- Non-food Packaging

- Mobile Cases and Covers Market

Mobile Cases and Covers Market Size, Share, and Growth Forecast, 2026 - 2033

Mobile Cases and Covers Market by Product Type (Back Plate Cases, Folio/Flip Covers, Others), Material (Silicone, Genuine/PU Leather, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

Mobile Cases and Covers Market Size and Trends Analysis

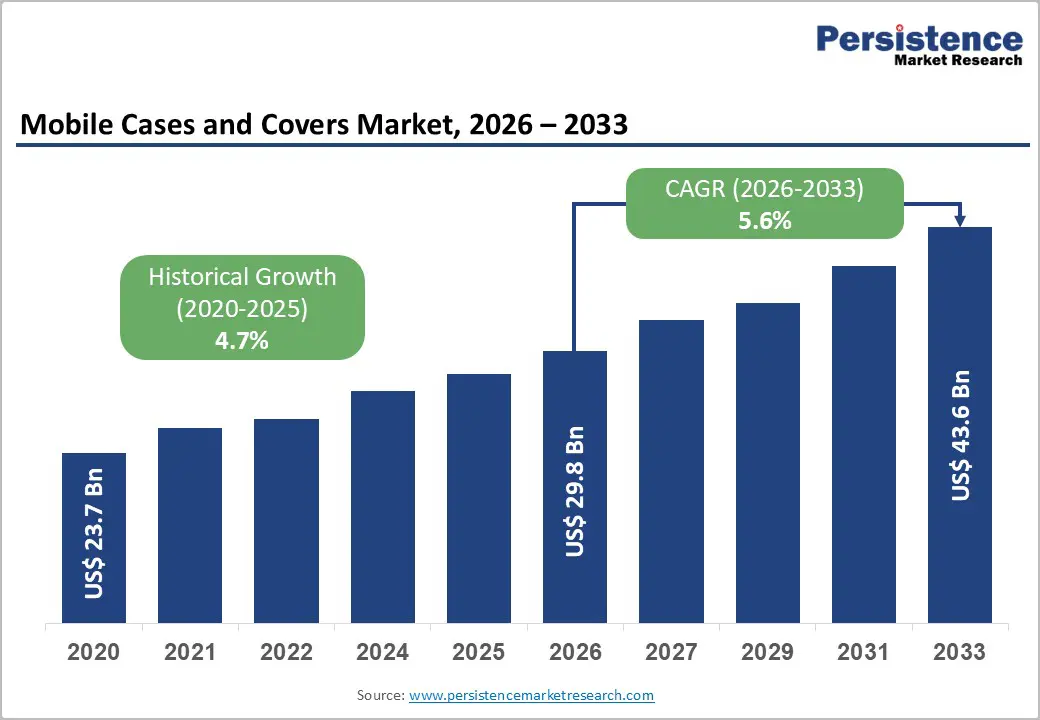

The global mobile cases and covers market size is likely to be valued at US$ 29.8 billion in 2026 and is expected to reach US$43.6 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, driven by sustained global smartphone shipments, longer device lifecycles that increase aftermarket spending on protective accessories, structural expansion of e-commerce distribution, and material innovation including eco-friendly polymers and ecosystem-compatible designs.

Margin expansion opportunities from premiumization are partially offset by price competition from low-cost manufacturers and volatility in raw material inputs. The market demonstrates resilience through diversified price tiers and omnichannel distribution.

