- Inks, Coatings, Adhesives & Sealants (ICAS)

- Polyethylene (PE) Foams Market

Polyethylene (PE) Foams Market Size, Share, and Growth Forecast 2026 - 2033

Polyethylene (PE) Foams Market by Product Type (XLPE, Non-XLPE), Density (LDPE Foam, HDPE Foam), Application (Protective Packaging, Automotive, Building & Construction, Footwear, Sports & Recreational, Medical, Others), and Regional Analysis for 2026 - 2033

Polyethylene (PE) Foams Market Size and Trend Analysis

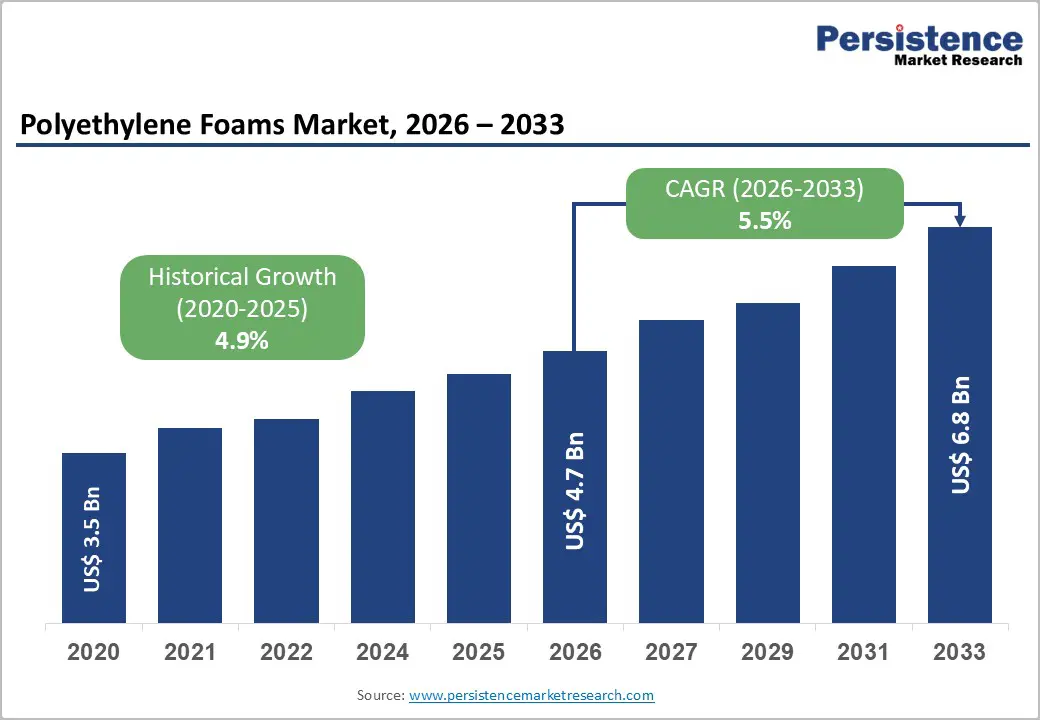

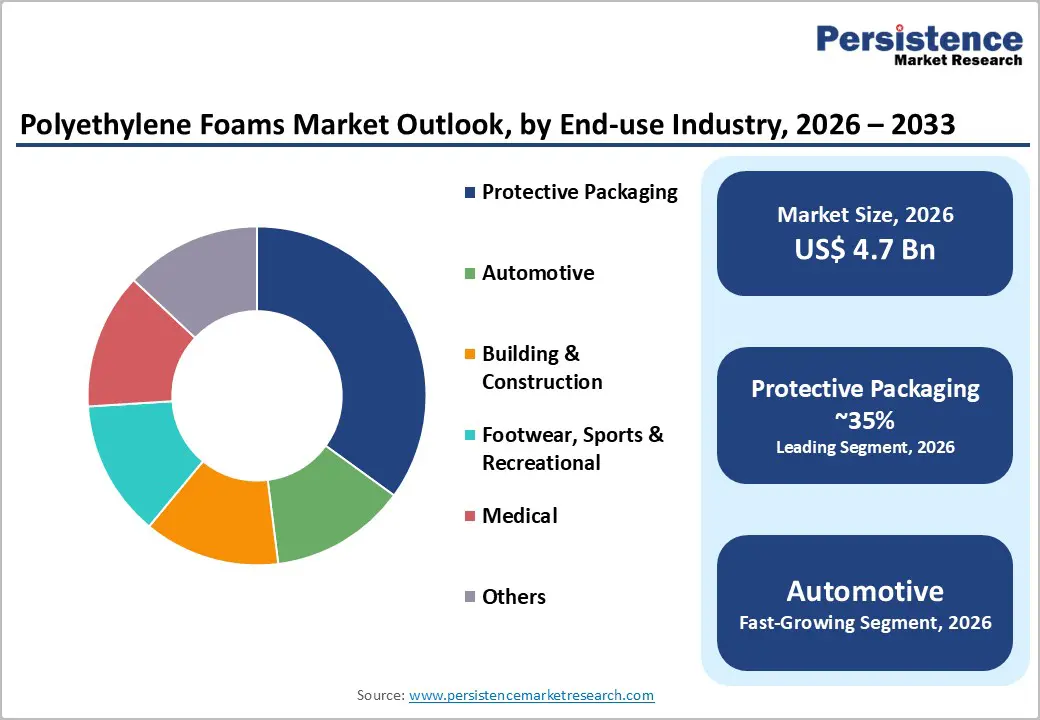

The global polyethylene (PE) foams market is valued at US$ 4.7 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Rising demand for lightweight protective packaging, driven by surging e-commerce volumes and aggressive automotive lightweighting initiatives to meet stringent CO2 emission regulations, is the primary catalyst propelling market expansion. The material’s