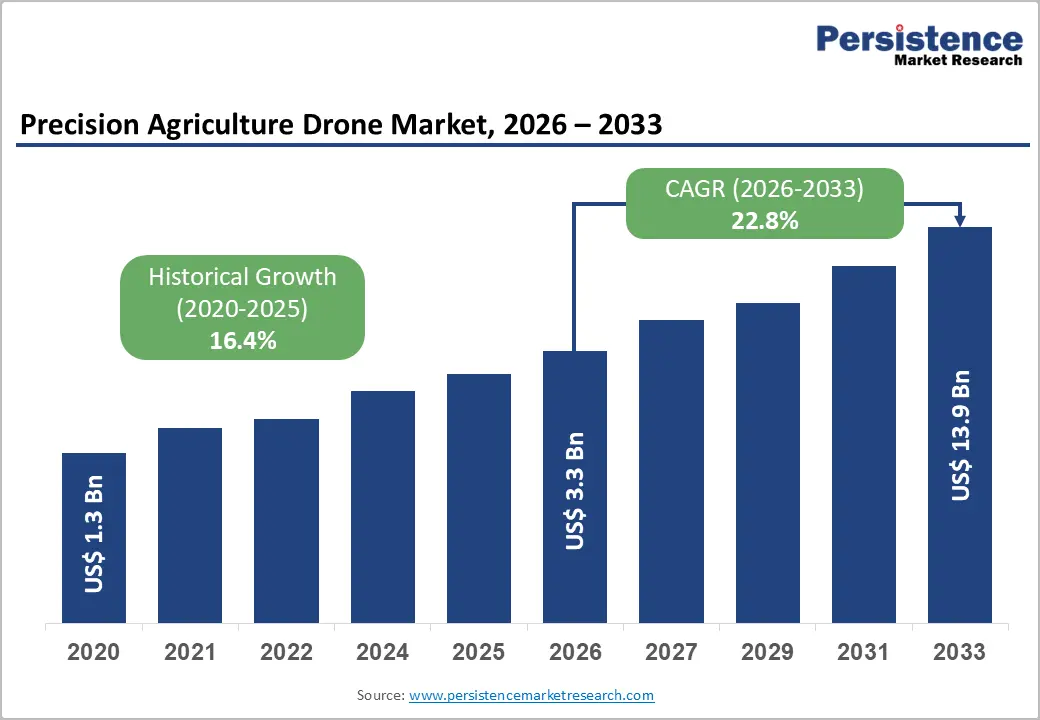

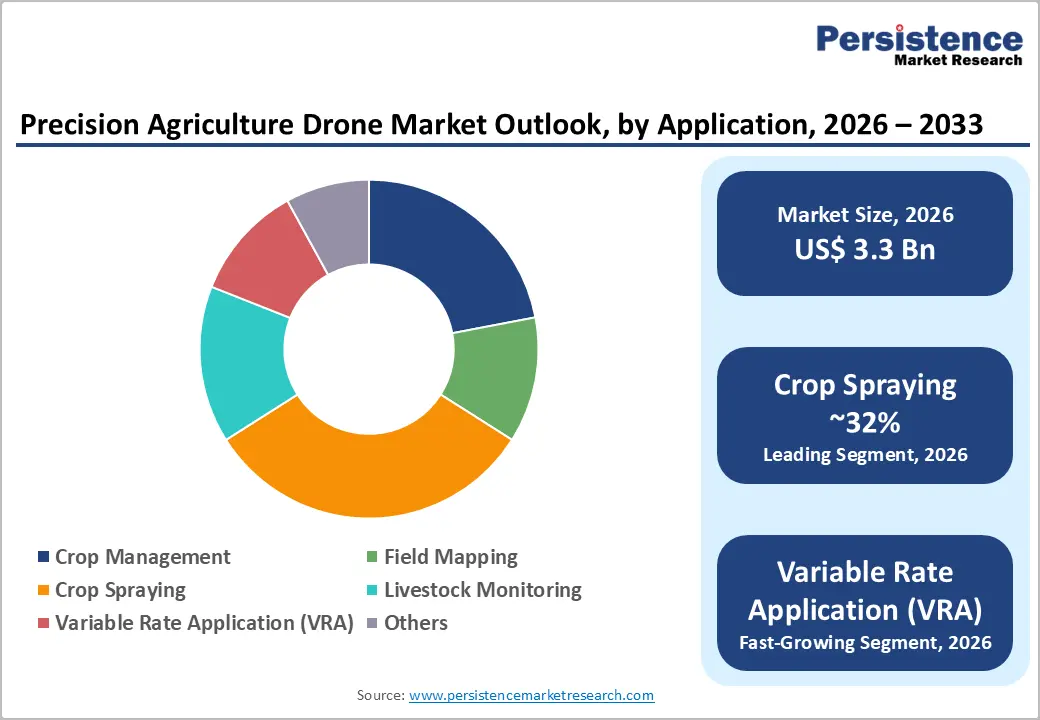

The global precision agriculture drone market size is supposed to be valued at US$ 3.3 billion in 2026 and is projected to reach US$ 13.9 billion by 2033, growing at a CAGR of 22.8% between 2026 and 2033.

The market growth emphasizes a broader agricultural technology ecosystem, driven by the global food security imperative, accelerating adoption of autonomous field operations, progressive regulatory liberalization of commercial UAV operations, and the measurable return-on-investment that drone-enabled precision spraying, field mapping, and crop monitoring deliver to large-scale commercial farming operations.

