- Automotive Components & Materials

- North America Automotive Seat Market

North America Automotive Seat Market Size, Share, and Growth Forecast 2026 - 2033

North America Automotive Seat Market by Seat Type (Bench Seat, Bucket Seat), by Vehicle Type (Passenger Vehicle: Compact Cars, Mid-sized Cars, SUVs, Luxury Cars; Light Commercial Vehicle, Heavy Commercial Vehicle), Technology (Standard Seats, Powered Seats, Heated Seats, Ventilated Seats, Memory Seats, Other Seats), Material (Leather, Fabric, Synthetic Materials, Others), Distribution Channel (OEM, Aftermarket), and Regional Analysis for 2026 - 2033

North America Automotive Seat Market Size and Trend Analysis

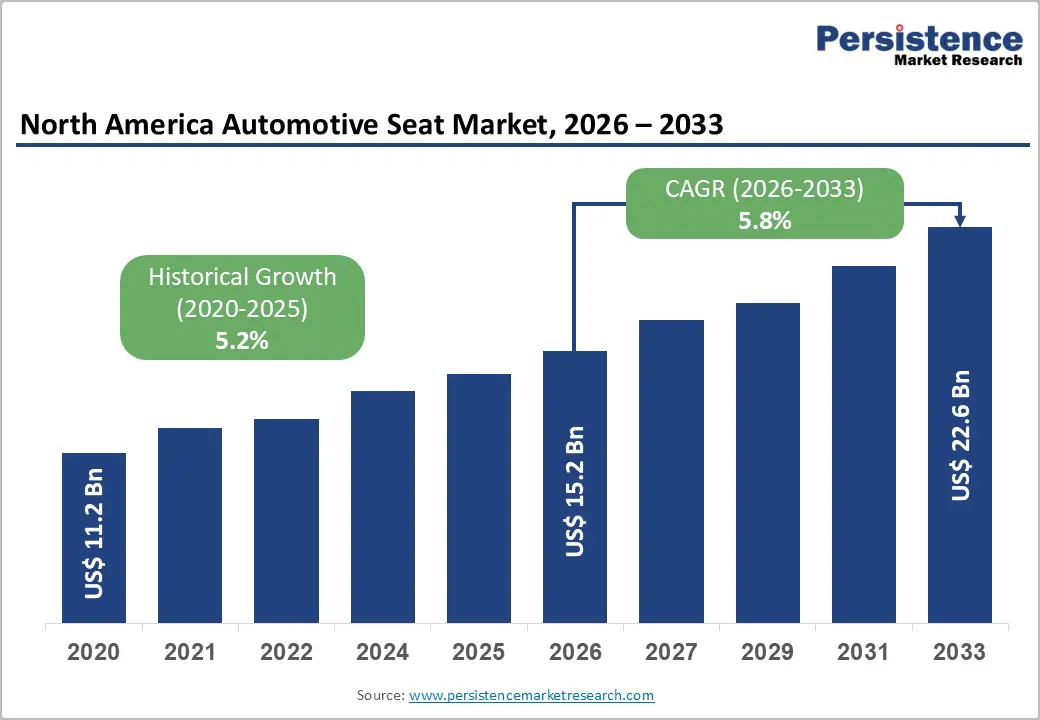

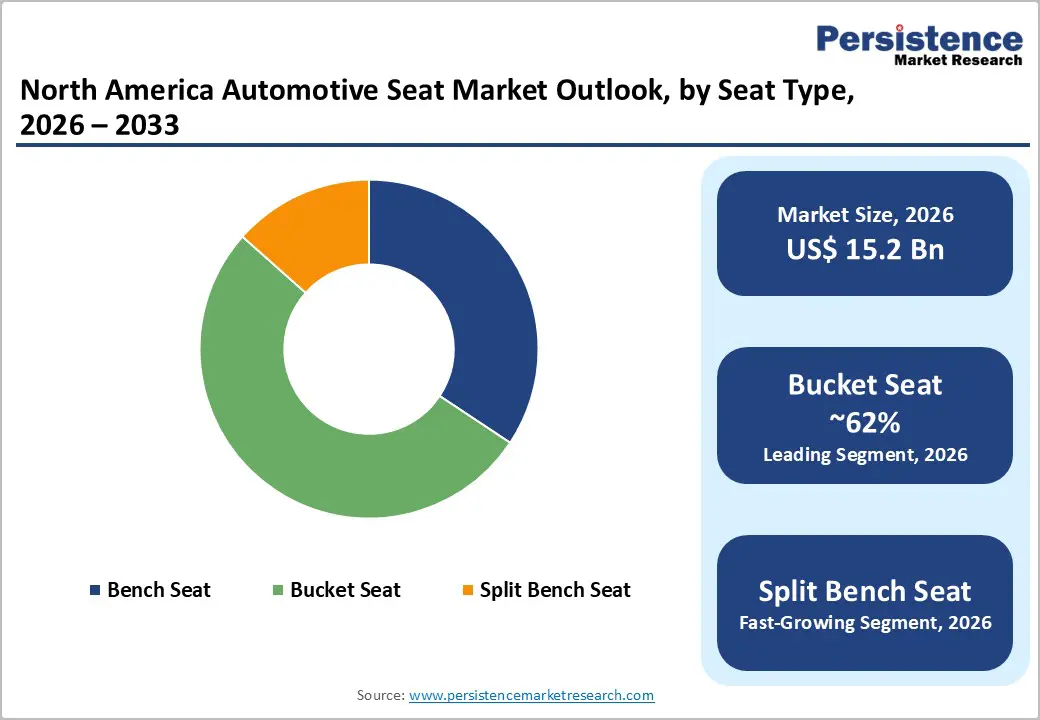

The North America Automotive Seat market size is supposed to be valued at US$ 22.6 Billion in 2026 and is projected to reach US$ 33.5 Billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The North America Automotive Seat market is experiencing sustained and structurally reinforced growth, driven by the region's strong automotive production base, the accelerating consumer preference shift toward SUVs, crossovers, and premium trucks that command the highest seat content value per vehicle, and the rapid integration of advanced seating technologies including powered, heated, ventilated, and memory seat systems across a growing share of new vehicle model lines by Ford Motor Company, General Motors, Stellantis, and Toyota.

Key Industry Highlights:

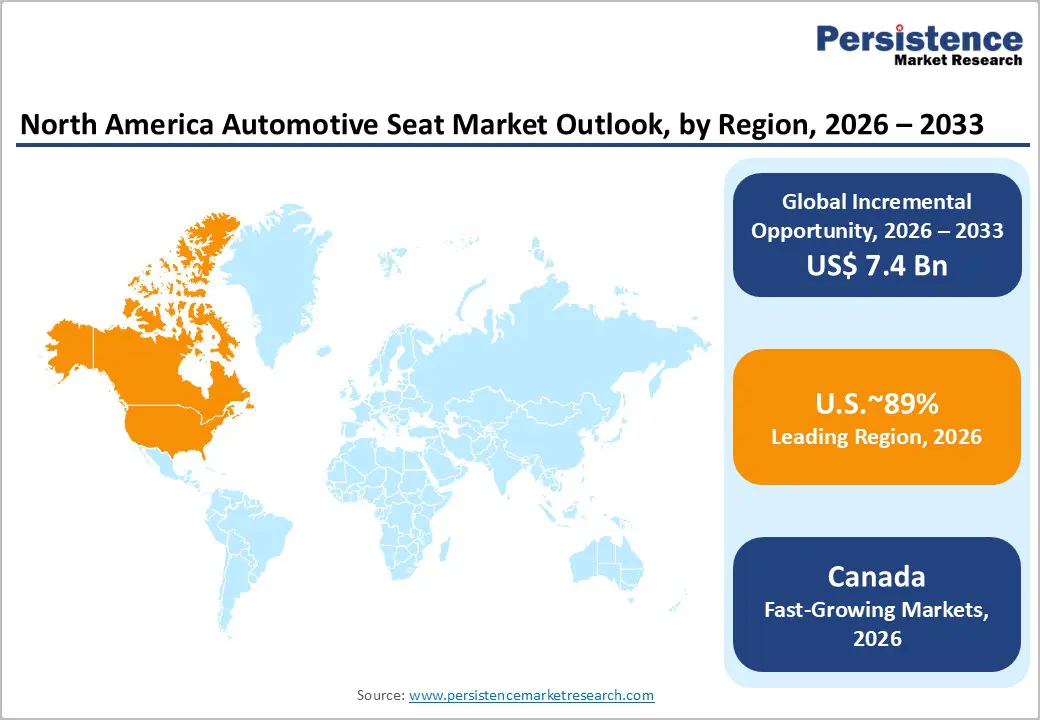

- Leading Country: The United States leads the North America Automotive Seat market, anchored by the Alliance for Automotive Innovation's 80% light truck sales dominance, and Lear Corporation, Adient, and Gentherm's Michigan-anchored OEM supply ecosystem.

- Fastest Growing Country: Canada is the fastest-growing North American market for automotive seats, driven by the Government of Canada's 100% ZEV mandate by 2035 under the Canadian Environmental Protection Act, Magna International's Aurora-headquartered global seat engineering and EV lightweighting investment, Ontario's OEM assembly plant concentration including Toyota Cambridge, Honda Alliston, and Stellantis Windsor, and above-average Canadian EV adoption growth generating smart seat technology procurement.

- Dominant Vehicle Type: Passenger Vehicles dominate the Vehicle Type segment with approximately 74% revenue share, anchored by CarPro's documented top-three U.S. OEM sales leaders generating millions of annual seat system orders, the Alliance for Automotive Innovation's 80% light truck dominance including premium SUV content, and full-size truck flagship trims including Ford F-150 King Ranch and RAM 1500 Limited generating the highest per-vehicle seat system average selling prices in the North American market.

- Fastest Growing Technology: Powered Seats are the fastest-growing Technology segment, propelled by Gentherm's 2023 US$ 1.14 billion revenue from thermal seat system supply growth, Alliance for Automotive Innovation data confirming heated seat availability across 75%+ of North American model lines, and GM's US$ 35 billion EV investment program driving smart seat technology integration across Ultium Platform SUV and truck models with CCS® ventilated and heated seat standard specifications.

- Key Market Opportunity: Autonomous vehicle reconfigurable seat architecture and EV-optimized lightweight seat structures represent the dual key opportunities, with Adient's SkyLounge autonomous seat concept unveiled September 2024, Waymo's commercial robotaxi expansion across U.S. cities, NHTSA's AV TEST Initiative regulatory framework, Lear Corporation's January 2025 EV seat partnership achieving 18% weight reduction, and Canada's 2035 ZEV mandate creating sustained North American premium seat system innovation demand through 2033.

| Key Insights | Details |

|---|---|

|

Automotive Seat Market Size (2026E) |

US$ 22.6 Billion |

|

Market Value Forecast (2033F) |

US$ 33.5 Billion |

|

Projected Growth CAGR (2026–2033) |

5.8% |

|

Historical Market Growth (2020–2025) |

5.2% |

Market Dynamics

Drivers - SUV, Crossover, and Premium Truck Sales Dominance Driving High-Content Seat System Procurement Growth

The structural dominance of SUVs, crossovers, and full-size pickup trucks in North American light vehicle sales, with the Alliance for Automotive Innovation (Auto Innovators) documenting that light trucks (including SUVs, crossovers, pickups, and vans) represented approximately 80% of total U.S. light vehicle sales in 2024, is the most commercially significant demand driver for the North American Automotive Seat market, as these vehicle categories command the highest per-vehicle seat system average selling prices due to their larger seating surface areas, higher trim-level seat content take rates for powered, heated, ventilated, and leather upholstered seat packages, and multi-row seating architecture requiring three-row seat system procurement per vehicle versus two-row sedans and hatchbacks.