unique combination of superior cushioning, thermal insulation, chemical resistance, and moisture barrier properties has made PE foam indispensable across protective packaging, automotive, building & construction, medical, and footwear applications globally.

Key Market Highlights

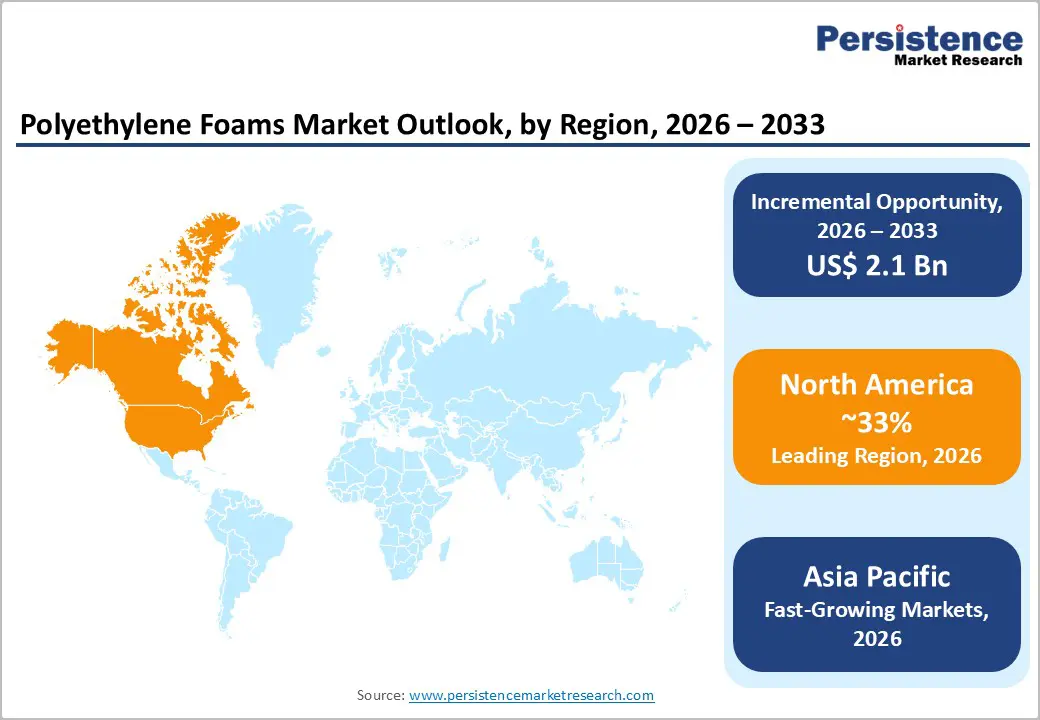

- Regional Leader: North America leads the global PE Foams market, with 33% market share, driven by advanced automotive OEM activity, surging e-commerce packaging demand, and the U.S. construction sector spending exceeding US$ 2 trillion annually, supported by ASTM International and EPA quality standards.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, propelled by rapid industrialization in China and India, expanding e-commerce ecosystems, government-backed manufacturing programs such as India’s PLI scheme, and large-scale infrastructure development under China’s Belt and Road Initiative.

