- Sensors & Controls

- North America Temperature Sensor Market

North America Temperature Sensor Market Size, Share, and Growth Forecast, 2026 - 2033

North America Temperature Sensor Market by Product Type (Thermocouples, Resistance Temperature Detectors (RTDs), Thermistors, IC -based Sensors, Infrared (IR) Sensors, Fiber Optic Sensors, Others), Connectivity (Wired, Wireless), Industry (Automotive, Consumer Electronics, Industrial, Healthcare, Energy & Power, Aerospace & Defense, Food & Beverage, Others), and Country Analysis for 2026 - 2033

North America Temperature Sensor Market Size and Trends

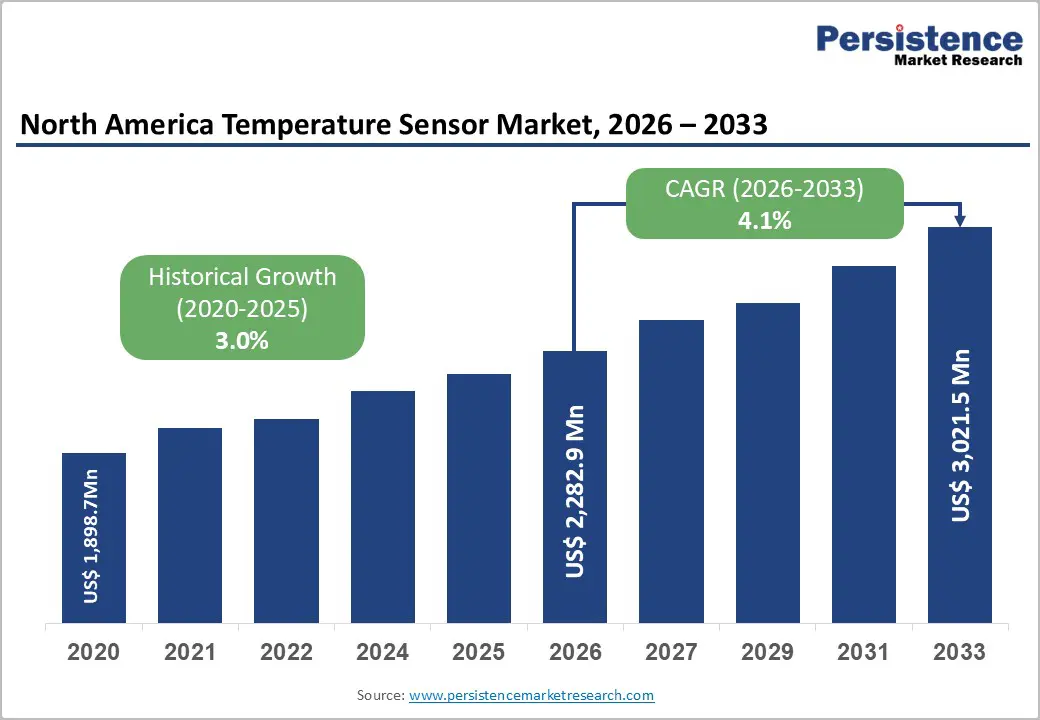

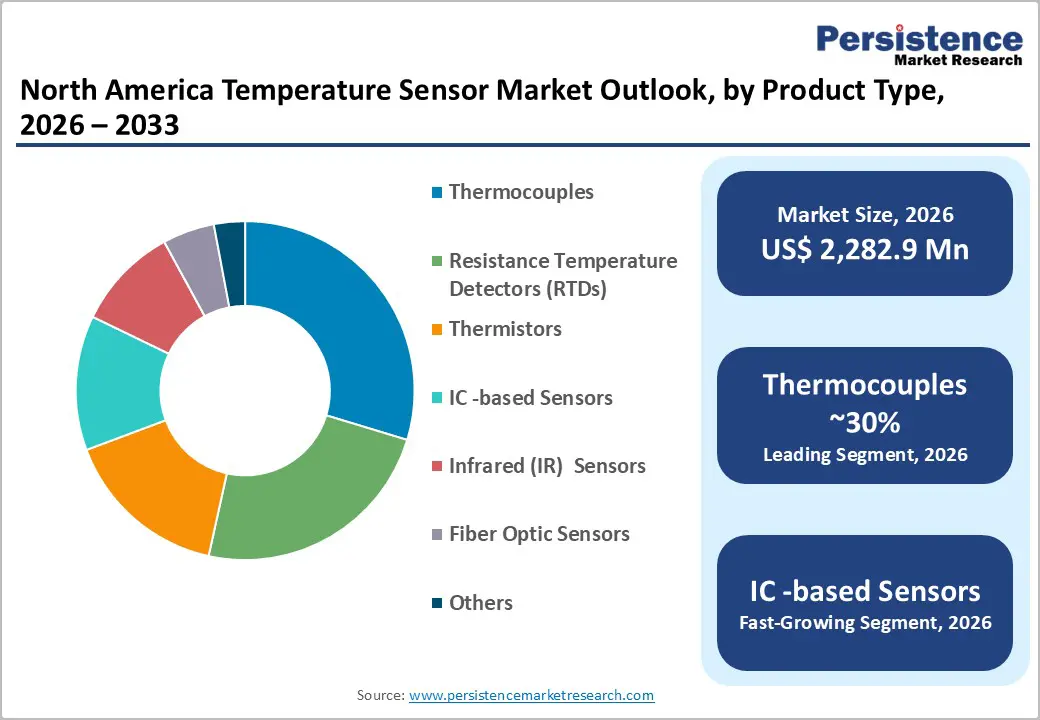

The North America temperature sensor market size is projected to rise from US$ 2,282.9 million in 2026 to US$ 3,021.5 million by 2033. It is anticipated to witness a CAGR of 4.1% during the forecast period from 2026 to 2033.

The market is expanding as temperature sensing is becoming a core layer of control, safety, and efficiency across industries. The demand is also rising as manufacturers shift toward connected equipment, compact electronics, and predictive maintenance systems that require higher accuracy, lower power use, and easier integration. North America remains attractive due to its advanced industrial base, strong adoption of EVs and automation, and the continued product innovation of major suppliers.

Key Industry Highlights:

- Leading Product Type: Thermocouples dominate the market with over 30% market share in 2026, valued at more than US$ 684.9 Mn, driven by strong demand in high-temperature and harsh industrial environments across manufacturing, power generation, and oil & gas sectors.

- Leading Connectivity: Wired connectivity holds over 72% market share in 2026, valued at more than US$ 1,643.7 Mn, due to its high reliability, low latency, and resistance to signal interference in critical industrial applications.

- Leading Industry: Automotive dominates with over 28% market share in 2026, valued at more than US$ 639.2 Mn, supported by the rising integration of temperature sensors in EV battery systems, power electronics, and engine management for safety and performance optimization.

- Leading Country: The United States leads North America with an over 75% share in 2026, driven by advanced semiconductor manufacturing, the rapid expansion of AI-enabled data centers, and a strong regulatory focus on industrial safety and energy efficiency. Canada is witnessing steady growth, supported by increasing adoption of smart HVAC systems, EV thermal management, and cold-chain monitoring applications.