Key Market Highlights

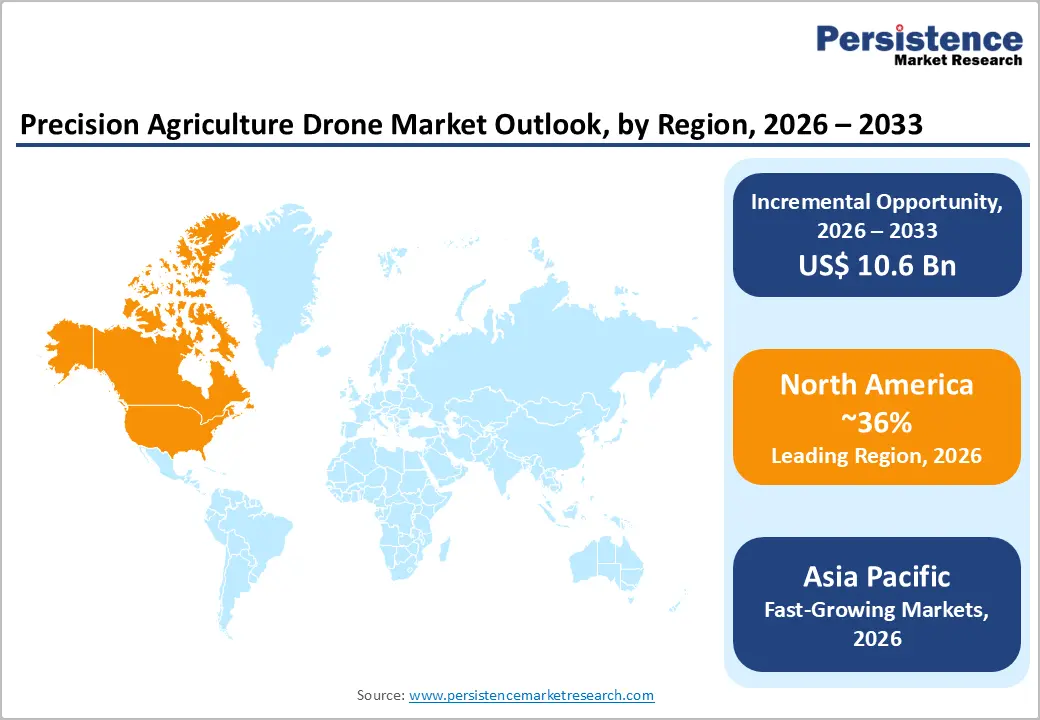

- Leading Region: North America leads the global Precision Agriculture Drone market in technology innovation and regulatory advancement, anchored by the FAA's Part 107 BVLOS authorization expansion, USDA ERS documented precision agriculture ROI evidence, AeroVironment, AgEagle, and Trimble's U.S.-headquartered commercial platforms, and the world's largest per-farm precision agriculture technology investment budgets sustaining above-average drone adoption across the U.S. Corn Belt and grain production regions.