- Leading Segment: Protective Packaging is the dominant application segment, accounting for approximately 35% of total market revenue, underpinned by surging global trade volumes tracked by the World Trade Organization (WTO) and rising demand for damage-proof electronics and pharmaceutical packaging.

- Fastest Growing Segment: LDPE Foam is the fastest-growing density segment, driven by its superior flexibility, processing ease, and competitive pricing advantage over HDPE Foam across packaging, sports, and automotive end-use applications.

- Key Market Opportunity: Medical-grade XLPE foam for orthopedic, prosthetics, and rehabilitation applications represents the highest-value growth opportunity, supported by the WHO’s projection of a global aging population of 1.5 billion aged 65+ by 2050 and expanding healthcare infrastructure investment in emerging markets.

| Key Insights | Details |

|---|---|

| Polyethylene (PE) Foams Market Size (2026E) | US$ 4.7 Bn |

| Market Value Forecast (2033F) | US$ 6.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 4.9% |

Market Dynamics

Market Growth Drivers

Surge in E-Commerce and Protective Packaging Demand

The rapid expansion of global e-commerce has substantially increased the demand for PE foam-based protective packaging. With worldwide online sales exceeding US$26 trillion and continuing to grow at double-digit rates in emerging markets, the requirement for reliable and efficient cushioning materials has intensified. PE foams, particularly cross-linked variants, are favored for their superior shock absorption, vibration damping, and moisture resistance, making them essential for safeguarding delicate electronics, automotive components, and pharmaceutical products during transit.

As supply chains become more complex and shipment volumes rise, major e-commerce platforms such as Amazon and Alibaba have adopted standardized PE foam inserts and liners to ensure product integrity. Consequently, PE foam has solidified its strategic, irreplaceable role within the global logistics and protective packaging ecosystem.

Automotive Lightweighting and Electric Vehicle (EV) Proliferation

The automotive industry’s relentless pursuit of lightweighting to meet stringent fuel-efficiency and emissions standards has positioned PE foams as a critical material in vehicle manufacturing. Regulatory bodies such as the European Commission have mandated average CO2 emission targets of 95 g/km for passenger cars, compelling automakers to replace heavy conventional materials with advanced lightweight alternatives. PE foams are extensively used for under-hood insulation, door panels, trunk liners, and NVH (Noise, Vibration, and Harshness) management components.

The surge in electric vehicle (EV) production further amplifies this trend, as EV manufacturers require specialized foam materials for battery pack insulation and thermal management systems. According to the International Energy Agency (IEA), global EV sales surpassed 17 million units in 2024, directly boosting demand for high-performance PE foam applications in battery systems and lightweight vehicle interiors across North America, Europe, and Asia Pacific.

Market Restraints

Volatility in Crude Oil-Linked Raw Material Prices

PE foams are derived from polyethylene, a petroleum-based polymer, making them highly susceptible to fluctuations in crude oil prices. The U.S. Energy Information Administration (EIA) has documented significant crude oil price swings, with Brent crude ranging from approximately US$ 70 to US$ 95 per barrel during 2023-2024, directly impacting polyethylene resin procurement costs. Such price volatility creates margin pressure for foam manufacturers, particularly small and mid-sized players with limited hedging capabilities.

Unpredictable input costs complicate long-term contract pricing and deter new capacity investment, potentially slowing the market’s overall expansion trajectory. Feedstock cost uncertainty also limits the ability of regional producers in Asia Pacific and Latin America to compete on price against vertically integrated multinationals.

