- Communication Infrastructure & Services

- Parking Management Software Market

Parking Management Software Market Size, Share, and Growth Forecast, 2026 - 2033

Parking Management Software Market by Solution (Software [Standalone Software, Integrated Software], Services), Deployment (On-Premises, Cloud-Based / SaaS, Hybrid), End User (Commercial, Government, Transportation & Transit, Residential, Others), and Regional Analysis for 2026 - 2033

Parking Management Software Market Size and Trends

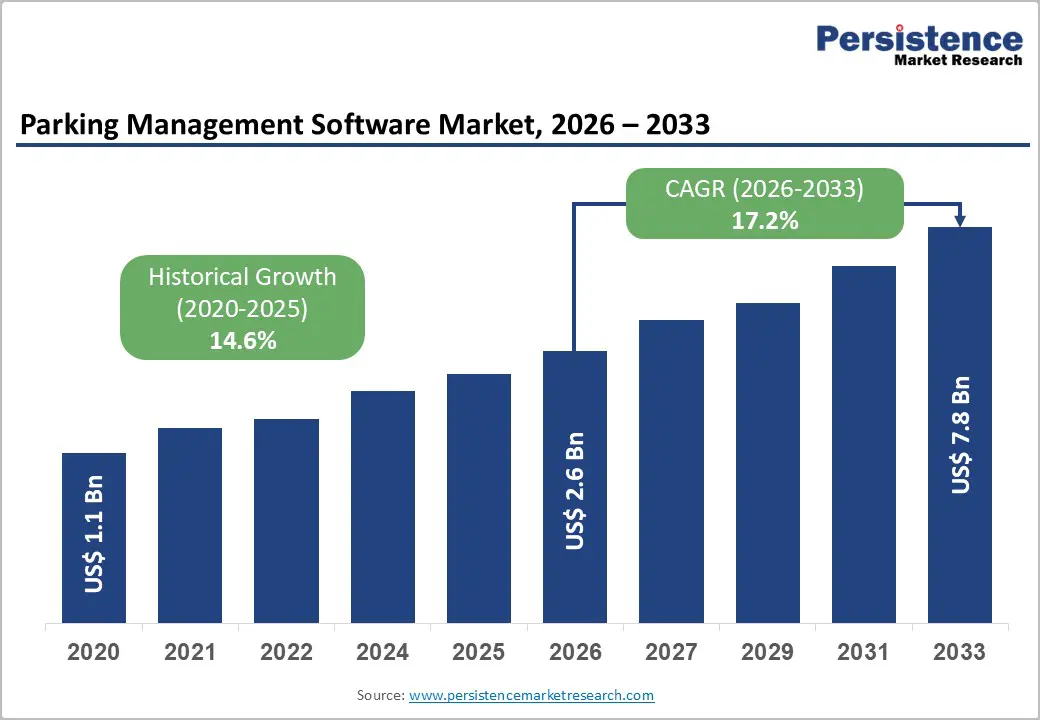

The global parking management software market size is projected to rise from US$2.6 Bn in 2026 to US$7.8 Bn by 2033. It is anticipated to witness a CAGR of 17.2% during the forecast period from 2026 to 2033, driven by accelerating urbanization, rising vehicle ownership, and expanding smart city initiatives, which are pushing cities and commercial operators to adopt intelligent, software-driven parking systems to tackle congestion and optimize space utilization. Integration of IoT, AI, mobile-based payments, and cloud hosting is transforming legacy parking operations into data-centric, contactless ecosystems that improve both user experience and revenue yield.

Key Industry Highlights:

- Leading Offering: Software dominates the market with over 71% share in 2026, valued at more than US$ 1.8 Bn, driven by rising demand for automation, real-time monitoring, AI-powered analytics, and integrated mobile payment platforms. Security & Surveillance leads within standalone software with over 24% share, supported by increasing deployment of LPR/ANPR-enabled enforcement and digital compliance systems. Services represent the fastest-growing segment, fueled by rising demand for system integration, consulting, and ongoing maintenance of IoT-enabled and cloud-based parking ecosystems.

- Leading Deployment: On-premises holds over 38% share in 2026, exceeding US$ 988 Mn, as municipalities and commercial operators prioritize data security, infrastructure control, and reliable system performance in high-traffic facilities. Cloud-Based / SaaS is the fastest-growing deployment at a 21.5% CAGR, driven by scalability, remote multi-site management, seamless updates, predictive analytics, and integration with mobile apps, IoT sensors, and automated enforcement platforms.

