- Home Care & Utilities

- Smart Home Devices Market

Smart Home Devices Market Size, Share, and Growth Forecast, 2026 - 2033

Smart Home Devices Market by Product Type (Lighting Systems, Speakers & Voice Assistants, Thermostats & HVAC Control Systems, Security & Access Control Systems, Entertainment Devices, Appliances (Kitchen & Home Appliances combined), Others) Technology (Wired Systems, Wireless Systems [Wi-Fi, Bluetooth, Zigbee, Others (Z-Wave, Thread, Proprietary Protocols)], Hybrid Systems) Distribution Channel, and Regional Analysis for 2026 - 2033

Smart Home Devices Market Size and Trends Analysis

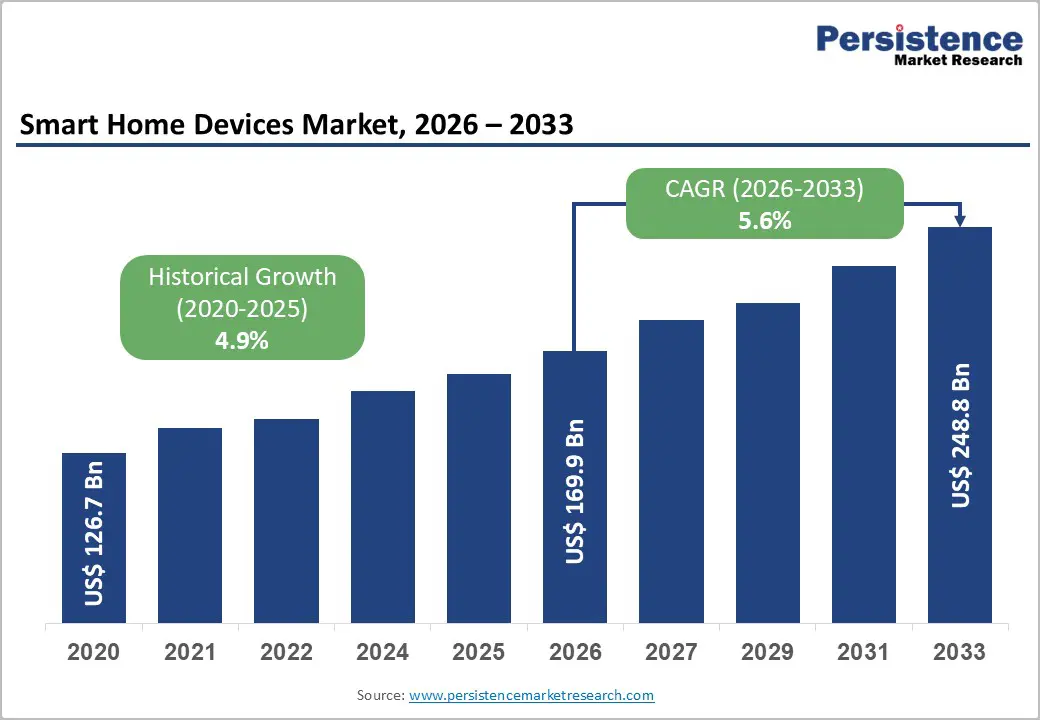

The global smart home devices market size is likely to be valued at US$ 169.9 billion in 2026 and is projected to reach US$ 248.8 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, reflecting a consistent structural shift toward connected living, AI-embedded home automation, and interoperable multi-device ecosystems.

Primary demand is sustained by the convergence of broadband penetration, the widespread adoption of IoT-enabled devices, and consumer prioritisation of energy efficiency, residential security, and seamless convenience.

According to the International Data Corporation (IDC), global smart home device shipments reached 892.3 million units in 2024, with the market expected to rebound to 931.1 million units in 2025 as emerging economies accelerate adoption. Platform-centric innovation by leading OEMs, including AI-driven automation and matter standard interoperability, continues to strengthen the market's long-term commercial trajectory.

