- Home Care & Utilities

- North America Toilet Seat Market

North America Toilet Seat Market Size, Share, and Growth Forecast, 2026 - 2033

North America Toilet Seat Market by Product Type (Ordinary Toilet Seats, Smart Toilet Seats, Specialised / Medical / Institutional Toilet Seats), Material Type (Plastic (PP, ABS), Urea Moulding Compound / Thermoset, Wood, Misc.), Distribution Channel (Online Retail, Offline Retail) and Regional Analysis for 2026 - 2033

North America Toilet Seat Market Size and Trends Analysis

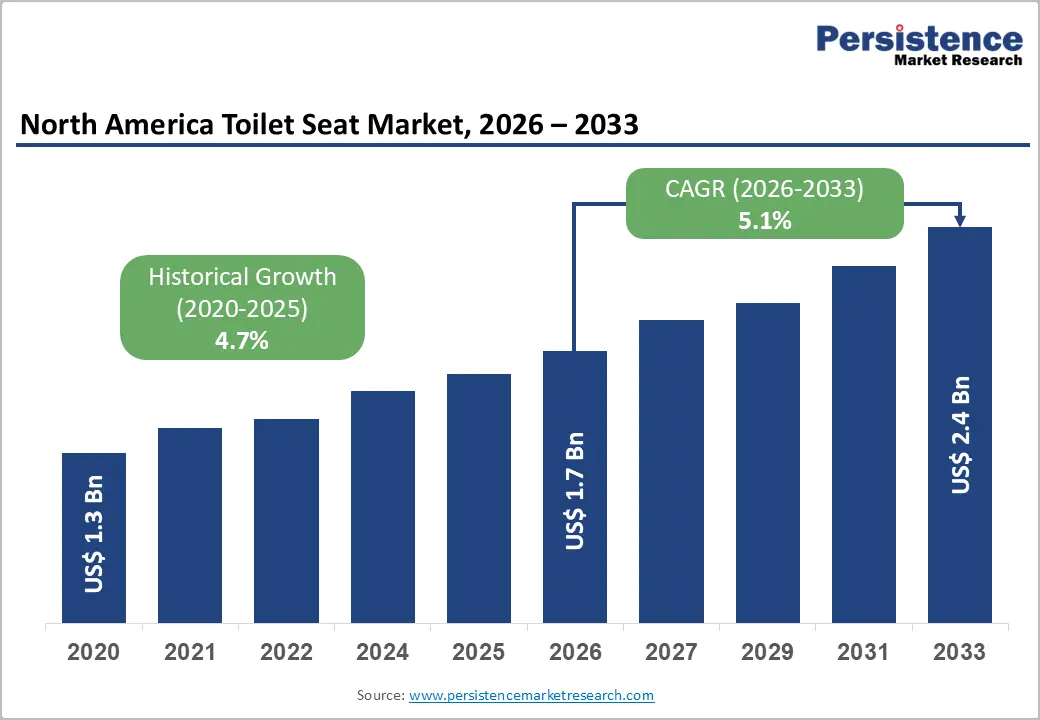

The North America toilet seat market size was valued at US$ 1.7 Bn in 2026 and is projected to reach US$ 2.4 Bn by 2033, growing at a CAGR of 5.1% between 2026 and 2033. The market recorded a historical CAGR of 4.7% from 2020 to 2026, reflecting sustained and consistent expansion across the region.

Primary growth factors include accelerating residential and commercial construction activity across the United States and Canada, a structural shift toward hygiene-conscious bathroom upgrades, and the rapid penetration of smart toilet seat technologies in premium residential and institutional segments. The market benefits from a large and aging housing stock requiring fixture replacement, strong consumer spending on home improvement, and expanding regulatory mandates promoting accessibility and water-efficient sanitation solutions.

