- Specialty & Fine Chemicals

- North America Flame Retardant Thermoplastics Market

North America Flame Retardant Thermoplastics Market Size, Share, and Growth Forecast 2026 - 2033

North America Flame Retardant Thermoplastics Market by Product Type (Acrylonitrile & Electricals (ABS), Polycarbonate (PC), Polypropylene (PP), Polystyrene (PS)), Application (Electrical & Electronics, Automotive & Transportation, Building & Construction, Industrial, Others), and Regional Analysis for 2026 - 2033

North America Flame Retardant Thermoplastics Market Size and Trend Analysis

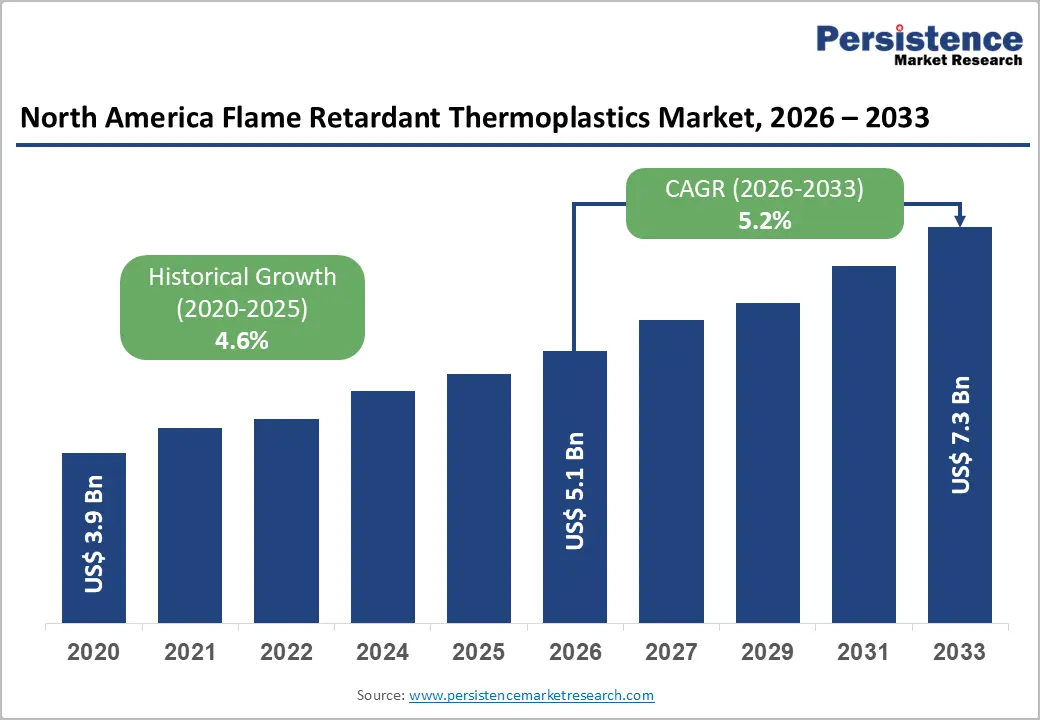

The North America flame retardant thermoplastics market size is valued at US$ 5.1 Bn in 2026 and is projected to reach US$ 7.3 Bn by 2033, growing at a CAGR of 5.2% between 2026 and 2033. This robust trajectory is primarily driven by intensifying fire safety regulations, the accelerating adoption of flame-retardant polymers in electric vehicles and consumer electronics, and sustained infrastructure investment under federally backed construction programs across the United States and Canada.

Tightening fire code compliance requirements enforced by bodies such as the National Fire Protection Association (NFPA), Underwriters Laboratories (UL), and the U.S. Consumer Product Safety Commission (CPSC) are compelling manufacturers to transition to certified flame-retardant thermoplastic solutions, sustaining broad-based demand growth across the forecast horizon.

