- Healthcare Services

- Oncology Clinical Trials Market

Oncology Clinical Trials Market Size, Share, and Growth Forecast 2026 - 2033

Oncology Clinical Trials Market by Phase (Phase I, II, III, IV), Study Design (Interventional Studies, Observational Studies, Expanded Access Studies), Cancer Type (Lung Cancer, Breast Cancer), and Regional Analysis, 2026 - 2033

Oncology Clinical Trials Market Size and Trends Analysis

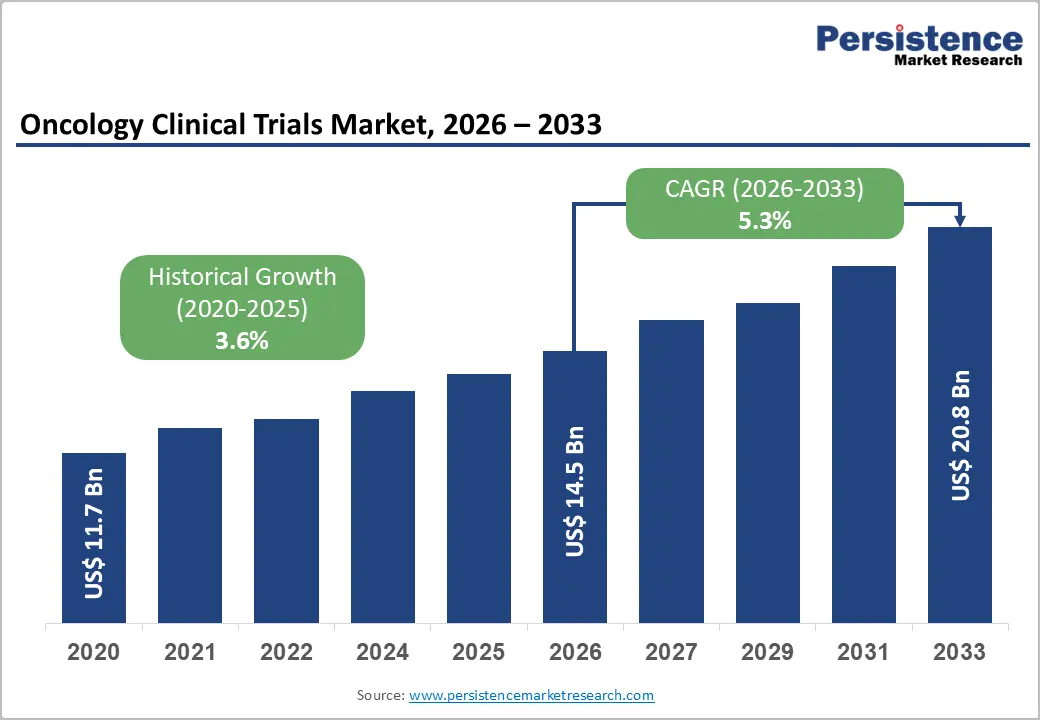

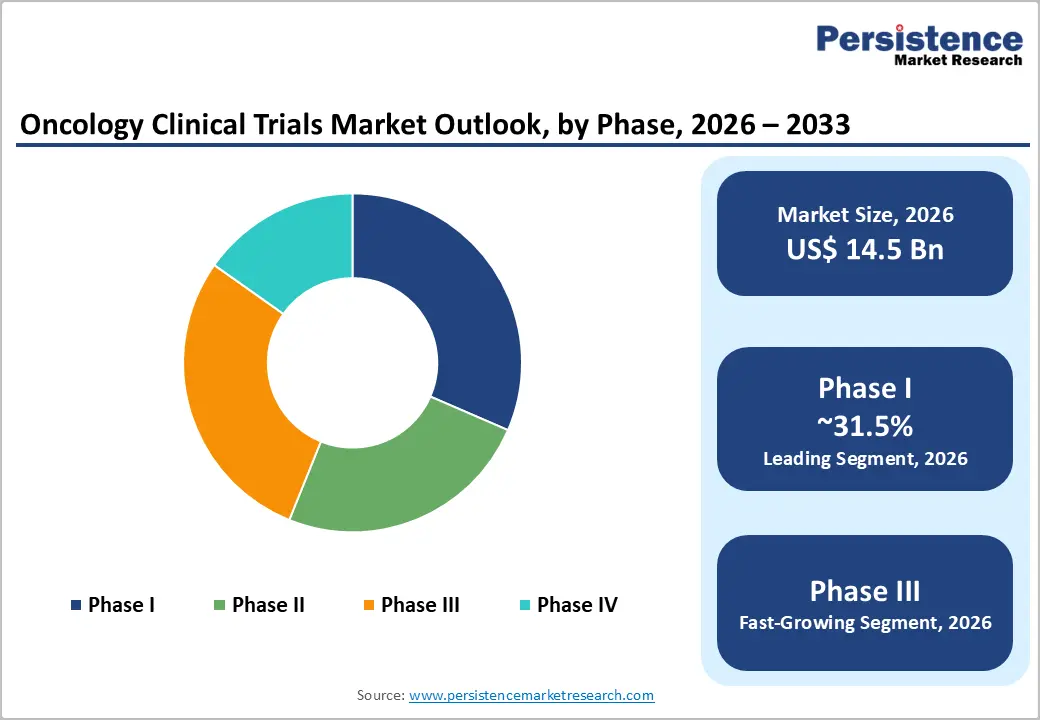