Key Industry Highlights:

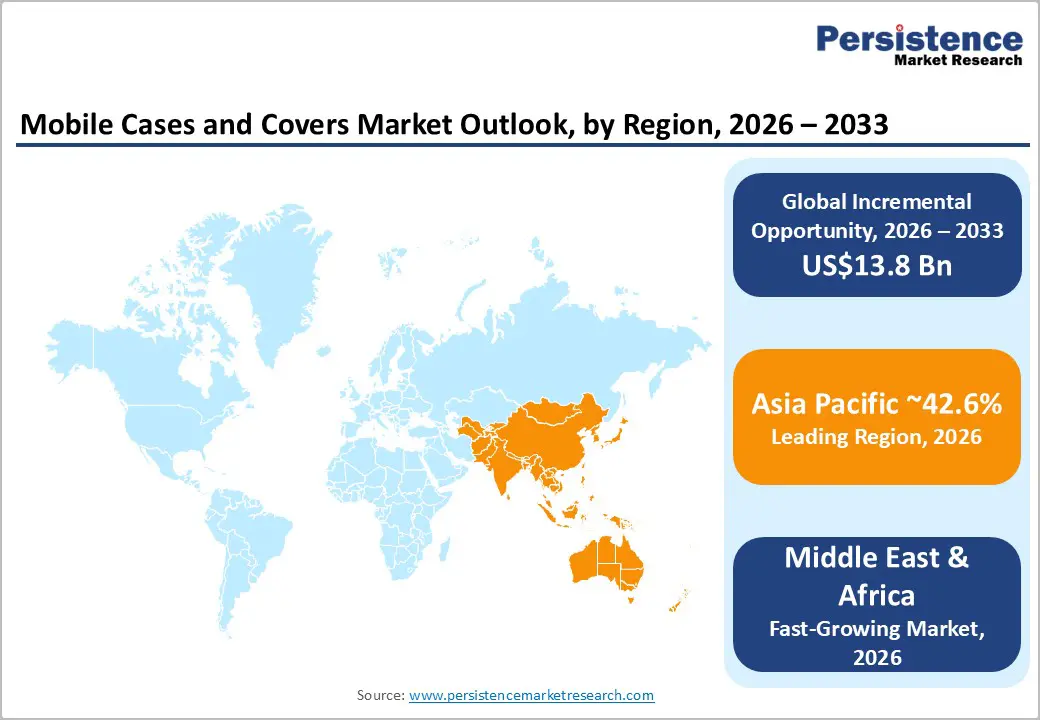

- Leading Region: Asia Pacific is projected to lead the global market with a 42.6% market share, supported by high smartphone volumes, strong manufacturing clusters, and expanding e-commerce penetration.

- Fastest-growing Region: The Middle East & Africa is projected to be the fastest-growing region through 2033, driven by rising premium smartphone adoption in GCC countries and improving retail and digital infrastructure across Africa.

- Investment Plans: Leading brands are investing in ecosystem-compatible designs, modular product architectures, and localized manufacturing partnerships, particularly in India and Southeast Asia, to strengthen supply chain resilience and expand regional presence.