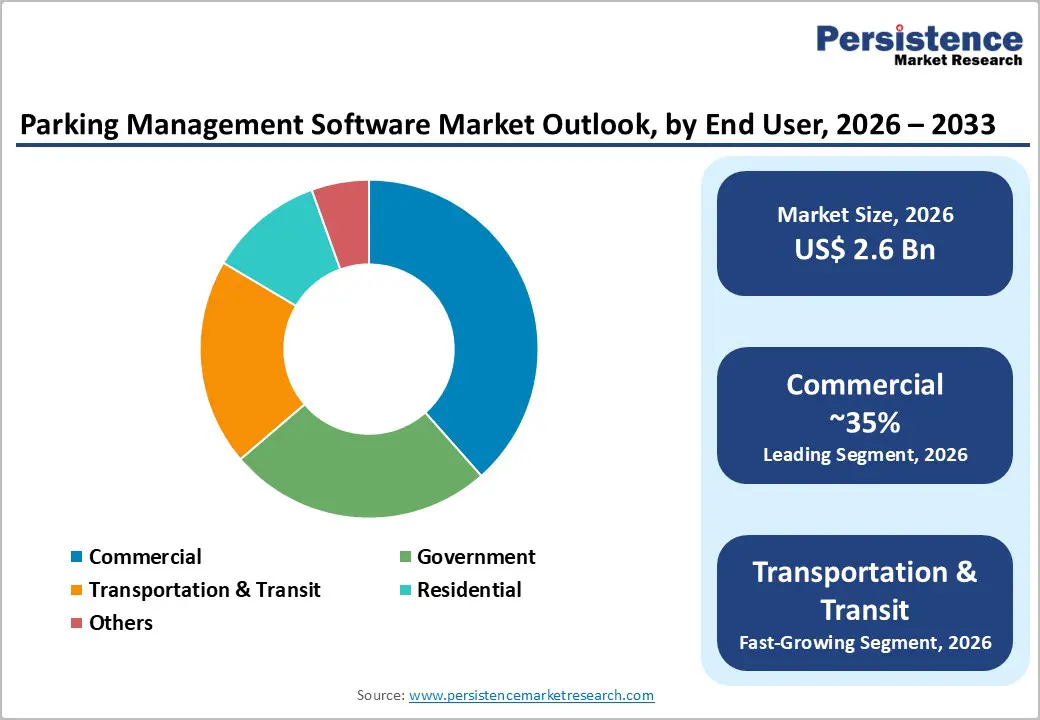

- Leading End-user: Commercial segment commands the largest share at over 35% in 2026, valued at more than US$ 910 Mn, supported by high vehicle volumes across malls, office complexes, retail centers, and mixed-use developments. Transportation & Transit is the fastest-growing segment at a 20.9% CAGR, propelled by rising congestion in airports, metro hubs, and bus terminals, and the need for LPR-integrated, real-time parking optimization systems.