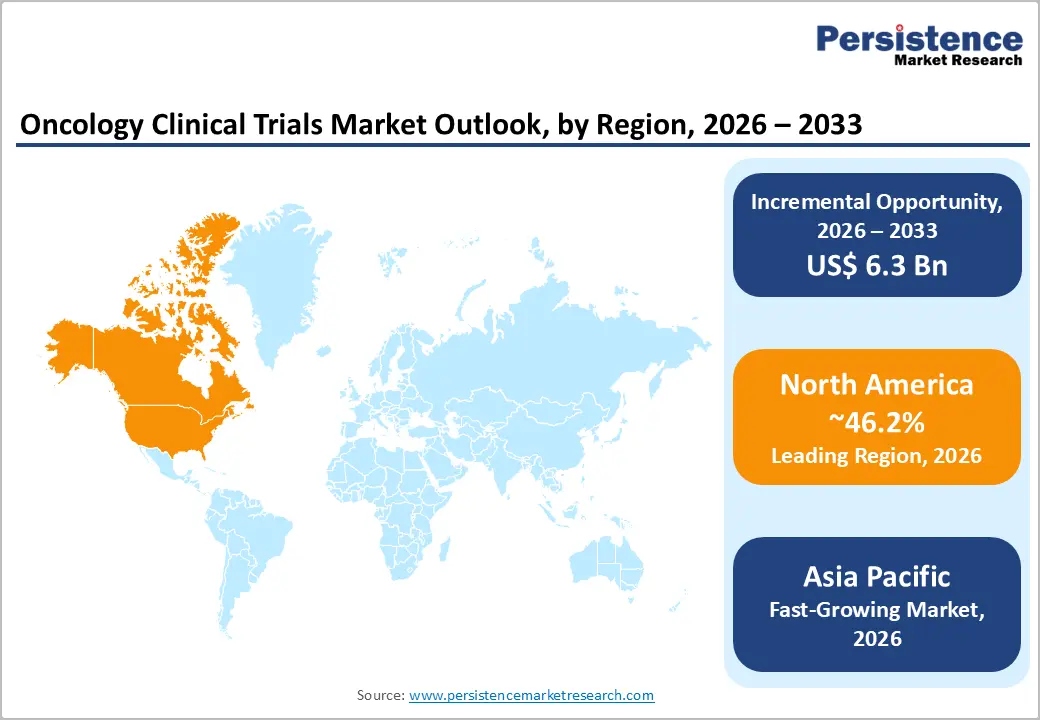

The global oncology clinical trials market size is expected to be valued at US$14.5 billion in 2026 and is predicted to reach US$20.8 billion by 2033, surging at a CAGR of 5.3% between 2026 and 2033, driven by the ongoing shift toward precision medicine, which is allowing trials to target specific mutations rather than broad tumor types. Regulatory agencies are also accelerating approvals for high-need therapies, encouraging sponsors to initiate more trials.

