- Automation & Robotics

- Mobile Robot Charging Station Market

Mobile Robot Charging Station Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Robot Charging Station Market by Robot Type (Fixed, Mobile), Level of Charging (Level 1, Level 2, Level 3), Commercial Application (Parking Facilities, Airports, Retail Centers and Malls, Others), and Regional Analysis for 2026 - 2033

Mobile Robot Charging Station Market Size and Trend Analysis

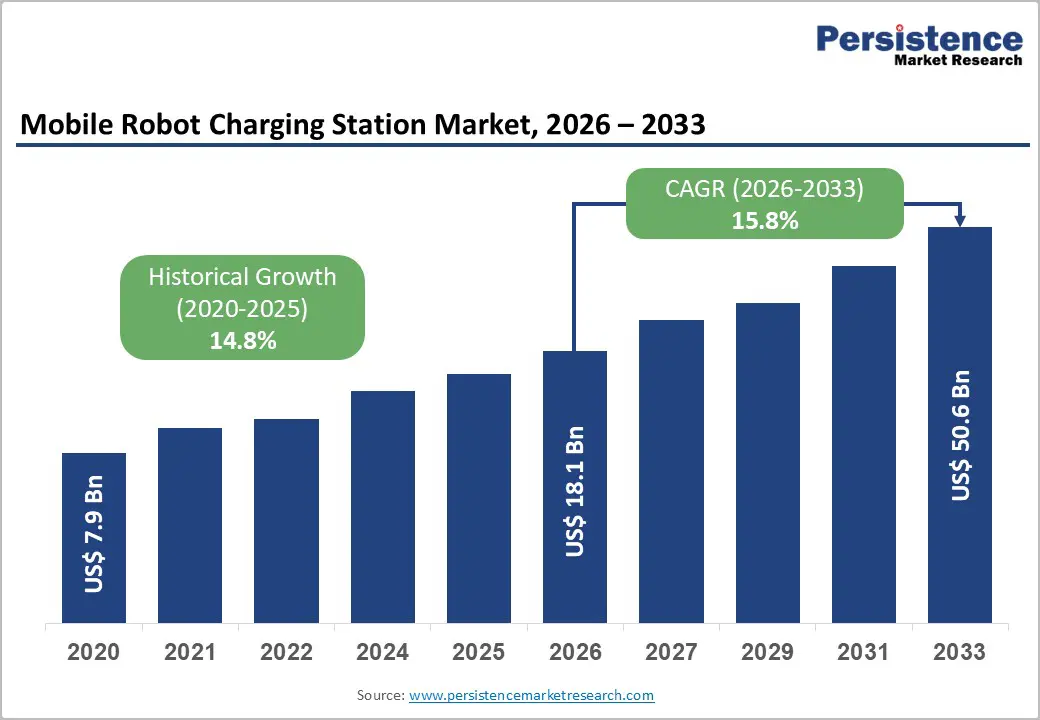

The global Mobile Robot Charging Station Market size is valued at US$ 18.1 billion in 2026 and is projected to reach US$ 50.6 billion by 2033, growing at a CAGR of 15.8% between 2026 and 2033.

This exceptional growth trajectory is driven by the structural convergence of global electric vehicle adoption, the critical infrastructure gap between deployed EV fleet volumes and available charging capacity, and the accelerating commercial deployment of AI-enabled autonomous robotic charging systems that eliminate human intervention from the EV charging process entirely.

Key Industry Highlights:

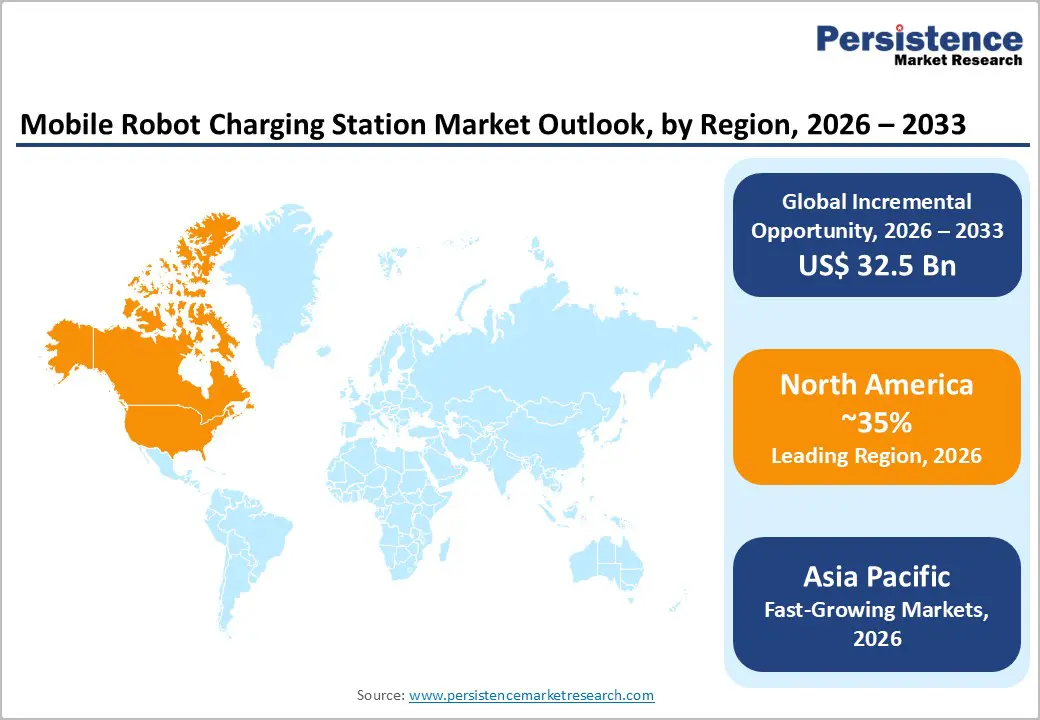

- Leading Region: North America leads the global Mobile Robot Charging Station Market with a projected CAGR of 15.4%, underpinned by the US$ 7.5 Bn Bipartisan Infrastructure Law EV charging allocation, the NEVI Formula Program, and EEI's confirmed need for 1.9 million Level 2 chargers in the U.S. by 2030.

- Fastest Growing Region: Asia Pacific is the fastest-growing region at a projected CAGR of 18.3%, driven by China's EV penetration exceeding 50% of new car sales in late 2024, Hyundai's commercial ACR deployment in South Korea, and India's mandatory EV charging infrastructure guidelines under the Ministry of Power.

- Leading Segment: The Mobile robot type segment dominates the Mobile Robot Charging Station Market with approximately 58% of total market share in 2026, as autonomous multi-vehicle servicing capability delivers superior infrastructure ROI over fixed robotic systems in high-density commercial parking environments.

- Fastest Growing Segment: Level 2 Charging is the dominant and fastest-deployable charging level segment, accounting for approximately 52% of market share in 2026, confirmed by EEI's projection of 1.9 million Level 2 units needed in the U.S. by 2030 as the primary infrastructure buildout category within national EV transition roadmaps.

- Opportunities: The most significant market opportunity lies in autonomous vehicle fleet integration and commercial fleet operator procurement with ROCSYS's 2024 logistics fleet deployment and Electrify America's autonomous robotic pilot confirming that hands-free robotic charging is the essential infrastructure enabler for commercially scalable autonomous EV fleet operations.

| Key Insights | Details |

|---|---|

|

Mobile Robot Charging Station Market Size (2026E) |

US$ 18.1 Bn |

|

Market Value Forecast (2033F) |

US$ 50.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

15.8% |

|

Historical Market Growth (CAGR 2020 to 2024) |

14.8% |

Market Dynamics

Drivers

Widening EV Charging Infrastructure Gap Creating Structural Demand for Autonomous Robotic Charging Deployment

The accelerating global transition to electric mobility is generating a critical and widening gap between the pace of EV fleet deployment and the density of available charging infrastructure, establishing an urgent structural demand environment for the Mobile Robot Charging Station Market. The Edison Electric Institute (EEI) confirmed in its 2024 report that as of August 2024, approximately 140,000 direct current fast chargers (DCFCs) and 1.9 million Level 2 chargers will need to be installed in the United States alone between the present and 2030 to meet projected demand a scale of deployment that requires infrastructure solutions capable of maximizing spatial coverage within constrained real estate. In Europe, the European Automobile Manufacturers' Association (ACEA) estimates that 8.8 million public charging points will be required by 2030, necessitating the installation of approximately 22,438 charging points per week, a pace far exceeding current network buildout rates.