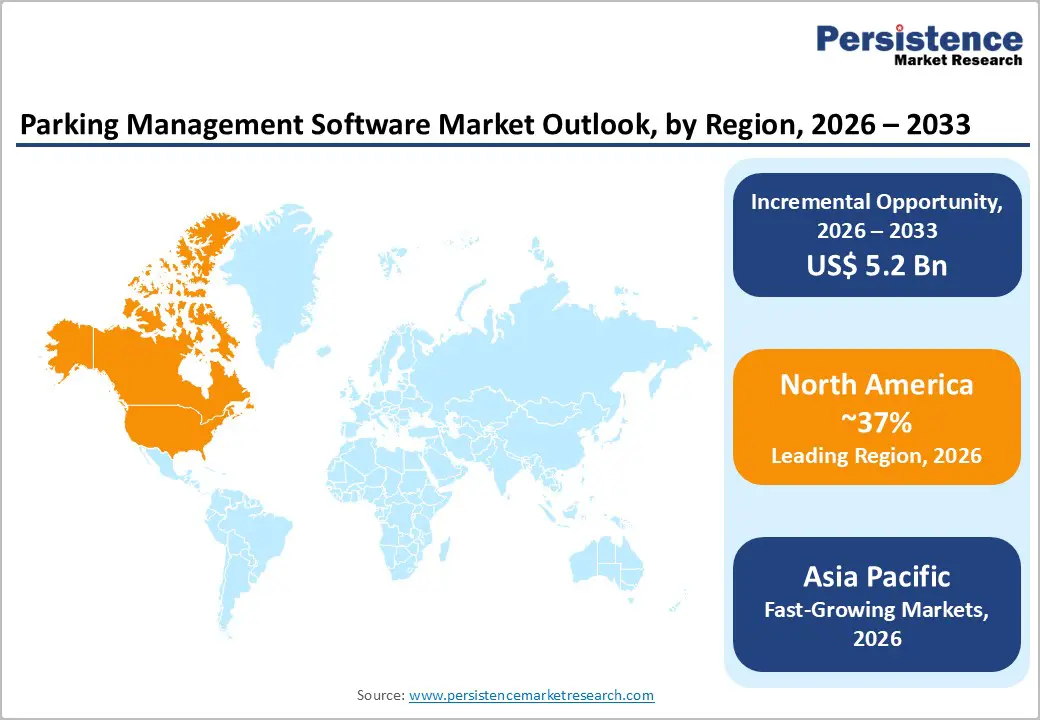

- Leading Region: North America leads with over 37% share in 2026, reaching approximately US$ 962 Mn, supported by early digital adoption, strong smart city initiatives, regulatory support for traffic optimization, and advanced IoT-enabled deployments. Asia Pacific is the fastest-growing region at a 22.1% CAGR, driven by rapid urbanization, government-backed smart city programs in China and India, expanding mobile payment ecosystems, and increasing deployment of AI-enabled and sensor-based parking infrastructure.

| Key Insights | Details |

|---|---|

| Parking Management Software Market Size (2026E) | US$2.6 Bn |

| Market Value Forecast (2033F) | US$7.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 14.6% |

Market Dynamics

Driver - Urbanization and Rising Vehicle Ownership Driving Demand

Rapid urbanization and rising vehicle ownership are intensifying parking shortages and congestion, pushing cities to adopt advanced parking management software for space optimization and traffic control. The United Nations projects that over 60% of the global population will live in urban areas by 2030, increasing infrastructure strain. Studies show 15-30% of traffic in dense cities results from drivers searching for parking, contributing to emissions and fuel waste. Cities across Europe and major U.S. metros are deploying zone-based pricing, real-time monitoring, and digital enforcement systems solutions that depend on integrated, AI-enabled parking software platforms to meet sustainability and congestion-reduction goals.

Rising Demand for Frictionless and Contactless Parking Experiences

The demand for frictionless and contactless parking is accelerating as drivers increasingly prefer seamless entry, real-time space guidance, and mobile-first payments over cash or ticket-based systems. App-based, QR/NFC, and license plate recognition (LPR/ANPR)-enabled solutions reduce wait times and eliminate physical touchpoints, improving user convenience and compliance. Operators are deploying cloud-based platforms integrating mobile apps, remote session management, and automated enforcement. This shift lowers cash-handling and hardware maintenance costs while minimizing revenue leakage and unpaid parking. As contactless parking becomes standard across retail centers, airports, stadiums, and municipal zones, software-driven, mobile-centric systems are witnessing sustained global demand.

Restraint - Fragmented Regulatory Landscape and Interoperability Gaps

Fragmented regulations across regions, despite EU interoperability directives and North American ITS frameworks, often require vendors to customize platforms to meet local payment rails, enforcement rules, and data-sharing mandates, thereby increasing costs and slowing SaaS scalability. Interoperability gaps between parking systems, traffic management platforms, and public transit ticketing limit integrated mobility offerings. For instance, in several European and Asian cities, parking apps remain disconnected from public transit fare systems, reducing user convenience and overall ecosystem value. Regulatory divergence and system incompatibility remain structural growth constraints.

High Upfront Investment and Legacy Infrastructure Lock-in

High upfront CAPEX for replacing legacy PARCS hardware, outdated ticketing kiosks, and manual enforcement systems creates significant financial barriers, especially for municipalities operating under fixed annual budget cycles and lengthy procurement processes. Integration challenges with legacy electromechanical infrastructure increase retrofit costs and extend deployment timelines, particularly in older public garages. Concerns around cybersecurity, data privacy regulations, SLA reliability, and vendor lock-in make operators cautious about fully migrating to centralized cloud platforms, leading many to prefer phased or hybrid deployments. These combined financial, technical, and governance constraints disproportionately slow adoption in smaller cities and developing markets with limited institutional and fiscal capacity.