Key Industry Highlights:

- Leading Phase: Phase I, with approximately 31.5% share in 2026, as modern designs include expansion cohorts that assess early efficacy, making these trials larger and longer than traditional early-stage studies.

- Dominant Study Design: Interventional studies, nearly 86.2% in 2026, because cancer drug development depends on actively testing new therapies, combinations, and dosing strategies in controlled settings.

- Leading Region: North America, with 46.2% share in 2026, spurred by novel research infrastructure, strong regulatory support, and early adoption of precision oncology trial designs.

- Fast-growing Region: Asia Pacific, due to its large patient pool, swift recruitment timelines, and improving regulatory frameworks, is attracting global sponsors.

- Strategic Partnership: In November 2025, Sarah Cannon Research Institute and Bristol Myers Squibb expanded their strategic partnership to improve patient enrolment. They also aimed to increase access to oncology clinical trials, mainly among underserved populations.

DRO Analysis

Driver - Increasing Prevalence and Incidence of Cancer Worldwide

The steady rise in cancer diagnoses is directly expanding the requirement for clinical trials, especially for targeted and early-stage interventions. According to the World Health Organization (WHO), global cancer cases are estimated to rise from 28.4 million to 29.9 million new cases per year by 2040. Aging populations and lifestyle risks such as obesity and pollution are predicted to act as key contributors.

This surge is not uniform. Countries in the Asia Pacific are witnessing speedy growth in cancers such as lung and colorectal, pushing sponsors to diversify trial locations. Hence, trial designs are increasingly including multi-regional cohorts to capture genetic and environmental variations, improving drug relevance and approval chances across geographies.

Increasing Investment Momentum in Oncology Research Pipelines

Pharmaceutical and biotech firms are primarily prioritizing oncology, reflected in expanding research and development pipelines and strategic collaborations. Companies such as Roche and Merck & Co. continue to allocate a key share of their research budgets to cancer therapies, specifically in immuno-oncology and precision medicine.

Recent developments, such as personalized mRNA cancer vaccines and CAR-T cell therapies, have intensified competition, requiring more complex and biomarker-based trials. This surge in funding is also encouraging small-scale biotech firms to enter niche oncology segments, leading to a high volume of trials targeting rare and hard-to-treat cancers.

Restraint - Overly Restrictive Patient Selection Criteria Delaying Enrolment

Oncology trials often impose highly specific inclusion criteria such as narrow biomarker profiles, prior treatment history, or strict performance status thresholds. These significantly shrink the eligible patient pool. A review by the American Society of Clinical Oncology found that less than 5% of adult cancer patients participate in clinical trials, with eligibility barriers being a key reason.

The issue is becoming more pronounced as precision oncology advances, requiring genomic matching that several patients cannot access in time. For instance, trials targeting rare mutations in lung cancer frequently face delays because identifying suitable candidates depends on unique sequencing infrastructure. Hence, recruitment timelines extend, increasing trial costs and delaying drug development cycles.

Opportunity - Expansion of Trial Networks into Mid-Tier Hospitals

Sponsors are now moving beyond top-tier urban centers and activating oncology trials in secondary hospitals across emerging markets. This shift helps address patient access gaps and improves recruitment diversity. It is evident in countries such as India and Brazil, where a large share of patients is treated outside metro hospitals.

Organizations such as the National Cancer Grid are enabling standardized protocols across small-scale hospitals, making them trial-ready. Recent decentralized trial models using tele-oncology and remote monitoring are further supporting this expansion. Hence, sponsors can enroll patients faster while also capturing real-world disease variations that are often missed in traditional urban-centric trials.

Rising Adoption of Biomarker-led and Personalized Treatment Trials

Increasing focus on precision oncology is creating new opportunities for highly targeted clinical trials. Developments in genomic profiling and liquid biopsy technologies are enabling researchers to design studies around specific mutations rather than broad cancer types. Initiatives by the National Cancer Institute, such as basket and umbrella trials, are accelerating this shift by testing therapies across multiple cancers sharing the same biomarker.

Recent progress in mRNA-based cancer vaccines and next-generation sequencing is also extending the pipeline of personalized therapies. This is increasing the demand for adaptive trial designs, companion diagnostics and small, swift studies with high success rates.

