- Industrial Machinery

- Microbrewery Equipment Market

Microbrewery Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Microbrewery Equipment Market by Equipment Type (Brew Kettles, Fermenters, Kegs, Cooling Systems, Filters), End Use (Commercial Breweries, Brewpubs, Home Breweries), Application (Beer Production, Craft Brewing, Research & Development), Distribution Channel (Online Retail, Direct Sales, Distributors), and Regional Analysis for 2026 - 2033

Microbrewery Equipment Market Size and Trend Analysis

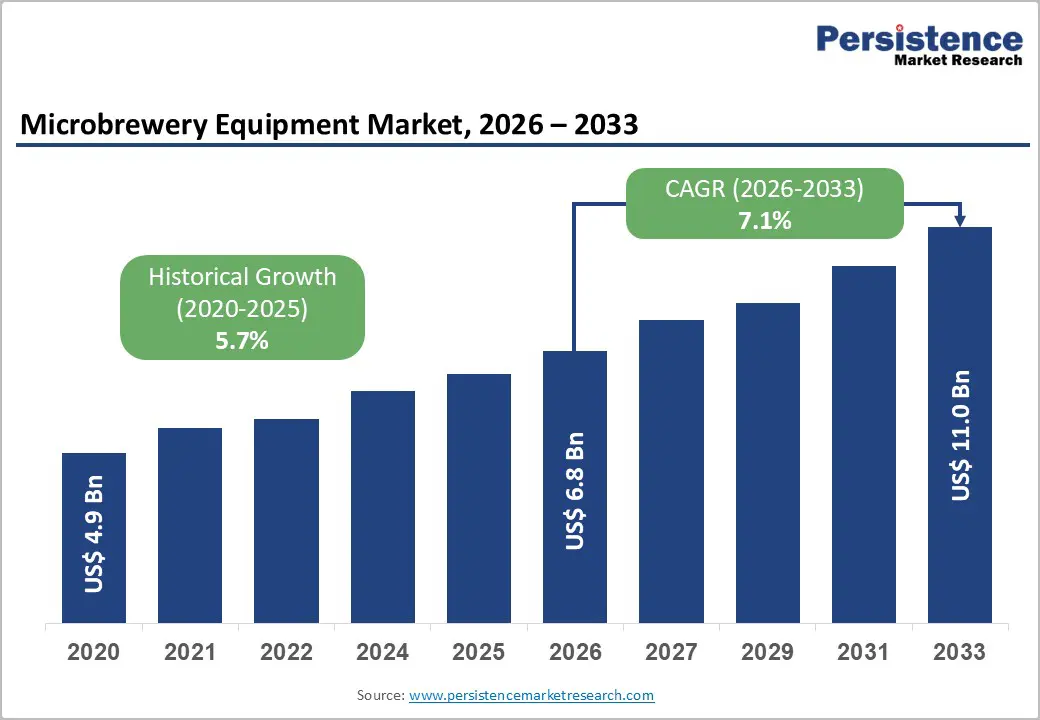

The global microbrewery equipment market size is valued at US$ 6.8 Bn in 2026 and is projected to reach US$ 11.0 Bn by 2033, growing at a CAGR of 7.1% between 2026 and 2033. This robust trajectory is driven by the global proliferation of craft breweries, rising consumer demand for artisanal and locally produced beer, and continuous investment in automation and energy-efficient brewing technologies.

According to the Brewers Association, craft beer's retail dollar value in the U.S. rose to an estimated USD 28.9 billion in 2024 accounting for 24.7% of the USD 117 billion total U.S. beer market creating sustained demand for specialized brewing equipment at both commercial and microbrewery scales.