Key Industry Highlights

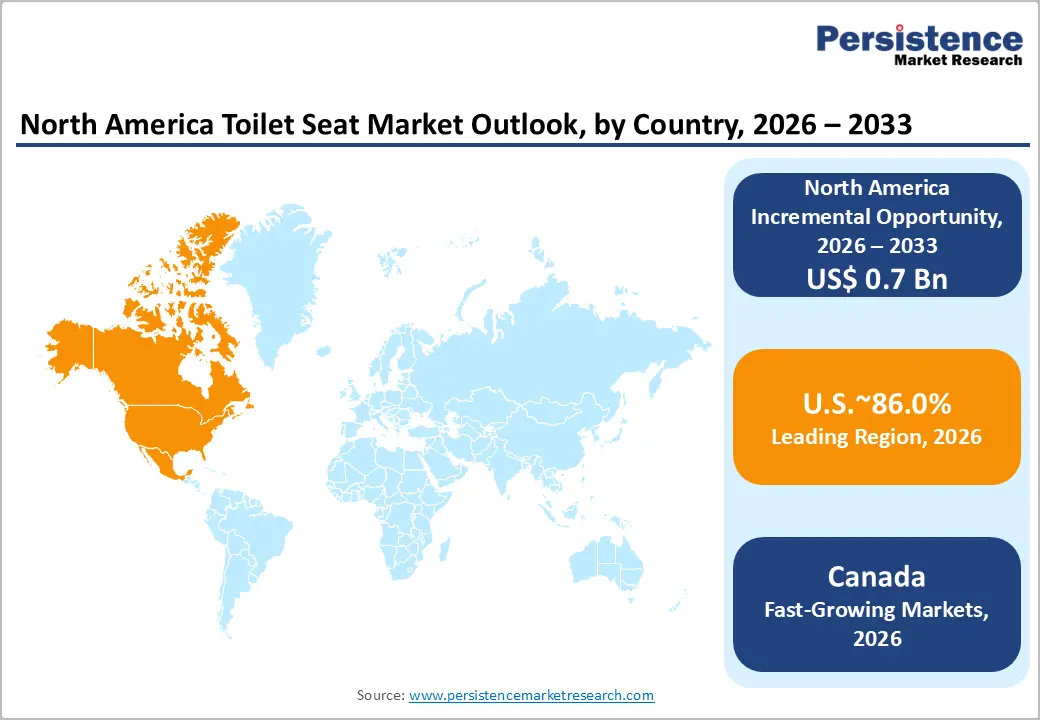

- Leading Country: The United States dominates the North American Toilet Seat Market with an 86% share, driven by a massive installed base of housing units, strong renovation cycles, and high adoption of premium and smart toilet seats.

- High-Volume Leading Segment: Ordinary toilet seats lead the market with 64% share, supported by extensive replacement demand, cost efficiency, and compatibility with standard residential and commercial installations.

- Fastest-Growing Segment: Smart toilet seats are the fastest-growing category, driven by rising adoption of bidet-integrated, hygiene-focused, and wellness-oriented bathroom technologies across residential and commercial sectors.