Full-size pickup trucks, including the Ford F-Series (the best-selling vehicle in the U.S. for 48 consecutive years as documented by Ford Motor Company), Chevrolet Silverado, and RAM 1500, incorporate premium SuperCrew and CrewMax cab configurations with large-format rear bench and front bucket seat systems that incorporate the full portfolio of heated, ventilated, memory, and powered seat technology features generating above-average revenue per seat system. Lear Corporation and Adient plc supply seat systems to Ford, GM, and Stellantis truck platform programs, with each new-generation full-size truck seat system representing a multi-billion-dollar multi-year supply contract anchoring long-term North American automotive seat market revenue growth.

Electric Vehicle Platform Proliferation Driving Smart Seat Technology and Lightweight Seating Architecture Innovation

The accelerating North American electric vehicle adoption, with Tesla's annual deliveries exceeding 1.8 million vehicles globally in 2023 and General Motors committing US$ 35 billion in EV and autonomous vehicle investment through 2025 under its Ultium Platform strategy, is generating a new and structurally distinct automotive seat demand category where EV-specific flat-floor platform architectures, longer-range battery optimization requirements, and autonomous driving feature roadmaps collectively drive demand for fundamentally redesigned lightweight, multifunctional, and electronically integrated seat systems that are architecturally and technically distinct from conventional internal combustion engine vehicle seat platforms.

Yanfeng Automotive Interiors unveiled its Electric Vehicle Interior (EVI) Smart Cabin Seat concept at CES 2024, integrating front seats, floor console, steer-by-wire input, HMI displays, seatbelts, airbags, and HVAC microclimate system into a single module, demonstrating the transformational seat architecture innovation trajectory that EV platform proliferation is creating for North American automotive seat system suppliers. Gentherm Incorporated (headquartered in Northville, Michigan), a global leader in Climate Control Seat (CCS®) thermal management systems, is directly positioned to capture the EV smart thermal seat adoption growth as EV manufacturers prioritize active seat heating and ventilation as energy-efficient cabin comfort solutions replacing engine-waste-heat dependent conventional HVAC systems in zero-emission vehicle platforms.

Restraints - Raw Material Price Volatility, Particularly Leather, Steel, and Polyurethane Foam, Creating Seat Manufacturing Cost Pressure

North American automotive seat manufacturers face persistent input cost volatility from the three dominant seat bill-of-materials components, leather upholstery (accounting for 15–25% of premium seat system material cost), structural steel frames, and polyurethane foam cushioning, whose prices are influenced by commodity livestock hide market cycles, global steel tariff policy changes, and petrochemical feedstock price movements that create automotive seat manufacturing margin compression during commodity price spike periods.

The U.S. International Trade Commission (USITC) and American Iron and Steel Institute (AISI) have documented significant North American steel price volatility in recent years, impacting seat frame structural steel procurement costs for Lear, Adient, and Magna at a scale that requires active commodity cost management programs and supply agreement price escalation clause negotiations with OEM customers.

Semiconductor Shortage and Electronic Component Supply Chain Disruption Constraining Advanced Seat Technology Production Ramp

The global semiconductor shortage, which the U.S. Department of Commerce documented as causing approximately US$ 210 billion in North American automotive revenue losses in 2021–2022, has created a structural supply chain risk for advanced automotive seat systems that incorporate increasing volumes of electronic control modules, position memory controllers, heating element controllers, and ventilation fan motor drivers in powered and smart seat system architectures.

While the immediate shortage has partially resolved, the Semiconductor Industry Association (SIA) has documented that automotive-grade semiconductor lead times remain 26–52 weeks for specialized microcontrollers, creating ongoing production scheduling challenges for powered, memory, heated, and ventilated seat system production planning by Lear Corporation, Gentherm, and Brose Fahrzeugteile GmbH serving North American OEM production programs.