Category-wise Analysis

Phase Insights

Phase I clinical trials are estimated to lead with approximately 31.5% of share in 2026, as the pipeline is heavily skewed toward novel and experimental therapies. Unlike other therapeutic areas, cancer research continuously explores new mechanisms such as cell and gene therapies, antibody-drug conjugates, and mRNA-based treatments. These must all begin with first-in-human safety studies. Data from the National Cancer Institute shows that a significant portion of oncology drugs fail in early stages. This compels companies to run multiple parallel Phase I trials to test different doses, combinations, and biomarkers.

Phase III clinical trials are predicted to be the fastest-growing in the forecast period, as it determines whether a therapy can move from experimental use to standard clinical practice. Regulators such as the U.S. Food and Drug Administration require superior comparative evidence, often against existing standard-of-care treatments, before granting full approval. In oncology, this phase is particularly complex due to endpoints such as survival and progression-free survival, which require long follow-ups.

Study Design Insights

Interventional studies are projected to dominate with nearly 86.2% of the share in 2026, owing to the dependence of oncology drug development on actively testing new treatments, combinations, and dosing strategies in controlled settings. These trials allow researchers to directly measure outcomes such as tumor response and survival benefits. The rise of adaptive trial designs has also strengthened this model, enabling multiple therapies or patient subgroups to be evaluated within a single protocol.

Observational studies are expected to remain in the second position as they capture real-world evidence that clinical trials often miss. Cancer treatments behave differently outside controlled environments, especially across diverse populations with comorbidities. Organizations such as the American Society of Clinical Oncology emphasize the importance of real-world data to support post-approval monitoring and label expansions. Registries tracking long-term outcomes of CAR-T therapies, for instance, are helping researchers understand durability, late toxicities, and effectiveness in broad patient groups.

Regional Insights

North America Oncology Clinical Trials Market Trends

In 2026, North America is predicted to account for a share of approximately 46.2% in 2026, as it blends funding strength, novel research infrastructure, and swift regulatory pathways for high-need therapies. The presence of leading cancer centers, integrated hospital networks, and superior collaboration between academia and industry allows complex trials, including cell and gene therapies, to be executed at scale. Agencies such as the U.S. Food and Drug Administration also provide expedited pathways, including Breakthrough Therapy designation, which encourage sponsors to prioritize the region for early and late-phase studies.

U.S. Oncology Clinical Trials Market Trends

The U.S. remains the core hub, driven by high research and development investments and access to innovative technologies such as genomic sequencing. Institutions supported by the National Cancer Institute run large cooperative group trials and precision oncology programs. The country also leads in unique designs such as decentralized trials and AI-backed patient matching. However, recruitment diversity remains a challenge, with minority participation still limited despite policy efforts to improve inclusion.

The leadership is further propelled by the presence of biopharma innovators, such as Pfizer and Merck & Co., which continue to prioritize oncology pipelines and sponsor complex multi-arm trials. The U.S. also benefits from regulatory flexibility through programs led by the U.S. Food and Drug Administration, including accelerated approvals and adaptive trial pathways that allow early patient access to breakthrough therapies. The integration of real-world data from electronic health records is also improving trial design and post-market evidence generation. However, rising trial costs and competition for eligible patients are pushing sponsors to adopt hybrid and global trial models to maintain efficiency.

Asia Pacific Oncology Clinical Trials Market Trends

Asia Pacific is expanding at a fast pace due to its large patient pool, rising cancer burden, and improving clinical infrastructure. Countries such as China, India, and South Korea are upgrading hospitals to meet global trial standards while delivering fast recruitment timelines. Regulatory reforms and cost advantages are attracting global sponsors to shift parts of their trial operations to the region, especially for Phase II and III studies.

China Oncology Clinical Trials Market Trends

China’s growth is propelled by regulatory transformation and strong domestic innovation. Reforms by the National Medical Products Administration have reduced approval timelines and set up processes in line with global standards. China-based biotech firms are also actively developing immunotherapies and biosimilars, leading to a surge in local trials. The country is also investing heavily in hospital-based research networks, improving patient access and enrolment speed. The momentum is further supported by China’s push to globalize its clinical development interface.