Key Industry Highlights

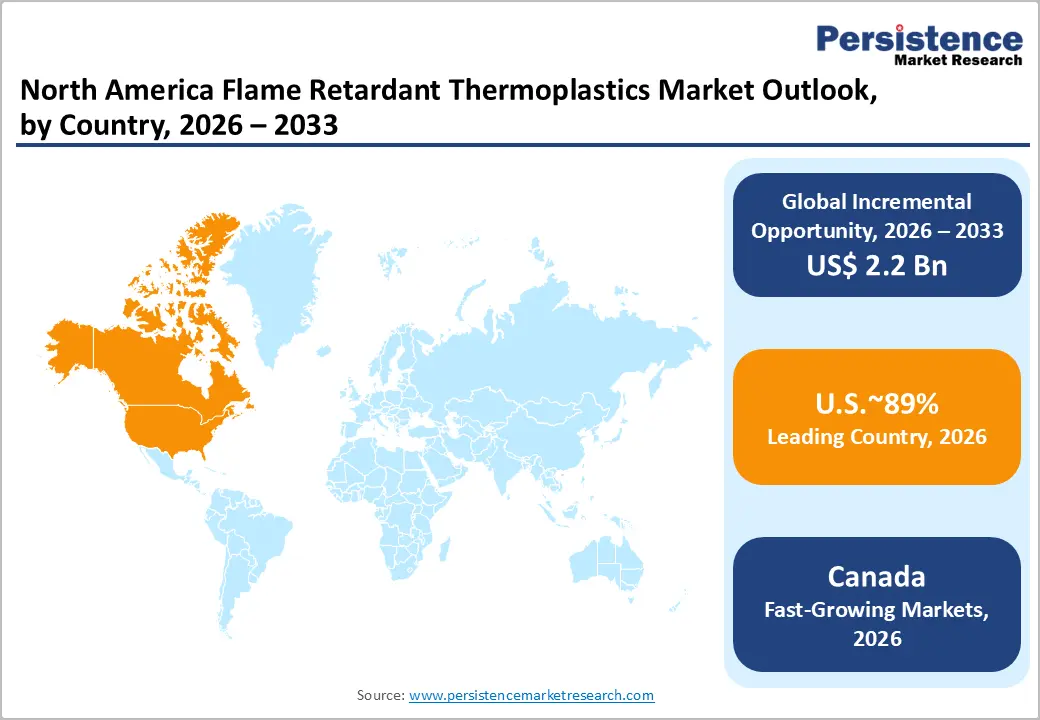

- Leading Region: The United States leads the North American Flame Retardant Thermoplastics market, driven by mandatory compliance with NFPA, UL 94, and CPSC fire safety standards across the electrical, automotive, and construction sectors, as well as a thriving consumer electronics and EV manufacturing ecosystem.

- Fastest Growing Region: Canada is the fastest-growing sub-regional market, propelled by the government's ZEV 2035 strategy, driving EV-related polymer demand, expanding construction activity with CMHC-reported housing starts above 200,000 annually, and stringent CEPA compliance requirements accelerating HFFR adoption.

- Dominant Segment: The Electrical & Electronics application segment dominates with approximately 42% of North America market revenue, anchored by mandatory UL 94 and IEC 60695 certifications for circuit breakers, connectors, and electronic enclosures amid robust consumer electronics and data center expansion.

- Fastest Growing Segment: Halogen-Free Flame Retardant (HFFR) Polycarbonate and Polypropylene compounds represent the fastest-growing product innovation segment, driven by regulatory restrictions on DecaBDE and brominated additives under TSCA, Proposition 65, and evolving CEPA frameworks, incentivizing rapid transitions to phosphorus-based formulations.

- Key Opportunity: The North American EV manufacturing boom, accelerated by IRA incentives and ZEV mandates, creates a high-value demand corridor for certified non-halogenated flame-retardant thermoplastics in EV battery housings, high-voltage connectors, and thermal management components through 2033.