Key Industry Highlights:

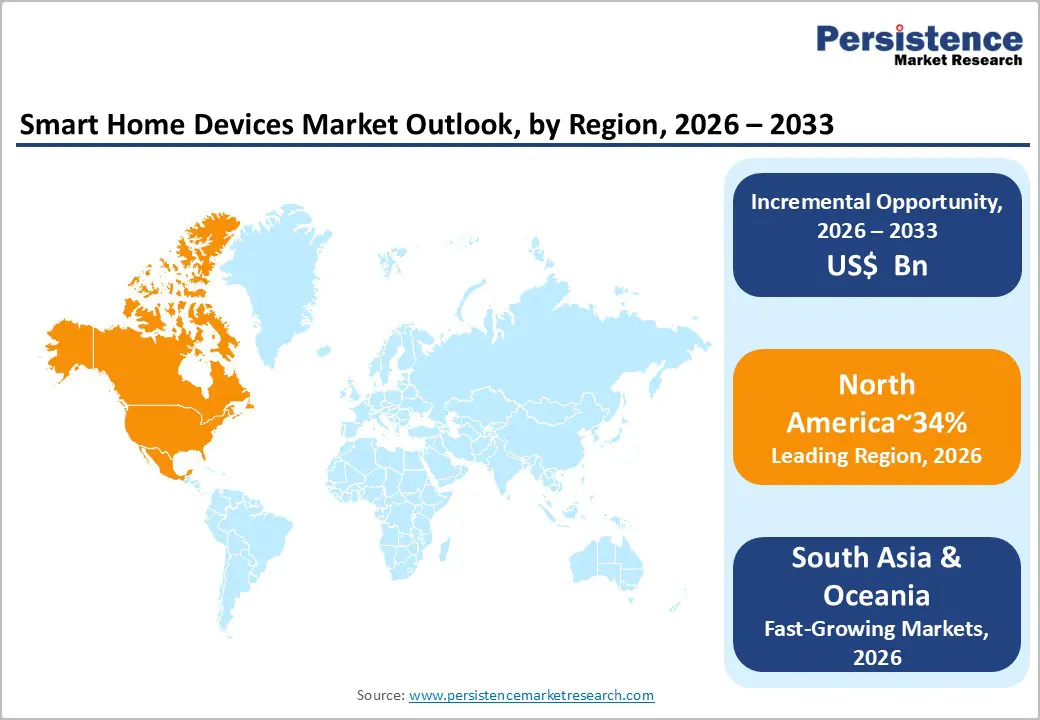

- North America Market Leadership: North America dominates the Smart Home Devices Market with approximately 34% share, driven by high consumer adoption, advanced IoT infrastructure, and strong presence of leading ecosystem players.

- East Asia High-Growth Region: East Asia accounts for nearly 21% share and represents the fastest-growing region, supported by large-scale manufacturing, AIoT innovation, and expanding middle-class adoption.

- Europe Compliance-Driven Adoption: Europe holds around 24% share, fueled by strict energy-efficiency regulations and mandates for smart building automation across residential infrastructure.