- Growing Region: Asia Pacific is the fastest-growing regional market, driven by China's MARA documented 1.3 million registered agricultural drones, India's INR 120 crore Drone Shakti subsidy program, Japan's MAFF precision agriculture promotion policies, DJI and XAG Chinese manufacturing scale, and ASEAN government-backed smart farming initiatives collectively sustaining the world's highest precision agriculture drone deployment growth velocity.

- Dominant Product Type: Rotary Wing drones dominate the Product Type segment with approximately 72% revenue share, anchored by DJI Agras T40/T50 and XAG P100 Pro commercial deployment dominance, China's MARA confirming 1.3 million agricultural multirotor registrations, and rotary wing VTOL capability enabling both crop spraying and precision hovering inspection missions that fixed-wing platforms cannot perform.

- Dominant Application: Crop Spraying is the dominant Application segment with approximately 36% revenue share, confirmed by XAG operational data documenting 35% pesticide reduction and 92% water savings, China's 1.3 million spraying drone registrations, and India's DGCA liberalized agricultural drone spraying regulations creating the world's most rapidly scaling new commercial crop spraying drone deployment market by 2033.

- Key Market Opportunity: AI-integrated drone analytics SaaS platforms and high-capacity crop spraying drone adoption in India and Southeast Asia represent the key dual opportunities, with European Commission Farm to Fork 50% pesticide reduction mandate, DroneDeploy and Pix4D subscription analytics growth, India's 100,000 agricultural drone deployment government target, and BVLOS regulatory approvals enabling autonomous large-area precision agriculture drone operations at commercial scale.

| Key Insights | Details |

|---|---|

|

Precision Agriculture Drone Market Size (2026E) |

US$ 3.3 Billion |

|

Market Value Forecast (2033F) |

US$ 13.9 Billion |

|

Projected Growth CAGR (2026–2033) |

22.8% |

|

Historical Market Growth (2020–2025) |

16.4% |

DRO Analysis

Drivers - Global Food Security Mandate and FAO-Documented Agricultural Productivity Gap Driving Precision Drone Adoption at Scale

The Food and Agriculture Organization of the United Nations (FAO) has documented that global agricultural productivity must increase by at least 50% by 2050 to meet the nutritional demands of a projected world population of 9.7 billion people, while simultaneously confronting progressive reduction in available arable land, declining freshwater availability for irrigation, and the escalating yield impacts of climate-driven weather volatility across major crop production geographies. Precision agriculture drones directly address this productivity gap by enabling centimeter-accurate field mapping through multispectral and RGB sensors, real-time crop health monitoring via NDVI (Normalized Difference Vegetation Index) analysis, and targeted variable-rate pesticide and fertilizer application that the U.S. Department of Agriculture (USDA) documents can reduce chemical input usage by 15–25% while sustaining or improving yield outcomes.

The USDA's Economic Research Service (ERS) documents that U.S. farms using precision agriculture technology, including drone-based monitoring, achieve measurably higher input efficiency ratios than non-adopters, reinforcing the commercial return-on-investment case that is accelerating drone adoption across large-scale grain, soybean, and specialty crop operations in North America, Europe, and Asia Pacific.

Progressive Regulatory Liberalization of Commercial Agricultural UAV Operations Enabling Large-Scale Field Deployment

The regulatory environment for commercial precision agriculture drone operations is undergoing a structural global liberalization, with the U.S. Federal Aviation Administration (FAA) progressively expanding commercial UAS operational authorizations under Part 107 regulations to include beyond visual line-of-sight (BVLOS) operations that are essential for large-scale autonomous field monitoring and spraying missions. The European Union Aviation Safety Agency (EASA)'s implementation of the U-space drone traffic management framework across EU member states, and India's Directorate General of Civil Aviation (DGCA)'s Drone Rules 2021 that created a liberalized "Green Zone" agricultural drone operation framework, collectively represent regulatory milestones that are directly expanding the addressable commercial agricultural drone operation deployment market across the world's three most agriculturally significant geographies.

Japan's Ministry of Agriculture, Forestry and Fisheries (MAFF) has actively promoted agricultural drone adoption through subsidy programs, with the Japanese agricultural drone market among the most mature globally, sustaining above-average commercial deployment density per cultivated hectare documented by MAFF's annual precision agriculture technology adoption survey data.

