- Power Generation, Transmission, & Distribution

- Water Desalination Market

Water Desalination Market Size, Share, and Growth Forecast 2026 - 2033

Water Desalination Market by Source (Seawater, Brackish water, River water, Others), Technology (Membrane Technology, Thermal Technology), Application (Industrial, Municipal, Others), and Regional Analysis, 2026 - 2033

Water Desalination Market Size and Trend Analysis

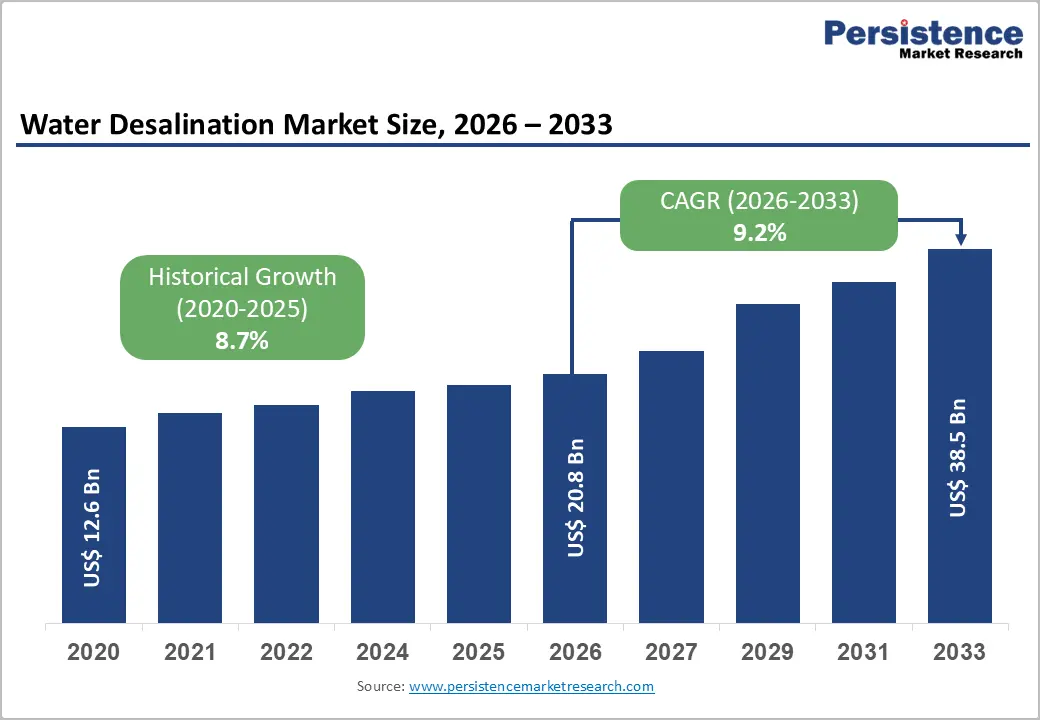

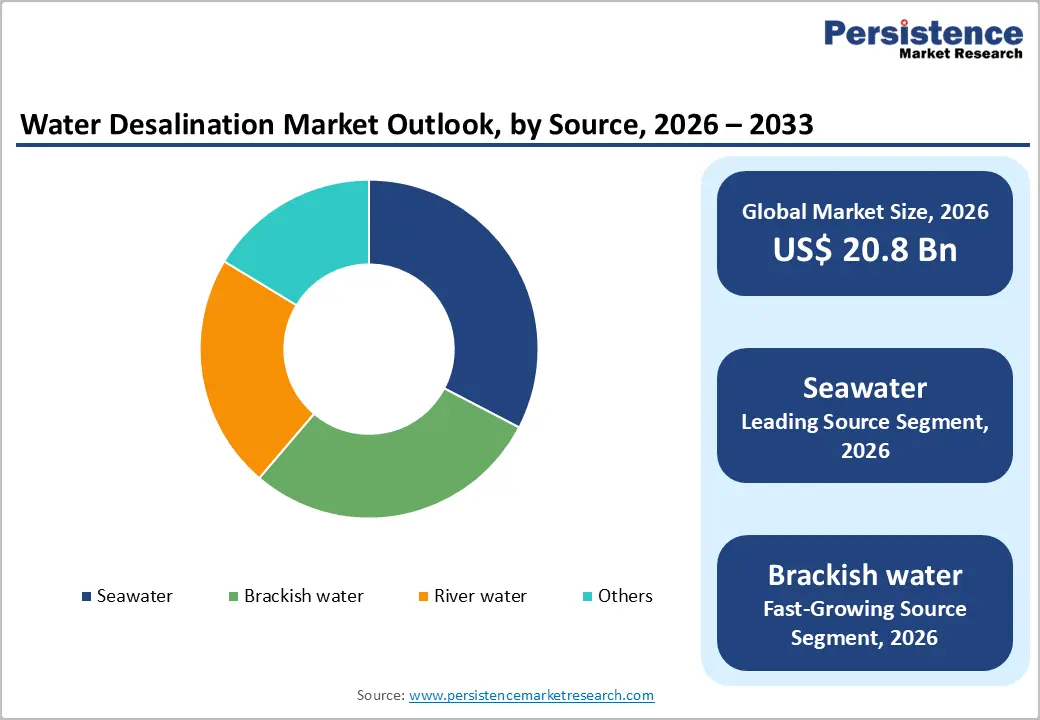

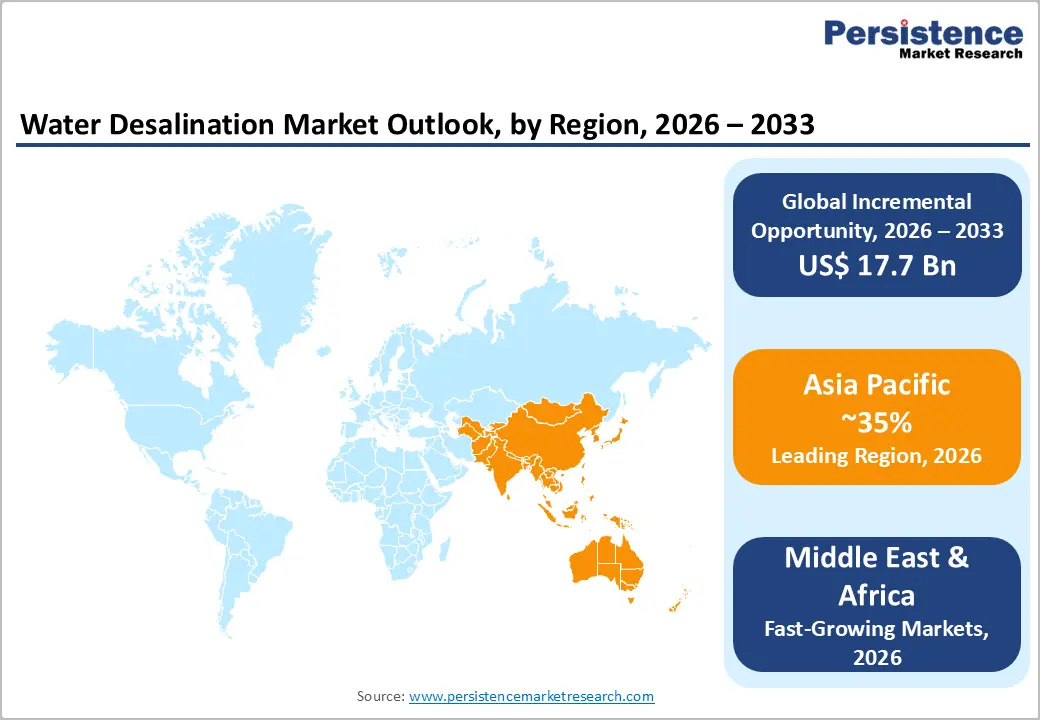

The global water desalination market size is expected to be valued at US$ 20.8 billion in 2026 and projected to reach US$ 38.5 billion by 2033, growing at a CAGR of 9.2% between 2026 and 2033.