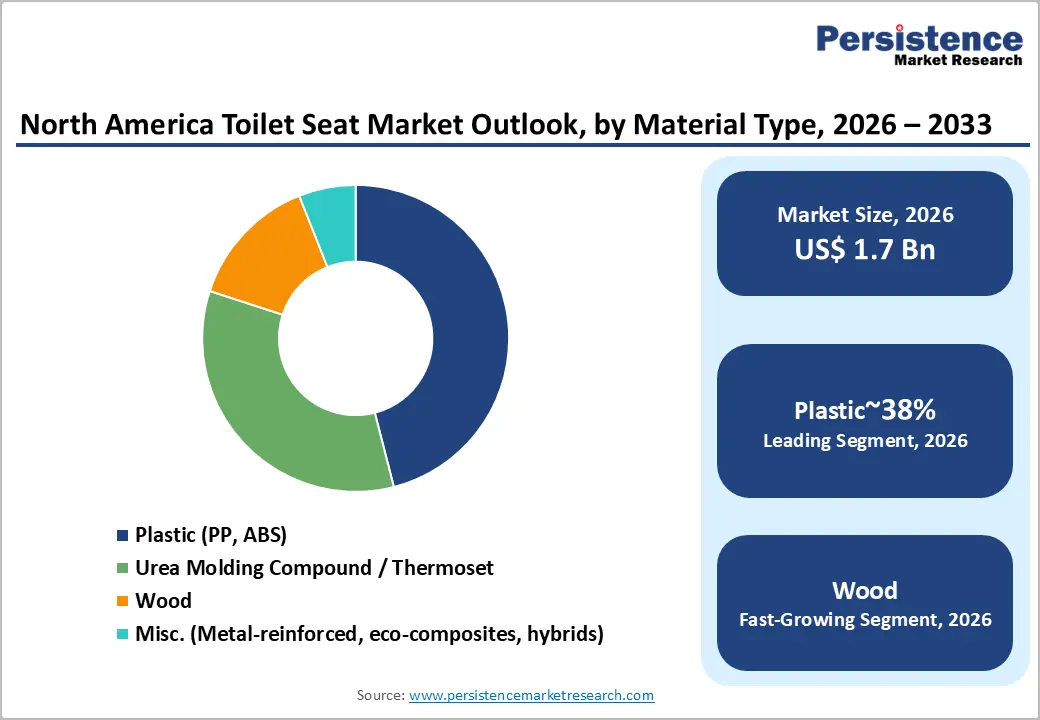

- Leading Material Segment: Plastic-based toilet seats (PP, ABS) dominate with a 46% share, owing to their cost-effectiveness, durability, and widespread use across both standard and mid-tier product categories.

- Key Growth Indicator: Strong expansion in U.S. construction activity, with total spending reaching $2.16 trillion in 2024, continues to generate significant first-fit and replacement demand for toilet seat installations.

- Key Opportunity: Large-scale retrofit and replacement demand from aging U.S. housing stock and expanding institutional infrastructure creates high-value opportunities across residential and commercial segments.

- Industry Development Trend: Increasing investments and innovations by key players, including TOTO’s U.S. manufacturing expansion and Bemis’s accessibility-focused product launches, are accelerating premiumization and smart product adoption in the market.

| Key Insights | Details |

|---|---|

| North America Toilet Seat Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Growth Drivers

Sustained Expansion in U.S. Construction Activity Underpins Demand for Toilet Seat Products

The robust performance of the U.S. construction sector represents a fundamental structural driver for the North America Toilet Seat Market, as every new residential and commercial build requires sanitation fixture installations, including toilet seats. Total construction spending in the United States reached US$ 2.16 trillion in January 2024, up from US$ 822.1 billion in January 2010, reflecting a more than 2.6x increase over 14 years. Residential construction spending alone is forecast to reach US$ 912.8 billion in 2024, recovering from US$ 606.9 billion in 2022.

Commercial construction spending reached US$ 143.0 billion in 2024, up from US$ 43.4 billion in 2010. Non-residential construction is projected to reach US$ 1.25 trillion in 2024, up from US$ 884.2 billion in 2020. Public construction spending surged to US$ 484.3 billion in 2024, the highest level observed in the period. This multi-sector construction expansion generates consistent first-fit and replacement demand, directly amplifying sales volumes across standard, commercial, and specialized toilet seat categories within the North American market.

Institutional and Infrastructure Investment in Canada Creates Structural Demand for Specialized Toilet Seat Applications

Canada's construction and fixed-asset base represent a critical and often underappreciated driver of the North American Toilet Seat Market, particularly in the specialized, institutional, and commercial segments. Canada's total construction fixed assets climbed from US$ 86.6 billion in 2020 to US$ 136.5 billion in 2024, a 57.6% increase in five years. Institutional buildings, including hospitals, schools, universities, and elderly care facilities, now represent the largest and fastest-expanding building asset category, with institutional building assets reaching US$ 25.4 billion in 2024, including US$ 8.2 billion in hospitals and US$ 12.7 billion in schools and universities.

Commercial buildings also grew to US$ 7.25 billion in 2024. Within Canada's December 2025 building permit data, non-residential construction value stood at US$ 4.82 billion, with institutional construction posting 24.9% year-on-year growth and commercial construction showing 25.8% year-on-year growth. These institutional and commercial expansions create direct demand for compliant, durable, and high-specification toilet seat solutions, including ADA-accessible, antimicrobial, and stainless-steel institutional products, reinforcing the Canadian market's strategic importance to the region's overall toilet seat ecosystem.