Restraints - High Capital Cost of Precision Agricultural Drone Systems and Accessories Constraining Small Farm Adoption

Commercial-grade precision agriculture multirotor and fixed-wing drone systems, encompassing the hardware platform, multispectral sensor payloads, RTK GPS positioning modules, and ground station software, represent capital investments of US$ 5,000–50,000+ per system that create significant procurement barriers for small and subsistence-scale farm operators who represent the majority of agricultural land managers in developing economies across South Asia, Sub-Saharan Africa, and Southeast Asia.

The FAO's documented average farm size data confirms that the majority of global farms are under 2 hectares in these regions, a scale at which the per-hectare capital cost of precision drone systems cannot be economically justified without access to government subsidy programs, agricultural drone-as-a-service models, or cooperative equipment sharing arrangements that mitigate individual farm procurement cost exposure.

Airspace Regulatory Complexity, Operator Certification Requirements, and Data Privacy Concerns Slowing Commercial Deployment

Despite progressive regulatory liberalization, commercial precision agriculture drone operators continue to face complex and jurisdiction-specific airspace authorization requirements, with BVLOS operational permits requiring multi-agency approvals in most countries that add deployment timeline costs and administrative burdens deterring adoption by farm operators without dedicated UAV operations management resources.

The FAA's documented UAS registration database contains over 855,000 registered commercial and recreational drones in the U.S., but certified commercial agricultural drone operators represent a small fraction of this total, reflecting the specialist certification and ongoing flight review requirements that constrain rapid operator ecosystem expansion. Data ownership and crop yield information privacy concerns among commercial farmers regarding third-party drone service providers' data management practices represent additional adoption friction documented in USDA agricultural technology adoption surveys.

Opportunities - Crop Spraying Drone Adoption Creating a Transformational Chemical Application Efficiency Opportunity Across Asia Pacific and Latin America

The commercial adoption of high-capacity agricultural spraying drones, led by XAG Co., Ltd.'s P series and R series agricultural drone platforms capable of carrying 16–40 kg payload spray tanks and covering 10–20 hectares per hour, represents the most commercially immediate and high-value precision agriculture drone growth opportunity, as crop spraying drones deliver documented 30–40% pesticide savings, 90% water usage reduction versus conventional knapsack sprayers, and the elimination of human operator chemical exposure risks that create compelling economic and safety justification for replacement of conventional ground-based spraying machinery.

China's Ministry of Agriculture and Rural Affairs (MARA) documents that over 1.3 million agricultural drones were registered for crop protection operations in China by 2023, confirming Asia Pacific's position as the world's most commercially advanced agricultural drone spraying deployment market. India's DGCA Drone Rules 2021 and the Indian government's allocation of INR 120 crore for the Drone Shakti scheme supporting agricultural drone startups confirm the institutional policy commitment driving India's emerging agricultural drone spraying market toward rapid commercial scale adoption, creating an above-CAGR growth opportunity for drone spraying platform manufacturers including XAG, DJI Agras, and Airbots Aerospace Pvt. Ltd. (headquartered in Pune, Maharashtra, India) targeting the Indian and South Asian market.

AI-Integrated Multispectral Drone Data Analytics Platforms Creating SaaS Revenue Model Opportunity Beyond Hardware Sales

The global precision agriculture drone market is undergoing a structural business model evolution, transitioning from hardware-centric single drone system sales toward integrated subscription-based software-as-a-service (SaaS) analytics platforms that generate recurring revenue streams from drone-collected multispectral, thermal, and RGB imagery processed through AI-powered crop health diagnostic algorithms. PrecisionHawk, DroneDeploy, and Pix4D SA are the three most commercially prominent global agricultural drone data analytics software platform providers, whose cloud-based field mapping, crop health monitoring, and agronomic recommendation engine platforms convert raw drone imagery into actionable variable-rate application prescriptions that agronomists and farm managers access through annual software subscription models generating predictable recurring revenues independent of drone hardware sales cycles.

The U.S. Department of Agriculture's documented precision agriculture technology investment growth, and the European Commission's Farm to Fork Strategy under the European Green Deal mandating a 50% reduction in pesticide use and 20% reduction in fertilizer use by 2030 across EU agricultural operations, are institutional policy catalysts that directly mandate the AI-driven precision spraying prescription and crop monitoring capabilities that drone analytics software platforms deliver.