Key Market Highlights

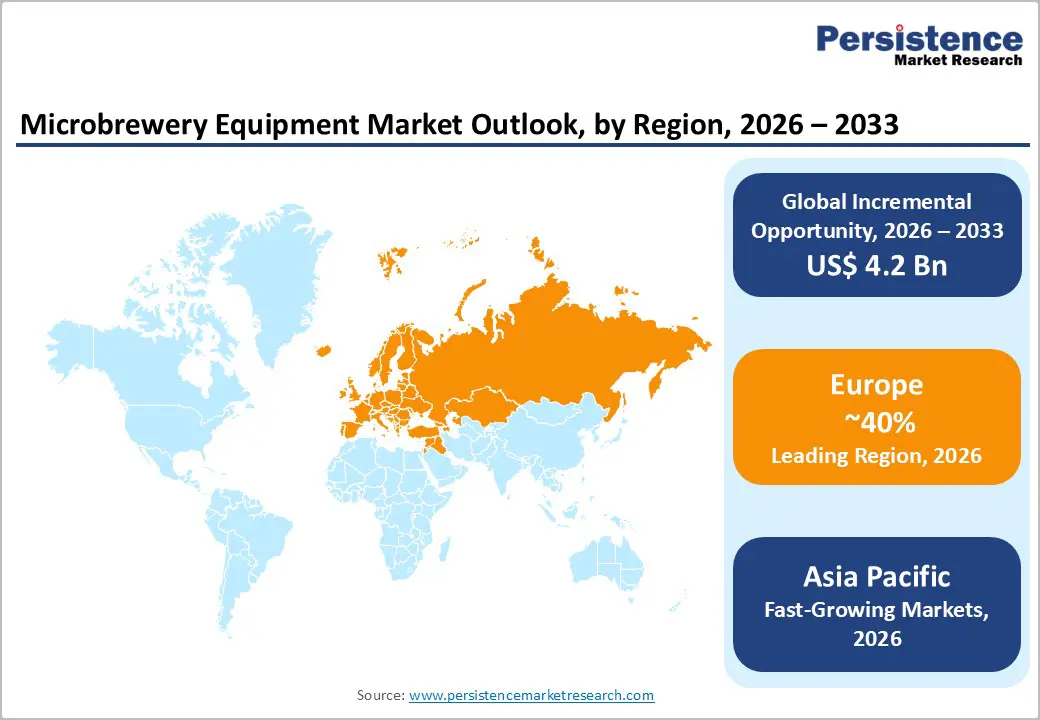

- Leading Region - Europe dominates with over 41% of global brewery equipment market share in 2025, underpinned by 9,680+ active breweries across the continent, a deep craft beer culture in Germany, the U.K., France, and Belgium, and strong sustainability-driven equipment upgrade activity.

- Fastest Growing Region - Asia Pacific leads growth driven by China's premiumization wave, India's craft brewery boom under favorable excise reforms, and a rising urban consumer base across ASEAN with India contributing 15.7% of the region's brewery equipment market.