Opportunities - Autonomous Vehicle Interior Revolution and Reconfigurable Seating Architecture Creating Next-Generation Seat System Opportunity

The North American autonomous vehicle technology development program, with Waymo LLC (a Google/Alphabet subsidiary) operating commercial robotaxi services in San Francisco, Los Angeles, and Phoenix, Cruise (General Motors) and Amazon's Zoox advancing commercial AV deployment programs, and the U.S. Department of Transportation (USDOT)'s AV TEST Initiative providing regulatory frameworks supporting autonomous vehicle testing across 40+ states, is creating a fundamentally transformational next-generation seat system demand category where the elimination of driver-controlled driving inputs enables fully reconfigurable cabin seating architectures with swiveling, reclining, face-to-face conversation, and lounge-mode seat configurations that are architecturally incompatible with current fixed-orientation seat system designs.

RECARO Automotive Seating (headquartered in Stuttgart, Germany) and Grammer AG (headquartered in Amberg, Germany) are actively developing autonomous vehicle optimized seating concepts, with RECARO's SL/RMS autonomous concept seat incorporating 360-degree swivel, integrated airbag systems, and active lateral support features engineered for autonomous highway travel comfort. The USDOT's National Highway Traffic Safety Administration (NHTSA) is developing updated Federal Motor Vehicle Safety Standards (FMVSS) seat belt and occupant protection regulations applicable to forward-facing, rearward-facing, and sideward-facing autonomous vehicle seating configurations, creating a regulatory-driven innovation mandate for North American seat suppliers to develop certified autonomous seating systems.

Heated, Ventilated, and Memory Seat Technology Penetration Growth in Mid-Market Vehicle Segments Creating Volume Opportunity

The North American automotive market's accelerating democratization of premium seat technologies, driven by competitive OEM feature content escalation where heated and ventilated seats have progressively moved from exclusive luxury vehicle features to standard or available features in mid-market SUV and pickup truck trim levels from Ford, GM, Toyota, and Hyundai-Kia, is creating a high-volume, above-average-growth revenue opportunity for heated and ventilated seat system component suppliers including Gentherm Incorporated (the world's leading Climate Control Seat (CCS®) thermal seat system supplier), Kongsberg Automotive, and TS Tech Co., Ltd.

The Alliance for Automotive Innovation documents that heated front seats are now available on over 75% of new vehicle model lines sold in North America, compared to approximately 40% a decade ago, confirming the structural democratization trajectory that is expanding heated and ventilated seat system procurement volumes beyond luxury vehicle platforms into high-volume mid-market SUV, crossover, and pickup truck production programs generating above-industry-average revenue growth for thermal seat technology suppliers through 2033.

Category-wise Analysis

By Seat Type Insights

Bucket Seats lead the North America Automotive Seat market by seat type, commanding approximately 62% of total seat type segment revenue in 2026, a dominant position reflecting the structural shift in North American vehicle sales toward SUVs, crossovers, and premium trucks that almost universally feature individual front bucket seat configurations as the standard specification across all trim levels, complemented by individual captain's chair second-row seat options in three-row SUVs including Chevrolet Tahoe, Ford Expedition, Cadillac Escalade, and Lincoln Navigator that replace conventional bench seat configurations with individual adjustable bucket seats delivering premium ergonomic support and personalized comfort adjustment.

The Alliance for Automotive Innovation's documented 80% light truck share of 2024 U.S. vehicle sales confirms the structural dominance of the bucket seat architecture across North American new vehicle production, as virtually all new SUV, crossover, and pickup truck models specify individual front bucket seat pairs as standard. Adient plc and Lear Corporation are the dominant front bucket seat complete seat system suppliers to North American Ford, GM, Stellantis, and Toyota OEM production programs. Bench Seats retain approximately 38% of seat type revenue, primarily in rear-seat configurations across three-row SUVs and pickup truck second-row bench options chosen by family buyers prioritizing maximum passenger capacity.