Category-wise Analysis

By Product Type Insights

Rotary Wing drones lead the global Precision Agriculture Drone market by product type, commanding approximately 72% of total product type segment revenue in 2026, a dominant position reflecting rotary wing platforms' decisive operational versatility advantages over fixed-wing systems for the core precision agriculture applications of crop spraying, hovering crop inspection, localized field section monitoring, and variable-rate application missions that require vertical take-off and landing (VTOL) capability, low-altitude precision flight control, and stable hovering behavior in confined field environments.

DJI's Agras T40 and T10 agricultural multirotor spraying drones, and XAG Co., Ltd.'s P and R series multirotors, represent the world's most commercially deployed rotary wing agricultural drone platforms, with China's Ministry of Agriculture and Rural Affairs (MARA) documenting over 1.3 million agricultural multirotor drones registered for crop protection in China alone by 2023. Fixed Wing drones hold approximately 28% of product type revenue, valued for large-area field mapping, terrain surveying, and extended endurance NDVI monitoring missions across large-scale grain and oilseed farms in North America, Australia, and South America.

By Component Insights

Hardware leads the global Precision Agriculture Drone market by component, accounting for approximately 58% of total component segment revenue in 2026, a dominant position reflecting the structurally hardware-intensive nature of precision agriculture drone system procurement, where the drone platform frame, flight control computer, RTK GPS navigation module, propulsion system, multispectral camera, and LiDAR or thermal sensor payload represent the highest bill-of-materials cost components per system.

Within the hardware sub-segment, Cameras and Sensors collectively represent the highest-value and fastest-growing hardware component category, driven by the adoption of MicaSense RedEdge-P and Altum-PT multispectral sensors, DJI Zenmuse payload series, and Sentera (headquartered in Minneapolis, Minnesota, USA) agricultural sensing systems that transform standard drone platforms into certified precision agriculture measurement instruments. Software holds approximately 27% of component revenue, growing at the fastest segment CAGR driven by DroneDeploy, Pix4D, and Trimble Inc. cloud analytics subscriptions. Services hold approximately 15%, expanding through drone-as-a-service commercial agricultural spraying contracts.

By Farming Environment Insights

Outdoor Farming leads the global Precision Agriculture Drone market by farming environment, commanding approximately 87% of total farming environment segment revenue in 2026, a dominant position reflecting the precision agriculture drone's primary design optimization for large-scale open-field crop production environments where the operational advantages of drone-based monitoring, mapping, and spraying over conventional ground-based machinery are most commercially compelling.

The FAO's documented global cultivated land area of approximately 1.4 billion hectares, of which the vast majority is outdoor field crop production, confirms the structural scale of the outdoor farming addressable market for precision agriculture drone deployment. Indoor Farming holds approximately 13% of farming environment revenue, growing as a fast-emerging segment driven by vertical farming, controlled environment agriculture (CEA), and greenhouse operations adopting compact indoor drone platforms for automated crop scouting, pollination assistance, and environmental monitoring within enclosed growing structures.

By Application Insights

Crop spraying leads the global market by application, commanding approximately 36% of total application segment revenue in 2026, a dominant and rapidly expanding position driven by the commercial maturity of agricultural spraying drone technology in Asia Pacific markets, the compelling economics of 30–40% pesticide input savings and 90% water reduction documented by XAG Co., Ltd. operational data, and the expanding adoption of high-capacity agricultural spraying drones as the preferred crop protection machinery replacement across rice, wheat, corn, and specialty crop production in China, Japan, India, and Southeast Asia.

China's MARA data confirms 1.3 million registered agricultural spraying drones operating domestically, generating the world's largest single-country precision agriculture drone service revenue concentration. Field Mapping holds the second-largest application share at approximately 24%, driven by Trimble Inc., DroneDeploy, and Pix4D high-resolution agricultural field mapping service platforms. Variable Rate Application (VRA) is emerging as the fastest-growing application segment, with AI prescription map generation driving precision input optimization.