| Key Insights | Details |

|---|---|

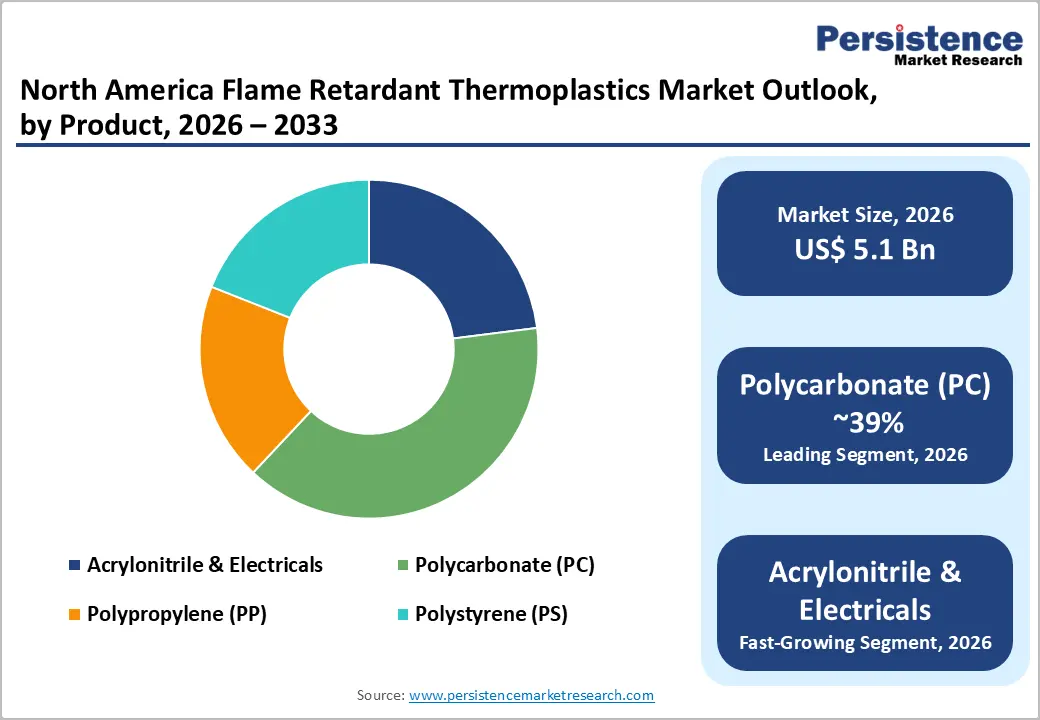

| North America Flame Retardant Thermoplastics Market Size (2026E) | US$ 5.1 Bn |

| Market Value Forecast (2033F) | US$ 7.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.6% |

DRO Analysis

Market Growth Drivers

Escalating Fire Safety Regulations Across Electrical, Construction, and Automotive Sectors

Stringent and continuously evolving fire safety standards remain the most powerful structural demand driver for flame-retardant thermoplastics in North America. Regulatory frameworks enforced by the National Fire Protection Association (NFPA), including NFPA 70 (National Electrical Code) and NFPA 101 (Life Safety Code), mandate the use of fire-resistant materials in wiring, enclosures, building infrastructure, and consumer electronics. The U.S. Consumer Product Safety Commission (CPSC) enforces flammability standards for household products, further broadening the scope of mandatory compliance.

In the automotive domain, Federal Motor Vehicle Safety Standards (FMVSS) issued by the National Highway Traffic Safety Administration (NHTSA) specify flame-resistant interior materials. These multi-sector regulatory demands create a compulsory and expanding market for UL 94 V-0 and V-2 flame-retardant thermoplastic compounds, including polycarbonate, polypropylene, and ABS grades, directly stimulating procurement across all major end-use industries.

Surge in Electric Vehicle Production Driving High-Performance Polymer Demand

The rapid expansion of the electric vehicle industry in North America is creating a structurally significant demand corridor for advanced flame-retardant thermoplastics. EV battery housings, high-voltage connectors, motor inverter terminal blocks, and thermal management components are exposed to extreme thermal and electrical stress, necessitating polymer materials that combine flame-retardant properties with high dielectric strength, thermal stability above 150°C, and low tool corrosion.

According to the International Energy Agency (IEA), global electric vehicle sales surpassed 17 million units in 2024, with North America among the fastest-growing regions. The U.S. Inflation Reduction Act (IRA) has directed billions in tax credits toward domestic EV manufacturing and the development of the battery supply chain, thereby expanding the addressable market for engineered flame-retardant thermoplastic materials in EV platforms. Non-halogenated grades, offering both performance compliance and environmental safety, are gaining particular traction in this segment.

Restraints - Toxicological and Environmental Concerns Over Halogenated Flame Retardant Compounds

Brominated and chlorinated flame retardant additives, historically dominant in thermoplastic formulations, face intensifying regulatory and environmental scrutiny across North America. The U.S. EPA's Toxic Substances Control Act (TSCA) and California's Proposition 65 have established restrictive thresholds for several halogenated compounds, while the Canadian Environmental Protection Act (CEPA) imposes strict reporting and control obligations on toxic chemical substances in commercial products.