Environmental Regulations and Single-Use Plastic Restrictions

Growing environmental scrutiny over plastic waste is emerging as a significant headwind for conventional PE foam manufacturers. The European Union’s Single-Use Plastics Directive and analogous legislation across Asian economies are tightening regulations on foam-based packaging materials. The Ellen MacArthur Foundation estimates that less than 14% of plastic packaging is currently recycled globally, raising serious concerns about the accumulation of foam waste in landfills and oceans.

Regulatory restrictions and shifting consumer preferences toward bio-based or fully recyclable alternatives are mounting pressure on conventional PE foam producers to invest in sustainable product reformulation, compliance infrastructure, and lifecycle assessment capabilities, all of which add substantially to operational costs and require extended development timelines.

Market Opportunities

Energy-Efficient Building Construction and Green Infrastructure Development

The global transition toward energy-efficient infrastructure is creating a significant growth avenue for PE foam manufacturers. Owing to its exceptional thermal insulation performance, with conductivity levels reaching as low as 0.033 W/m·K, PE foam is well-suited for wall, roof, and underfloor insulation in contemporary green buildings.

The building sector accounts for nearly 36% of global energy consumption and 39% of CO2 emissions, prompting strong policy measures to accelerate the use of advanced insulation materials. Initiatives such as the European Green Deal and India’s National Action Plan on Climate Change (NAPCC) mandate higher efficiency standards for both new construction and retrofits. Additionally, rapid urbanization across the Asia Pacific and the Middle East, combined with certification programs such as LEED and BREEAM, is stimulating robust demand for PE-based insulation through 2033.

Medical-Grade PE Foams for Aging Population and Healthcare Expansion

The medical sector represents a rapidly expanding and high-value opportunity for PE foam manufacturers. Medical-grade PE foams, particularly cross-linked polyethylene (XLPE) variants, are increasingly utilized in orthopedic supports, prosthetic components, wound-care products, and patient-positioning systems. With the World Health Organization projecting the global population aged 65 and above to reach 1.5 billion by 2050, demand for advanced rehabilitation and orthopedic devices is expected to rise substantially.

Regulatory frameworks established by the U.S. FDA and the European Medicines Agency further encourage quality-driven investments, enabling premium pricing and reinforcing barriers to entry. Additionally, the ongoing expansion of healthcare infrastructure across emerging markets in Asia, Africa, and Latin America, supported by international health-financing institutions, continues to create sustained demand for cost-effective, high-performance medical foam solutions through 2033.

Category-wise Insights

Product Type Analysis

The Non-XLPE (Non-Cross-Linked Polyethylene Foam) segment currently maintains a dominant position in the Polyethylene (PE) Foams market, accounting for nearly 62% of total market share. This leadership is primarily driven by its lower production costs, ease of processing, and broad suitability across packaging and construction applications. Manufactured through physical or chemical blowing processes, Non-XLPE foams are well-suited for high-volume, cost-sensitive uses such as protective packaging liners, thermal insulation panels, and sports flooring.

According to the American Chemistry Council, polyethylene remains one of the most widely produced plastics globally, supporting a robust manufacturing base for Non-XLPE foams. Its adaptability in density customization and compatibility with mechanical recycling further reinforce its market strength, ensuring sustained dominance over the forecast period.

Density Analysis

The LDPE (Low-Density Polyethylene) foam segment maintains the leading position in the PE foams market by density, accounting for an estimated 68% share. Its dominance is attributable to superior flexibility, low weight, and strong cushioning performance, making it highly suitable for protective packaging, sports and recreational products, and medical device cushioning. As reported by Plastics Europe, low-density polyethylene represents a substantial portion of total polyethylene production across Europe, ensuring a stable and competitive supply base.

LDPE foam’s low water absorption and broad chemical resistance further enhance its suitability across diverse application environments. Additionally, its ease of fabrication, allowing cutting, laminating, and thermoforming, provides significant processing versatility, supporting large-scale adoption in automotive components, consumer electronics packaging, and construction applications, while HDPE foam gains traction in high-strength structural uses.

Application Analysis

Protective Packaging is the dominant application segment in the Polyethylene (PE) Foams market, accounting for an estimated 35% of total market revenue. The segment’s leadership is underpinned by the explosive growth of e-commerce, rising consumer electronics shipments, and the critical requirement for product safety during transit and storage. PE foam’s unique combination of shock absorption, moisture resistance, and lightweight properties makes it indispensable for packaging high-value goods, including electronics, automotive parts, medical instruments, and precision industrial components.