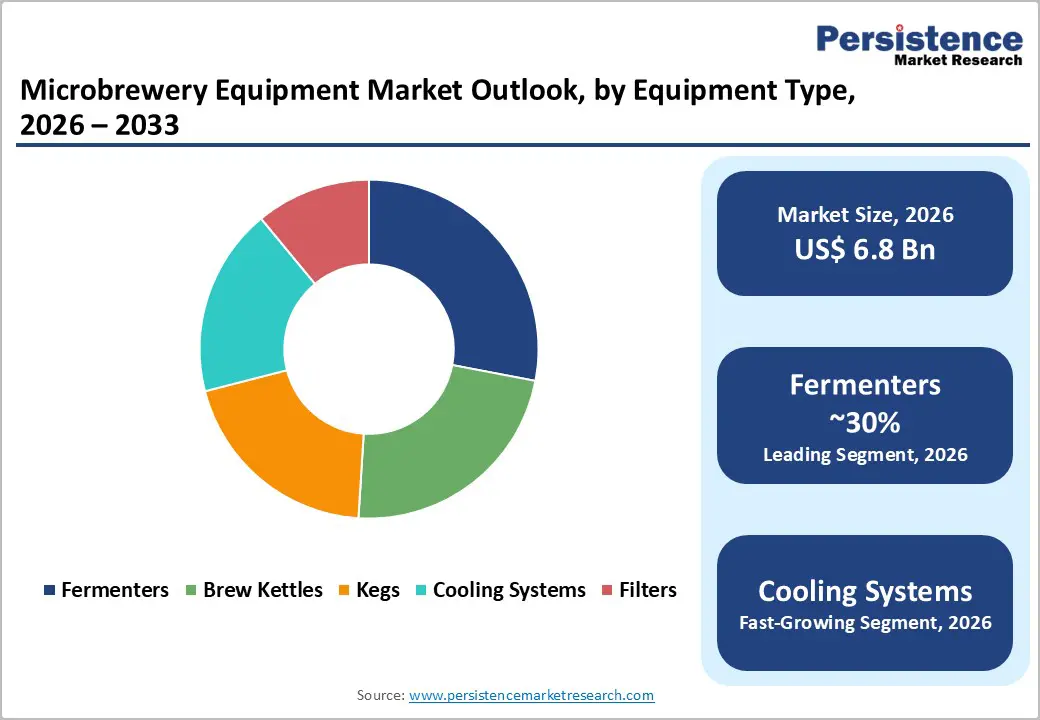

- Dominant Segment - Fermenters lead the equipment type category, as most microbreweries require 3-6 vessels per operational cycle. Closed conical and IoT-integrated fermenter systems are driving higher unit values across commercial brewery and brewpub segments globally.

- Fastest Growing Segment - Online retail is the fastest-growing distribution channel, enabling homebrewers and small commercial operators to access microbrewery equipment globally, with platforms like Amazon and specialized e-commerce sites rapidly expanding market reach into new geographies.

- Key Market Opportunity - Brewpub and Taproom Expansion + IoT-Enabled Equipment: Over 3,389 U.S. brewpubs and 3,695 taproom breweries in active operation, combined with rising Asia Pacific brewpub culture, are creating high-value equipment investment opportunities, enhanced by IoT-driven automation and energy efficiency product premiums.

| Key Insights | Details |

|---|---|

| Microbrewery Equipment Market Size (2026E) | US$ 6.8 Bn |

| Market Value Forecast (2033F) | US$ 11.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 5.7% CAGR |

DRO Analysis

Market Growth Drivers

Global Surge in Craft Brewery Establishments and Rising Craft Beer Culture

The single most powerful driver of the Microbrewery Equipment market is the sustained global proliferation of microbreweries and craft breweries. According to the Brewers Association, the U.S. alone hosted 9,612 operating craft breweries in 2024, including 1,934 microbreweries and 3,389 brewpubs each representing an active equipment investment opportunity.

Employment in the craft brewing sector grew to 197,112 in 2024, a 3.0% increase from the prior year, driven by the expansion of taproom and hospitality-focused models that require dedicated brewing infrastructure. The Brewers of Europe similarly reports approximately 9,680 active breweries across Europe, reflecting a deeply entrenched craft beer culture that continuously drives demand for brew kettles, fermenters, kegs, and filtration systems.

Technological Innovation Automation, IoT Integration, and Energy Efficiency

Rapid advances in brewing technology are amplifying equipment investment across all scales of microbrewery operations. The adoption of automated brewing systems which enable precise control of temperature, pressure, fermentation timing, and cleaning cycles has fundamentally lowered the operational expertise barrier for new entrants, broadening the addressable customer base. Automatic brewing equipment held approximately 43% of the microbrewery equipment market share in 2024, according to industry data, as operators prioritize consistency and quality at scale.

The integration of IoT (Internet of Things) sensors and cloud-based monitoring platforms allows brewmasters to track fermentation in real-time and implement predictive maintenance, reducing downtime and waste. Simultaneously, energy-efficient equipment including heat recovery systems, CO2 capture systems, and water-recycling filtration units is gaining commercial traction as sustainability becomes a core operational priority.