Compliance with these expanding restrictions requires costly product reformulation, third-party toxicological certification, and substitution of raw materials. Manufacturers unable to bear these compliance expenditures face market access limitations, particularly in consumer electronics and food-contact packaging, constraining revenue growth in halogenated thermoplastic product lines.

Raw Material Cost Volatility and Supply Chain Disruptions

The production of flame-retardant thermoplastics is dependent on petrochemical feedstocks and specialty chemical additives, including phosphorus compounds, antimony trioxide, and bromine derivatives, whose prices are closely correlated with global crude oil market conditions and geopolitical supply dynamics. The U.S. Energy Information Administration (EIA) has consistently documented the structural volatility of energy and chemical feedstock costs, which cascades directly into raw material inflation for thermoplastic compounders.

Prolonged episodes of cost inflation compress profit margins across the value chain, limit mid-tier manufacturers' ability to invest in product innovation, and create pricing pressure that undermines market accessibility for smaller downstream fabricators. Supply chain vulnerabilities exposed by post-pandemic logistics disruptions further amplify this challenge for the flame-retardant thermoplastics industry.

Opportunities - Transition to Halogen-Free Flame Retardant (HFFR) Thermoplastics: A Regulatory-Driven Growth Wave

The accelerating regulatory and industry-led shift toward halogen-free flame-retardant (HFFR) thermoplastic compounds represents one of the most compelling medium- to long-term growth opportunities for market participants. Growing restrictions on decabromodiphenyl ether (DecaBDE) and other persistent halogenated compounds, aligned with the EU RoHS Directive, China's GB 38031-2020 EV battery safety standard, and the U.S. EPA's Action Plan for Brominated Phthalates, are accelerating the industry transition to phosphorus-based and nitrogen-synergist HFFR solutions.

Phosphorus-based flame retardants currently account for approximately 42% of the halogen-free flame retardant materials market, enabling UL 94 V-0 ratings in thin-wall electronics and automotive components at lower loadings while preserving mechanical strength. Companies developing application-specific, high-performance HFFR thermoplastic grades for 5G infrastructure, EV components, and smart building systems are positioned to access premium-value, fast-growing procurement channels in the coming years.

Smart Buildings and Green Infrastructure Investment Creating Construction Sector Opportunity

The building and construction sector presents a high-potential demand opportunity for flame-retardant thermoplastics, driven by public and private investment in smart, energy-efficient, and fire-safe infrastructure across North America. The U.S. Infrastructure Investment and Jobs Act has allocated over US$ 1.2 trillion toward infrastructure modernization, including electrical systems, public buildings, and transportation networks, each requiring compliant fire-resistant polymer components. The proliferation of smart building systems, including intelligent wiring, HVAC ducting, electrical panels, and building management electronics, drives the adoption of flame-retardant thermoplastics meeting ASTM E84, IBC (International Building Code), and NFPA 285 standards.

Canada is simultaneously experiencing strong growth in commercial and residential construction, with the Canada Mortgage and Housing Corporation (CMHC) reporting housing starts consistently above 200,000 units annually in recent years. Manufacturers developing construction-optimized flame-retardant polypropylene and polystyrene compound grades aligned with the National Building Code of Canada (NBC) are well-positioned to capture this durable and policy-supported demand stream.

Category-wise Analysis

Product Type Insights

Polycarbonate (PC) is the dominant segment in the product type category, accounting for approximately 39% of total North American flame-retardant thermoplastics market revenue. Polycarbonate's market leadership is rooted in its exceptional combination of high impact resistance, intrinsic flame retardancy, superior thermal stability up to 250°F (120°C), dimensional precision, and excellent electrical insulation properties. These characteristics make PC-based flame-retardant grades the material of choice for electrical enclosures, circuit breaker housings, lighting fixtures, safety equipment, and consumer electronics components, all of which are subject to mandatory UL 94 V-0 or 5VA fire performance certifications.

