- Beverages

- Non-Alcoholic Wine Market

Non-Alcoholic Wine Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

The Non-Alcoholic Wine Market is segmented by Product Type (Red Wine, White Wine, Rosé Wine, Sparkling Wine), by Packaging Type (Glass Bottles, Cans), by Sales Channel (HoReCa, Supermarkets & Hypermarkets, Specialty Wine & Liquor Stores, Airlines & Travel Retail, Online Retail, Others), and by Regional Analysis, 2026 - 2033

Non-alcoholic Wine Market Share and Trends Analysis

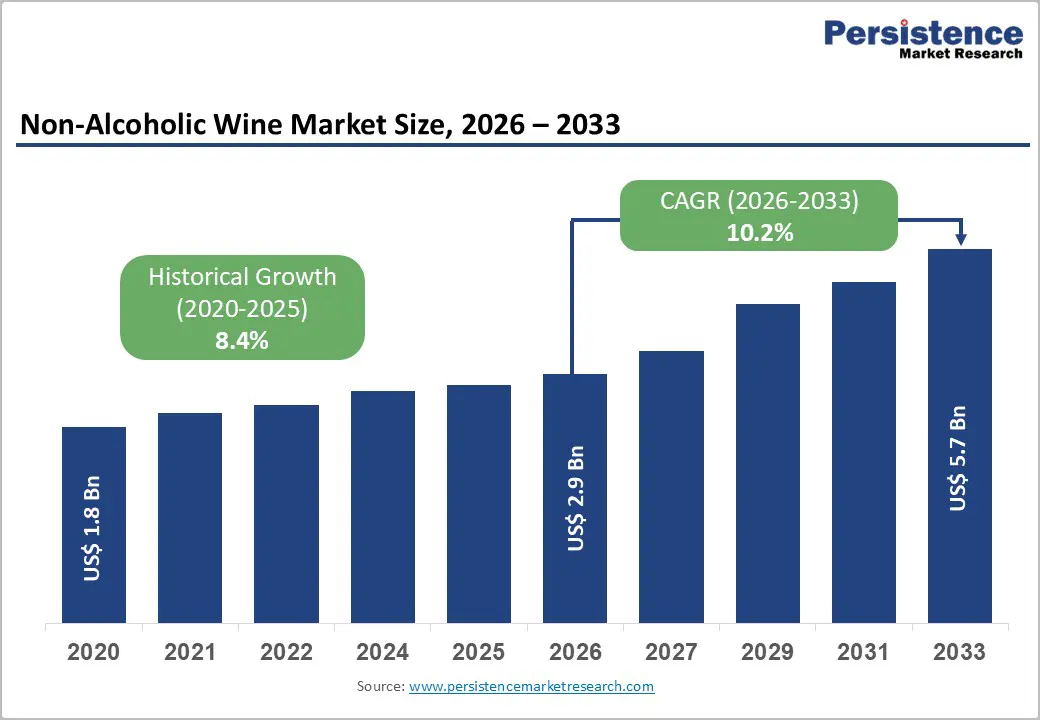

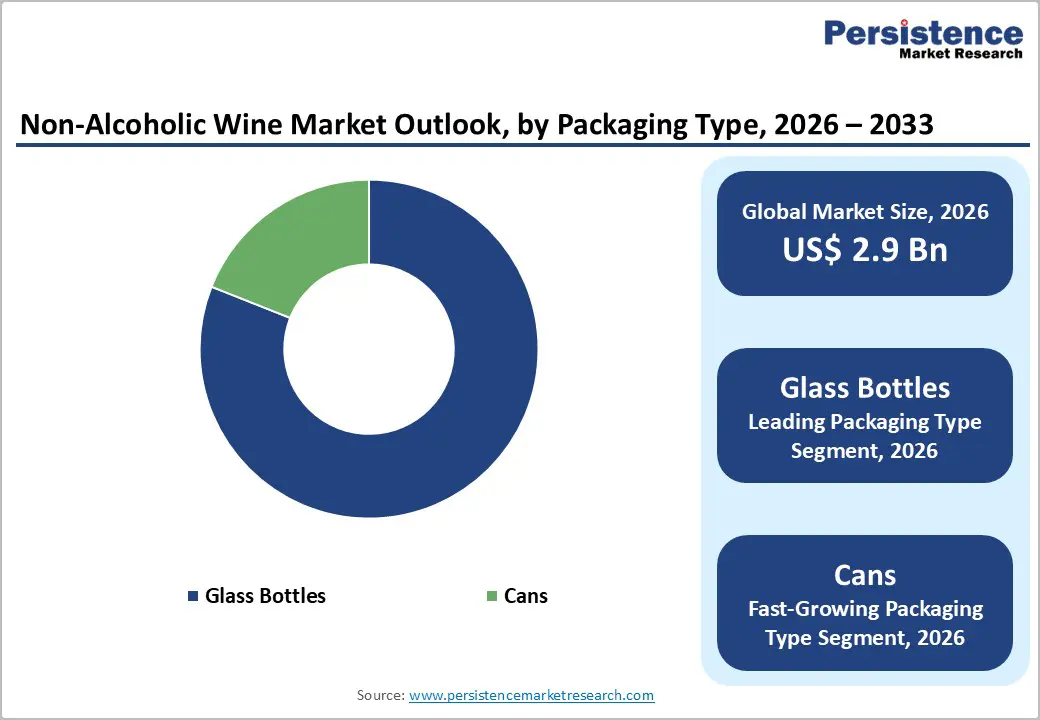

The global non-alcoholic wine market size is expected to be valued at US$ 2.9 billion in 2026 and projected to reach US$ 5.7 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

This rapid expansion is primarily propelled by the global sober curious movement and a fundamental shift toward health-conscious lifestyle choices among younger demographics. As consumers seek to reduce alcohol consumption without sacrificing the social rituals and complex flavor profiles associated with traditional viticulture, the demand for high-quality de-alcoholized alternatives has intensified. Furthermore, significant advancements in vacuum distillation and spinning cone column technologies have allowed producers to maintain the nuanced aromas and structural integrity of the wine, making these products increasingly competitive with their alcoholic counterparts in both retail and fine-dining environments.

Key Industry Highlights:

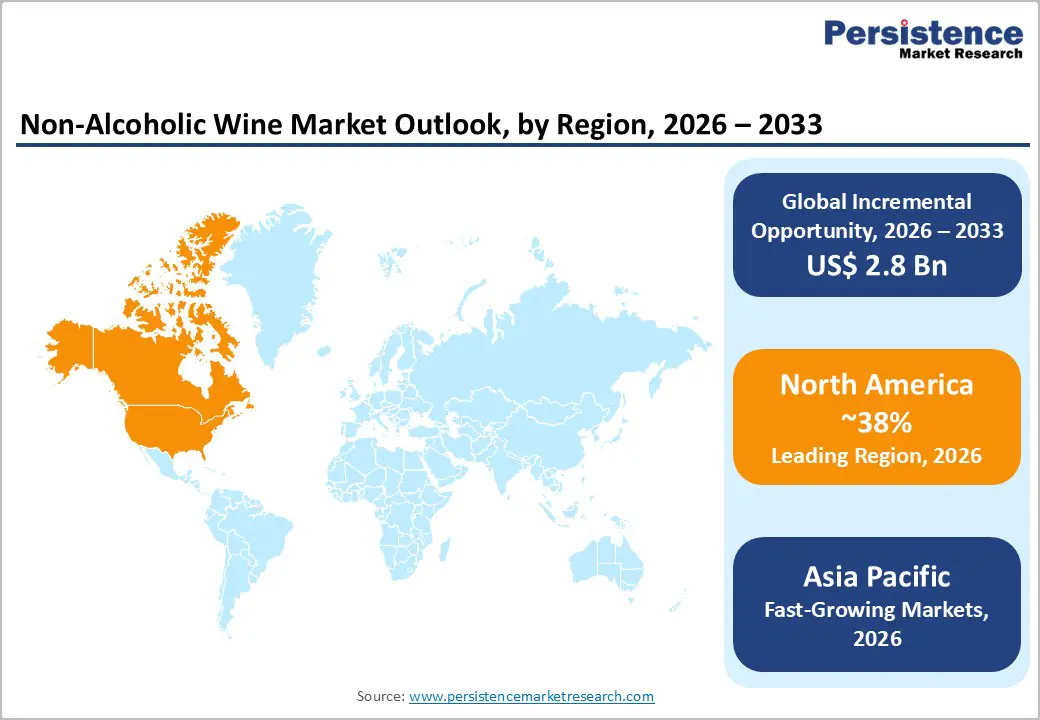

- Leading Region: North America, holding 38% market share, driven by strong wellness culture, advanced retail infrastructure, and high adoption of low-calorie, alcohol-free beverages.

- Fastest-Growing Region: Asia Pacific, fueled by rising middle-class population, urbanization, westernized drinking habits, and increasing acceptance of non-alcoholic alternatives across key markets.

- Fastest-Growing Product Type Segment: Sparkling Non-Alcoholic Wine, driven by superior sensory experience, celebratory consumption occasions, and strong demand in hospitality and social settings.

- Market Drivers: Rising health consciousness and sober-curious trends are accelerating demand for alcohol-free alternatives that offer wine-like experiences without compromising wellness, calorie control, and lifestyle preferences.

- Opportunities: Premiumization through advanced dealcoholization technologies is enabling high-quality offerings, unlocking growth in luxury segments, fine dining, and experiential consumption channels.

- Key Developments: In January 2026, O’Neill Vintners & Distillers launched FitVine Free, a functional non-alcoholic wine. In December 2025, Abrau-Durso Group introduced a non-alcoholic still wine, while Moët Hennessy invested in French Bloom to expand premium alcohol-free offerings.

| Key Insights | Details |

|---|---|

| Global Non-Alcoholic Wine Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 5.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.4% |

Market Dynamics

Driver - Rising Health Consciousness Driving Shift Toward Zero Alcohol Beverages

A fundamental shift in global consumer behavior toward healthier lifestyles is significantly driving demand for non-alcoholic wine. Consumers are becoming increasingly aware of the long-term health impacts associated with alcohol consumption, including liver disease, cardiovascular issues, and mental health concerns. This awareness is encouraging a transition toward low-alcohol and alcohol-free beverage alternatives that allow consumers to maintain social drinking habits without compromising their health goals.

Non-alcoholic wine offers a compelling value proposition by delivering the sensory experience of traditional wine such as flavor complexity, aroma, and pairing compatibility while eliminating alcohol content. This is particularly appealing to health-conscious individuals, fitness-oriented consumers, and those following specific dietary or wellness regimes. Additionally, rising participation in sober curious movements and temporary abstinence initiatives such as dry months is accelerating product adoption across developed markets.

The growing focus on calorie reduction is another key factor, as non-alcoholic wines generally contain fewer calories compared to traditional wines. This aligns with weight management and clean lifestyle trends. As consumers increasingly seek functional and better-for-you beverage options, non-alcoholic wine is emerging as a viable and sustainable alternative within the evolving global beverage landscape.

Restraints - Limited Consumer Acceptance Due to Perceived Inferior Taste and Authenticity Concerns

Despite growing awareness and availability, consumer perception remains a significant barrier to the widespread adoption of non-alcoholic wine. Many consumers associate wine with its alcohol content, which contributes not only to its intoxicating effect but also to its body, mouthfeel, and flavor complexity. Removing alcohol from wine can alter its structural balance, often resulting in products that are perceived as thinner, less aromatic, or lacking depth compared to traditional wines.