The World Trade Organization (WTO) has reported sustained growth in global merchandise trade volumes, directly correlating with expanding demand for protective packaging materials. Additionally, the accelerated growth of pharmaceutical exports and the post-COVID-19 surge in cold-chain logistics requirements have increased the use of PE foam packaging for temperature-sensitive medical products. Technological advances in foam lamination and die-cutting processes are enabling increasingly customized and efficient packaging solutions across diverse industries.

Regional Insights

North America Polyethylene (PE) Foams Trends

North America represents the most mature and technologically advanced market for Polyethylene (PE) Foams, with the United States accounting for the largest share of regional consumption. The region benefits from a highly developed end-use industry ecosystem encompassing major automotive OEMs, advanced packaging manufacturers, and an expansive construction sector. Annual U.S. construction spending exceeded US$2 trillion in 2023, supporting sustained demand for PE foam insulation, vapor barriers, and cushioning materials.

Regulatory frameworks established by the Environmental Protection Agency (EPA) and product standards set by ASTM International continue to drive quality improvements and technological advancement across the foam industry. Although geopolitical tensions such as U.S.-Iran conflicts have occasionally disrupted crude oil supply and influenced resin costs, robust domestic shale gas production and abundant ethane-derived ethylene provide a competitive feedstock advantage, while Canada’s expanding construction and automotive activities further strengthen regional demand.

Europe Polyethylene (PE) Foams Trends

Europe constitutes a substantial and innovation-oriented market for PE foams, with Germany, France, the United Kingdom, and Spain serving as key consumption centers. Germany’s advanced automotive manufacturing ecosystem, driven by leading OEMs such as BMW Group, Volkswagen AG, and Mercedes-Benz Group, continues to drive significant demand for PE foams for lightweighting and NVH applications. Europe produced more than 12 million passenger vehicles in 2023, underscoring the region’s sustained need for high-performance foam components.

Regulatory harmonization under the EU Green Deal and the Circular Economy Action Plan is encouraging manufacturers to adopt recyclable formulations and closed-loop systems. Although rising natural gas prices, driven by geopolitical tensions, have increased production costs, ongoing investments in bio-based and sustainable PE foam technologies by companies such as BASF SE and Recticel NV are helping producers maintain competitiveness while aligning with stringent regional environmental mandates.

Asia Pacific Polyethylene (PE) Foams Trends

Asia Pacific represents the fastest-growing regional market for Polyethylene (PE) Foams, driven by robust manufacturing expansion across China, India, Japan, and the broader ASEAN region. China remains the dominant contributor, supported by its extensive electronics, automotive, and packaging export industries, with continued industrial output growth sustaining strong demand for protective packaging and construction-grade PE foams. India is emerging as a particularly dynamic market, where the government’s Production-Linked Incentive (PLI) scheme for electronics and automotive manufacturing is driving increased use of PE foam in packaging and thermal insulation.

Although geopolitical developments, such as U.S.-Iran tensions impacting crude oil supply routes, have influenced feedstock costs for regional producers, Asia Pacific’s competitive manufacturing base, expanding middle-class population, and large-scale infrastructure programs continue to drive substantial demand. As a result, the region is firmly positioned as the primary global growth engine through 2033.

Competitive Landscape

The global Polyethylene (PE) Foams market is characterized by a moderately consolidated competitive landscape, comprising multinational chemical corporations and specialized foam manufacturers operating across product type, density, and application segments. Leading companies such as JSP Corporation, Armacell International, Dow Inc., Zotefoams PLC, and BASF SE leverage strong research capabilities, extensive production networks, and established customer relationships to maintain competitive advantages. Key differentiators include performance attributes, sustainability certifications, and tailored application solutions. Market growth is driven by strategic initiatives such as greenfield expansion in Asia Pacific, acquisitions, and co-development with automotive and electronics OEMs, alongside increasing emphasis on recycling and bio-based foam innovations.

Key Market Developments

- January 2024: JSP Corporation has acquired a 30% stake in the foam recycling business of General-Industries Deutschland GmbH, a leading European recycler of expanded polypropylene (EPP) and polyethylene (EPE) foams.