The processability of polycarbonate, enabling complex, thin-wall molded geometries critical for miniaturized electronics, gives it a formulation advantage over competing thermoplastics. The growing adoption of PC/ABS and PC/PBT blend compounds in electric vehicle connector systems and high-voltage automotive components adds a structurally significant incremental demand layer, reinforcing the segment's sustained market leadership through 2033.

Application Insights

Electrical & Electronics (E&E) is the dominant application segment, accounting for approximately 42% of the total North America flame retardant thermoplastics market revenue. This segment's primacy reflects the pervasive requirement for fire-safe polymer materials across circuit breakers, wiring harnesses, plugs and connectors, printed circuit board housings, consumer electronics enclosures, and industrial switchgear components. Regulatory mandates enforced by UL 94, IEC 60695, and RoHS standards require flame-retardant thermoplastic materials to be certified across virtually all electrical product categories.

The accelerating growth of consumer electronics, data center infrastructure, semiconductor fabrication equipment, gaming hardware, and 5G network equipment, all of which consume significant volumes of certified flame-retardant polymer compounds, underpins the segment's dominant and durable position. According to the Consumer Technology Association (CTA), U.S. consumer technology industry revenues regularly exceed US$ 400 billion annually, reflecting the scale of the underlying electronics demand base that continuously drives high-volume procurement of flame-retardant thermoplastic materials.

Country Analysis

U.S. Flame Retardant Thermoplastics Trends & Insights

The United States is the dominant market within North America for flame retardant thermoplastics, driven by an extensive and multi-layered regulatory framework, a large and diversified industrial manufacturing base, and robust consumer electronics and automotive production ecosystems.

The U.S. Consumer Product Safety Commission (CPSC), Underwriters Laboratories (UL), ASTM International, and the National Fire Protection Association (NFPA) collectively define the fire-safety compliance requirements that make flame-retardant thermoplastics mandatory across multiple sectors. The construction industry's sustained growth, buoyed by federal infrastructure funding under the Infrastructure Investment and Jobs Act and the proliferation of megaprojects in smart cities, data centers, and energy infrastructure, is an important catalyst for incremental demand.

The U.S. automotive sector's accelerated pivot toward electric vehicle production, supported by the Inflation Reduction Act (IRA) manufacturing incentives, is generating structural new demand for high-performance, non-halogenated flame-retardant thermoplastic grades in EV powertrains, battery systems, and thermal management modules. Additionally, the rapid buildout of 5G wireless infrastructure and the expansion of hyperscale data centers across the Sun Belt and Pacific Northwest are amplifying demand for UL 94-certified polycarbonate and polypropylene resin compounds. The U.S. market is further distinguished by a dense innovation ecosystem, anchored by research programs at institutions such as the National Institute of Standards and Technology (NIST), that drives continuous advancement in thermoplastic flame retardant chemistry and product performance.

Canada Flame Retardant Thermoplastics Trends & Insights

Canada represents a structurally growing and strategically important secondary market within North America for flame-retardant thermoplastics, characterized by its stringent environmental regulations, expanding manufacturing base, and increasing construction activity.

The Canadian Environmental Protection Act (CEPA) and Health Canada's chemical assessment frameworks impose rigorous restrictions on hazardous flame-retardant additives in consumer and industrial products, thereby directly incentivizing Canadian manufacturers to adopt halogen-free and phosphorus-based thermoplastic compounds. Canada's building and construction sector has recorded robust housing and commercial activity, with the Canada Mortgage and Housing Corporation (CMHC) reporting sustained housing starts exceeding 200,000 units annually, generating consistent demand for fire-resistant thermoplastics in electrical systems, insulation, and structural polymer components.

The automotive manufacturing corridor concentrated in Ontario, home to major OEM assembly plants and Tier 1 component suppliers, represents a significant procurement base for engineering-grade flame-retardant polycarbonate and polypropylene materials. The Government of Canada's Zero Emission Vehicle (ZEV) strategy, targeting 100% zero-emission light-duty vehicle sales by 2035, is accelerating EV platform development in the Ontario corridor and driving new demand for certified flame-retardant polymer materials in next-generation automotive components. Canada's comparatively lower facility setup costs and competitive labor environment relative to the U.S. are additionally attracting thermoplastic compounding investment, further strengthening the domestic supply ecosystem.