| Key Insights | Details |

|---|---|

| North America Temperature Sensor Market Size (2026E) | US$ 2,282.9 Mn |

| Market Value Forecast (2033F) | US$ 3,021.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.0% |

Market Dynamics

Driver - Rising Adoption of Predictive Maintenance and Industrial IoT Platforms

Enterprises are increasingly shifting from reactive to predictive maintenance models to reduce downtime and optimize asset utilization. The National Institute of Standards and Technology (NIST) highlights that IIoT-enabled monitoring systems significantly improve operational efficiency in the manufacturing and utilities sectors. Temperature sensors are a core component of these systems, enabling real-time monitoring of equipment health.

Companies are embedding advanced analytics and wireless connectivity into their sensor offerings. The ability to detect anomalies early and prevent equipment failure is driving adoption of predictive maintenance across the industrial, automotive, and energy sectors.

Electrification of Vehicles and Expanding Thermal Management Requirements

Modern battery management systems (BMS) in EVs require continuous, real-time thermal monitoring to prevent thermal runaway events and optimize cell performance. Studies indicate that the number of temperature-sensor integration points per vehicle has grown from 3-5 in early 2000s models to 15-20 in current-generation electric and hybrid vehicles. The U.S. automotive sector annually invests billions in R&D, a significant share directed toward advanced sensor-embedded systems.

As North American automakers accelerate EV production targets, sustained demand for robust, highly accurate temperature sensors across battery packs, power electronics, and motor management systems is firmly underpinned.

Restraint - Raw Material Price Volatility and Supply Chain Disruptions

Temperature sensor manufacturing is heavily dependent on critical raw materials, including platinum for Resistance Temperature Detectors (RTDs), rare-earth elements, and specialty semiconductor substrates. Significant volatility in raw material prices driven by geopolitical tensions, trade tariff escalations, and supply chain disruptions directly inflates production costs and compresses manufacturer margins.