- October 2025: Armacell, a global leader in flexible foam for the equipment insulation market and a leading provider of engineered foams, officially inaugurated its newest manufacturing facility in Pune, India.

- November 2024: Dow announced the launch of a portfolio of low-carbon material solutions, which can help the footwear industry develop more sustainable products that offer the same high-performance results. The upgraded portfolio consists of bio-circular materials attributed under a mass balance approach, reversible cross-linking resins, post-consumer recycled resins, and polyolefin elastomers for artificial leather in various footwear materials and applications.

Top Companies in Polyethylene (PE) Foams

- JSP Corporation (Japan) is a globally recognized leader in the PE foams market, with a diversified product portfolio spanning expanded polyethylene, polypropylene, and polystyrene foam solutions. The company’s broad global manufacturing network spanning Asia, Europe, and North America, coupled with deep automotive OEM partnerships with major vehicle manufacturers, positions JSP as one of the most strategically influential and commercially dominant players in the global PE Foams market.

- Dow Inc. (U.S.) is one of the world’s largest chemical companies and a critical upstream supplier of high-purity polyethylene resins that underpin PE foam production. Through advanced materials science capabilities and a broad product portfolio that includes proprietary foam-enabling polymer technologies, Dow plays a pivotal role in accelerating material innovation across PE foam applications in protective packaging, building insulation, and automotive sectors, making it a central value chain influencer.

- Zotefoams PLC (U.K.) specializes in cellular materials manufactured through a proprietary high-pressure nitrogen foaming process that produces exceptionally uniform, high-purity closed-cell PE foams. The company’s differentiated AZOTE® and T-FIT® product lines serve highly demanding applications in aerospace, sports performance equipment, medical devices, and industrial insulation, enabling premium pricing and establishing Zotefoams as the dominant player in high-performance specialty PE foam segments globally.

Companies Covered in Polyethylene (PE) Foams Market

- JSP Corporation

- Armacell International

- Dow Inc.

- Zotefoams PLC

- Sealed Air Corporation

- BASF SE

- Recticel NV

- Inoac Corporation

- Thermotec Pty Ltd.

- Foam Products

- Dafa A/S

- Protac Inc.

- Sekisui Chemical Co., Ltd.

- UFP Technologies

- Toray Plastics (America), Inc.

Frequently Asked Questions

The global Polyethylene (PE) Foams market is valued at US$ 4.7 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, expanding at a compound annual growth rate (CAGR) of 5.5% over the 2026-2033 forecast period. Historically, the market grew at a CAGR of 4.9% between 2020 and 2025, underpinned by strong demand from protective packaging and automotive sectors.

The proliferation of electric vehicles, with global EV sales surpassing 17 million units in 2024 per the International Energy Agency (IEA), is strongly stimulating demand for specialized PE foam insulation in battery systems.

The Non-XLPE (Non-Cross-Linked Polyethylene Foam) segment leads the global market by product type, holding approximately 62% of total market share. Its dominance is driven by lower production costs, processing versatility, and broad applicability across high-volume, cost-sensitive end-uses such as standard protective packaging, construction insulation, and sports flooring, supported by an extensive global polyethylene resin supply infrastructure documented by the American Chemistry Council (ACC).

North America, led by the U.S., holds the leading position in the global Polyethylene (PE) Foams market. The region benefits from a mature end-use industrial base, with U.S. construction spending exceeding US$ 2 trillion annually per the U.S. Census Bureau, a large automotive manufacturing sector, and a well-developed e-commerce logistics infrastructure that collectively sustain robust and diversified demand for PE foam materials.

The development and commercialization of medical-grade XLPE foams represents the highest-value growth opportunity, driven by the global aging population trajectory projected by the World Health Organization (WHO) to reach 1.5 billion people aged 65 and above by 2050.

Key players include JSP Corporation, Armacell International, Dow Inc., Zotefoams PLC, Sealed Air Corporation, BASF SE, Recticel NV, Inoac Corporation, Thermotec Pty Ltd., Foam Products, Dafa A/S, and Protac Inc., among others. These companies compete on product performance, sustainability credentials, geographic reach, and application-specific customization capabilities.