- Power Generation, Transmission, & Distribution

- Uranium Enrichment Market

Uranium Enrichment Market Size, Share, and Growth Forecast 2026 - 2033

Uranium Enrichment Market by Technology (Gas Centrifuge, Gaseous Diffusion, Laser Enrichment, Others), by Enrichment Level (Low Enriched Uranium (LEU: ≤5%), High-Assay Low Enriched Uranium (HALEU: 5-20%), Highly Enriched Uranium (HEU: >20%)), by Application, by Industry, and Regional Analysis, 2026 - 2033

Uranium Enrichment Market Size and Trend Analysis

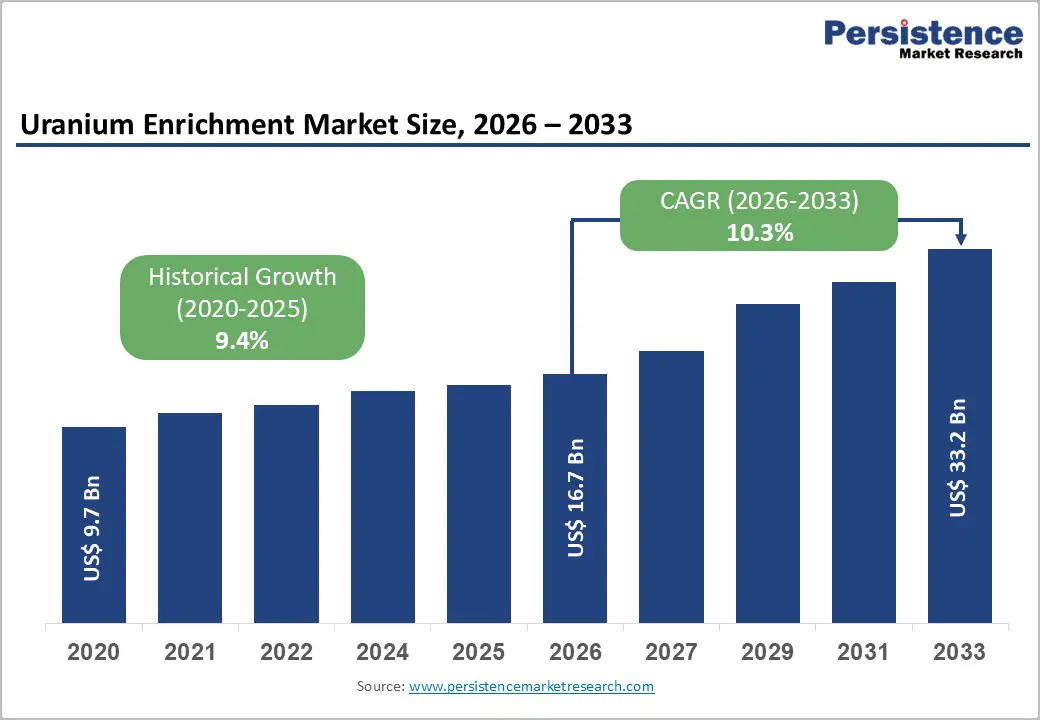

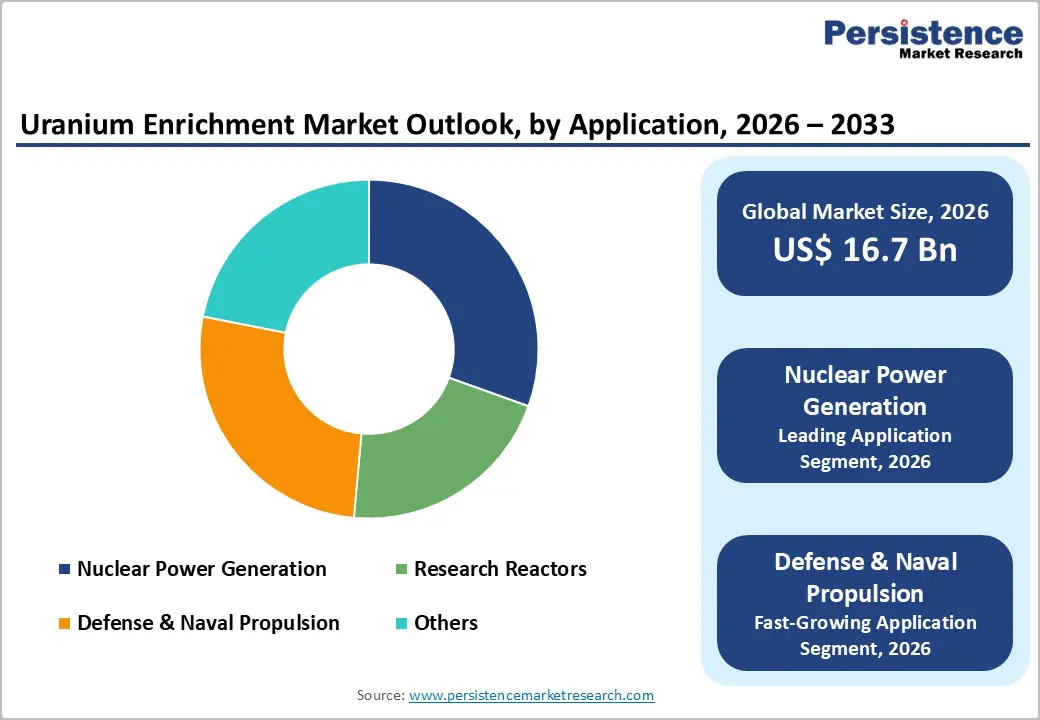

The global uranium enrichment market size is expected to be valued at US$ 16.7 billion in 2026 and projected to reach US$ 33.2 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033. This