Market Restraints

High Capital Expenditure and Tight Profit Margins for Small Breweries

Microbreweries and brewpubs operate in a highly competitive environment with notoriously thin profit margins, making significant upfront capital investment in brewing equipment a persistent restraint. A complete microbrewery setup encompassing brew kettles, fermenters, cooling systems, kegs, and filtration units can require investment ranging from tens of thousands to several hundred thousand dollars, depending on capacity and automation level.

According to the Brewers Association, tariffs on imported brewing equipment, steel kegs, and aluminum cans have exacerbated financial pressures for small and independent breweries in 2024, forcing many to delay expansion plans or absorb losses, directly limiting equipment procurement activity. The closure rate while low at approximately 5% in 2024 reflects the fragility of marginally profitable operators in this segment.

Stagnating Craft Beer Volume Growth in Mature Markets

The craft beer category is facing volume headwinds in its most established markets, dampening the urgency of equipment investment. The Brewers Association reported that U.S. craft brewers produced 23.1 million barrels of beer in 2024, representing a 4.0% decline from 2023, while the total number of operating craft breweries dropped nationwide for the first time since 2005.

Over the year, 434 new breweries opened while 501 closed, reflecting a maturing and increasingly competitive market. Volume deceleration in North America and parts of Europe is prompting operators to prioritize operational efficiency over capacity expansion tempering demand growth for new equipment in these key established markets, though it simultaneously drives demand for retrofit and upgrade solutions.

Market Opportunities

Rapid Microbrewery Expansion Across Asia Pacific and Emerging Economies

The most compelling near-term growth opportunity for Microbrewery Equipment market participants lies in the accelerating adoption of craft beer culture across Asia Pacific, Latin America, and Africa. India's craft brewery sector is expanding rapidly on the back of rising disposable incomes, a growing urban middle class, and favorable regulatory reforms at the state level that are progressively enabling microbrewery-licensed operations.

China the world's largest beer market by volume and the world's largest vehicle of beer production is simultaneously witnessing the emergence of a premium craft beer segment, driving demand for small-batch brewing equipment. Multiple leading players attended the Craft Beer China Conference & Exhibition 2025, Asia Pacific Convention IBD 2025, and the flagship drink Tec 2025 trade event, underscoring growing industry engagement with Asia Pacific markets.

Brewpub, Taproom, and Online Retail Distribution Channel Growth

The rapid shift toward hospitality-integrated brewing models including brewpubs, taproom breweries, and brewpub-restaurants is generating incremental equipment demand that extends beyond pure production capacity investments. The Brewers Association data confirms that employment growth in the U.S. craft brewing sector in 2024 was driven primarily by hospitality-focused models, with 3,389 brewpubs and 3,695 taproom breweries in active operation. Each new brewpub or taproom establishment requires a fully integrated equipment set from brew kettles and fermenters to kegs and cooling systems and typically invests in mid-tier, aesthetically optimized, space-efficient brewing setups.

Simultaneously, the Online Retail distribution channel is emerging as the fastest-growing procurement avenue for microbrewery equipment, particularly for home brewing and smaller commercial operators. Platforms including Amazon and specialized beverage equipment e-commerce sites are expanding market reach into previously underserved geographies.

Category-wise Analysis

Equipment Type Insights

Fermenters represent the dominant segment in the Microbrewery Equipment market by equipment type, commanding approximately 28% of total market share. This leadership position reflects the fundamental and indispensable role fermentation vessels play in every beer production cycle it is during fermentation that yeast converts sugars into alcohol and carbon dioxide, defining a beer's character, flavour, and quality.

Most microbreweries require between three to six fermenter vessels to maintain continuous production cycles while simultaneously accommodating multiple beer styles at different stages. The strong market position of fermenters is further reinforced by increasing investment in closed conical fermenters which dominate craft brewery adoption due to their versatility, ease of yeast harvesting, and cleanability and innovation in specialty barrel fermenters for premium small-batch offerings.

End Use Insights

Commercial Breweries hold the dominant position in the Microbrewery Equipment market by end use, accounting for approximately 55-60% of total market share. This leadership is anchored by the consistent and high-volume procurement patterns of commercial-scale craft and microbrewery operators, who invest in full-system setups incorporating brewhouses, fermenters, kegs, cooling systems, and filtration lines.