Competitive Landscape

The North America flame retardant thermoplastics market exhibits a moderately consolidated competitive structure, with a tier of large multinational specialty chemical and polymer companies holding dominant revenue positions, complemented by a broader layer of regional compounders and application specialists. Market leaders including BASF SE, Albemarle Corporation, and LANXESS compete through proprietary flame retardant chemistry platforms, broad application development networks, and sustained R&D investment in halogen-free and bio-based solutions.

Key competitive differentiators include UL 94 certification breadth, non-halogenated formulation capabilities, custom compounding services, and application engineering support. Strategic trends include cross-sector technology licensing, capacity expansion targeting EV and 5G infrastructure verticals, and sustainability-oriented product portfolio realignment driven by tightening TSCA and CEPA compliance mandates.

Key Developments:

- January 2025, BASF SE launched the flame-retardant Ultramid® T6000 polyphthalamide (PPA) grade for EV terminal block applications, replacing non-FR materials in inverter and motor systems, delivering superior thermal shock resistance and non-halogenated electrical isolation for high-voltage EV components.

- May 2024, SABIC unveiled thermoplastic-based thermal runaway barrier solutions for electric vehicle batteries, with its STAMAX 30YH570 long glass fiber polypropylene compound demonstrating strong thermal barrier performance to mitigate fire hazards in EV battery modules.

- September 2023, LANXESS AG launched Emerald Innovation NH 500, a non-halogen phosphorus-based flame retardant specifically engineered for glass fiber-reinforced polymers serving the electrical and electronics industry, reinforcing its leadership in sustainable flame retardant additive chemistry.

Companies Covered in North America Flame Retardant Thermoplastics Market

- BASF SE

- LANXESS

- Dow Inc.

- ICL

- RTP Company

- Huber Engineered Materials

- Clariant AG

- Plastics Color Corporation

- Albemarle Corporation

- PolyOne Corporation

- SABIC

- Asahi Kasei Corporation

- WASHINGTON PENN PLASTIC CO., INC.

- Koninklijke DSM N.V.

- Teknor Apex

Frequently Asked Questions

The North America Flame Retardant Thermoplastics market is estimated at US$ 5.1 Bn in 2026 and is projected to reach US$ 7.3 Bn by 2033, registering a CAGR of 5.2% during the forecast period, underpinned by regulatory compliance mandates and growing demand from the electric vehicle and electronics manufacturing sectors.

The principal demand drivers are stringent fire safety regulations enforced by the National Fire Protection Association (NFPA), Underwriters Laboratories (UL), and the U.S. Consumer Product Safety Commission (CPSC), combined with the rapid proliferation of electric vehicles, with global EV sales reaching approximately 17 million units in 2024 per IEA data, generating critical demand for high-performance, non-halogenated thermoplastic flame retardant materials.

Polycarbonate (PC) is the leading product type segment, holding approximately 39% of North America market revenue, driven by its superior combination of high impact resistance, thermal stability up to 250°F (120°C), flame retardancy meeting UL 94 V-0 standards, and exceptional processability for electrical enclosures, EV components, and consumer electronics applications.

The United States dominates the North America Flame Retardant Thermoplastics market, backed by its comprehensive fire safety regulatory ecosystem, encompassing NFPA 70, FMVSS, and TSCA, alongside a large and diversified industrial base spanning automotive OEMs, Tier 1 suppliers, consumer electronics, and data center infrastructure, each generating sustained high-volume demand for certified flame retardant polymer compounds.

The most significant opportunity lies in the accelerating transition to Halogen-Free Flame Retardant (HFFR) thermoplastic formulations, driven by regulatory restrictions on halogenated compounds under TSCA, California's Proposition 65, and CEPA. Phosphorus-based HFFR systems, holding approximately 42% of halogen-free retardant material share, are gaining rapid adoption in EV components, 5G infrastructure, and smart building systems, offering premium pricing upside for compliant suppliers.

Leading companies in the North America Flame Retardant Thermoplastics market include BASF SE, Albemarle Corporation, LANXESS AG, Clariant AG, ICL Group, Dow Inc., RTP Company, SABIC, Huber Engineered Materials, Koninklijke DSM N.V., PolyOne Corporation (Avient), Asahi Kasei Corporation, Washington Penn Plastic Co., Inc., and Teknor Apex, among others.