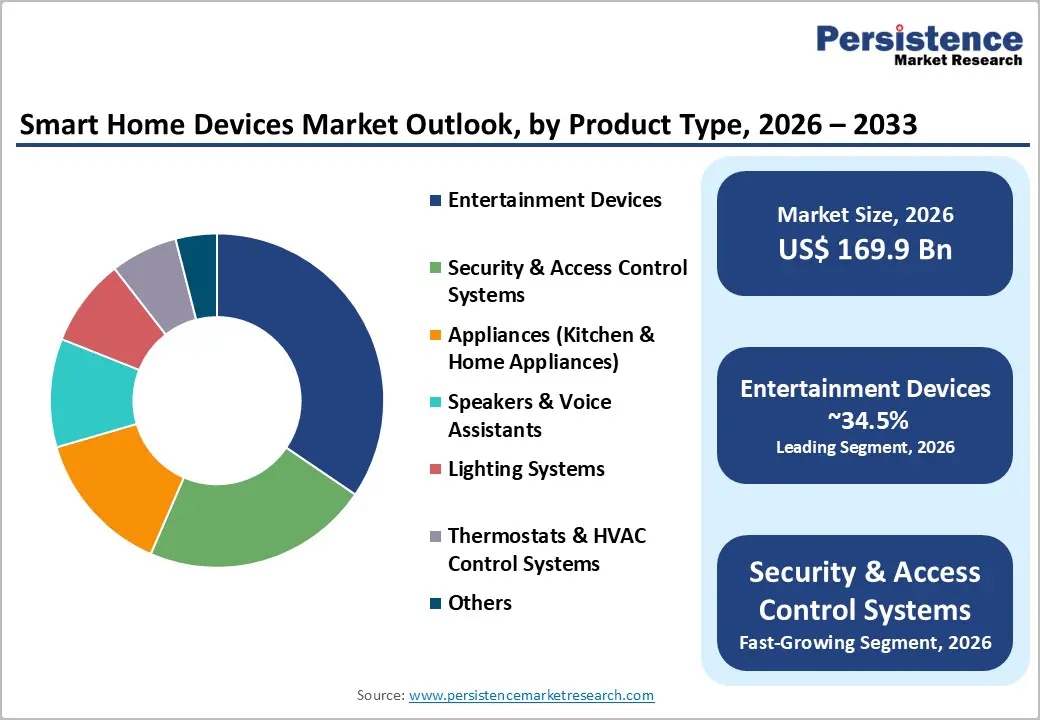

- Entertainment Devices Leading Segment: Entertainment devices lead with approximately 34.5% share, as smart TVs and connected media hubs act as central control interfaces in smart home ecosystems.

- Security & Access Control Fastest-Growing Segment: Security and access control systems account for over 22% share and are expanding rapidly due to rising demand for AI-enabled surveillance and smart safety solutions.

- Wireless Systems Dominant Technology: Wireless technologies hold nearly 48% share, driven by ease of installation, strong retrofit demand, and widespread adoption of Wi-Fi, Zigbee, and Bluetooth protocols.

| Key Insights | Details |

|---|---|

| Smart Home Devices Size (2026E) | US$ 169.9 Bn |

| Market Value Forecast (2033F) | US$ 248.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

DRO Analysis

Drivers - Rapid Deployment of AI and IoT Integration Across Residential Ecosystems

AI and IoT convergence have fundamentally repositioned the value proposition of smart home devices, transforming them from isolated connected gadgets into intelligent, self-optimizing residential ecosystems. This drive reflects a paradigm shift in how automation, energy management, and personalized user experiences are delivered at the home level. According to IDC's Worldwide Quarterly Smart Home Device Tracker, global device shipments are projected to exceed 1.1 billion units by 2028, with AI-powered features becoming a standard across categories such as HVAC, security, and entertainment.

In September 2025, Samsung Electronics launched its "AI Home: Future Living, now" ecosystem, integrating Galaxy AI, Vision AI, and Bespoke AI across its SmartThings platform, encompassing lighting, HVAC, appliances, and entertainment in a single AI-responsive framework. The smart home devices Market directly benefits from this AI-centric transition, as predictive automation, edge intelligence, and personalized environmental control reduce energy consumption while elevating product lifecycle value for both consumers and manufacturers.

Matter Standard Adoption and Cross-Platform Interoperability

The adoption of the Matter communication protocol, developed by the Connectivity Standards Alliance (CSA), has emerged as a structural enabler for the Smart Home Devices Market, addressing the longstanding fragmentation that previously limited ecosystem scalability. Matter provides a unified, royalty-free standard for smart home devices, enabling reliable cross-platform communication among Apple HomeKit, Google Home, Amazon Alexa, and SmartThings.

In November 2025, IKEA launched 21 Matter-compatible products spanning lighting, sensors, and control systems, all integrated through its DIRIGERA hub, directly accelerating affordable smart home adoption globally. Similarly, ABB India launched its ABB-free@home® wireless system in September 2024 with native Matter compatibility, supporting seamless integration across multi-brand home environments. As of 2025, the CSA reported over 5,000 certified Matter devices in the global market, validating industry-wide convergence and creating a strong procurement incentive for residential consumers to upgrade to interoperable smart home infrastructures.

Regulatory Push for Energy-Efficient and Sustainable Buildings

Government mandates targeting energy efficiency in residential buildings have created a policy-driven demand corridor for the Smart Home Devices Market, particularly for smart HVAC, thermostats, and connected lighting systems. The U.S. Department of Energy (DOE) estimates that smart home energy management systems can reduce household energy consumption by 10–15% annually. In Europe, the Energy Performance of Buildings Directive (EPBD) revised by the European Parliament in 2023, mandates building automation and control systems in new construction and major renovations, directly specifying intelligent building technologies.