Fluctuations in these raw material prices are attributed to ongoing global economic dynamics, increasing demand, and unpredictable trade policies. Such cost pressures are especially acute for smaller sensor manufacturers lacking vertical integration, limiting their ability to maintain competitive pricing without sacrificing product quality or profitability.

High Implementation Costs and Calibration Complexity

Advanced temperature sensors, particularly those designed for critical industrial and aerospace applications, entail higher upfront capital expenditures for procurement, installation, and calibration. Precision-grade RTDs and Fiber Optic Sensors often require specialized expertise for system integration and periodic recalibration to maintain measurement accuracy. For small and mid-sized enterprises in North America, these cumulative costs deter adoption or delay upgrading cycles. Integration with legacy industrial control systems adds engineering complexity and time-to-deployment, further restricting market penetration in price-sensitive and operationally conservative end-use segments.

Opportunity - Expansion of Smart Healthcare and Wearable Medical Devices

Wearable medical devices, such as smart thermometers, patient-monitoring patches, and implantable sensors, are experiencing rapid adoption across hospitals and home healthcare settings. According to the U.S. Centers for Disease Control and Prevention (CDC), remote patient monitoring has expanded significantly post-pandemic, driving demand for continuous temperature tracking systems. IC-based sensors and thermistors are widely used in medical diagnostics due to their accuracy and compact size.

Companies are developing miniaturized, high-precision sensors tailored for biomedical applications. Integration of wireless connectivity with AI-based health monitoring platforms is further enhancing real-time diagnostics.

Growth of Data Centers and High-Performance Computing Infrastructure

Temperature sensors play a critical role in monitoring server rack heat levels, preventing overheating, and optimizing cooling efficiency. The U.S. Department of Energy (DOE) highlights that data center energy consumption has increased significantly due to AI workloads and high-performance computing. Infrared and fiber optic sensors are increasingly deployed for non-contact and high-density thermal monitoring applications. Major cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are investing heavily in advanced cooling infrastructure. This is driving the adoption of precision-sensing solutions integrated with liquid-cooling systems, significantly boosting market opportunities for sensor manufacturers.

Category-wise Analysis

Product Type Insights

Thermocouples dominate the market, capturing more than 30% market share in 2026 with a value exceeding US$ 684.9 Mn, due to their strong need in high-temperature and harsh industrial environments. They are widely preferred in applications where durability, a wide temperature range, and fast response are critical. Industries such as manufacturing, power generation, and oil & gas rely on them for continuous thermal monitoring of equipment and processes. Their simple design and cost-effectiveness make them suitable for large-scale deployment across industrial systems. The growing need for reliable process safety and operational efficiency continues to reinforce their adoption.

IC-based sensors are expected to grow rapidly due to the increasing need for compact, energy-efficient, and highly accurate sensing solutions. They are essential in modern electronics where space constraints and miniaturization are key requirements. The rising demand for smart devices, IoT systems, and real-time data monitoring is accelerating their usage. These sensors offer improved integration with digital systems, reducing overall system complexity. Their ability to deliver precise readings in low-power environments makes them highly suitable for next-generation applications.

Connectivity Insights

Wired holds over 72% share in 2026, with a value exceeding US$ 1,643.7 Mn, driven by the need for stable, interference-free, and continuous data transmission. They are widely used in critical industrial environments where reliability is more important than mobility. Industries prefer wired connections for their higher accuracy, lower latency, and reduced signal loss. Applications such as process control systems and heavy machinery monitoring rely heavily on wired setups. The need for uninterrupted monitoring in mission-critical operations sustains their strong market presence.

Wireless is expected to grow rapidly due to increasing demand for flexibility, remote monitoring, and easier installation. They eliminate complex wiring requirements, making them ideal for modern smart infrastructure and distributed systems. The expansion of IoT ecosystems and cloud-based monitoring is significantly boosting adoption. Wireless solutions are especially useful in hard-to-reach or mobile environments where wiring is impractical. The need for scalable and cost-efficient monitoring solutions is driving strong future growth in this segment.

Industry Insights

Automotive commands the largest market share at over 28% in 2026, with a value exceeding US$ 639.2 Mn, driven by the growing need for thermal management in advanced vehicle systems. Temperature sensors are essential in engine control units, battery systems, and emission control mechanisms. The rise in electric vehicles has further increased the demand for precise thermal monitoring to ensure safety and performance. Automotive manufacturers rely on sensors to optimize efficiency and comply with regulations. The need for enhanced vehicle safety, reliability, and fuel efficiency continues to support strong adoption.