Regional Insights

North America Precision Agriculture Drone Trends & Insighs

The United States leads the North America Precision Agriculture Drone market, anchored by the world's most advanced agricultural technology adoption ecosystem, the FAA's progressive commercial UAS regulatory framework under Part 107 and ongoing BVLOS authorization expansion, and the USDA's Economic Research Service (ERS) documented above-average precision agriculture technology adoption rates among large commercial grain, soybean, and specialty crop operations across the Corn Belt, Great Plains, and Pacific Coast growing regions. AgroVironment, Inc., AgEagle Aerial Systems Inc., and Trimble Inc. are the most commercially significant U.S.-headquartered precision agriculture drone and analytics platform companies serving North American agricultural operators.

The USDA's Precision Agriculture: Adoption, Profitability, and Implications report confirms measurable yield and input efficiency improvements among U.S. farms adopting drone-based crop monitoring, reinforcing institutional support through USDA Farm Service Agency (FSA) and USDA Natural Resources Conservation Service (NRCS) precision agriculture technology adoption programs that provide cost-share funding for eligible agricultural drone system investments. Canada's Agriculture and Agri-Food Canada (AAFC) is actively promoting precision agriculture technology adoption through its Canadian Agricultural Partnership funding programs, with Canadian canola and grain producers in Saskatchewan, Manitoba, and Alberta representing a fast-growing North American precision agriculture drone adoption sub-market supported by Transport Canada's progressive commercial drone regulatory framework.

Europe Precision Agriculture Drone Trends & Insights

Europe is a structurally significant and regulatory innovation-active precision agriculture drone market, driven by the European Commission's Farm to Fork Strategy under the European Green Deal mandating a 50% reduction in chemical pesticide use and 20% reduction in fertilizer application by 2030 across EU member state agricultural operations, creating a regulatory-driven institutional mandate for precision application technologies including variable-rate agricultural drone spraying that directly reduces chemical input volumes per cultivated hectare. Germany, France, Spain, and the UK collectively represent Europe's four largest precision agriculture drone adoption markets, with Germany's large-scale grain and sugar beet production, France's viticulture sector drone adoption, and Spain's olive and specialty crop precision monitoring representing the most commercially advanced European agricultural drone application segments.

The European Union Aviation Safety Agency (EASA)'s U-space drone traffic management regulatory framework, progressively implemented across EU member states through 2024–2025, is creating the operational airspace infrastructure enabling commercial agricultural drone BVLOS operations at scale across European field crop production geographies. Parrot Drone SAS and Pix4D SA represent the most commercially prominent European-headquartered precision agriculture drone and analytics software companies, with Parrot's ANAFI Ai and ANAFI Work platforms certified for EASA operational categories and targeting European agricultural precision mapping and monitoring applications. Sky-Drones Technologies Ltd (headquartered in London, UK) serves European commercial agricultural and industrial drone operator markets with advanced autopilot and flight management system technology.

Asia Pacific Precision Agriculture Drone Trends & Insights

Asia Pacific is the dominant global Precision Agriculture Drone market by both deployment volume and manufacturing scale, anchored by China's position as the world's most commercially mature agricultural drone spraying market with China's Ministry of Agriculture and Rural Affairs (MARA) documenting over 1.3 million agricultural drones registered by 2023, Japan's Ministry of Agriculture, Forestry and Fisheries (MAFF) government-sponsored precision agriculture drone adoption programs sustaining high commercial deployment density per cultivated hectare, and India's DGCA Drone Rules 2021 and Drone Shakti scheme driving the world's fastest-emerging new agricultural drone deployment market.

DJI and XAG Co., Ltd., both headquartered in China, are the world's two most commercially dominant agricultural drone manufacturers by deployment volume, collectively representing the majority of global agricultural spraying drone operational fleet share. India's agricultural drone market, supported by the Indian government's INR 120 crore Drone Shakti initiative, Indian Council of Agricultural Research (ICAR) documented drone-based precision farming pilots across Kharif and Rabi crop seasons, and the Indian government's agricultural drone subsidy under the Sub-Mission on Agricultural Mechanisation (SMAM) scheme, is experiencing among the world's fastest agricultural drone adoption growth rates.

Airbots Aerospace Pvt. Ltd. (headquartered in Pune, Maharashtra, India) is India's most commercially active domestic agricultural drone manufacturer, developing indigenous agricultural spraying and mapping drone platforms certified by DGCA and targeting the Indian government's goal of deploying 100,000 agricultural drones across Indian farming operations under its precision agriculture modernization program.