growth is driven by accelerating nuclear energy adoption as countries prioritize low-carbon baseload power alongside rising electricity demand and energy security concerns.

Expanding reactor fleets and the life extension of existing plants are strengthening long-term fuel requirements. According to the IAEA, nuclear energy contributes around 10% of global electricity from 440 reactors, with further capacity additions planned. This directly boosts demand for LEU and enrichment services, sustaining strong market momentum.

Key Industry Highlights:

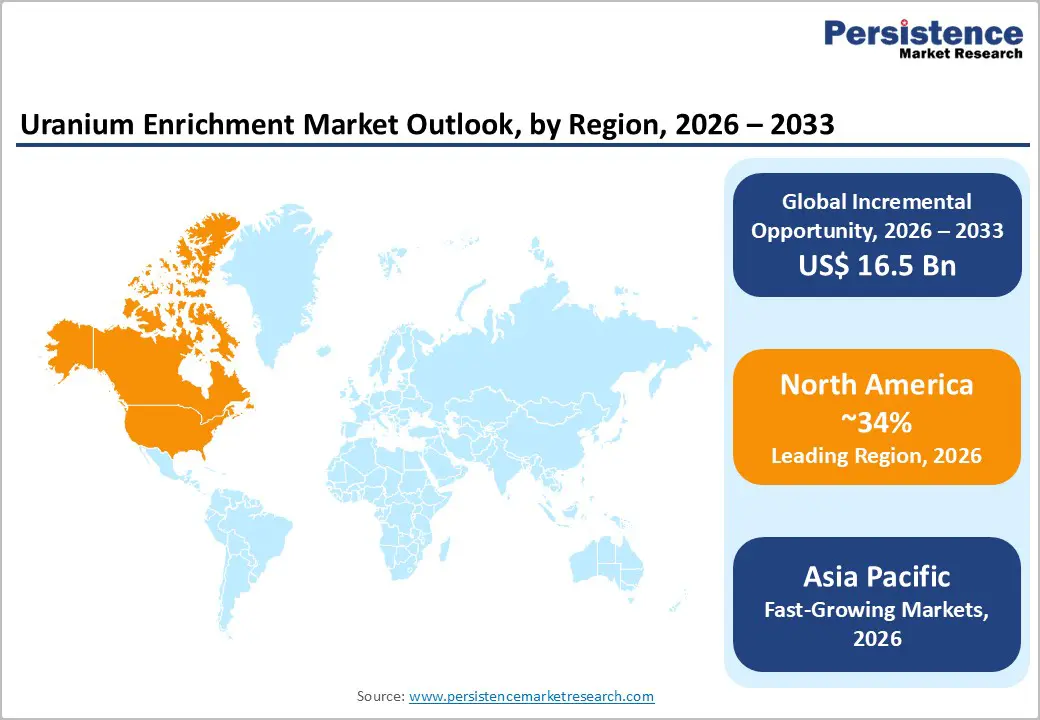

- Leading Region: North America leads the Uranium Enrichment Market with 34% share in 2025, driven by strong domestic enrichment programs and advanced reactor initiatives.