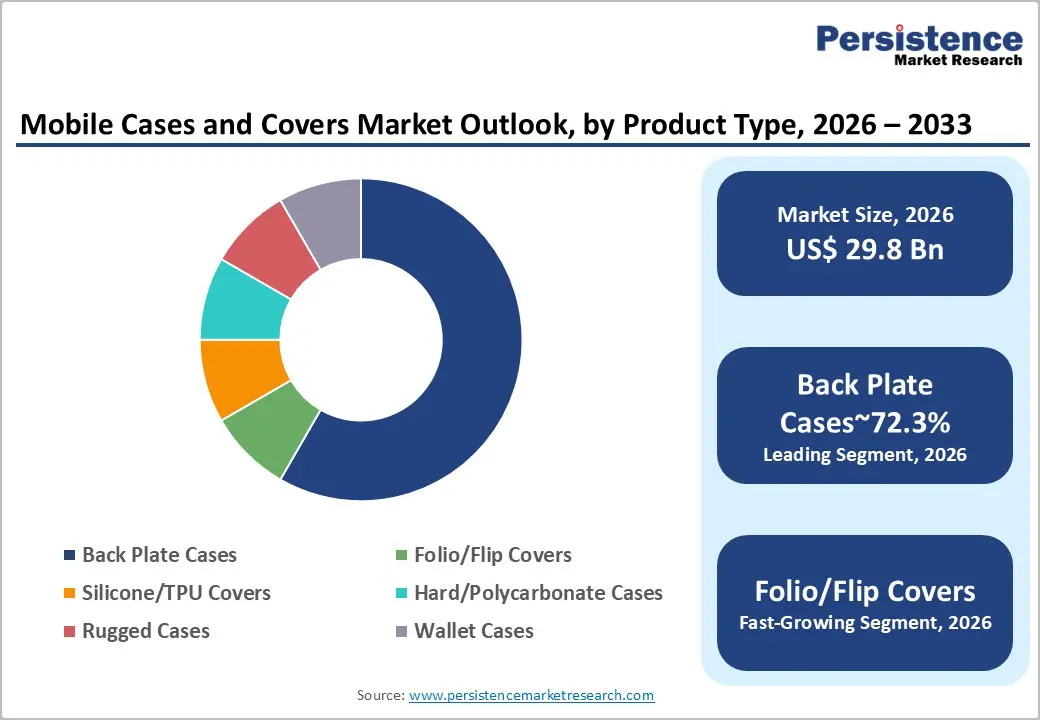

- Dominant Product Type: Back plate cases dominate the product type segment with an anticipated 72.3% market share, reflecting strong consumer preference for lightweight, scalable, and cost-effective protection solutions.

- Leading Material: Silicone materials lead the material segment with an anticipated 55.8% market share, supported by cost efficiency, durability, and high production scalability across mass-market SKUs.

| Key Insights | Details |

|---|---|

| Mobile Cases and Covers Market Size (2026E) | US$29.8 Bn |

| Market Value Forecast (2033F) | US$43.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Smartphone Penetration and Replacement Cycles

Smartphone unit shipments remain the primary demand catalyst for mobile cases and covers. Even modest shipment growth translates directly into incremental accessory demand. A 1-2% increase in global smartphone shipments typically generates low-single-digit growth in protective case demand, factoring in both new purchases and replacement cycles. Longer device ownership cycles are also reshaping consumer behavior. As users retain devices for extended periods, demand shifts toward durable and premium protective solutions, including rugged, hybrid, and multifunctional cases. This dynamic supports higher average selling prices (ASPs) even in moderate unit-growth environments. Stable shipment volumes combined with extended device usage drive recurring replacement demand and elevate the value mix toward premium SKUs.

Expansion of Online Retail and Direct-To-Consumer Channels

Global retail e-commerce penetration continues to expand, supporting structural channel transformation in consumer accessories. Online retail is the fastest-growing channel in this market, with a user-specified CAGR of 7.21%, outpacing offline retail growth. Digital marketplaces reduce distribution friction, enable personalization, and allow rapid product launches aligned with flagship smartphone releases. Direct-to-consumer (D2C) models provide brands with higher gross margins and deeper customer data insights. Cross-border fulfillment and print-on-demand services also expand long-tail device compatibility. Channel efficiency improves profitability for scaled brands while intensifying competition from private-label and unbranded manufacturers operating via global marketplaces.

Material Innovation and Ecosystem Integration

Innovation in materials and functionality continues to expand premium segments. Eco-materials such as biodegradable polymers, recycled plastics, and alternative leather finishes are gaining traction, particularly in developed markets with sustainability-focused consumers. Integration with smartphone ecosystems, magnetic alignment systems, wireless charging compatibility, modular wallet attachments, and protective certifications enhances product differentiation. Brands increasingly design cases compatible with emerging wireless standards and magnetic accessory systems. Functional and material innovation supports ASP growth, strengthens brand positioning, and creates defensible value propositions against commoditized low-cost products.

Barrier Analysis - Price Competition and Commoditization

The market remains structurally divided between premium branded products and high-volume, low-cost manufacturing concentrated in East Asia. Price-based competition exerts downward pressure on mid-tier brands lacking differentiation. In highly competitive online environments, ASP erosion of approximately 3-6% year-over-year is possible in commoditized segments. Currency volatility, shipping costs, and tariff adjustments further constrain margin protection.