Consumer Electronics is expected to grow at a CAGR of 8.2% driven by the increasing demand for compact, high-performance, and thermally efficient devices. Temperature sensors play a crucial role in smartphones, wearables, laptops, and smart home devices to prevent overheating. Rising consumer demand for longer device lifespans and better performance is boosting sensor integration. Miniaturization trends in electronics require highly precise and low-power sensing technologies. The need for real-time temperature monitoring in increasingly powerful devices is fueling sustained growth in this segment.

Country Insights

U.S. Temperature Sensor Market Trends

U.S. holds over 75% share in 2026, driven by the rapid expansion of advanced manufacturing and semiconductor production supported under federal initiatives such as the CHIPS and Science Act. These facilities require highly precise thermal monitoring to maintain strict process control in chip fabrication, where even minor temperature variations impact yield and performance. The growth of AI-driven data centers, supported by the U.S. Department of Energy’s focus on improving energy efficiency and grid stability, is increasing the use of temperature sensors in liquid cooling systems and high-density server environments to optimize thermal performance and reduce energy consumption. The rising need for compliance with U.S. regulatory standards from agencies such as OSHA and the EPA, mandates continuous temperature monitoring in industrial environments to ensure workplace safety and reduce equipment failure risks.

Canada Temperature Sensor Market Trends

The Canada Temperature Sensor Market is growing at a significant rate, primarily fueled by the need for efficient heating, ventilation, and air conditioning (HVAC) systems, especially due to the country’s long and extreme winter conditions. Temperature sensors are widely used in smart thermostats and building automation systems to optimize indoor heating, improve energy efficiency, and maintain occupant comfort. For example, residential and commercial buildings increasingly rely on sensor-based climate control systems to reduce energy consumption during peak winter months. In EVs, these sensors are essential for battery thermal management to ensure safe operation in very cold climates such as Ontario and Quebec. In healthcare, they support cold-chain monitoring for vaccines and medicines across long transport routes, while in industries like oil and gas and food processing, they help maintain safety, compliance, and product quality under varying operating conditions.

Competitive Landscape

The North America temperature sensor market exhibits a moderately fragmented structure, with leading players collectively accounting for approximately 20 - 30% of total market share. Companies are focusing on portfolio expansion through strategic acquisitions, R&D investment in MEMS-based and wireless sensing technologies, and collaboration with Industry 4.0 integrators.

Key differentiators include sensor miniaturization, multi-parameter functionality, energy efficiency, and IoT compatibility. Emerging business models include cloud-connected predictive maintenance platforms and co-development partnerships with EV manufacturers for custom thermal management solutions.

Key Developments:

- In April 2025, Wilcoxon launched a new digital triaxial accelerometer integrated with a temperature sensor, designed for industrial condition monitoring and predictive maintenance applications. The solution enables simultaneous vibration and temperature data tracking to improve equipment health diagnostics and operational efficiency in industrial environments.

- In January 2025, Thermo Electric - Cotemp Sensing announced the successful development of a 300mm instrumented thermocouple wafer with 65 temperature measurement points for semiconductor applications. The solution, calibrated with liquid nitrogen, delivers high-precision temperature mapping with an accuracy of ±0.5°C (0.4%), supported by advanced data acquisition and thermal analysis software for improved process control.

Companies Covered in North America Temperature Sensor Market

- Honeywell International Inc.

- Texas Instruments Incorporated

- Analog Devices, Inc.

- Emerson Electric Co.

- Amphenol Corporation

- Microchip Technology Inc.

- Watlow Electric Manufacturing Company

- Omega Engineering Inc.

- Teledyne Technologies Incorporated

- Fluke Corporation

- Thermo Sensors Corporation

- TE Connectivity Ltd.

- AMETEK Inc.

- Others

Frequently Asked Questions

The North America Temperature Sensor market is projected to be valued at US$ 2,282.9 Mn in 2026.

The rising demand for precise thermal monitoring across industries, where operational safety and efficiency are critical are key driver of the market.

The North America Temperature Sensor market is expected to witness a CAGR of 4.1% from 2026 to 2033.

Growing adoption of AI-driven data centers and advanced healthcare diagnostics is creating strong growth opportunities.

Honeywell International Inc., Texas Instruments Incorporated, Analog Devices, Inc., Emerson Electric Co., Microchip Technology Inc., Watlow Electric Manufacturing Company, Teledyne Technologies Incorporated, and Fluke Corporation are among the leading key players.