- Non-food Packaging

- Packaging Coatings Market

Packaging Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Packaging Coatings Market by Resin Type (Epoxy, Acrylics, Others), Coating Technology (Water-based, UV-curable, Others), Packaging Type, End-use Industry, and Regional Analysis for 2026 - 2033

Packaging Coatings Market Size and Trends Analysis

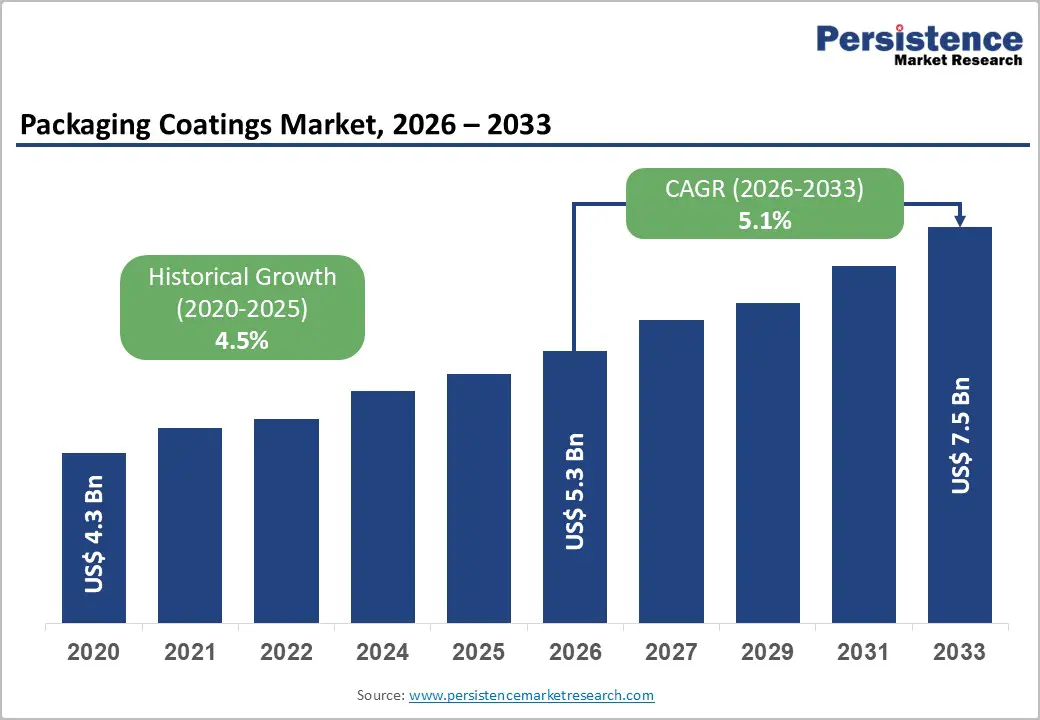

The global packaging coatings market size is likely to be valued at US$5.3 billion in 2026 and is expected to reach US$7.5 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033, driven by stricter regulatory compliance requirements, rapid substitution of BPA-based chemistries, and increasing adoption of recyclable and low-migration coating systems.

While food and beverage packaging remains the dominant demand base, future growth will be supported by healthcare packaging, paper-based substrates, and flexible packaging formats requiring high-performance barrier solutions.

Key Industry Highlights:

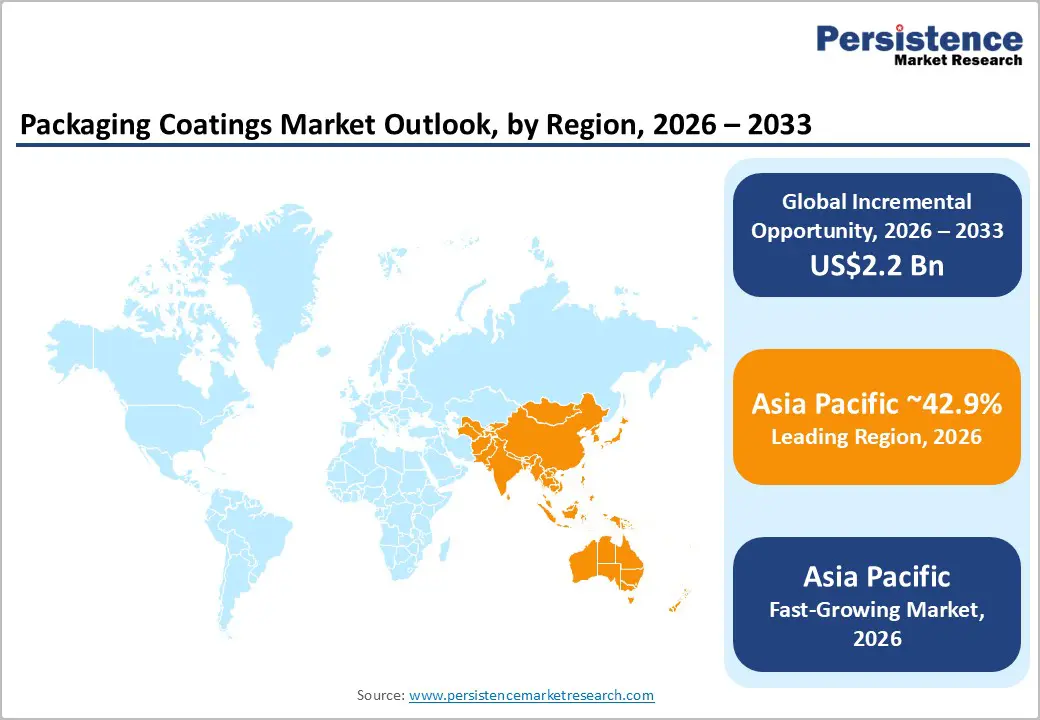

- Leading Region: Asia Pacific is projected to hold the dominant position with 42.9% market share, driven by strong manufacturing capabilities and high demand for packaged goods.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid urbanization, expanding food processing industries, and rising adoption of sustainable packaging solutions.

- Investment Plans: Major players such as AkzoNobel and PPG Industries are investing in BPA-free and sustainable coating technologies, along with regional capacity expansion in Asia, with over 30-40% of new investments directed toward sustainable and compliant solutions.

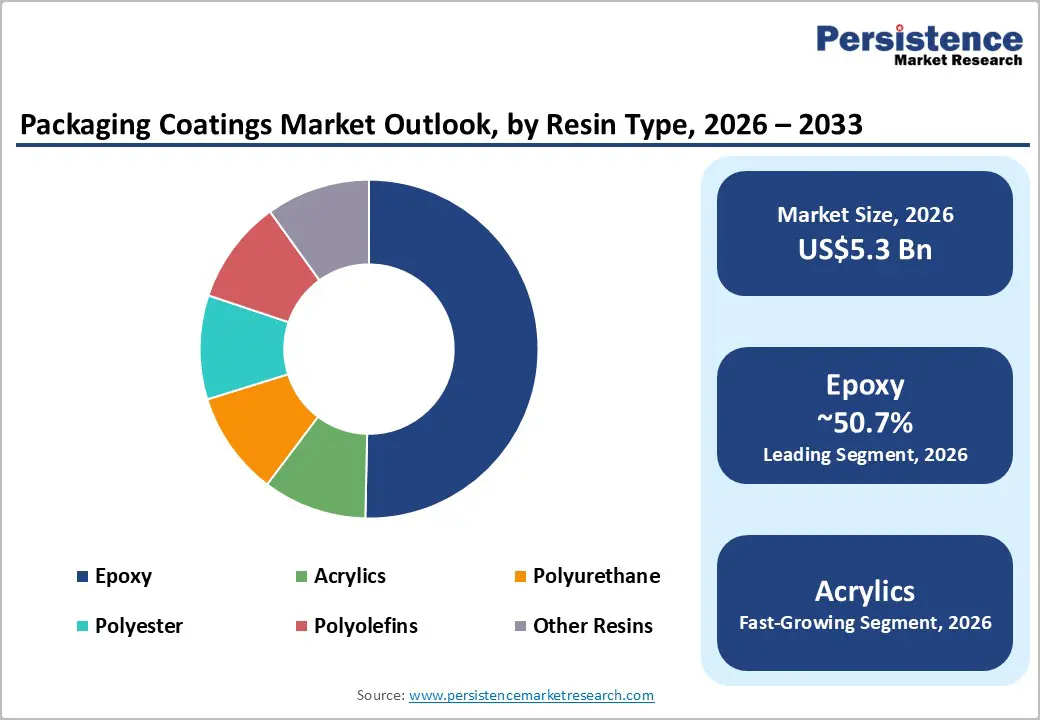

- Dominant Resin Type: Epoxy resins are anticipated to lead with a 50.7% market share, driven by their extensive use in metal packaging applications such as food and beverage cans.