AI and Robotics Technology Maturation Enabling Commercial Deployment of Hands-Free Autonomous Charging

The commercial readiness of autonomous robotic EV charging is advancing rapidly from prototype to deployment-grade systems, driven by maturation of AI-powered vision systems, robotic arm precision engineering, and car-to-infrastructure communication protocols that together enable fully hands-free vehicle charging. Hyundai Motor Group first introduced its Automatic Charging Robot (ACR) in 2023, utilizing a 3D camera-based AI algorithm to locate vehicle charging ports in all environmental conditions including darkness and adverse weather, autonomously connecting and disconnecting charging cables and closing the port cover without human interaction capability the company's Head of R&D described as "a significant milestone in verifying the practical benefits" of robotic EV charging. Volkswagen Group Components developed a mobile charging robot prototype capable of fully autonomous navigation within parking structures, app-initiated or car-to-X communication triggered, able to simultaneously service multiple vehicles by transporting and connecting mobile energy storage units.

Market Restraints

High Capital Investment and Unit Cost of Autonomous Robotic Charging Hardware Limiting Near-Term Deployment Scale

The primary commercial barrier constraining broader adoption within the Mobile Robot Charging Station Market is the substantial upfront capital requirement associated with designing, manufacturing, deploying, and maintaining autonomous robotic charging units relative to conventional fixed charging alternatives. Current-generation robotic charging systems require precision-engineered robotic arms, high-resolution 3D AI vision systems, mobility platforms, embedded connectivity hardware, and integration software collectively producing hardware costs that significantly exceed standard AC or DC fast-charging stations. For commercial operators in price-sensitive markets including South and Southeast Asia and Latin America, this capital intensity creates prohibitive payback periods, constraining deployment to high-throughput premium parking and fleet environments where utilization rates justify the investment.

Absence of Universal Charging Protocol Standards Impeding Cross-Platform Robotic Interoperability

The Mobile Robot Charging Station Market faces a meaningful near-term technical restraint in the absence of universally adopted standards governing vehicle-to-robot communication, robotic arm connector compatibility, and car-to-X protocol interfaces required for fully autonomous hands-free charging across heterogeneous EV models. Volkswagen identified car-to-X communication as a prerequisite for its mobile charging robot to achieve market maturity, while Hyundai's ACR system requires specific AI-calibrated port recognition for each vehicle model type. The fragmented landscape of proprietary charging connectors including CCS, CHAdeMO, and Tesla NACS across global markets compounds interoperability complexity, increasing per-unit development costs and creating uncertainty for infrastructure investors committing capital to robotic charging deployment in multi-brand public environments.

Market Opportunities

Autonomous Vehicle Ecosystems and Smart Parking Infrastructure Creating an Integrated Demand Environment

The progressive commercialization of autonomous and semi-autonomous electric vehicles is creating a natural and technologically aligned demand environment for the Mobile Robot Charging Station Market, as fully driverless vehicle fleets require equally autonomous charging solutions to deliver genuinely uninterrupted end-to-end operational capability. Autonomous vehicles parked in designated self-driving zones cannot rely on human occupants to plug in charging cables, making robotic mobile charging stations a functional prerequisite for commercial AV fleet operations at scale.

Electrify America, in collaboration with Stable Auto in San Francisco, has already piloted autonomous robots that navigate parking lots, identify compatible EVs, and initiate charging without any human intervention establishing a proof-of-concept for integrated smart parking and autonomous charging that is replicable across commercial parking operators globally.