Leading domestic companies, such as BeiGene and Innovent Biologics, are increasingly running Multi-Regional Clinical Trials (MRCTs) to secure approvals in the U.S. and Europe alongside China, reducing time to market. The acceptance of real-world evidence and priority review pathways is enabling quick transitions from early to late-stage trials, mainly in oncology. The expansion of contract research organizations and digital trial platforms is also improving site efficiency and data management. Hence, China is shifting from being a recruitment hub to a key development and trial design center in the field of oncology worldwide.

India Oncology Clinical Trials Market Trends

India is emerging as a preferred destination due to its diverse patient population and improving regulatory clarity. Networks such as the National Cancer Grid are standardizing treatment protocols across hospitals, making multi-center trials more feasible. Recent policy changes have streamlined ethics approvals and encouraged global collaborations. However, challenges such as uneven infrastructure across regions and limited awareness about clinical trials still affect participation rates.

Europe Oncology Clinical Trials Market Trends

Europe is seeing increased activity due to cross-border trial collaboration and superior academic research networks. The implementation of harmonized regulations through the European Medicines Agency has improved trial approvals and transparency across member states. Europe’s leadership in translational research, particularly in immuno-oncology and rare cancers, is also attracting global sponsors.

U.K. Oncology Clinical Trials Market Trends

The U.K. is strengthening its position through fast-track approval systems and integrated healthcare data. The National Health Service provides access to large, centralized patient datasets, enabling efficient recruitment and long-term follow-up. Initiatives supporting genomic medicine and real-world evidence are also encouraging sponsors to conduct early and late-stage oncology trials in the country.

Germany Oncology Clinical Trials Market Trends

Germany’s growth is supported by its well-established hospital infrastructure and emphasis on precision medicine. The country has a high concentration of specialized oncology centers that can handle complex trial protocols, including unique biologics and combination therapies. Backing from organizations such as the German Cancer Research Center promotes collaboration between research institutes and industry, ensuring a consistent pipeline of oncology studies.

Competitive Landscape

The global oncology clinical trials market is fragmented but highly competitive. Large players, mid-sized specialists, and niche biotech-focused providers are competing on different capabilities rather than pure expansion. A small group of large Contract Research Organizations (CROs), such as IQVIA, ICON plc, and Parexel, control a significant share of oncology trials due to their global site networks, regulatory expertise, and ability to run multi-country studies.

Competition, however, remains open because mid-sized firms such as Medpace and Novotech differentiate through speedy study start-up and therapeutic focus. On the other hand, niche players specialize in biomarkers, cell therapy, or lab analytics. This creates a layered market where sponsors often use multiple partners instead of relying on a single provider. Strategic collaborations between CROs, biotech firms, and manufacturers are also becoming a key differentiator.

Key Industry Developments:

- In May 2026, the DEFINITIVE project declared two important operational milestones at the ESMO Breast Cancer 2026 congress. Regulatory approvals have been secured across all seven participating countries, and 33 clinical sites are now actively enrolling patients.

- In April 2026, GSK reported positive early-stage clinical trial results for its ovarian and endometrial cancer drug Mo-Rez. It also announced plans to advance the therapy into multiple late-stage global trials.

- In March 2026, Gilead Sciences announced the acquisition of Tubulis to strengthen its oncology pipeline, especially in antibody-drug conjugates currently in mid-stage clinical trials.

Companies Covered in Oncology Clinical Trials Market

- AstraZeneca

- Merck & Co. Inc.

- IQVIA Inc.

- Gilead Sciences, Inc.

- F. Hoffmann-La Roche Ltd.

- PRA Health Sciences

- Syneos Health

- Medpace

- Novotech

- Parexel International Corporation

Frequently Asked Questions

The global oncology clinical trials market is projected to be valued at US$14.5 billion in 2026.

The oncology clinical trials market is expected to reach US$20.8 billion by 2033.

Rise of biomarker-based trials, increasing use of decentralized and AI-enabled trial models, and surging focus on personalized cancer therapies are a few key market trends.

Phase I segment will likely lead by 2026 with nearly 31.5% share, backed by the requirement of extensive first-in-human safety testing for cell and gene treatments.

The oncology clinical trials market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

AstraZeneca, Merck & Co. Inc., IQVIA Inc., and Gilead Sciences, Inc. are a few key market players.