Commercial breweries operate under regulatory quality standards including compliance with TTB (Alcohol and Tobacco Tax and Trade Bureau) regulations in the U.S. and comparable frameworks globally that mandate professional-grade, validated equipment meeting food safety and sanitation requirements. The rising number of commercial craft breweries globally, with the Brewers Association tracking over 9,600 active U.S. breweries in 2024, sustains strong demand for equipment procurement, upgrades, and replacement cycles.

Application Insights

Beer Production remains the dominant application segment in the Microbrewery Equipment market, commanding approximately 62% of overall market share. This dominance is a direct reflection of the scale and consistency of beer brewing as the primary commercial use case for microbrewery equipment globally, spanning core lager, ale, stout, and IPA production across both commercial breweries and brewpubs.

The U.S. beer market was valued at USD 117 billion in 2024 according to Brewers Association data, with craft beer contributing 24.7% of that value, providing a substantial commercial foundation for ongoing equipment investment in standard beer production applications. The Craft Brewing application sub-segment, while smaller, is expanding rapidly as consumer preferences shift toward experimental small-batch styles, specialty ingredients, and limited-edition seasonal releases all of which require versatile, multi-use brewing equipment configurations that support frequent recipe changes.

Distribution Channel Insights

Direct Sales dominate the Microbrewery Equipment market by distribution channel, holding approximately 55% of total market share. This channel dominance reflects the highly customized, consultative nature of commercial brewery equipment procurement, where operators work directly with manufacturers or specialized dealers to design, configure, and commission complete brewing systems tailored to their specific production capacity, floor plan, and style requirements.

Direct sales relationships are particularly entrenched among commercial breweries purchasing mid-to-large system configurations, where technical support, warranty management, and commissioning services are critical differentiators. Leading manufacturers including GEA Group, Krones AG, Alfa Laval, and PAUL MUELLER COMPANY maintain dedicated direct sales and engineering support teams globally.

Regional Analysis

Europe

Europe is the world's largest regional market for microbrewery equipment, representing over 41% of global brewery equipment revenue in 2025, driven by a deeply embedded craft beer culture and the highest density of active breweries globally. The Brewers of Europe reported approximately 9,680 active breweries across the continent in 2022, with Germany, the U.K., France, Belgium, and Czech Republic leading in brewery counts. Germany's centuries-old brewing tradition, anchored by the Reinvestigate purity law, continues to generate substantial demand for high-precision brewing equipment from both traditional lager brewers and a fast-growing craft segment. The U.K. has witnessed significant craft brewery proliferation, with the Society of Independent Brewers (SIBA) tracking thousands of independent breweries that invest regularly in small-batch brewing equipment and keg systems.

France and Spain are emerging as high-growth microbrewery markets, with increasing consumer openness to craft beer alternatives to wine and lager traditions. European Union sustainability directives and energy efficiency regulations are compelling breweries to upgrade to modern, low-energy cooling systems, heat recovery kettles, and automated cleaning systems driving premium equipment sales.

Asia Pacific

Asia Pacific is the fastest-growing regional market for microbrewery equipment, propelled by rapidly expanding craft beer culture in China, Japan, India, and across ASEAN nations. China the world's largest beer market by volume is experiencing a significant premiumization wave, with consumers increasingly seeking locally crafted, artisanal beers over mass-produced lagers. This shift is spurring investment in microbrewery equipment across an expanding network of urban craft breweries and brewpubs, particularly in Beijing, Shanghai, Chengdu, and Guangzhou.

India is the most dynamic emerging sub-market, with the country's craft brewery sector accelerating on the back of favorable state-level excise policy reforms, rising disposable incomes, and a rapidly expanding urban millennial consumer base. The India brewery equipment sub-market contributed approximately 15.7% of the Asia Pacific total in 2024. Southeast Asian markets particularly Vietnam, Thailand, and Indonesia are emerging as new frontiers for microbrewery and brewpub investment, benefiting from growing tourism, rising middle class beer consumption, and expanding hospitality sectors.