Advanced Hygiene Technologies and Smart Bathroom Adoption Reshaping Consumer Expectations

The proliferation of hygiene-centric smart toilet seat technologies is a defining demand driver for the North America Toilet Seat Market, fundamentally altering product development priorities and consumer purchasing behavior. In December 2022, TOTO USA confirmed that its WASHLET® line exceeded 60 million units sold globally, with the milestone from 50 to 60 million units achieved in just three years , signaling accelerating acceptance of smart toilet seat technologies in the North American premium segment.

In January 2026, Kohler Co. launched the PureWash E860 Dual-Wand Elongated Bidet Toilet Seat, introducing UV-light automatic wand sterilization that eliminates bacteria by up to 99.9%, a medical-grade stainless steel rear wand, and hybrid water heating. American Standard (LIXIL) reinforced hygiene positioning through its HygieneClean™ System, emphasizing sanitation assurance as a key residential purchase driver. These developments reflect the consumer transition away from commodity toilet seats toward feature-rich, wellness-focused products, driving both average selling price premiums and volume momentum across North American retail and commercial channels.

Restraint - High Product Cost and Price Sensitivity in the Mid-Market Segment

The elevated price points of smart and advanced toilet seat categories remain a structural barrier to broader adoption across the North America Toilet Seat Market. Smart bidet seats with features such as UV sterilization, dual wands, heated water, and self-cleaning functionality command significant premiums over conventional plastic seats, limiting their penetration in cost-sensitive residential and small commercial segments.

A large portion of replacement purchases, particularly in multi-family housing and value-tier retail remain driven by price rather than feature differentiation, constraining the speed at which premium product categories can scale. Supply chain volatility affecting resin, thermoset materials, and electronic components further pressures margin structures for manufacturers across both the standard and smart seat segments.

Residential Construction Cooling in Canada and Renovation Cycle Uncertainty

Canada's residential construction sector is exhibiting a notable deceleration, with residential building permits declining 11.8% year-on-year in December 2025, including single-family permits falling 14.7% and multi-unit housing down 10.4%. Total dwelling units in Canada declined 15.5% year-on-year, signaling a meaningful contraction in new-build first-fit demand that directly affects toilet seat installation volumes.

In the U.S., rising mortgage rates and material cost inflation caused residential construction to drop from US$ 923.6 billion in 2020 to US$ 606.9 billion in 2022, a 34.3% contraction, underscoring vulnerability to macroeconomic rate sensitivity. These cyclical downturns in residential construction create headwinds for baseline volume demand, particularly in the standard and economy toilet seat tiers that depend heavily on new housing completions for first-time installations.

Opportunities - Retrofit and Replacement Demand in the Aging U.S. Housing and Institutional Stock

The North American toilet seat market is uniquely positioned to benefit from an enormous replacement and retrofit cycle driven by the aging U.S. housing infrastructure. The U.S. housing stock includes tens of millions of units built in the 1970s through 1990s, many of which require fixture upgrades as bathroom renovation activity accelerates. Bemis Manufacturing, at KBIS 2026, highlighted that its products are installed on over 225 million toilets in the United States alone, underscoring the scale of the potential replacement opportunity. The company's launch of the Universal Fit™ Toilet Seat at KBIS 2025, designed to fit both round and elongated bowls, directly targets this replacement market by reducing SKU fragmentation for retailers and plumbing professionals.

Beyond residential replacement, U.S. non-residential construction data points to significant retrofit opportunity in educational ($140.97B) and healthcare ($69.07B) construction segments (October 2025, seasonally adjusted). Sewage and waste disposal infrastructure spending posted 15.8% year-on-year growth, reflecting broader public reinvestment in institutional sanitation infrastructure. This creates a dual-track opportunity: residential replacement for upgraded comfort and aesthetics, and institutional replacement for ADA compliance, antimicrobial performance, and long-lifecycle durability, both of which are high-margin, specification-driven demand channels for the North America Toilet Seat Market.