Rapidly intensifying water scarcity is accelerating adoption, as declining freshwater reserves and urban expansion strain supply systems. Over 2.2 billion people lack access to safe drinking water, underscoring the urgency for alternative solutions. Climate-driven droughts and rising water stress across multiple regions are strengthening policy support and investments. At the same time, advancements in membrane efficiency and energy optimization are reducing costs, positioning desalination as a critical, scalable solution for long-term global water security.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the market with 35% share in 2025, driven by large-scale municipal and industrial desalination demand.

- Fastest Growing Region: Middle East & Africa is the fastest-growing region due to strong water security investments and extreme water scarcity.

- Leading Source: Seawater dominates with 65% share in 2025, supported by abundant availability and coastal plant concentration.

- Fastest Growing Technology: Membrane Technology is the fastest growing due to efficiency, scalability, and wide RO adoption.

- Key Market Opportunity: Renewable-integrated desalination offers 20-30% cost savings and supports sustainable water infrastructure growth.

Market Dynamics

Drivers - Rising Global Water Stress and Increasing Population Demand Pressure

Global water scarcity is a major driver of the water desalination market, with nearly 4 billion people facing shortages for at least one month annually. Climate change, groundwater depletion, and uneven rainfall patterns are worsening supply conditions. Rapid urbanization and population growth are intensifying pressure on limited freshwater resources, particularly in arid regions such as the Middle East and North Africa.

Governments and utilities are increasingly turning to desalination as a reliable and drought-resilient water source. Expanding populations, projected to grow by 2 billion by 2050, are accelerating large-scale desalination investments. Coastal regions are prioritizing seawater and brackish water treatment to secure long-term potable and industrial water supply, strengthening infrastructure pipelines and public funding initiatives.

Technological Advancements Driving Energy Efficiency and Cost Optimization

Technological innovation is significantly improving the economic viability of desalination processes. Modern membrane-based reverse osmosis systems have reduced energy consumption to nearly 3 kWh/m³, compared to traditional thermal methods requiring substantially higher energy input. These advancements are addressing one of the sector’s most critical cost barriers and enhancing operational efficiency across large-scale plants.

Energy recovery devices and system optimization techniques are further lowering energy use by up to 50%, making desalination more financially attractive. Additionally, integration with renewable energy sources such as solar and wind is gaining traction, particularly in coastal regions. This shift supports sustainability goals while reducing dependence on fossil fuels, encouraging broader adoption and investment through public-private partnerships.

Restraints - High Capital Investment Requirements and Ongoing Operational Cost Burdens

High capital and operational costs remain a key restraint in the Water Desalination market, limiting widespread adoption. Large-scale plants require significant upfront investment, often reaching US$ 1-2 million per million gallons per day capacity. Additionally, ongoing expenses such as energy, maintenance, and system upgrades contribute heavily to total lifecycle costs, creating financial barriers for utilities and governments.

Energy consumption alone can account for 30-50% of operating costs, making desalination particularly sensitive to energy price fluctuations. The need for advanced pretreatment systems and corrosion-resistant materials further increases expenditure. In regions with subsidized water pricing or limited financial resources, these cost challenges can delay project execution and restrict adoption, especially among smaller utilities and emerging economies.

Environmental Impact Concerns and Stringent Regulatory Compliance Requirements

Environmental challenges, particularly related to brine disposal, pose significant constraints on desalination expansion. Concentrated brine discharge can disrupt marine ecosystems by altering salinity, temperature, and oxygen levels, potentially harming aquatic life. These ecological risks have raised concerns among environmental organizations, emphasizing the need for improved waste management and mitigation technologies.

Stringent regulatory frameworks across regions require strict monitoring and treatment of discharge and chemical by-products, increasing compliance costs and project complexity. Additionally, public opposition to large coastal desalination plants in some areas has led to permitting delays and redesign requirements. These environmental and regulatory pressures can slow project approvals and limit market growth despite rising water demand.

Opportunities - Growing Integration of Desalination Systems with Renewable Energy Sources

The integration of desalination with renewable energy is emerging as a major growth opportunity for the market. Technologies combining solar and wind power with reverse osmosis systems are helping reduce dependence on fossil fuels while lowering operational costs. Such hybrid solutions are particularly suitable for coastal regions with high solar irradiance and wind potential, enabling sustainable large-scale water production.