Raw Material Volatility and Regulatory Compliance

Silicone, TPU, polycarbonate, and hybrid resins constitute the majority of case materials. Fluctuations in petrochemical feedstock prices increase cost variability. Chemical compliance regulations in major markets require certification, testing, and documentation, increasing operational complexity. Reformulation to meet regulatory standards may increase production costs by 1-2% for established suppliers and up to 3-6% for smaller manufacturers requiring retooling.

Opportunity Analysis - Premium Accessory Ecosystems

The integration of protective cases within broader smartphone accessory ecosystems is creating sustainable revenue expansion pathways. Manufacturers increasingly design cases compatible with magnetic wallets, modular kickstands, camera lens attachments, and wireless or magnetic charging platforms. This ecosystem-driven model strengthens cross-selling potential while reinforcing brand loyalty through accessory interoperability. Premium-compatible cases, including those certified for advanced charging or OEM-aligned magnetic systems, command higher average selling prices and improve margin resilience. Limited-edition collaborations, seasonal design drops, and personalization options further stimulate replacement demand beyond device upgrade cycles. These approaches reduce reliance on one-time protective purchases and extend customer lifetime value.

Emerging Market Premiumization

Rapid smartphone penetration across India, Southeast Asia, and the Middle East continues to expand the total addressable market for mobile protection accessories. Rising urbanization, expanding 4G and 5G coverage, and improving affordability of mid-range smartphones are increasing accessory attachment rates in these regions. As disposable incomes improve, consumers show a growing willingness to pay for branded, multifunctional, and aesthetically differentiated cases. Demand is shifting from basic protective covers toward hybrid protection, wallet integration, and design-driven SKUs aligned with regional preferences and OEM launch cycles. Localization of product portfolios and pricing structures strengthens competitive positioning.

Category-wise Analysis

Product Type Insights

Back plate cases are anticipated to account for 72.3% of the market share in 2026, reflecting sustained consumer preference for lightweight, slim-profile, and cost-efficient protection solutions. Their structural simplicity allows manufacturers to scale production across multiple smartphone models with minimal tooling adjustments, supporting rapid time-to-market during major OEM launches. This compatibility advantage strengthens their presence across both flagship and mid-range device segments. Retailers prioritize back plate designs due to high inventory turnover and SKU flexibility. Transparent and matte-finish variants complement OEM aesthetics, particularly for devices from brands such as Apple Inc. and Samsung Electronics, where consumers seek protection without obscuring original device design. Anti-yellowing coatings, reinforced corners, and MagSafe-compatible variants further expand value propositions within the category.

Folio and flip covers are projected to expand, driven by increasing demand for multifunctionality and premium styling. Integrated card slots, magnetic closures, adjustable stands, and full-screen protection elevate perceived value, positioning these products as lifestyle accessories rather than basic protective items. Corporate gifting programs, enterprise mobility deployments, and fashion-oriented consumer segments support growth in leather and leather-style folios. Premium smartphone users, particularly in business environments, prefer comprehensive protection solutions that reduce screen repair risk and consolidate wallet functionality. Brands such as Otter Products LLC and Spigen Inc. have expanded folio portfolios with RFID-blocking features and vegan leather alternatives, reflecting evolving consumer priorities around security and sustainability.

Material Insights

Silicone materials are anticipated to represent 55.8% of market share in 2026, supported by their cost efficiency, shock absorption properties, and high design adaptability. Silicone and thermoplastic polyurethane blends provide flexibility, impact dispersion, and scratch resistance while maintaining low production costs, making them suitable for large-volume SKUs targeting entry-level and mid-tier smartphones. Manufacturers leverage silicone’s molding flexibility to introduce textured grips, color gradients, and limited-edition patterns aligned with seasonal trends. Production scalability enables rapid replenishment cycles in offline retail channels and supports competitive pricing strategies. Leading accessory brands such as Belkin International integrate antimicrobial coatings and reinforced bumpers into silicone-based designs to enhance durability and hygiene performance.