Smart Toilet Seat Penetration in Commercial Hospitality, Healthcare, and Elder Care Facilities

The convergence of hygiene-conscious facility management and smart bathroom technology creates a compelling commercial expansion pathway for participants in the North America Toilet Seat Market. Hospitality, healthcare, and senior living facilities represent high-value, specification-driven procurement channels where smart toilet seat features, including self-cleaning UV nozzle sterilization, reducing microbial surface counts by 99.9% within 60 seconds, antimicrobial surfaces, and heated seat functionality directly support operational hygiene standards. Commercial smart seat models are typically rated for 200,000 actuations, addressing the durability requirements of high-traffic environments.

Canada's institutional building investment, which reached US$ 25.4 billion in fixed assets in 2024, including US$ 8.2 billion in hospitals and significant investment in elderly care, positions the institutional toilet seat segment as a structural growth vector. Facility procurement decisions in these segments are driven by infection control standards, accessibility compliance (ADA/CSA B651), and lifecycle cost analysis, all of which favor higher-specification products. At KBIS 2026, TOTO USA reinforced this trajectory through its Aurora™ WASHLET®+ S7A launch, showcasing fully integrated bidet seat systems for commercial-grade premium bathrooms, affirming that design-led smart toilet seat innovation is gaining institutional traction across the North American market.

Category-wise Analysis

Product Type Insights

Ordinary toilet seats retain a dominant market share in the North America toilet seat market, accounting for 64.0% of total market revenue in 2026. This segment's leadership reflects the vast installed base of conventional residential bathrooms, where cost-effectiveness, wide material availability, and compatibility with standard toilet configurations drive purchase decisions. The majority of first-fit installations in new residential construction, supported by U.S. residential construction spending recovering to a forecast US$ 912.8 billion in 2024, continue to spec standard seats. Replacement cycles in multi-family housing, budget-tier retail, and commercial buildings further consolidate this segment's volume leadership.

The segment benefits from broad distribution across mass-market home improvement chains and e-commerce platforms, with brands such as Bemis, whose products are installed on over 225 million toilets in the U.S., exemplifying the scale of the standard seat category. Product innovations such as the Universal Fit™ Toilet Seat by Bemis, launched at KBIS 2025, are actively extending the value proposition of ordinary seats through improved compatibility and installation efficiency, reinforcing the segment's long-term commercial relevance even as the product mix gradually shifts.

Smart toilet seats represent the most dynamically evolving product category in the North America Toilet Seat Market, driven by the intersection of hygiene technology adoption, wellness-focused consumer behavior, and premium bathroom renovation trends. TOTO USA's WASHLET® line has surpassed 60 million units globally, and the 50M-to-60M unit increment achieved in just three years is a defining market signal. In January 2026, Kohler Co.'s PureWash E860 introduced a first-to-market dual-wand bidet system with UV-light sterilisation (99.9% bacteria reduction), continuous warm water supply, and pre-use bowl misting, setting a new product benchmark.

Material Type Insights

Plastic-based toilet seats, manufactured from Polypropylene (PP) and Acrylonitrile Butadiene Styrene (ABS), command the largest material segment share in the North America toilet seat market at approximately 46% in 2026. PP and ABS are the materials of choice for the mass residential and commercial replacement markets due to their cost efficiency, corrosion resistance, ease of molding into ergonomic forms, and compatibility with soft-close hinge mechanisms. The dominance of plastic in the standard and mid-tier toilet seat tiers aligns with the broader volume leadership of ordinary toilet seats, as both residential construction and replacement cycles default to plastic-moulded seats for their favourable cost-performance ratio.

Plastic remains the predominant substrate for smart toilet seats, with ABS used for outer-shell fabrication due to its dimensional stability and paintability. Manufacturers, including Bemis, Kohler, and American Standard, leverage thermoplastic processing to deliver product lines spanning economy to mid-premium tiers. The Stay- Tite® hinge system showcased by Bemis at KBIS 2026 exemplifies how engineering innovation in plastic seat components is addressing key durability and maintenance concerns, extending the functional lifespan and commercial appeal of plastic seats in high-usage environments.

Wood toilet seats represent the fastest-growing segment in the North America Toilet Seat Market, driven by a structural shift in consumer preferences toward natural materials, artisanal aesthetics, and premium bathroom interior design. Solid and compressed wood seats, including MDF-core with lacquered finishes, natural oak, and bamboo composites, are gaining traction in the premium residential renovation segment, where bathroom design is increasingly treated as a lifestyle investment. The growing "biophilic design" trend in interior architecture, which emphasizes natural textures and materials to create wellness-oriented living environments, is directly translating into demand for wood toilet seats as a distinctive visual element.