Energy savings of 20-30% compared to conventional systems are improving project feasibility and investor interest. Several countries in the Gulf Cooperation Council, Australia, and North Africa are already deploying renewable-powered desalination plants. This approach not only supports climate goals but also strengthens long-term water security, making it a scalable and future-ready solution for water-stressed regions.

Expanding Municipal and Industrial Demand Driving Desalination Adoption

Rising urbanization and industrialization are significantly expanding the application scope of desalination globally. With more than half of the world’s population living in urban areas, demand for reliable and clean water sources is intensifying, especially in coastal megacities. Municipal authorities are increasingly adopting desalination to ensure a continuous potable water supply and reduce dependency on limited freshwater reserves.

At the same time, industries such as power generation, mining, petrochemicals, and semiconductors require consistent high-quality water for operations. This is accelerating the adoption of desalination in industrial processes. Government-led water security initiatives and infrastructure investments are further supporting market growth, driving demand for both modular systems and large-scale desalination plants worldwide.

Category wise Insights

Source Analysis

Seawater is the leading segment in the water desalination market, accounting for approximately 65% of the global share in 2025. Its dominance is driven by its vast availability, as it constitutes nearly 97% of Earth’s total water resources, making it the most viable feedstock for large-scale desalination. Coastal regions, particularly in the Middle East and North Africa, rely heavily on seawater-based plants to meet municipal and industrial water demand.

Brackish water is emerging as the fastest-growing segment due to its lower salinity and reduced energy requirements for treatment. It offers a cost-effective alternative for inland and semi-arid regions where seawater access is limited. Increasing adoption in industrial and municipal applications, along with easier regulatory approvals and lower operational complexity, is driving rapid growth of brackish water desalination systems globally.

Technology Insights

Membrane technology, particularly reverse osmosis (RO), dominates the market with an estimated 75% share in 2025. Its leadership is attributed to lower energy consumption, modular scalability, and operational efficiency compared to traditional thermal methods. Advancements in membrane materials and system design have further enhanced performance, making it the preferred choice for both large-scale municipal projects and industrial applications worldwide.

It also remains the fastest-growing segment, driven by continuous innovation and cost optimization. Increasing integration with renewable energy systems and digital monitoring solutions is accelerating adoption. Its flexibility in handling different water sources and suitability for decentralized systems are expanding its use across emerging markets, positioning it as the key driver of future desalination infrastructure development.

Application Insights

The municipal segment leads the water desalination market, holding approximately 55% share in 2025. This dominance reflects the critical role of desalination in providing potable water to urban populations, especially in water-scarce regions. Governments and utilities are investing heavily in large-scale desalination plants to ensure a reliable drinking water supply and strengthen urban water security systems.

Industrial application is the fastest-growing segment, driven by increasing demand for high-quality process water across sectors such as power generation, petrochemicals, and mining. Industries are adopting desalination to reduce dependence on freshwater sources and comply with environmental regulations. Growing industrialization and stricter water usage policies are accelerating the expansion of desalination solutions in industrial operations globally.

Regional Insights

North America Water Desalination Market Trends and Insights

North America is a mature yet steadily growing water desalination market, driven by increasing water stress in coastal and arid regions, particularly in the United States. The region is estimated to grow at a CAGR of 8.5% during the forecast period, supported by rising investments in drought-resilient water infrastructure and advanced desalination technologies.

Growth is supported by government funding initiatives such as the Infrastructure Investment and Jobs Act, which promotes desalination and water reuse projects. The presence of advanced facilities like the Carlsbad Desalination Plant highlights technological leadership in large-scale reverse osmosis systems. Strong regulatory frameworks, environmental compliance standards, and innovation in energy recovery systems are further enhancing efficiency and encouraging sustainable desalination development across the region.

Asia Pacific Water Desalination Market Insights

Asia Pacific is the leading region in the Water Desalination market, accounting for approximately 35% of the global share in 2025. This dominance is driven by rapid urbanization, industrial expansion, and increasing freshwater stress across major economies such as China, India, Japan, and Southeast Asia. Large-scale desalination projects, particularly in coastal megacities, are strengthening municipal water supply systems and supporting long-term water security initiatives.