By Vehicle Type Insights

Passenger Vehicles lead the North America Automotive Seat market by vehicle type, commanding approximately 74% of total vehicle type segment revenue in 2026, anchored by passenger vehicles' structural dominance of North American light vehicle sales volume, with CarPro's documented 2024 U.S. sales showing Toyota (1,986,954 units), Ford (1,960,338 units), and Chevrolet (1,730,075 units) as the top three brands, collectively generating millions of annual seat system procurement orders from Lear, Adient, Magna, Toyota Boshoku, and TS Tech as their primary seat system Tier-1 suppliers.

Within the Passenger Vehicle category, SUVs (including crossovers) represent the dominant and fastest-growing sub-segment, with passenger cars commanding 73.6% of the North America automotive seat market, where SUVs and full-size trucks drive the highest per-vehicle seat content value through premium trim penetration of heated, ventilated, powered, and leather upholstered seat package options. Light Commercial Vehicles hold approximately 17% of vehicle type revenue, driven by commercial van and mid-size pickup seat procurement. Heavy Commercial Vehicles contribute approximately 9%, with premium-priced high-durability seating from Grammer AG and RECARO serving commercial truck operator procurement.

By Technology Insights

Standard Seats lead the North America Automotive Seat market by technology in absolute revenue share, accounting for approximately 38% of total technology segment revenue in 2026, reflecting the large base of entry-level and mid-range vehicle production incorporating non-powered, non-heated standard seat systems as the base trim specification across high-volume compact and mid-size vehicle platforms.

However, Powered Seats represent the fastest-growing technology segment, with the Alliance for Automotive Innovation documenting that powered seat availability has expanded across over 75% of new North American vehicle model lines, driven by OEM competitive content escalation across SUV and truck platforms where 8-way and 10-way power-adjustable front seat pairs have become standard in mainstream trim levels of Ford F-Series, Chevrolet Silverado, and Toyota Tundra. Gentherm Incorporated's documented Climate Control Seat (CCS®) thermal seat penetration growth confirms heated and ventilated seat technology as a structurally expanding category, with Gentherm's 2023 revenue of approximately US$ 1.14 billion substantially generated by North American OEM thermal seat system supply contracts. Memory Seats hold approximately 11% of technology revenue, concentrated in luxury and near-luxury vehicle segments.

By Material Insights

Leather leads the North America Automotive Seat market by material, commanding approximately 44% of total material segment revenue in 2026, a dominant position driven by North American consumer preference for leather-upholstered seat surfaces across the premium and near-premium vehicle segments that represent a disproportionately large share of total vehicle revenue value, with luxury and near-luxury vehicles representing approximately 12–15% of U.S. unit sales but a significantly higher proportion of total seat system revenue due to premium material and technology content specifications.

Full-grain and semi-aniline leather seat surfaces, specified in Cadillac Escalade, Lincoln Navigator, Ford F-150 King Ranch, Chevrolet Silverado High Country, and Ram 1500 Limited flagship trim packages, command seat system average selling prices of US$ 2,500–6,000 per complete seat set that are substantially above fabric seat equivalents, generating above-average revenue contribution per vehicle. Synthetic Materials hold approximately 29% of material revenue, gaining share through perforated synthetic leather (Sensatec, SynTex) used in BMW, Tesla, and Honda vehicles targeting vegan-friendly and animal welfare-conscious consumer preferences. Fabric holds approximately 22%, serving entry-level and fleet vehicle segments.

By Distribution Channel Insights

OEM (Original Equipment Manufacturer) leads the North America Automotive Seat market by distribution channel, commanding approximately 83% of total distribution channel revenue in 2026, a structurally dominant position reflecting the automotive seat industry's fundamental business model architecture where seat system Tier-1 suppliers Lear Corporation, Adient plc, Magna International, and Toyota Boshoku supply complete seat systems under long-term multi-year OEM production contracts delivered just-in-time (JIT) in sequence to vehicle assembly line stations at Ford, GM, Stellantis, Toyota, and other North American production facilities. The OEM channel's dominance is reinforced by the automotive seat system's classification as a safety-critical vehicle component, with NHTSA's Federal Motor Vehicle Safety Standards (FMVSS 207, 208, 209, and 210) mandating seat structural integrity, occupant restraint integration, and airbag compatibility certifications that effectively require OEM-qualified seat systems for all new vehicle production.