- Leading Coating Technology: Water-based coatings dominate the technology segment with a 43.6% market share, supported by increasing regulatory pressure and demand for low-VOC, environmentally friendly solutions.

| Key Insights | Details |

|---|---|

| Packaging Coatings Market Size (2026E) | US$5.3 Bn |

| Market Value Forecast (2033F) | US$7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Transition Away From BPA-Based Coatings Is Accelerating Reformulation Demand

Global regulatory frameworks are fundamentally reshaping the packaging coatings landscape. The European Union’s ban on bisphenol A (BPA) in food-contact materials, combined with stringent U.S. food safety regulations, has created a structural shift toward BPA-NI (non-intent) coatings and low-migration chemistries. These regulations extend beyond coatings to inks, adhesives, and substrates, forcing manufacturers to redesign entire packaging systems rather than implement incremental upgrades. As a result, compliance has become a core purchasing criterion for brand owners and converters. Leading suppliers are actively expanding BPA-free and PFAS-free portfolios to align with these requirements, accelerating product innovation cycles and increasing demand for next-generation coating solutions across metal, paper, and flexible packaging.

Sustainability Regulations Are Driving Demand for Recyclable and Fiber-Based Coating Solutions

Environmental policies aimed at reducing packaging waste and improving circularity are significantly influencing coating technology adoption. Regulations promoting recyclability and reduced plastic usage are encouraging the transition toward fiber-based packaging and sustainable barrier coatings. This shift has increased demand for coatings that enable recyclability, repulpability, compostability, and reduced environmental impact without compromising performance. Manufacturers are developing water-based and bio-based barrier coatings that support paperboard, cupstock, and takeaway packaging applications. These innovations are transforming coatings from purely protective layers into functional enablers of circular packaging systems, creating new growth avenues in sustainable packaging formats.

Advancements in Water-Based and UV-Curable Technologies are Enhancing Efficiency and Compliance

Technological innovation in coating formulations is improving both environmental performance and production efficiency. Water-based coatings are gaining traction due to their low VOC emissions and compatibility with sustainability targets, while UV-curable coatings offer rapid curing, reduced energy consumption, and high throughput. These technologies allow converters to maintain high production speeds while meeting stringent regulatory and environmental requirements. The ability to balance performance characteristics such as adhesion, barrier protection, and printability with compliance and efficiency is making advanced coating technologies a key differentiator. As a result, manufacturers are increasingly investing in R&D to develop multifunctional coatings that align with evolving industry demands.

Barrier Analysis - Regulatory Complexity and Long Qualification Cycles Increase Time-To-Market

Packaging coatings must meet stringent food-contact regulations, migration limits, and performance standards across multiple jurisdictions. Each formulation requires extensive testing, certification, and approval from regulatory authorities and end users, particularly in sensitive applications such as beverage cans and pharmaceutical packaging. This leads to prolonged product development and qualification cycles, delaying commercialization and increasing operational costs. The need to validate coatings across various substrates and processing conditions further complicates deployment, making regulatory compliance a significant barrier to rapid innovation.

Rising Formulation Costs and Raw Material Dependencies Impact Profitability

The transition away from legacy chemistries such as BPA-based epoxy systems requires the development of alternative resin systems and additives. These new formulations often involve higher costs due to complex raw material requirements and additional processing steps. Maintaining performance characteristics such as corrosion resistance, shelf-life stability, and chemical durability while reducing environmental impact increases formulation complexity. This creates pricing pressure, particularly in cost-sensitive markets, and may limit adoption among smaller converters or emerging economies.

Opportunity Analysis - Asia Pacific and India Present Strong Volume-Driven Growth Potential

The Asia Pacific region offers significant growth opportunities due to its large population base, expanding manufacturing sector, and increasing consumption of packaged goods. Countries such as China, India, Japan, and those in Southeast Asia are experiencing rapid urbanization and rising demand for processed and packaged food products. India, in particular, has emerged as a major packaging market, supported by growth in the food processing and retail sectors. This creates substantial demand for packaging coatings across rigid and flexible formats. Local production capabilities and cost advantages further enhance the region’s attractiveness for both global and regional coating manufacturers.

Paper-Based Packaging and Barrier Innovation Offer High-Value Opportunities

The shift toward sustainable packaging solutions is driving demand for advanced barrier coatings for paper and fiber-based substrates. These coatings must provide resistance to moisture, grease, oxygen, and heat while maintaining recyclability and compostability. This creates opportunities for innovation in bio-based and water-based coating systems. Applications such as food containers, takeaway packaging, and dry food pouches are particularly promising. Companies that can deliver high-performance coatings compatible with circular economy requirements are likely to capture premium market segments and establish long-term competitive advantages.