Commercial Fleet Operators in Logistics and Airport Ground Operations Seeking Scalable Automated Charging

Commercial fleet operators in logistics, e-commerce fulfillment, and airport ground services represent a structurally high-priority opportunity for the Mobile Robot Charging Station Market, combining high vehicle density, predictable charging schedules, centralized depot infrastructure, and strong management incentives to minimize labor costs and maximize vehicle uptime through automated charging.

The ROCSYS partnership with Autocar in March 2024 to deploy hands-free robotic charging for electric terminal tractors at port and logistics facilities demonstrates validated commercial interest from heavy-duty fleet operators in automating the charging process to eliminate shift-dependent manual plug-in labor and reduce operational interruption. Airport ground operations present a parallel high-value deployment environment, with electric ground support vehicles including baggage tugs, pushback tractors, and catering vehicles requiring frequent, rapid charging turnarounds between flights in environments where labor availability is a commercial constraint.

Category-wise Analysis

Robot Type Insights

The Mobile robot type segment holds the leading position in the global Mobile Robot Charging Station Market, commanding approximately 58% of total market share in 2026. Mobile robot chargers, capable of autonomous navigation within defined parking zones and service areas, are preferred over fixed robotic systems because their agility enables a single unit to sequentially serve multiple vehicles across a space without requiring dedicated hardware at each parking bay, delivering substantially superior return on deployed capital in high-density environments. Hyundai Motor Group's ACR system and Volkswagen Group's mobile charging robot both validate this architecture, with their autonomous navigation, AI-based port identification, and hands-free connection capabilities representing the commercial benchmark for the mobile segment.

Level of Charging Insights

The Level 2 charging segment leads the Mobile Robot Charging Station Market by charging level, accounting for approximately 52% of total market share in 2026. Level 2 charging, delivering between 7 kW and 22 kW of power through AC connections, represents the optimal technical and economic balance point for automated robotic charging stations deployed in commercial parking facilities, retail centers, airports, and fleet depots where vehicles remain stationary for 1 to 8 hours. The EEI confirmed that 1.9 million Level 2 chargers are required in the United States by 2030, representing the largest single infrastructure deployment category in the national EV charging roadmap. For robotic mobile charging systems, Level 2 power delivery is compatible with a wider range of battery chemistries and vehicle classes than DC fast charging, reducing per-unit hardware cost and broadening the addressable deployment environment while delivering sufficient energy transfer within typical commercial parking dwell times.