- Fastest Growing Region: Asia Pacific holds 31% share in 2025 and is the fastest growing region, supported by large-scale nuclear expansion in China, India, and other emerging economies.

- Leading Technology: Gas Centrifuge dominates with 35% share in 2025, due to high efficiency, lower operating cost, and global deployment.

- Fastest Growing Category (Enrichment Level): HALEU (5-20%) is the fastest growing segment, driven by demand from advanced reactors and SMRs.

- Key Market Opportunity: HALEU fuel supply chain development is a major opportunity, enabling next-generation reactors and long-term market expansion.

Market Dynamics

Drivers - Rising Nuclear Capacity and Strong Clean Energy Commitments Globally

A major driver of the Uranium Enrichment Market is the global expansion of nuclear power generation, supported by decarbonization and energy security policies. According to the IEA and WNA, over 90% of nuclear electricity comes from low-carbon sources. Many G7 and EU countries are integrating nuclear into clean energy roadmaps, sustaining long-term demand for enriched uranium, especially LEU, and driving enrichment capacity expansion.

This policy-driven nuclear build-out is translating into higher fuel requirements and stronger contract demand for enrichment services. As new reactors are planned and existing plants undergo life extension, utilities are securing long-term uranium supply agreements. This is encouraging enrichment operators to invest in capacity upgrades and technological modernization, reinforcing steady market growth momentum.

Strengthening Supply Chain Diversification and Energy Security Measures

Geopolitical tensions and supply chain vulnerabilities are accelerating diversification of uranium enrichment sources. Following the Russia-Ukraine conflict, Western nations and utilities have intensified efforts to reduce dependency on Russian enrichment services, increasing demand for suppliers in Europe, North America, and Asia. This shift is reshaping procurement strategies and strengthening regional supply resilience.

The EU’s Euratom Supply Agency has reinforced diversification and monitoring requirements, encouraging development of domestic enrichment capabilities. This is driving investments in new facilities, capacity expansions, and technology partnerships. As a result, alternative enrichment providers are gaining traction, expanding the competitive landscape and supporting long-term market growth for uranium enrichment services globally.

Restraints - Stringent Non-Proliferation Rules and Heavy Regulatory Oversight

A key restraint on the Uranium Enrichment Market is the strict regulatory environment governed by international non-proliferation frameworks and national nuclear authorities. Enrichment facilities must comply with IAEA safeguards, security protocols, and environmental clearances, which significantly extend approval timelines. Licensing and regulatory processes can delay projects by 12-18 months or more, increasing compliance costs and slowing capacity expansion.

These stringent requirements create high entry barriers for new participants and limit market participation to a few established players. In emerging economies, underdeveloped nuclear regulatory systems further complicate project execution. As a result, expansion becomes slow and capital-intensive, reducing the flexibility to scale enrichment infrastructure to meet rapidly growing global nuclear fuel demand.

High Capital Intensity and Extended Payback Period Challenges

Another major restraint is the extremely high capital requirement for uranium enrichment infrastructure. Modern gas centrifuge facilities require multi-billion-dollar investments, along with long construction timelines and significant upfront spending on safety systems, technology acquisition, and operational setup. These financial demands make uranium enrichment one of the most capital-intensive segments of the nuclear fuel cycle.

According to OECD NEA insights, such projects often involve decade-long planning and implementation cycles, making returns slow and dependent on long-term contracts. This discourages private investment without strong government backing or guaranteed offtake agreements. Consequently, the market remains concentrated among a few large, state-backed players, limiting competition and slowing the pace of new capacity additions globally.

Opportunities - Expansion of HALEU Supply Chain for Next-Generation Nuclear Reactors

One of the most significant opportunities in the Uranium Enrichment Market is the growing demand for High Assay Low Enriched Uranium (HALEU) to support advanced reactors and small modular reactors (SMRs). These next-generation reactor designs require uranium enriched between 5% and 20% U-235, significantly higher than conventional LEU used in light water reactors, creating a new fuel category and expanding market scope.

The U.S. Department of Energy (DOE) and other global agencies are actively supporting HALEU development through funding programs and partnerships, including initiatives with companies like Centrus Energy. Establishing a secure HALEU supply chain is expected to unlock new long-term revenue streams for enrichment providers while reshaping the nuclear fuel ecosystem and strengthening demand visibility for advanced nuclear technologies.