These sensory limitations have led to skepticism among regular wine consumers, particularly connoisseurs who value authenticity and traditional winemaking processes. Even as technology improves, replicating the full sensory profile of alcoholic wine remains a challenge for producers. As a result, first-time users may experience dissatisfaction, limiting repeat purchases and slowing category growth.

Opportunity - Premiumization of Non-Alcoholic Wines Through Advanced Dealcoholization and Flavor Technologies

Technological advancements in dealcoholization and flavor enhancement are driving strong opportunities for premiumization in the non-alcoholic wine market. Early generations of alcohol-free wines often struggled to maintain flavor integrity after alcohol removal. However, modern techniques such as vacuum distillation, reverse osmosis, and spinning cone column technology enable producers to better preserve aromatic compounds and the structural characteristics of wine.

These innovations allow manufacturers to create high-quality non-alcoholic wines that closely mimic the taste, mouthfeel, and complexity of traditional wines. As a result, brands can position their offerings in premium and super-premium segments, targeting consumers willing to pay more for quality and authenticity. This is especially relevant in developed markets, where consumers are already familiar with wine culture and expect elevated sensory experiences.

Premiumization also creates opportunities in hospitality, including fine dining restaurants, hotels, and specialty retailers, where demand for sophisticated non-alcoholic options is increasing. Additionally, attractive packaging, varietal differentiation, and storytelling about craftsmanship further enhance perceived value. As product quality continues to improve, premium non-alcoholic wines are likely to attract both occasional drinkers and dedicated wine enthusiasts seeking alcohol-free alternatives.

Category-wise Analysis

Product Type Analysis

The sparkling wine segment is a dominant force in the market, particularly favored for celebrations and as an alternative to traditional Champagne or Prosecco. The presence of carbonation helps to mask the thin mouthfeel often associated with de-alcoholized products, providing a sensory experience that is very close to the original. Brands like Henkell & Co. Sektkellerei KG and Schloss Wachenheim AG have seen high success in this category. Meanwhile, Red Wine remains the most challenging but high-demand segment, as consumers seek the complex tannins and oak profiles found in traditional Cabernets or Merlots. The Rosé Wine and White Wine segments are also seeing robust growth, driven by their popularity as light, refreshing daytime beverages in the HoReCa channel.

Packaging Type Insights

The glass bottles segment is the leading segment in Category-2, accounting for a dominant 81% market share in 2025. This leadership is justified by the consumer's deep-seated association of glass with premium quality and the traditional wine-drinking experience. Glass remains the preferred choice for formal dining and gift-giving, as it supports the ritual of cork removal and pouring. However, Cans is identified as the fastest growing segment through 2032. The shift is driven by the demand for convenience and the rise of outdoor drinking occasions where glass is often prohibited. Aluminum cans also align with the sustainability mandates of global organizations, appealing to a younger demographic that prioritizes environmental impact alongside portability.

Regional Insights

North America Non-Alcoholic Wine Market Trends and Insights

North America currently holds the leading market share of 38% in 2025, underpinned by a highly mature wellness culture and a massive demand for low-calorie beverage alternatives. The United States leads the region in terms of both innovation and consumption, with a strong presence of venture-capital-backed non-alcoholic beverage startups. Organizations like the National Restaurant Association have noted a significant increase in the number of restaurants offering dedicated non-alcoholic wine lists to cater to a more diverse clientele.

The innovation ecosystem in the U.S. and Canada is characterized by a high volume of D2C activity, with brands like Trinchero Family Estates and Constellation Brands aggressively expanding their NoLo portfolios. Regulatory clarity from the FDA regarding nutritional labeling has helped build consumer trust. Furthermore, the strong presence of fitness-oriented social influencers has helped de-stigmatize non-alcoholic drinking, positioning it as a sophisticated lifestyle choice rather than a compromise. The region's well-developed retail and e-commerce infrastructure ensures that North America remains the primary engine for global market value throughout the forecast period.