Category-wise Analysis

Resin Type Insights

Epoxy resins dominate the packaging coatings market, anticipated to hold 50.7% market share in 2026, due to their superior chemical resistance, strong adhesion, and long-term durability, making them indispensable in high-performance applications. They are extensively used in metal packaging, particularly in food and beverage cans, caps, and closures, where maintaining product integrity and preventing contamination is critical. Epoxy coatings provide excellent resistance to corrosion, sterilization processes, and aggressive food contents such as acidic or high-salt products. Despite regulatory pressure on BPA-based systems, epoxy coatings continue to maintain their leadership due to the installed base of metal packaging infrastructure and proven reliability. Manufacturers are increasingly transitioning toward BPA-NI (non-intent) epoxy formulations, especially for beverage can linings and food-contact applications. For example, beverage can manufacturers are adopting BPA-free epoxy alternatives that deliver equivalent barrier performance while complying with evolving global regulations. This balance between performance retention and regulatory compliance ensures epoxies remain structurally dominant in the near term.

Acrylic resins are emerging as the fastest-growing segment, due to their formulation flexibility, environmental compatibility, and strong regulatory alignment. They offer excellent clarity, flexibility, UV resistance, and weatherability, making them suitable for both protective and decorative coatings across rigid and flexible packaging formats. Acrylics are particularly well-suited for water-based and low-migration coating systems, which are increasingly preferred in food-contact and consumer packaging applications. Their growth is further supported by the shift toward sustainable and non-toxic materials, as acrylic systems can be engineered to meet stringent food safety and environmental standards without relying on restricted substances. For instance, acrylic-based coatings are widely used in beverage overprint varnishes, flexible packaging films, and paper-based packaging, where visual appeal and compliance are equally important. As packaging formats diversify and sustainability expectations rise, acrylics are expected to gain significant traction as a next-generation resin platform.

Coating Technology Insights

Water-based coatings leads, anticipated to hold 43.6% market share in 2026, due to their low environmental impact, reduced VOC emissions, and strong alignment with global sustainability regulations. These coatings are widely used across food packaging, paperboard, corrugated materials, and flexible packaging, where regulatory compliance and environmental performance are critical. They provide effective barrier properties such as resistance to moisture, grease, and oxygen while maintaining compatibility with recycling processes. The segment’s dominance is also driven by increasing adoption in fiber-based and paper packaging applications, where water-based coatings act as sustainable alternatives to plastic laminates. For example, water-based barrier coatings are commonly used in takeaway food containers, cupstock, and folding cartons, enabling recyclability while maintaining product protection. Their ease of application, cost-effectiveness, and compatibility with existing coating lines further strengthen their position as the preferred technology for large-scale packaging operations.

UV-curable coatings represent the fastest-growing technology segment due to their rapid curing speed, energy efficiency, and superior surface performance. These coatings cure instantly under ultraviolet light, enabling high-speed production lines and reduced energy consumption compared to conventional thermal curing methods. They deliver excellent properties such as scratch resistance, gloss retention, and chemical stability, making them ideal for high-quality packaging applications. Their adoption is particularly strong in printing and decorative packaging, including labels, flexible films, and premium consumer packaging, where aesthetics and durability are critical. UV-curable coatings are also increasingly designed to meet low-migration requirements, making them suitable for indirect food-contact applications. For instance, UV coatings are widely used in high-end beverage labels, cosmetic packaging, and specialty cartons, where both visual appeal and regulatory compliance are essential. As converters seek faster, cleaner, and more efficient production processes, UV-curable technologies are expected to witness sustained growth.

Regional Insights

North America Packaging Coatings Market Trends - Regulatory-Driven Innovation & Premium Compliance Demand

North America represents a mature yet high-value market characterized by strong regulatory oversight and advanced manufacturing capabilities. The U.S. leads the region, supported by a well-established food and beverage industry and stringent food safety regulations enforced by agencies such as the U.S. Food and Drug Administration. Regulatory frameworks emphasize compliance with food-contact standards, driving demand for BPA-free, PFAS-free, and low-migration coatings across metal and flexible packaging applications.

Innovation remains a key growth driver, with major players such as PPG Industries and Eastman Chemical Company investing in advanced coating technologies. For instance, PPG’s expansion of BPA-NI beverage can coatings has strengthened supply for major beverage brands transitioning away from legacy chemistries. Similarly, Eastman’s collaboration on compostable and biobased coating solutions is supporting the shift toward sustainable paper packaging in North America. Brand owners such as Coca-Cola and PepsiCo are also actively adopting recyclable and compliant packaging formats, indirectly accelerating coating innovation. While overall volume growth is moderate compared to emerging regions, the market benefits from high value per unit, premium product demand, and strong innovation ecosystems.