The International Energy Agency (IEA) has documented that residential buildings account for approximately 26% of global energy-related CO2 emissions, reinforcing the urgency of smart home adoption as a decarbonization strategy. These regulatory frameworks compel developers, contractors, and homeowners to integrate smart devices at the point of construction or renovation, embedding the Smart Home Devices Market within mainstream real estate development cycles.

Restraint - High Device Costs and Premium Ecosystem Lock-In Barriers

The upfront cost of building a comprehensive smart home ecosystem spanning lighting, security, HVAC, and entertainment remains prohibitive for middle-income households. Premium integrated platforms such as Control4 or Crestron can require investments of US$ 10,000–50,000 for full-home deployment. Even mid-tier ecosystems require investment in compatibility, as device fragmentation across protocols has historically forced consumers into vendor-specific environments. This lock-in effect, combined with high hardware costs, limits penetration across price-sensitive demographics in both developed and emerging markets, constraining the Smart Home Devices Market's volume expansion beyond affluent consumer segments.

Data Privacy Concerns and Cybersecurity Vulnerabilities

Smart home devices are frequent targets for cyberattacks due to always-on connectivity and extensive personal data collection. The U.S. Federal Trade Commission (FTC) has documented multiple enforcement actions against smart device manufacturers for inadequate data protection practices. The European Union Agency for Cybersecurity (ENISA) identified connected home devices as among the most vulnerable IoT endpoint categories in its 2023 Threat Landscape report. Consumer distrust of surveillance risks, particularly for cameras, voice assistants, and smart locks, leads to measurable purchase hesitancy, slowing adoption in security-conscious segments and creating compliance obligations that increase manufacturers' operating costs.

Opportunities - Edge AI and Privacy-First Smart Home Automation

On-device AI processing represents a transformational opportunity for the Smart Home Devices Market, enabling autonomous automation without cloud dependency and directly addressing consumer privacy concerns. Edge intelligence allows smart home devices to learn behavioral patterns, detect occupancy, and optimize environmental settings in real time, all without transmitting personal data to remote servers. In December 2024, Universal Electronics Inc. (UEI) unveiled its QuickSet® homeSense platform at CES, incorporating an advanced on-device AI engine that automates HVAC, lighting, and entertainment through sensor fusion, behavioral learning, and privacy-focused rules-based architecture.

For market participants, this technology shift opens a premium product tier where privacy assurance becomes a commercially differentiated feature. The IEA confirms that AI-assisted HVAC optimization alone can achieve 10–15% residential energy savings, providing quantifiable ROI that supports premium pricing. As global data privacy regulations, including the EU AI Act and state-level U.S. privacy legislation, tighten requirements on cloud data processing, edge AI platforms position manufacturers to stay ahead of compliance obligations while capturing the growing consumer segment that actively prioritizes data sovereignty.

Smart Home Device Adoption in Emerging Economies

Emerging markets across South Asia, Southeast Asia, and Latin America represent a structurally underserved opportunity for the Smart Home Devices Market, where smartphone penetration outpaces smart home adoption, creating a ready infrastructure for affordable connected device deployment. According to IDC, following volume stagnation in mature markets in 2024, the anticipated 4.4% rebound in 2025 to 931.1 million units globally is primarily attributed to demand acceleration in emerging economies, validating this regional growth thesis.

Governments across these regions are actively incentivizing smart infrastructure. India's Smart Cities Mission, administered by the Ministry of Housing and Urban Affairs, has committed over US$ 26 billion toward urban digital infrastructure, creating residential demand for connected systems in newly constructed smart urban zones. The affordability shift driven by Asian manufacturers introducing cost-effective smart vacuum cleaners, entry-level security cameras, and budget-tier smart speakers further lowers the adoption threshold. For multinational players, establishing localized distribution, vernacular-language AI assistants, and region-specific regulatory compliance frameworks presents a first-mover advantage in markets projected to contribute disproportionately to the Smart Home Devices Market's long-term volume base.