Aftermarket holds approximately 17% of distribution channel revenue, comprising seat cover replacement, heated seat retrofit installation by dealers and independent installers, and commercial vehicle seat replacement from suppliers including RECARO and Grammer AG serving truck fleet operators.

Regional Insights

U.S. Automotive Seat Market Trends

The United States is the dominant North American Automotive Seat market, anchored by the world's most commercially active light vehicle market where Toyota (1,986,954 units), Ford (1,960,338 units), and Chevrolet (1,730,075 units) represent the three largest-volume OEM seat system procurement customers in North America. The U.S. Environmental Protection Agency (EPA)'s fuel economy and emissions standards, and the Inflation Reduction Act (IRA)'s US$ 7,500 consumer EV tax credit sustained through 2032, are driving EV adoption that creates structurally growing smart seat system demand from Tesla, GM Ultium Platform, and Ford Mustang Mach-E and F-150 Lightning EV programs.

The National Highway Traffic Safety Administration (NHTSA)'s ongoing Federal Motor Vehicle Safety Standards (FMVSS) regulatory framework, including FMVSS 207 (seat anchorage strength), FMVSS 202a (head restraints), and evolving autonomous vehicle occupant protection standards under NHTSA's AV TEST Initiative, shapes North American seat system engineering compliance requirements that reinforce the technical barriers to entry protecting established Lear, Adient, and Magna OEM supply positions. Gentherm Incorporated's Northville, Michigan headquarters and Brose Fahrzeugteile's North American operations sustain the U.S. as the global center of thermal seat management and seat mechanism innovation for automotive seat content escalation driving above-CAGR growth in the premium technology seat system segment.

Canada Automotive Seat Market Trends

Canada is a strategically important North American Automotive Seat market, anchored by Magna International's global headquarters in Aurora, Ontario, making Canada the home base of one of the world's three largest automotive seat system suppliers, combined with Ontario's concentration of major OEM vehicle assembly plants including Toyota's Cambridge and Woodstock plants producing RAV4 and Corolla Cross, Honda's Alliston Civic and CR-V production facility, and Stellantis' Windsor assembly plant producing Chrysler Pacifica minivans, all generating domestic Canadian automotive seat system procurement from qualified Tier-1 suppliers. Statistics Canada documented Canadian vehicle production at approximately 1.3 million units annually in recent years, sustaining a proportionally significant domestic seat system manufacturing and supply activity by Magna International, Adient, and Lear Canadian production facilities.

Magna International's comprehensive Canadian automotive seat business, encompassing seat structures, seat covers, seat foam systems, and complete seat assembly under its Seating division, positions Canada as a net exporter of automotive seat system engineering expertise and manufactured content to the broader North American vehicle production ecosystem. The Government of Canada's Zero-Emission Vehicle (ZEV) mandate, requiring 100% zero-emission new light-duty vehicle sales by 2035 under the Canadian Environmental Protection Act, is creating a regulatory-driven EV seat innovation mandate paralleling U.S. IRA incentives, stimulating Magna's Canadian R&D investment in lightweight EV-optimized seat structures and smart thermal management seat systems for the growing North American EV production platform pipeline.

Competitive Landscape

The North America Automotive Seat market is highly consolidated at the OEM Tier-1 level, with Lear Corporation, Adient plc, and Magna International collectively commanding the dominant share of North American OEM complete seat system supply contracts, supported by specialist technology suppliers Gentherm (thermal management), Brose (seat mechanisms), and RECARO (performance and commercial vehicle seating). Toyota Boshoku and TS Tech serve captive Toyota and Honda OEM supply chains.