North America

North America is one of the world's most established and dynamic markets for microbrewery equipment, anchored by the United States' extraordinarily mature craft beer ecosystem. According to the Brewers Association, the U.S. had 9,612 operating craft breweries in 2024 including 1,934 microbreweries, 3,389 brewpubs, and 3,695 taproom breweries representing a vast installed base of brewing equipment and a continuous replacement and upgrade cycle. Craft beer's retail dollar value reached USD 28.9 billion in the U.S. in 2024, accounting for 24.7% of the total beer market, reflecting the sector's commercial significance and its capacity to sustain equipment investment.

Regulatory frameworks administered by the Alcohol and Tobacco Tax and Trade Bureau (TTB) and individual state licensing bodies continue to shape equipment standards and operational requirements for U.S. microbreweries. The innovation ecosystem is robust, with specialized equipment manufacturers including Portland Kettle Works, ABE Equipment, and Ampco Pumps Company actively developing advanced brewing systems. Canada contributes incremental growth driven by craft brewery expansion in Ontario, British Columbia, and Quebec.

Competitive Landscape

The global Microbrewery Equipment market exhibits a highly fragmented competitive structure, spanning multinational industrial equipment leaders, specialized craft brewery equipment suppliers, and regional fabricators. Large players such as GEA Group, Alfa Laval, Krones AG, and PAUL MUELLER COMPANY leverage broad product portfolios, global service networks, and R&D capabilities to capture commercial and high-capacity microbrewery segments.

Key competitive differentiators include system automation levels, energy efficiency ratings, digital integration capabilities, and application-specific engineering expertise.

Key Market Developments

- In July 2025, Alfa Laval AB launched a new line of energy-efficient brewing equipment specifically designed to reduce water and energy consumption across microbrewery and craft brewery operations, targeting sustainability-focused operators globally.

- In September 2025, GEA Group AG completed the acquisition of a regional brewing equipment manufacturer, expanding its product portfolio and local service capabilities in Eastern Europe to address growing demand for tailored brewery solutions.

Companies Covered in Microbrewery Equipment Market

- ALFA LAVAL

- GEA Group Aktiengesellschaft

- Krones AG

- PAUL MUELLER COMPANY

- CRIVELLER GROUP

- DELLA TOFFOLA USA

- SCHULZ

- Hypro

- Praj Industries

- ABE Equipment

- Ampco Pumps Company

Frequently Asked Questions

The global Microbrewery Equipment market is valued at US$ 6.8 Bn in 2026 and is projected to reach US$ 11.0 Bn by 2033, growing at a CAGR of 7.1% during the forecast period.

The primary drivers include the global surge in craft brewery establishments with the Brewers Association reporting 9,612 operating U.S. craft breweries and craft beer's retail value reaching USD 28.9 billion in 2024 alongside growing adoption of automated and IoT-enabled brewing systems.

Fermenters dominate the Microbrewery Equipment market by equipment type, holding approximately 28% of total market share. Their dominance stems from their indispensable role in every beer production cycle and the fact that most microbreweries maintain 3-6 fermenter vessels to support simultaneous multi-style production.

Europe leads the global Microbrewery Equipment market, accounting for over 41% of global brewery equipment revenue in 2025. The region's dominance is driven by approximately 9,680 active breweries reported by the Brewers of Europe, a centuries-deep craft beer culture in Germany, Belgium, the U.K., and France, and active regulatory-driven equipment upgrade cycles under EU energy efficiency and sustainability directives.

The leading companies in the Microbrewery Equipment market include ALFA LAVAL, GEA Group Aktiengesellschaft, Krones AG, PAUL MUELLER COMPANY, CRIVELLER GROUP, DELLA TOFFOLA USA, SCHULZ , Hypro, Praj Industries, ABE Equipment, and Ampco Pumps Company.