Genuine and polyurethane leather materials are projected to grow, reflecting consumer preference for premium finishes and professional aesthetics. Leather cases command higher average selling prices and are frequently positioned within executive and corporate procurement categories. Their tactile finish and durability align with aspirational purchasing behavior in urban markets. Sustainability considerations increasingly shape material selection, particularly in North America and Europe, where traceable sourcing, recycled linings, and vegan leather certifications influence purchasing decisions. Premium collaborations and limited-edition launches, including designer-inspired collections by brands such as CASETiFY, reinforce leather’s role in premiumization strategies while expanding margins within the accessory value chain.

Regional Insights

North America Mobile Cases and Covers Market Trends - Premium Smartphone Ecosystems and High Accessory Attachment Rates Driving Value Growth

North America represents a substantial share of global market value, supported by high premium smartphone penetration and strong accessory attachment rates. The U.S. drives regional performance due to its mature retail infrastructure, high disposable income levels, and ecosystem-based purchasing behavior. According to data from the Consumer Technology Association, smartphone ownership in the U.S. exceeds 85% of adults, reinforcing recurring demand for protective accessories aligned with upgrade cycles. Flagship smartphone launches from Apple Inc. and Samsung Electronics continue to stimulate accessory renewal demand. The introduction of MagSafe-compatible iPhone models strengthened sales of MagSafe-compatible cases, wallets, and charging accessories, enabling brands such as Otter Products LLC and Belkin International to expand certified ecosystem portfolios. This ecosystem integration increases average selling prices and enhances brand loyalty.

Direct-to-consumer expansion and omnichannel integration also shape growth dynamics. Companies such as CASETiFY have expanded experiential retail locations in major U.S. cities while strengthening online customization platforms, reinforcing premium personalization trends. At the same time, large retailers, including Best Buy, continue to optimize in-store accessory merchandising linked to smartphone purchase bundles, increasing attachment rates at the point of sale. Corporate procurement and gifting programs provide incremental volume support, particularly for folio and leather-style cases aligned with professional use. Regulatory oversight from agencies such as the U.S. Consumer Product Safety Commission and chemical compliance frameworks at the state level raise compliance thresholds, limiting the influx of unverified imports and strengthening the competitive position of established brands with transparent supply chains.

Middle East & Africa Mobile Cases and Covers Market Trends - 5G Expansion and Youth-Driven Smartphone Adoption Accelerating Accessory Uptake

The Middle East & Africa (MEA) region is projected to be the fastest-growing market through 2033, supported by rising smartphone adoption in Gulf Cooperation Council economies and improving retail and logistics infrastructure across selected African markets. Expanding 5G deployment in countries such as the UAE and Saudi Arabia supports premium device uptake, increasing demand for higher-value accessory categories. In the Gulf region, premium smartphone penetration remains high, driven by flagship releases from Apple Inc. and Samsung Electronics. Retail groups such as Jarir Marketing Company have expanded electronics assortments and omnichannel capabilities, enabling broader distribution of branded protective cases. This retail modernization improves accessibility to certified ecosystem-compatible accessories, supporting premiumization trends.

Across Africa, growth stems from expanding smartphone penetration supported by brands such as Transsion Holdings, whose Tecno and Infinix devices target mid-range consumers. Rising device ownership increases demand for cost-effective silicone and hybrid cases. The expansion of cross-border e-commerce platforms, including Jumia, enhances product availability beyond major urban centers, accelerating online accessory adoption. Demographic factors further influence market performance. MEA has one of the youngest population profiles globally, strengthening demand for fashion-oriented and design-led mobile accessories. However, fragmented import regulations and certification standards across African markets require localized compliance strategies and distributor partnerships to mitigate customs and labeling risks.