Category-wise Analysis

Product Type Insights

Entertainment devices are likely to hold a dominant position in the product type segment, with a 34.5% share in 2026, driven by the widespread adoption of smart TVs, streaming sticks, whole-home audio systems, and connected display devices that anchor the consumer's smart home experience. Statista confirms that video entertainment devices accounted for approximately 270 million of the 892.3 million total smart home device shipments globally in 2024, the single-largest category by unit volume. The entertainment hub's central role in smart home ecosystems, where it functions as both a consumption device and a control interface for lighting, ambient audio, and content recommendations, reinforces its leadership. Major platform ecosystems, including Amazon Fire TV, Google Chromecast, and Apple TV, embed AI-driven personalization and smart home control capabilities directly into entertainment hardware, enhancing stickiness and household penetration.

Security and access control systems are the fastest-growing product category, propelled by rising consumer awareness around residential safety and the rapid evolution of AI-powered surveillance capabilities. IDC data confirms that home monitoring and security devices, including connected cameras, smart doorbells, and smart locks, account for over 27% of total smart home device shipments, establishing this as the second-largest category by volume. The Smart Home Devices Market in this segment is further energized by service-based revenue models: cloud storage subscriptions, AI-powered analytics, and professional monitoring packages generate recurring revenue that justifies continuous device refresh cycles. Amazon's Ring integrated AI in June 2025 to distinguish routine deliveries from suspicious activity, while Google Nest cameras use Gemini AI to reduce false alerts, developments that materially improve consumer confidence and sustained category investment.

Technology Insights

Wireless systems command 48% of the technology segment in 2026, reflecting consumer preference for installation flexibility, retrofit compatibility, and the elimination of invasive cabling in residential environments. The proliferation of Wi-Fi 6 and 6E infrastructure across households, with Wi-Fi Alliance reporting over 5 billion Wi-Fi devices shipped globally in 2023, has dramatically improved the network foundation for wireless smart home deployments. The February 2026 launch of ABB Ltd.'s free@home® Wireless System Access Point 3.0, which supports up to 150 connected devices and provides secure cloud-based remote access, exemplifies the segment's commercial maturity. Bluetooth, Zigbee, and Thread sub-protocols collectively extend wireless coverage into energy-efficient, low-latency device networks, particularly for sensors, smart locks, and lighting controllers

Hybrid systems, combining wired backbone reliability with wireless flexibility, represent the fastest-growing technology configuration as the Smart Home Devices Market matures from single-room setups toward whole-home integration. Hybrid architectures are particularly favored in new residential construction and high-end renovation projects, where builders integrate structured cabling for HVAC and security backbone while layering wireless protocols for peripheral device connectivity. ABB Ltd.'s free@home® Wireless platform, launched at Light + Building 2026, demonstrated the commercial appetite for hybrid-capable platforms that eliminate the need for rewiring while maintaining enterprise-grade reliability. As smart home deployments scale to encompass 150+ devices per household in premium segments, the performance stability and bandwidth consistency of hybrid architectures provide a compelling technical and commercial case for accelerated adoption.

Regional Insights and Trends

East Asia Smart Home Devices Market Trend

East Asia accounts for approximately 21% of the global smart home devices market in 2026, with China, Japan, and South Korea each contributing distinct demand drivers and innovation capabilities. China is the world's largest hub for smart home device manufacturing, with the China National Bureau of Statistics reporting over 1.4 billion IoT device connections as of 2023. Domestic brands, including Xiaomi, Haier, and Huawei, have established deeply integrated AIoT ecosystems for the Chinese residential market. Japan's Ministry of Economy, Trade and Industry (METI) allocated approximately ¥50 billion (US$ 340 million) in 2024 toward smart home energy conservation under its Green Innovation Fund, focusing on smart HVAC and home energy management systems. South Korea's Ministry of Science and ICT reported that 5G household penetration exceeded 40% in 2024, creating a high-speed wireless infrastructure backbone that supports latency-sensitive smart home automation applications nationwide.

North America Smart Home Devices Market Trends

North America holds the largest regional share at approximately 34% of the Global Smart Home Devices Market in 2026, led by the United States, where consumer willingness to invest in smart home technology is among the highest globally. The U.S. Department of Energy's weatherization and energy efficiency programs, with US$ 3.5 billion allocated under the Inflation Reduction Act for residential efficiency, include smart thermostat tax credits that directly incentivize the adoption of smart home devices. However, IDC confirmed that U.S. market saturation contributed to the 0.6% global shipment stagnation in 2024, reflecting extended replacement cycles in high-penetration households. Despite near-term maturity headwinds, platform innovation remains vigorous: Samsung's September 2025 launch of its AI Home ecosystem and UEI's QuickSet® homeSense at CES in December 2024 underscore North America's continued role as the primary innovation and commercial launches of premium smart home solutions.