Europe Packaging Coatings Market Trends - Sustainability Regulations Fueling Advanced Coating Technologies

Europe is a key market driven by regulatory harmonization and aggressive sustainability initiatives. Policies introduced by the European Commission, including restrictions on hazardous substances and circular economy mandates, are accelerating the transition toward recyclable, low-migration, and environmentally compliant coatings. Countries such as Germany, the U.K., France, and Spain are at the forefront of adopting sustainable packaging solutions, particularly in the food, beverage, and personal care sectors.

European manufacturers are responding with targeted investments in innovation and production. For example, AkzoNobel has expanded BPA-free coating production capabilities, including new lines in Asia to serve global demand while maintaining strong R&D operations in Europe. Siegwerk Druckfarben AG & Co. KGaA and allnex are advancing low-migration and UV-curable technologies tailored for European compliance standards. Meanwhile, Henkel is strengthening its packaging coatings portfolio for pharmaceutical and food applications, reflecting rising demand for high-performance and compliant solutions. These developments highlight how Europe’s regulatory environment is not only enforcing compliance but also driving technological leadership and long-term market transformation.

Asia Pacific Packaging Coatings Market Trends - High-Growth Manufacturing Hub with Expanding Sustainable Solutions

Asia Pacific is the largest and fastest-growing region, holding 42.9% market share in 2026, supported by rapid industrialization, urbanization, and increasing consumption of packaged goods. Key markets such as China, India, Japan, and Southeast Asian economies are driving strong demand across both rigid and flexible packaging formats. The region benefits from cost-effective manufacturing, expanding middle-class populations, and robust supply chain ecosystems, making it a global hub for packaging production.

Recent developments underscore the region’s growing importance. AkzoNobel launched its first BPA-free can coating production line in Asia, enabling localized supply for beverage and food packaging manufacturers transitioning to compliant chemistries. DIC Corporation continues to expand its water-based barrier coating portfolio across Asia, supporting demand for sustainable packaging in paper and flexible applications. In India, UFlex Limited is investing in advanced coating and flexible packaging solutions to meet rising domestic and export demand. Global consumer brands such as Nestlé and Unilever are also increasing their focus on recyclable and sustainable packaging in the region, further accelerating adoption of advanced coatings.

These developments demonstrate that Asia Pacific is not only a volume-driven market but also a rapidly evolving innovation and production center, making it the primary growth engine for the packaging coatings industry.

Competitive Landscape

The global packaging coatings market is moderately consolidated, with a few global players dominating high-value segments while numerous regional and local manufacturers operate in niche markets. Leading companies maintain competitive advantages through technological expertise, regulatory compliance capabilities, and strong customer relationships. The market remains competitive, with continuous innovation and product differentiation driving growth.

Key strategies include sustainability-driven innovation, regulatory compliance, and regional expansion. Companies are focusing on developing eco-friendly coatings, expanding production capabilities in emerging markets, and strengthening partnerships to enhance market presence.

Key Industry Developments:

- In July 2025, PPG Industries expanded its INNOVEL and iSENSE coating portfolio with new BPA-NI beverage can end coatings, aiming to enhance performance while meeting evolving global regulatory standards.

- In May 2025, AkzoNobel highlighted industry-wide innovation trends including PFAS phase-out, BPA substitution, and advanced sustainable coating technologies, reinforcing its strategic focus on environmentally compliant packaging solutions.

Companies Covered in Packaging Coatings Market

- AkzoNobel

- PPG Industries

- Sherwin-Williams

- Axalta Coating Systems

- Kansai Paint

- Nippon Paint Holdings

- Jotun

- Beckers Group

- Siegwerk Druckfarben AG & Co. KGaA

- DIC Corporation

- allnex

- Covestro

- Eastman Chemical Company

- Henkel

- ALTANA AG

- Wacker Chemie AG

Frequently Asked Questions

The global packaging coatings market is estimated to be valued at US$5.3 billion in 2026.

The packaging coatings market is projected to reach US$7.5 billion by 2033.

Key trends shaping the market include a shift toward BPA-free and low-migration coatings driven by stringent food-contact regulations and the rising adoption of water-based and UV-curable technologies for sustainability and efficiency.

The epoxy resin segment leads the market, accounting for 50.7% share, primarily due to its extensive use in metal packaging applications such as food and beverage cans.

The packaging coatings market is expected to grow at a CAGR of 5.1% from 2026 to 2033.

Some of the major players include AkzoNobel, PPG Industries, Siegwerk Druckfarben AG & Co. KGaA, DIC Corporation, and Henkel.