Policy-Driven Nuclear Expansion Across Emerging and Developing Economies

Another major opportunity comes from large-scale nuclear expansion programs led by governments in Asia and other developing regions. Countries such as China, India, and South Korea are aggressively increasing nuclear capacity to meet rising electricity demand, while emerging economies in Southeast Asia and the Middle East are initiating new nuclear power programs with international collaboration and technical support.

These expansions are typically backed by long-term fuel supply agreements, providing stable demand for uranium enrichment services over multiple decades. In some cases, governments are also considering domestic enrichment capabilities or strategic joint ventures. This is expected to create new regional enrichment hubs, diversify the global supply chain, and significantly enhance long-term market growth potential.

Category-wise Analysis

Technology Insights

Gas centrifuge is the clear leading segment, accounting for approximately 35% of global uranium enrichment capacity in 2025. Its dominance is driven by superior energy efficiency, lower operating costs, and significantly higher separation performance compared to legacy methods such as gaseous diffusion. Major players such as Urenco and Rosatom have heavily invested in large-scale centrifuge cascades, while older diffusion-based facilities have largely been phased out globally.

Laser enrichment is emerging as the fastest-growing technology segment, driven by its potential for higher separation efficiency, smaller facility footprint, and reduced energy requirements. Although still in pilot and demonstration stages due to technical and regulatory challenges, it is gaining strategic interest for next-generation fuel production systems.

Enrichment Level Insights

Low Enriched Uranium (LEU ≤5%) dominates the Enrichment Level category, representing approximately 52% of the market in 2025. This reflects the widespread use of LEU in over 400 commercial light water reactors globally, making it the backbone of nuclear fuel demand. Long-term utility contracts and standardized reactor fuel cycles further reinforce its dominant position in the enrichment ecosystem.

High-Assay Low Enriched Uranium (HALEU) is emerging as the fastest-growing segment, driven by advanced reactor designs and small modular reactors requiring higher enrichment levels for efficiency and longer fuel cycles. Government-backed initiatives and dedicated supply chain development are accelerating its adoption, positioning HALEU as a key future growth driver.

Application Insights

Nuclear power generation is the dominant application segment, accounting for approximately 58% of total uranium enrichment demand in 2025. Continuous fuel requirements from operating reactors, life extension programs, and new nuclear plant construction are major drivers. Utilities and power operators form the largest customer base, supported by long-term fuel procurement contracts that ensure stable enrichment demand globally.

Defense & naval propulsion is the fastest-growing application segment, supported by increasing investments in nuclear-powered submarines, aircraft carriers, and strategic defense programs. These applications require highly specialized fuel and are closely tied to national security strategies, leading to stable, long-duration contracts with state-backed enrichment providers.

Industry Insights

The energy & utilities segment leads the Industry category, accounting for approximately 42% of global demand in 2025. This dominance is driven by nuclear power plants operated by utilities and state agencies, which rely heavily on LEU fuel for continuous electricity generation. Long-term supply agreements and decarbonization commitments further reinforce this segment’s structural importance.

Government & Defense is emerging as the fastest-growing end-use segment, supported by rising investments in nuclear propulsion programs, research reactors, and national energy security strategies. These requirements are typically supported by state-led procurement frameworks, making the segment strategically important despite its smaller overall volume.

Regional Insights

North America Uranium Enrichment Market Trends and Insights

North America is a key hub in the Uranium Enrichment Market, accounting for approximately 34% share in 2025, with the United States leading regional demand and policy initiatives. The region benefits from a mature nuclear fleet, strong regulatory oversight by the U.S. Nuclear Regulatory Commission (NRC), and active government support from the Department of Energy (DOE). Programs supporting domestic enrichment, including HALEU production initiatives by Centrus Energy, are strengthening supply chain resilience and enabling next-generation reactor deployment.

The region is also witnessing increased life extensions of existing nuclear plants and selective new build considerations driven by clean energy goals and grid reliability needs. Strategic partnerships between national laboratories, private companies, and utilities are accelerating innovation in enrichment technologies. These developments are reinforcing long-term demand stability and positioning North America as both a consumption and strategic supply base for enriched uranium services.

Europe Uranium Enrichment Market Trends and Insights

Europe remains a major player in the Uranium Enrichment Market, with leading facilities operated by Urenco and Orano across Germany, France, and the Netherlands. The region accounts for a significant share of global enrichment capacity and is supported by strong regulatory alignment under the Euratom framework. Europe is projected to grow at a CAGR of around 8.5%, driven by energy security concerns, nuclear inclusion in the clean energy taxonomy, and post-Ukraine geopolitical shifts.