Competitive Landscape

The North America toilet seat market is moderately consolidated to oligopolistic in nature, with a small group of large multinational manufacturers controlling a significant share of the premium, smart, and OEM-integrated segments. Companies such as Kohler Co., TOTO USA, American Standard (LIXIL Group), Bemis Manufacturing Company, Centoco, and Sloan dominate the market through strong brand equity, established distribution networks, and deep penetration in both residential and commercial applications. These players collectively shape pricing, product innovation, and channel strategies across the region.

The market retains a competitive mid-layer of regional and niche manufacturers, particularly in the standard and replacement toilet seat segments. Firms like Glacier Bay (Home Depot private label), Delta Faucet Company, Ginsey Home Solutions, and Bath Royale compete aggressively on cost efficiency and retail penetration. This creates a dual-structure market where premium innovation is led by global players, while volume-driven sales are supported by private labels and regional suppliers.

The competitive intensity is further heightened by continuous product innovation in smart toilet seats, bidet integration, soft-close mechanisms, and antimicrobial materials, areas where TOTO, Kohler, and American Standard are particularly strong. These companies leverage R&D capabilities and integrated bathroom system offerings to maintain differentiation, especially in the high-value smart and luxury segments of the North American market.

Key Developments :

- In Aug,2025, TOTO USA inaugurated a $224 million state-of-the-art manufacturing facility in Morrow, Georgia (USA) to significantly expand its North American luxury toilet and toilet seat production capacity. The new facility increases U.S. production capacity for high-end one-piece toilets by approximately 150%, reflecting strong and sustained demand in the North American premium bathroom fixtures market, including integrated toilet seat systems. This investment represents a key milestone in TOTO’s regional growth strategy, aimed at strengthening its Americas supply chain and reducing dependence on Asia-based manufacturing.

- In April 2024, Bemis Manufacturing Company (USA) introduced the Bemis Assist Premium Toilet Seat under its Independence line, expanding the specialized/medical toilet seat segment in the North American market. The product is designed to enhance bathroom safety and user independence, particularly for elderly users and individuals with physical mobility challenges, addressing a key demand driver in the aging-in-place bathroom modification market across the United States. The Bemis Assist toilet seat features built-in support arms that can support up to 500 pounds, eliminating the need for traditional wall-mounted safety rails commonly used in residential and healthcare bathroom installations.

Companies Covered in North America Toilet Seat Market

- Kohler Co.

- American Standard Brands (LIXIL Group Corporation)

- TOTO U.S.A., Inc.

- Bemis Manufacturing Company

- Centoco Incorporated

- Mansfield Plumbing Products, LLC

- Gerber Plumbing Fixtures LLC

- Glacier Bay (Home Depot Private Label Brand)

- Sloan Valve Company

- Acorn Engineering Company (A Crane Co. brand)

- Icera, LLC

- Western Pottery Group, Inc.

- Niagara Conservation Corporation

- Ginsey Home Solutions, LLC

- Topseat International Inc.

Frequently Asked Questions

The North America Toilet Seat Market is projected to be valued at US$ 1.7 Bn in 2026.

The Ordinary Toilet Seats segment is expected to account for approximately 64% of the North America Toilet Seat Market by Product Type in 2026.

The North America toilet seat market is expected to witness a CAGR of 5.1% from 2026 to 2033.

The North America Toilet Seat Market is driven by sustained expansion in U.S. residential, commercial, and public construction activity, rising institutional and infrastructure investment in Canada, and accelerating adoption of advanced hygiene, smart, and bidet-integrated toilet seat technologies.

The key opportunities in the North America Toilet Seat Market lie in large-scale residential and institutional retrofit/replacement demand from aging infrastructure, and rising adoption of smart, hygiene-focused toilet seats across hospitality, healthcare, and elder care facilities.

Key players in the Toilet Seat Market include Kohler Co., TOTO USA, American Standard (LIXIL Group), Bemis Manufacturing Company, Centoco, and Sloan.