The region is also witnessing strong expansion in both municipal and industrial applications due to growing population density and manufacturing activity. Countries like China and India are heavily investing in coastal desalination infrastructure, while Singapore and Japan are integrating advanced membrane systems with water reuse technologies. Favorable manufacturing ecosystems and government-backed water security programs are further accelerating adoption, reinforcing Asia Pacific’s leadership position globally.

Middle East & Africa Water Desalination Market Analysis

Middle East & Africa is the fastest-growing region in the Water Desalination market, driven by extreme water scarcity and heavy reliance on non-conventional water sources. The region holds a significant share of global desalinated water production, supported by large-scale government investments and strategic water security programs, particularly across GCC countries such as Saudi Arabia and the UAE.

Expansion is fueled by rising population demand, urban development, and limited freshwater availability, making desalination a critical infrastructure priority. Mega projects and public-private partnerships are accelerating capacity additions, especially in seawater desalination plants. Increasing adoption of energy-efficient and renewable-integrated systems is further supporting growth, positioning the region as the fastest-expanding desalination market globally.

Competitive Landscape

The global water desalination industry is moderately consolidated, with a limited number of large global engineering and water infrastructure providers controlling a significant share of high-value projects and installed capacity. These players primarily secure large-scale public-private partnership and build-operate-own contracts, especially in regions with acute water scarcity and strong government involvement. Competitive advantage is driven by advanced membrane systems, energy recovery technologies, and integrated digital monitoring platforms that improve plant efficiency and lifecycle performance.

The market remains fragmented at the execution level, with many regional and specialized firms operating in niche applications. These include brackish water treatment systems, modular desalination units for remote areas, and emergency water supply solutions. Increasing adoption of service-based contracts, performance-guaranteed operations, and long-term infrastructure agreements is reshaping competition. This dual structure creates opportunities for both established global players and agile regional participants to coexist and expand.

Key Developments:

- In June 2025, Veolia secured a contract worth approximately US$ 1.2 billion for the Shuqaiq 3 expansion project in Saudi Arabia, which will increase the plant’s desalination capacity by around 450,000 m³ per day and reinforce the country’s position as a world-leading desalination hub.

- In March 2024, IDE Technologies launched a solar-powered reverse osmosis desalination plant in Australia, integrating large-scale photovoltaic arrays with energy-recovery devices to reduce operational energy consumption by about 40% compared with conventional gridconnected plants.

- In October 2023, Acciona was awarded a €500 million contract to upgrade and expand several desalination facilities in Spain, enhancing combined output by approximately 200,000 m³ per day and improving energy efficiency through advanced automation and membrane-monitoring systems.

Water Desalination Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 12.6 Bn |

| Current Market Value (2026) | US$ 20.8 Bn |

| Projected Market Value (2033) | US$ 38.5 Bn |

| CAGR (2026 - 2033) | 9.2% |

| Leading Region | Asia Pacific, 35% share |

| Dominant Application | Municipal, 55% share |

| Top-ranking Product | Seawater, 65% |

| Incremental Opportunity | US$ 17.7 Bn |

Companies Covered in Water Desalination Market

- Veolia Environnement

- SUEZ

- IDE Technologies

- Doosan Enerbility

- ACCIONA Agua

- Xylem Inc.

- Aquatech International

- Toray Industries

- LG Chem

- Abengoa Water

- VA Tech Wabag

- Hyflux Ltd.

- Kurita Water Industries

- Evoqua Water Technologies

- ACWA Power

Frequently Asked Questions

The Water Desalination market is projected to reach around US$ 20.8 Billion in 2026, driven by rising global water scarcity and infrastructure expansion.

Key demand drivers include severe water scarcity, rapid urbanization, climate change impacts, and advances in energy-efficient reverse osmosis technology.

Asia Pacific leads the market with 35% share in 2025, supported by large-scale desalination projects across China, India, and Southeast Asia.

A major opportunity is integrating desalination with renewable energy, reducing costs, emissions, and supporting sustainable water infrastructure development.

Key players include major global water and engineering firms such as Veolia, IDE Technologies, Acciona, Siemens, Suez, Doosan, Metito, and others.