The region is also focusing on reactor life extensions, EPR deployments, and small modular reactor development, all of which sustain long-term demand for enriched uranium. Policy support for reducing dependency on external suppliers and increasing fuel cycle autonomy is encouraging investment in both conventional LEU and emerging HALEU technologies. Europe’s integrated nuclear ecosystem ensures stable, policy-driven market expansion over the forecast period.

Asia Pacific Uranium Enrichment Market Trends and Insights

Asia Pacific is the fastest-growing region in the Uranium Enrichment Market, holding approximately 31% share in 2025, driven by rapid nuclear capacity expansion across China, India, South Korea, and emerging Southeast Asian economies. China’s large-scale reactor construction program and India’s long-term nuclear expansion strategy are significantly increasing demand for both domestic and imported enrichment services.

The region is also becoming a focal point for advanced reactors and SMR deployments, supported by strong government backing and industrial policy initiatives. Increasing electricity demand, decarbonization targets, and energy security concerns are further accelerating nuclear investments. Regional cooperation frameworks and manufacturing capabilities for nuclear components are strengthening supply chain integration, positioning the Asia Pacific as a long-term growth engine and potential future center for enrichment technology development.

Competitive Landscape

The Uranium Enrichment Market is highly consolidated, with a small group of state-owned or state-linked entities controlling most global enrichment capacity. High capital requirements, strict regulatory oversight, and complex nuclear technologies create strong entry barriers, limiting participation from new players. Long-term supply contracts with utilities and government agencies further reinforce the dominance of established operators and ensure stable demand visibility across the value chain.

Competition is increasingly defined by technological efficiency, fuel flexibility, and geographic reach. Operators are investing in advanced centrifuge systems, digital monitoring, and safer, more efficient enrichment processes. Growing demand for advanced reactor fuels is also encouraging partnerships, joint ventures, and integrated fuel supply models, reshaping competitive strategies across the industry.

Key Developments:

- In June 2024, Centrus Energy commissioned the first U.S.-based facility capable of producing High-Assay Low Enriched Uranium (HALEU) under a contract with the U.S. Department of Energy, marking a critical milestone in the development of a domestic HALEU supply chain for advanced reactors.

- In October 2024, Urenco announced a capacity expansion at its Almelo enrichment plant in the Netherlands, increasing separative work capability by several hundred thousand SWU (Separative Work Units) to better serve European utilities and support energy-security objectives.

- In March 2025, Orano signed a long-term LEU-supply agreement worth several hundred million dollars with U.S. utilities, reflecting growing demand for diversified, non-Russian enrichment sources and reinforcing Europe’s role as a key supplier in the global market.

Uranium Enrichment Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 9.7 Bn |

| Current Market Value (2026) | US$ 16.7 Bn |

| Projected Market Value (2033) | US$ 33.2 Bn |

| CAGR (2026 - 2033) | 10.3% |

| Leading Region | North America, 34% share |

| Dominant Application | Nuclear Power Generation, 58% share |

| Top-ranking Technology | Gas Centrifuge, 35% |

| Incremental Opportunity | US$ 16.5 Bn |

Companies Covered in Uranium Enrichment Market

- Urenco Group

- Orano

- Rosatom

- China National Nuclear Corporation

- Centrus Energy Corp.

- China General Nuclear Power Group

- Japan Nuclear Fuel Limited

- Global Laser Enrichment

- Nuclear Fuel Complex

- Pakistan Atomic Energy Commission

- Kazakhstan Uranium Enrichment Center

- NAC Kazatomprom

- Westinghouse Electric Company

- Cameco Corporation

- Enusa Industrias Avanzadas

Frequently Asked Questions

The uranium enrichment market is expected to be valued at US$ 16.7 billion in 2026 and reach US$ 33.2 billion by 2033, growing at a CAGR of 10.3%.

Demand is driven by nuclear power expansion, decarbonization policies, reactor life extensions, and supply chain diversification, with over 400 operating reactors increasing LEU fuel requirements.

North America is the leading region in the Uranium Enrichment Market, accounting for approximately 34% of global demand in 2025.

The key opportunity is HALEU fuel supply chain development for advanced reactors and SMRs, supported by government-backed nuclear innovation programs.

The key market participants include Urenco, Rosatom, Orano, Centrus Energy, CNNC, and Anglo American.