Opportunity - Data-Monetization and Mobility-as-a-Service (MaaS) Partnerships

Parking platforms are increasingly evolving into data-rich mobility nodes, generating actionable datasets such as real-time occupancy, dwell time, turnover rates, and digital payment patterns. Cities like Los Angeles and Barcelona already leverage parking sensor data to optimize traffic flows and curb utilization, demonstrating how anonymized analytics support congestion management and transit planning. Integration with MaaS ecosystems and ride-hailing platforms such as Uber Technologies Inc. enables real-time parking availability feeds within routing engines, reducing last-mile inefficiencies. Vendors offering open APIs, real-time pricing layers, and fleet-parking modules can therefore shift from transactional parking software providers to high-margin urban mobility data partners through API licensing and analytics monetization.

Smart Parking Kiosks Enhancing Revenue Streams

The emergence of smart parking kiosks integrated with cloud-based Parking Management Software and PARCS (Parking Access and Revenue Control Systems) enables multi-modal payments, improving compliance rates and reducing revenue leakage. Digital kiosks connected to License Plate Recognition (LPR/ANPR) and real-time monitoring systems enhance enforcement efficiency and audit transparency, directly boosting operator revenue. Touchscreen interfaces support dynamic pricing, location-based advertising, and partnerships with nearby retailers or events, creating ancillary revenue streams. For example, cities such as New York City and Chicago have deployed smart pay-and-display kiosks integrated with mobile apps to increase payment compliance and optimize curbside revenue collection.

Category-wise Analysis

Solution Insights

Software dominates the global market, capturing more than 71% market share in 2026 with a value exceeding US$ 1.8 Bn, as it addresses the growing need for efficiency, automation, and real-time control in parking operations. It helps to optimize space usage, reduce congestion, and ensure seamless vehicle flow. Integration with mobile payment apps and automated enforcement enhances convenience for both operators and users. Advanced analytics and AI further support demand forecasting, revenue management, and improved user experience, making software the central component of modern parking systems. Among standalone software, Security and Surveillance holds over 24% share in 2026.

Services demonstrate a significant growth rate due to organizations increasingly needing customized system integration, ongoing support, and maintenance to ensure the smooth operation of complex parking solutions. As urban areas and commercial spaces adopt IoT sensors, automated enforcement, and real-time analytics, continuous technical assistance and consulting become essential. Businesses also require expert guidance for upgrades, compliance, and optimization, driving higher demand for professional services.

Deployment Insights

On-premises hold over 38% market share in 2026, with a value exceeding US$ 988 Mn, as organizations prioritize data security and control over sensitive parking and revenue information. They often require customized integration with existing infrastructure, such as access control and payment systems. On-premises setups ensure reliable performance without depending on network stability, which is crucial for high-traffic facilities. The ability to manage updates and maintenance internally also aligns with operational and compliance needs.

Cloud-Based / SaaS is expected to grow at the highest rate, with a CAGR of 21.5%, as they address the increasing need for flexibility, scalability, and remote management. Operators monitor multiple parking sites in real-time, optimize space usage, and update systems without on-site interventions. Integration with mobile payment apps, IoT sensors, and automated enforcement also enhances user convenience and operational efficiency. Predictive analytics and data-driven decision-making help reduce congestion and maximize revenue, meeting the demand for smarter, more connected parking solutions.

End-user Insights

Commercial commands the largest market share at over 35% in 2026, with a value exceeding US$ 910 Mn, due to businesses such as shopping malls, office complexes, and retail centers face high vehicle volumes and require efficient parking solutions. Commercial operators prioritize revenue optimization, capacity utilization, and customer-experience enhancements, all of which are directly addressed by parking management software featuring dynamic pricing, reservation slots, loyalty programs, and multi-channel payment processing. In high-footfall commercial hubs, operators report measurable improvements in turnover rates and revenue per bay after deploying software-driven parking systems, which reinforces demand in this segment.