Asia Pacific Mobile Cases and Covers Market Trends - Manufacturing Concentration and High Device Turnover Sustaining Market Leadership

Asia Pacific is projected to lead the market with a 42.6% share in 2026, combining large smartphone shipment volumes with highly concentrated manufacturing ecosystems. The region serves both as the primary consumption base and as a global production hub for mobile accessories, enabling scale efficiencies and rapid product iteration. China plays a dual role as a manufacturing center and a premium upgrade market. Accessory manufacturers clustered in Shenzhen supply global brands while supporting domestic OEM launches from companies such as Xiaomi Corporation and Huawei Technologies Co., Ltd. Rapid prototyping capabilities and vertically integrated supply chains shorten development cycles for new case designs following flagship device announcements. This agility reinforces Asia Pacific’s export competitiveness.

India represents one of the fastest-expanding smartphone markets, supported by government-led initiatives such as Make in India that encourage local electronics manufacturing. Production-linked incentive schemes have attracted investments from global suppliers serving brands including Samsung Electronics and Apple Inc. Growing mid-tier smartphone adoption increases demand for competitively priced silicone and back plate cases, while urban consumers demonstrate rising interest in premium and customized variants. Japan and ASEAN economies contribute through premium design collaborations and strong retail ecosystems. In Japan, consumer preference for minimalist aesthetics supports high-quality case brands with refined finishes. In Southeast Asia, marketplaces such as Shopee facilitate the rapid distribution of trend-driven designs, reinforcing personalization trends. High device turnover rates, strong e-commerce penetration, and manufacturing scalability underpin sustained growth. Regulatory compliance related to environmental standards and electronic waste management is strengthening, prompting suppliers to integrate recyclable materials and certified sourcing practices.

Competitive Landscape

The global mobile cases and covers market is moderately fragmented, combining global premium brands, regional manufacturers, and high-volume ODM exporters. Revenue concentration is higher in branded premium segments, while unit volumes are dispersed across private-label and marketplace sellers. Premium players differentiate through certified ecosystem compatibility, rugged certifications, and sustainable materials. Leading companies prioritize premiumization, ecosystem certification, omnichannel distribution, and material innovation. Rapid design refresh cycles aligned with smartphone launches are central to maintaining relevance and capturing attachment demand. Personalization and modular accessory ecosystems represent emerging competitive differentiators.

Key Industry Developments:

- In February 2026, Belkin expanded its accessory portfolio with a major ‘Designed for Samsung’ lineup for the Samsung Galaxy S26 series, including magnetic-ring integrated phone cases, screen protectors, and a 3-in-1 UltraCharge Modular Charging Dock supporting Qi2 wireless charging.

- In February 2026, Spigen launched the Classic LS MagFit Case in India for iPhone 17 Pro and Pro Max, featuring a retro design inspired by early Macintosh computers, integrated magnetic elements, and enhanced camera protection.

Companies Covered in Mobile Cases and Covers Market

- Apple Inc.

- Samsung Electronics

- Otter Products LLC

- Spigen Inc.

- Belkin International

- CASETiFY

- Incipio LLC

- Urban Armor Gear LLC

- ZAGG Inc.

- Tech21 UK Ltd.

- Ringke

- Nillkin

- Speck Products

- Mous Products Ltd.

- Anker Innovations

- Baseus

- X-Doria

- ESR

Frequently Asked Questions

The global mobile cases and covers market size is projected to be valued at US$ 29.8 billion in 2026.

The mobile cases and covers market is expected to reach US$ 43.6 billion by 2033.

The mobile cases and covers market is forecast to grow at a CAGR of 5.6% between 2026 and 2033.

Key trends include ecosystem-compatible and magnetic accessory integration, premium material adoption such as leather and hybrid composites, rapid growth in online retail (7.21% CAGR), localized SKU development in emerging markets, and increased demand for sustainable and recyclable materials.

Back plate cases lead the product type segment with an anticipated 72.3% market share, owing to their lightweight design, affordability, and compatibility across diverse smartphone models.

Major players include Apple Inc., Samsung Electronics, Otter Products LLC, Belkin International, and Spigen Inc.