Key differentiators include NHTSA FMVSS-certified safety integration, just-in-time sequenced delivery capabilities, lightweighting for EV range optimization, and smart seat IoT connectivity. Emerging trends include sustainable bio-based foam and recycled fabric materials, autonomous vehicle reconfigurable seat architecture development, and integrated occupant health monitoring biometric seat sensor systems.

Key Developments:

- In January 2025, Lear Corporation announced a strategic partnership with a leading North American EV manufacturer to supply next-generation lightweight seat systems for a new 2026 model year EV platform, featuring recycled material seat covers, aluminum-intensive seat structures reducing weight by 18% versus conventional steel frames, and integrated thermal comfort zone management aligned with EPA EV efficiency optimization requirements.

- In September 2024, Adient plc unveiled its SkyLounge autonomous vehicle seat concept at the 2024 Paris Motor Show, featuring 180-degree reclining capability, integrated entertainment system, and NHTSA-compliant autonomous occupant restraint architecture designed for deployment in next-generation North American robotaxi and personal autonomous vehicle platforms by 2027–2028.

- In March 2024, Gentherm Incorporated reported record quarterly revenue driven by above-forecast Climate Control Seat (CCS®) system shipments to North American Ford and GM OEM customers, reflecting accelerating heated and ventilated seat technology content adoption across mainstream F-Series, Silverado, and Equinox EV mid-market SUV and truck model lines confirming above-CAGR thermal seat technology penetration growth.

Companies Covered in North America Automotive Seat Market

- Lear Corporation

- Adient plc

- Magna International

- Faurecia

- Johnson Controls

- Toyota Boshoku Corporation

- Tachi-S Co., Ltd.

- NHK Spring Co., Ltd.

- RECARO Automotive Seating

- Brose Fahrzeugteile GmbH & Co. KG

- Grammer AG

- TS Tech Co., Ltd.

- Gentherm Incorporated

Frequently Asked Questions

The North America Automotive Seat market is estimated to be valued at US$ 22.6 Billion in 2026 and is projected to reach US$ 33.5 Billion by 2033, registering a forecast CAGR of 5.8% from 2026 to 2033.

The primary drivers are the Alliance for Automotive Innovation's documented 80% light truck dominance of 2024 U.S. vehicle sales, with Ford F-Series (48 consecutive years as best-selling U.S. vehicle) and Chevrolet Silverado generating premium bucket seat and thermal comfort system procurement, and General Motors' US$ 35 billion EV investment under its Ultium Platform driving smart, lightweight seat system innovation demand from Lear Corporation, Adient plc, and Gentherm Incorporated serving the North American EV production ramp.

Passenger Vehicles lead the Vehicle Type segment with approximately 74% revenue share in 2026, anchored by CarPro's documented 2024 top-three U.S. vehicle sales leaders Toyota (1,986,954 units), Ford (1,960,338 units), and Chevrolet (1,730,075 units) collectively generating the largest annual OEM seat system procurement volumes, with Persistence Market Research confirming passenger vehicles commanding 73.60% of the North America automotive seat market driven by SUV and pickup truck premium content escalation.

The United States leads the North America Automotive Seat market, driven by the the world's highest-volume light vehicle market with Toyota, Ford, and Chevrolet collectively selling over 5.7 million vehicles in 2024 documented by CarPro, and Lear Corporation, Adient plc, and Gentherm Incorporated's Michigan-centered North American OEM automotive seat supply and innovation ecosystem.

The most significant opportunities are autonomous vehicle reconfigurable seat architecture and EV-optimized lightweight seat system development, with Adient's SkyLounge September 2024 autonomous seat concept, Waymo's commercial robotaxi expansion across U.S. cities, NHTSA's AV TEST Initiative across 40+ states, Lear Corporation's January 2025 EV seat achieving 18% weight reduction, and Canada's 2035 ZEV mandate collectively driving premium seat technology innovation procurement through 2033.