Transportation & Transit are expected to grow at a CAGR of 20.9% due to the increasing demand for efficient traffic flow and seamless parking solutions in urban transit hubs. Integration with License Plate Recognition (LPR/ANPR) and real-time analytics helps reduce congestion and improve the commuter experience. Operators require automated systems to manage high vehicle volumes, optimize space utilization, and enable faster payment processing. The growing adoption of mobile payment apps and digital enforcement further supports smoother operations in airports, metro stations, and bus terminals.

Regional Insights

North America Parking Management Software Market Trends

North America holds over 37% share in 2026, reaching US$ 962 Mn value, due to early adoption of advanced digital technologies and strong smart city initiatives. The region benefits from a favorable regulatory framework that encourages traffic optimization, emissions reduction, and data-driven urban planning. Integration of parking systems with public transit networks and real-time guidance platforms enhances mobility management and improves user convenience. A mature innovation ecosystem supported by venture funding, technology partnerships, and municipal digital transformation programs accelerates the deployment of analytics-driven and IoT-enabled parking solutions.

Asia Pacific Parking Management Software Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 22.1%, driven by rapid urbanization across China, India, and ASEAN countries. Government-backed smart city programs are accelerating deployment of IoT-enabled parking systems, AI-powered analytics, and LPR/ANPR-based enforcement technologies. China’s digital mobility investments and India’s Smart Cities Mission are strengthening automated compliance and revenue management frameworks. Strong regional manufacturing capabilities and rising mobile payment adoption in cities such as Shanghai, Delhi, and Singapore are enhancing cost efficiency and commuter experience.

Europe Parking Management Software Market Trends

Europe is expected to hold more than 23% share by 2026, supported by strong smart city investments and regulatory harmonization across the EU. Unified standards promote interoperable parking platforms, enabling scalable and cross-border deployment. Sustainability goals are accelerating the adoption of AI-driven analytics and sensor-based guidance systems to reduce congestion and emissions. In Germany and the United Kingdom, growing smart mobility initiatives and EV adoption are increasing demand for integrated, cashless, and EV-enabled parking management solutions.

Competitive Landscape

The parking management software market exhibits a moderately fragmented competitive landscape, with both global technology firms and regionally specialized providers competing for market share. Companies are expanding their solution portfolios, investing in R&D for AI and analytics capabilities, forging partnerships with municipal authorities, and focusing on interoperability across hardware and software ecosystems. Providers differentiate themselves through advanced features such as real-time analytics, seamless mobile payments, and integrated enforcement functionalities, while emerging business models emphasize subscription-based deployments and platform-as-a-service offerings.

Key Industry Developments

- In January 2026, HUB Parking Technology announced the global launch of a new multi-purpose self-service parking kiosk designed to go beyond traditional payment functions. The solution supports ticketed and ticketless payments, subscription renewals, voucher validation, retail purchases, and targeted digital content, while enabling integration with third-party systems such as indoor navigation, transportation services, and entertainment ticketing across airports, hotels, and shopping centers.

- In November 2025, ParkMobile is expanding reservation services to around 8,000 new off-street parking locations nationwide through a strategic partnership with Flash. The rollout, covering major cities like New York City, Los Angeles, Chicago, and Atlanta, aims to enhance real-time parking reservations and digital payments, with full nationwide implementation.

Companies Covered in Parking Management Software Market

- SKIDATA GmbH

- Amano McGann

- ParkMobile

- T2 Systems, Inc.

- FlashParking, Inc.

- Flowbird Group

- SWARCO AG

- Robert Bosch GmbH

- Scheidt & Bachmann

- Passport Labs, Inc.

- Get My Parking

- Kapsch TrafficCom AG

- Others

Frequently Asked Questions

The global market is projected to be valued at US$2.6 Bn in 2026.

The need for efficient space utilization, reduced congestion, and seamless vehicle flow in urban and commercial areas are key driver of the market.

The market is expected to witness a CAGR of 17.2% from 2026 to 2033.

Rapid adoption of AI-powered analytics, IoT-enabled smart parking, and mobile payment integration that enhance operational efficiency and user convenience is creating strong growth opportunities.

SKIDATA GmbH, Amano McGann, ParkMobile, T2 Systems, Inc., FlashParking, Inc., Flowbird Group, SWARCO AG, and Robert Bosch GmbH are among the leading key players.