Europe Smart Home Devices Market Trends

Europe accounted for approximately 24% of the global smart home devices market in 2026, shaped by a dual mandate of technological leadership and regulatory compliance. The European Parliament's revised Energy Performance of Buildings Directive (EPBD, 2023) mandates smart readiness indicators and building automation control systems in new and substantially renovated buildings, creating legislative pull for smart HVAC, lighting control, and energy management devices across Germany, France, Spain, and the Netherlands. Germany's Federal Office for Information Security (BSI) published updated smart home cybersecurity guidelines in 2024, elevating device certification requirements and reinforcing consumer trust. The EU's Green Deal industrial strategy ties €1 trillion in public and private investment to decarbonization through 2030, directly embedding smart home devices into the region's core climate infrastructure program.

Competitive Landscape

The global smart home devices market demonstrates a moderately consolidated to oligopolistic structure, with a few dominant multinational players driving a significant share of revenues while smaller players contribute to innovation and niche offerings. Leading companies such as Samsung Electronics Co. Ltd., LG Electronics Inc., Robert Bosch GmbH, Koninklijke Philips N.V., and Panasonic Holdings Corporation maintain strong market positions through diversified product portfolios and integrated smart ecosystems.

The competition is increasingly centred around AI integration, IoT connectivity, and interoperability standards like Matter, enabling seamless cross-device communication. Additionally, firms such as Siemens AG and Johnson Controls International plc. strengthen the market through advanced building automation capabilities. Despite the presence of these major players, regional and emerging brands, particularly from Asia, are intensifying competition with cost-effective solutions and rapid innovation.

Key Developments:

- In Sept 2025, Samsung Electronics announced the launch of its “AI Home: Future Living, Now” ecosystem, integrating smart appliances, devices, and services via its SmartThings platform to enable a fully connected home. The solution leverages Galaxy AI, Vision AI, and Bespoke AI to deliver automated, personalised experiences across lighting, HVAC, appliances, and entertainment systems. This development strengthens the Smart Home Devices Market by accelerating the shift toward AI-driven, interoperable ecosystems focused on energy efficiency, automation, and enhanced user-centric living.

- In November 2025, IKEA launched a new smart home range featuring 21 Matter-compatible products across lighting, sensors, and control systems, aimed at improving interoperability and ease of use. The portfolio is built around Matter standard, enabling seamless integration with multi-brand ecosystems through hubs like DIRIGERA. This development strengthens the Smart Home Devices Market by accelerating standardisation, enhancing cross-platform compatibility, and expanding affordable smart home adoption globally.

Companies Covered in Smart Home Devices Market

- Samsung Electronics Co. Ltd.

- LG Electronics Inc.

- Robert Bosch GmbH

- Koninklijke Philips N.V.

- Panasonic Holdings Corporation

- Haier Group Corporation

- Xiaomi Corporation

- Generac Holdings Inc.

- Crestron Electronics

- Siemens AG

- Johnson Controls International plc.

Frequently Asked Questions

The global Smart Home Devices Market is projected to be valued at US$ 169.9 Bn in 2026.

The Entertainment Devices segment is expected to account for approximately 34.5% of the Global Smart Home Devices Market by Product Type in 2026.

The market is expected to witness a CAGR of 5.6% from 2026 to 2033.

Smart home device market growth is driven by rapid AI and IoT integration, increasing adoption of Matter-enabled interoperable ecosystems, and strong regulatory push for energy-efficient and sustainable residential infrastructure.

Key market opportunities in the smart home devices market lie in the adoption of edge AI-enabled, privacy-first automation systems and the rapid expansion of affordable smart home solutions across emerging economies driven by rising smartphone penetration and smart infrastructure investments.

Key players in the Smart Home Devices Market include Samsung Electronics Co. Ltd., LG Electronics Inc., Robert Bosch GmbH, Koninklijke Philips N.V., and Panasonic Holdings Corporation.