Asia Pacific Non-Alcoholic Wine Market Trends and Insights

Asia Pacific is identified as the fastest growing segment for the non-alcoholic wine market through 2033. This rapid expansion is primarily driven by the burgeoning middle class in China, India, and the ASEAN countries, who are increasingly adopting Western-style social drinking habits while remaining mindful of traditional cultural and religious values that often discourage alcohol. Australia and New Zealand are the regional leaders in production, with brands like Giesen Group Ltd pioneering high-quality de-alcoholized Sauvignon Blancs.

The growth dynamics in the region are further supported by a young, urbanized population and the rapid expansion of modern retail and e-commerce platforms. In Japan, the NoLo trend is well-established in the beer category and is now rapidly diversifying into wine. Manufacturing advantages in the region, combined with a rising interest in functional and health-fortified beverages, are attracting global players to set up regional distribution hubs. As the sober curious movement gains traction in major Asian metropolitan centers, the Asia Pacific region is poised to become a critical future battleground for both local producers and international groups like Treasury Wine Estates.

Competitive Landscape

The non-alcoholic wine market exhibits a moderately consolidated structure at the top tier, where a few global beverage conglomerates and established winery groups hold significant influence over global supply chains. Key market leaders like LVMH Moët Hennessy, Constellation Brands, and Diageo PLC leverage their massive distribution networks and marketing budgets to dominate the Supermarkets & Hypermarkets and HoReCa channels. These companies often employ strategies focused on strategic acquisitions of specialized boutique brands to diversify their portfolios and capture the premium market segment. However, the market remains highly dynamic at the regional level, with a vibrant array of artisanal players like ZERONIMO and Pierre Chavin driving innovation in flavor profile and craft appeal. Key differentiators include the use of proprietary de-alcoholization technology and the attainment of sustainability certifications. Emerging business models are increasingly prioritizing D2C sales and social media-led marketing to build strong brand communities and bypass traditional retail gatekeepers.

Key Developments:

- In January 2026, O’Neill Vintners & Distillers (FitVine Wine) launched FitVine Free, a functional verjus-based non-alcoholic wine, positioning itself as a purpose-driven, wellness-focused innovation in the alcohol-free wine segment.

- In December 2025, Abrau-Durso Group introduced a non-alcoholic still wine, expanding its portfolio beyond traditional sparkling offerings and strengthening its presence in the evolving low- and no-alcohol beverage category.

- In October 2025, Moët Hennessy announced a strategic minority investment in French Bloom, reinforcing its expansion into premium non-alcoholic sparkling wines and enhancing its portfolio of luxury alcohol-free beverages.

Companies Covered in Non-Alcoholic Wine Market

- LVMH Moët Hennessy

- Pernod Ricard SA

- Constellation Brands

- Diageo PLC

- Campari Group

- Treasury Wine Estates Ltd

- Giesen Group Ltd

- ZERONIMO

- Trinchero Family Estates

- Schloss Wachenheim AG

- Henkell & Co. Sektkellerei KG

- Miguel Torres S.A

- Heineken N.V.

- Pierre Chavin

- Others

Frequently Asked Questions

The global Non-Alcoholic Wine market is projected to be valued at US$ 5.7 Bn in 2026.

Rising Health Consciousness Driving Shift Toward Zero Alcohol Beverages is a major factor driving the global Non-Alcoholic Wine market.

The Global Non-Alcoholic Wine market is poised to witness a CAGR of 10.2% between 2026 and 2033.

Premiumization of Non-Alcoholic Wines Through Advanced Dealcoholization and Flavor Technologies is a significant opportunity in the Non-Alcoholic Wine market.

Major players in the Global Non-Alcoholic Wine market include LVMH Moët Hennessy, Pernod Ricard SA, Constellation Brands, Diageo PLC, Campari Group, Treasury Wine Estates Ltd, Giesen Group Ltd, and others