Competitive Landscape

The global Precision Agriculture Drone market is moderately consolidated at the hardware platform level, with DJI commanding an estimated 70%+ share of the global consumer and commercial agricultural drone platform market by unit volume, while remaining highly competitive and fragmented at the agricultural analytics software, sensor payload, and specialized application platform levels where DroneDeploy, Pix4D, PrecisionHawk, and Sentera compete.

XAG dominates the Asia Pacific agricultural spraying segment. Key differentiators include FAA/EASA/DGCA regulatory certifications, RTK GPS positioning accuracy, spray system payload capacity, multispectral sensor integration, and AI crop analytics platform capability. Emerging business model trends include drone-as-a-service agricultural spraying contracts, AI-powered subscription crop monitoring SaaS platforms, and public-private partnership government subsidy-enabled drone fleet deployment programs.

Key Developments:

- In January 2025, DJI launched the Agras T50 agricultural spraying drone, featuring a 50 kg spray payload capacity, AI obstacle avoidance, and upgraded terrain-following radar, targeting large-scale commercial crop protection operations in Asia Pacific and Latin America, claiming the highest single-flight area coverage in its agricultural drone portfolio.

- In March 2024, XAG Co., Ltd. announced deployment of its P100 Pro agricultural drone fleet across 500,000 hectares of rice paddy operations in Hunan and Jiangxi provinces, China, achieving documented 35% pesticide reduction and 92% water savings versus conventional ground-based spraying machinery validated by China's Ministry of Agriculture and Rural Affairs (MARA).

- In October 2024, AgEagle Aerial Systems Inc. completed its strategic restructuring and product portfolio refocus, concentrating commercial operations on its eBee VISION fixed-wing precision mapping drone and RedEdge-P multispectral sensor platform, targeting North American and European commercial agricultural mapping and crop monitoring service provider customers.

Companies Covered in Precision Agriculture Drone Market

- DJI

- Parrot Drone SAS

- AgEagle Aerial Systems Inc.

- AeroVironment, Inc.

- PrecisionHawk

- Trimble Inc.

- DroneDeploy

- Autel Robotics

- Draganfly Inc.

- Pix4D SA

- Sky-Drones Technologies Ltd

- Sentera

- XAG Co., Ltd.

- Airpix

- Airbots Aerospace Pvt. Ltd.

Frequently Asked Questions

The global Precision Agriculture Drone market is estimated to be valued at US$ 3.3 Billion in 2026 and is projected to reach US$ 13.9 Billion by 2033, registering a forecast CAGR of 22.8% from 2026 to 2033.

The primary drivers are the FAO's documented global food demand growth mandate requiring agricultural productivity improvement, with USDA ERS data confirming 15–25% chemical input savings from drone-based precision application, and global regulatory liberalization including the FAA's Part 107 BVLOS framework, EASA's U-space implementation, and India's DGCA Drone Rules 2021.

Rotary Wing drones lead the Product Type segment with approximately 72% revenue share in 2026, driven by DJI Agras T50's 50 kg payload capacity, XAG P100 Pro's documented 35% pesticide reduction in Chinese rice paddy operations, and rotary wing VTOL and hovering capabilities enabling both precision crop spraying and targeted field inspection missions that fixed-wing platforms cannot replicate.

North America leads the global Precision Agriculture Drone market in technology leadership and commercial innovation, anchored by the FAA's Part 107 and progressive BVLOS authorization framework, USDA ERS documented precision agriculture ROI evidence, Trimble Inc.'s integrated precision agriculture drone and data platform, AeroVironment and AgEagle's U.S.-developed commercial drone systems.

The most significant opportunities are AI-integrated SaaS drone analytics platforms generating recurring subscription revenue, driven by European Commission Farm to Fork 50% pesticide reduction mandates, DroneDeploy and Pix4D cloud analytics growth, and high-capacity crop spraying drone adoption in India sustained by INR 120 crore Drone Shakti subsidies.

The leading companies include DJI, XAG Co., Ltd, Trimble Inc, AgEagle Aerial Systems Inc., AeroVironment, Inc., DroneDeploy, Pix4D SA, PrecisionHawk, Parrot Drone SAS, Sentera, Autel Robotics, Draganfly Inc., Sky-Drones Technologies Ltd, Airbots Aerospace Pvt. Ltd., Airpix, and Yamaha Motor Co., Ltd.