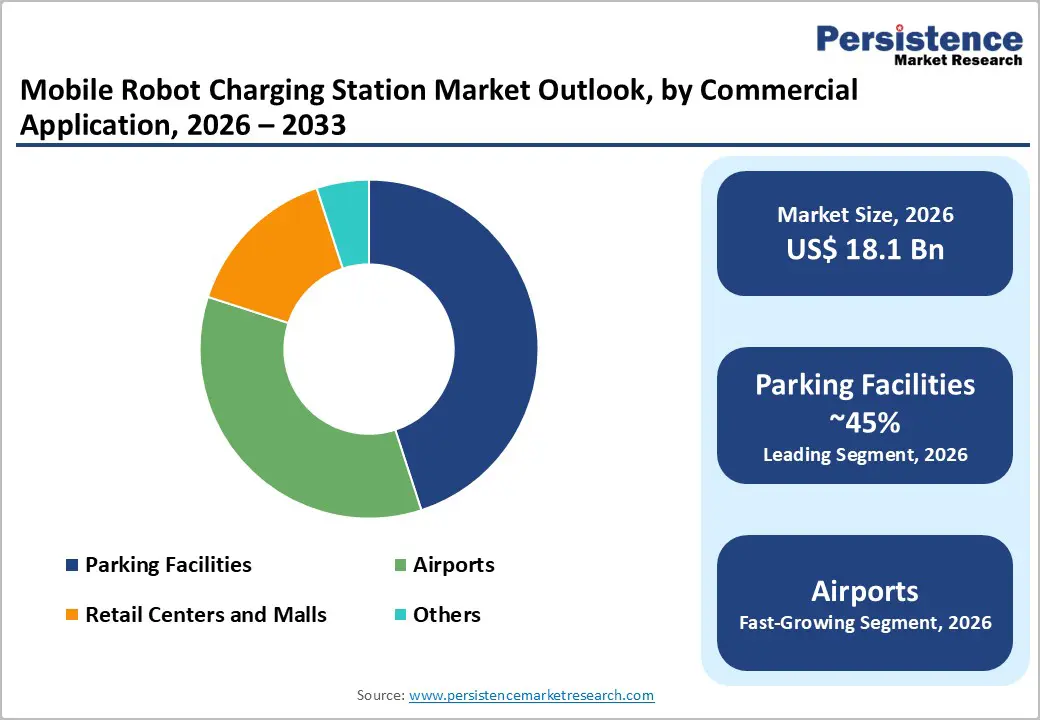

Commercial Application Insights

The Parking Facilities segment is the leading commercial application category within the Mobile Robot Charging Station Market, representing approximately 45% of total commercial application market share in 2026. Multi-story and surface parking facilities represent the most operationally aligned deployment environment for mobile robot charging systems, combining high vehicle density, controlled access boundaries within which autonomous robots can safely navigate, extended vehicle dwell times conducive to Level 2 and Level 3 charging, and commercial operator incentives to monetize previously passive parking spaces through value-added charging services. Volkswagen Group's early mobile charging robot prototype was explicitly designed for autonomous navigation within multi-vehicle parking structures, validating parking facilities as the primary deployment context for robotic mobile charging solutions.

Regional Insights

North America Mobile Robot Charging Station Trends

North America leads the global Mobile Robot Charging Station Market, with the United States anchoring regional leadership through its combination of extensive federal EV infrastructure investment, a technology-intensive innovation ecosystem, and one of the world's largest and fastest-expanding EV adoption markets. The Bipartisan Infrastructure Law allocated US$ 7.5 billion specifically for EV charging network development, with the Joint Office of Energy and Transportation administering the National Electric Vehicle Infrastructure (NEVI) Formula Program to deploy fast-charging stations along 75,000 miles of U.S. highway corridors.

Early commercial pilots including Electrify America and Stable Auto's autonomous robotic EV charging deployment in San Francisco confirm that North America's innovation ecosystem is actively advancing robotic charging from prototype to commercial service. Tesla's development of smart charger robotic arm prototypes and the strong U.S. venture capital environment supporting companies including ROCSYS, EV Safe Charge Inc., and Autev collectively reinforce the region's strategic position as both the primary demand market and the leading commercialization environment for mobile robotic EV charging technology globally.

Europe Mobile Robot Charging Station Trends

Europe is a structurally significant and policy-driven market for the Mobile Robot Charging Station Market, underpinned by the European Union's legally binding EV infrastructure mandates and the continent's deep industrial base in automotive and robotics engineering. The Alternative Fuels Infrastructure Regulation (AFIR), effective from April 2024, requires EU member states to deploy public fast-charging points of at least 150 kW every 60 kilometers along the TEN-T Core Network and 300 kW capacity at every TEN-T Core Network motorway service area by 2025, creating structured demand for high-throughput automated charging solutions across European transport corridors.

Germany and the United Kingdom lead European commercial innovation in the sector, with Volkswagen Group's robotic charging robot prototype developed by Volkswagen Group Components in Braunschweig representing Europe's most advanced OEM-developed autonomous charging system. ROCSYS, headquartered in the Netherlands, has established itself as a commercially active European robotic charging specialist with documented fleet operator partnerships.

Asia Pacific Mobile Robot Charging Station Trends

Asia Pacific is the fastest-growing regional market for the Mobile Robot Charging Station Market, driven by China's position as the world's largest EV market, Japan's automotive robotics engineering leadership, and India's rapidly accelerating EV transition supported by government-backed charging infrastructure mandates. According to Persistence Market Research, Asia Pacific is projected to advance at a CAGR of 18.3% through the forecast period, outpacing all other regions in growth velocity and establishing the region as the most commercially dynamic frontier for mobile robotic charging technology.

Hyundai Motor Group, headquartered in Seoul, South Korea, is one of the most technically advanced global OEMs in the robotic EV charging space, having unveiled its production-relevant Automatic Charging Robot (ACR) in 2023 and deploying it in partnership with Kia for commercial validation. Japan's domestic automotive and robotics companies including Mitsubishi Electric and Sony are investing in robotic and automated charging technologies aligned with the Japanese Government's roadmap for achieving 100% zero-emission new vehicle sales by 2035.

Competitive Landscape

The global mobile robot charging station market exhibits a fragmented competitive structure, comprising a diverse ecosystem of global automotive OEMs with in-house robotic charging development programs, dedicated EV charging technology startups, and established industrial robotics companies entering the autonomous charging space. Hyundai Motor Group, Volkswagen Group, and NaaS Technology represent the highest-profile tier of market participants by brand recognition and R&D investment scale. Key differentiators include AI-powered 3D vision system accuracy for multi-model vehicle port identification, autonomous navigation reliability in uncontrolled multi-user environments, and backward compatibility with existing charging protocol standards.

Key Developments:

- In May 2025, Hyundai Motor Group and Kia deployed commercially their Automatic Charging Robot (ACR) with the company's Head of R&D confirming the deployment as "a significant milestone in verifying the practical benefits" of fully autonomous robotic EV charging for consumer and fleet applications.

- In March 2024, ROCSYS partnered with Autocar to pilot hands-free robotic EV charging for electric terminal tractors, targeting fleet charging automation and operational efficiency improvement at logistics and port facilities, advancing commercial deployment beyond passenger vehicle applications.

Companies Covered in Mobile Robot Charging Station Market

- Hyundai Motor Group

- EV Safe Charge Inc.

- Mob-Energy S.A.S

- VOLTERIO GmbH

- ROCSYS

- NaaS Technology, Inc

- Volkswagen

- Autev

- EVAR Inc.

- ALVERI Ltd

- Other Key Players

Frequently Asked Questions

The global Mobile Robot Charging Station Market is valued at US$ 18.1 Bn in 2026 and is projected to reach US$ 50.6 Bn by 2033, growing at a CAGR of 15.8%.

The foremost drivers are the massive EV charging infrastructure gap with the EEI confirming 1.9 million Level 2 chargers needed in the U.S. by 2030 and ACEA estimating 8.8 million charging points required across Europe by 2030 and the commercial maturation of AI robotic charging technology exemplified by Hyundai's 3D camera AI Automatic Charging Robot and ROCSYS's commercial fleet deployment in March 2024.

The Mobile robot type segment leads, commanding approximately 58% of total market share in 2026. Mobile robotic chargers dominate because their autonomous navigation capability enables a single unit to service multiple vehicles sequentially across a parking zone without dedicated per-space hardware, delivering superior charging throughput per unit of deployed capital critical advantage given the ICCT's confirmation that public EV charging infrastructure must advance at 30% annually to meet demand.

North America leads the global Mobile Robot Charging Station Market with a projected CAGR of 15.4%, anchored by the U.S. Bipartisan Infrastructure Law's US$ 7.5 Bn EV charging allocation, the NEVI Formula Program deploying charging along 75,000 miles of U.S. highways, and active commercial robotic charging pilots by Electrify America and Stable Auto in San Francisco confirming North America as both the largest demand market and the leading innovation ecosystem for autonomous robotic charging.

Leading companies in the global Mobile Robot Charging Station Market include Hyundai Motor Group, Volkswagen Group, ROCSYS, NaaS Technology Inc., EV Safe Charge Inc., VOLTERIO GmbH, Mob-Energy S.A.S, Autev, EVAR Inc., ALVERI Ltd., Continental AG, Tesla Inc., Envision Group, Ford Motor Company, and ABB Ltd., spanning automotive OEMs, dedicated robotic charging specialists, and diversified industrial automation companies.