- Metals & Minerals

- Metalworking Fluids Market

Metalworking Fluids Market Size, Share, and Growth Forecast 2026 - 2033

Metalworking Fluids Market by Product Type (Mineral-Based, Synthetic, Semi-Synthetic, Bio-Based), Fluid Type (Removal Fluids, Forming Fluids, Protecting Fluids, Treating Fluids), Industry (Automotive & Transportation, Aerospace, Machinery & Equipment, Metal Fabrication, Construction, Electrical & Power, Agriculture, Others), and Regional Analysis, 2026 - 2033

Metalworking Fluids Market Size and Trend Analysis

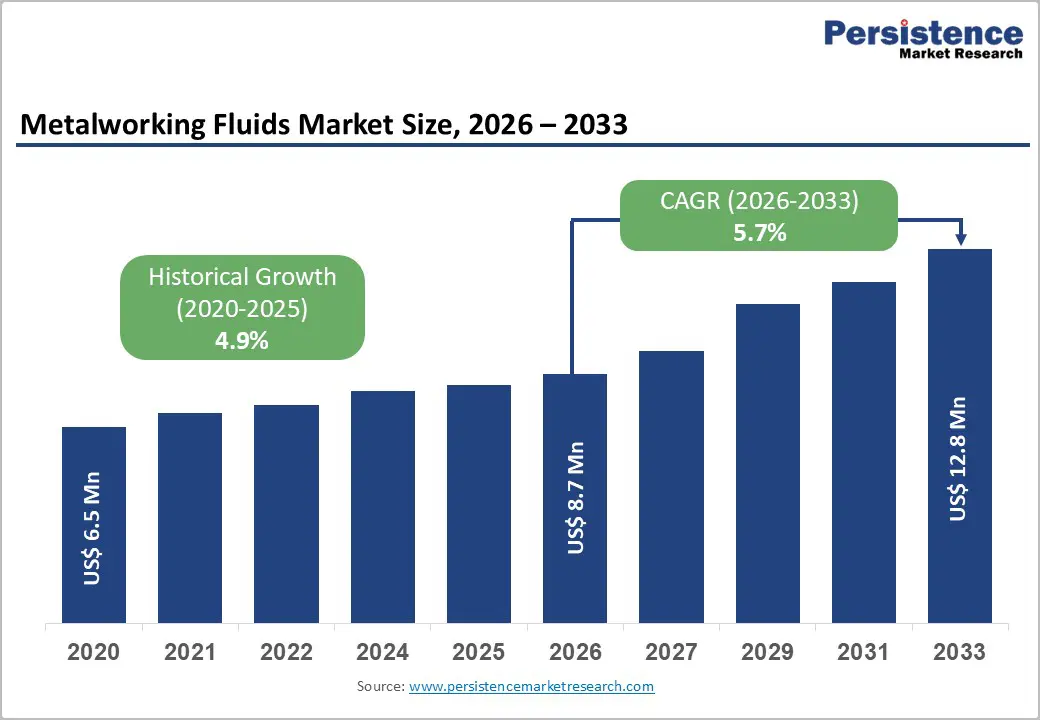

The global metalworking fluids market size is expected to be valued at US$ 8.7 billion in 2026 and projected to reach US$ 12.8 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

This sustained growth is primarily propelled by rising automotive and aerospace production volumes, the global expansion of precision machining operations, and growing regulatory and industrial pressure toward advanced synthetic and bio-based fluid formulations. According to the International Organization of Motor Vehicle Manufacturers (OICA), global automobile production reached approximately 93.5 million vehicles in 2023, generating sustained, high-volume demand for cutting, grinding, and forming fluids across automotive component manufacturing lines. Simultaneously, Airbus and Boeing projected combined aircraft deliveries of close to 1,550 units in 2025 versus 1,263 in 2024, substantially increasing titanium, nickel-alloy, and aluminum machining activity, all of which require high-performance metalworking fluid formulations to sustain tool life, cooling efficiency, and dimensional accuracy throughout demanding production cycles.

Key Industry Highlights:

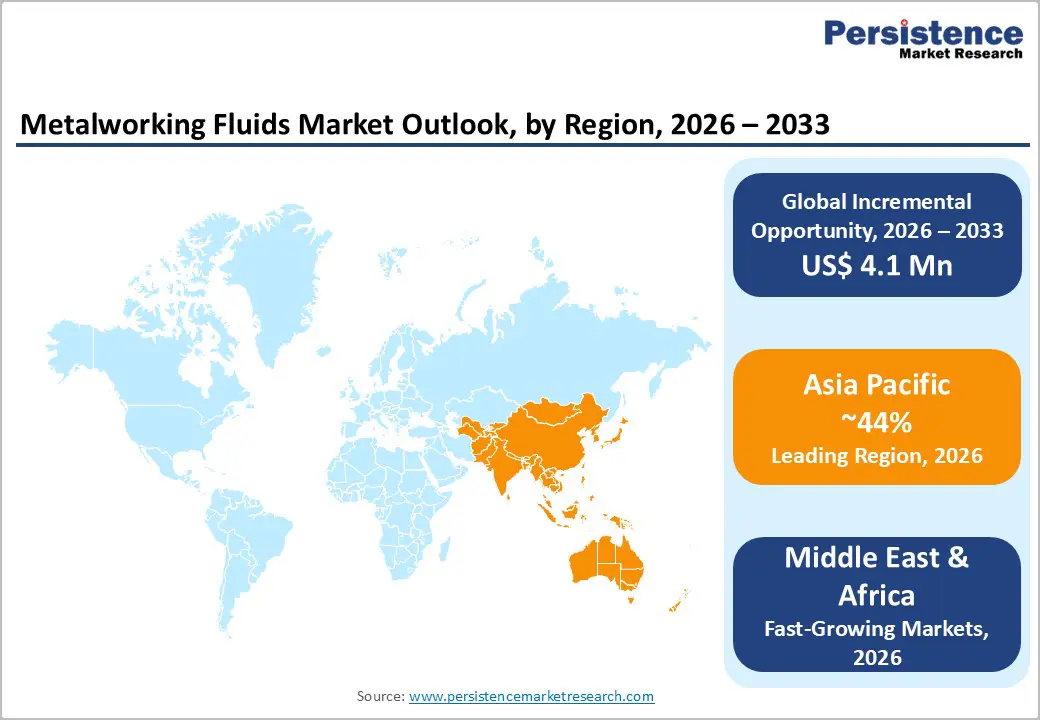

- Leading Region: Asia Pacific dominates the global Metalworking Fluids market with approximately 44% share in 2025, anchored by China's 93.5-million-unit automotive manufacturing capacity, Quaker Houghton's new Zhangjiagang facility, and India's fast-growing aerospace MRO sector.

- Fastest Growing Region: Middle East & Africa is the fastest-growing region through 2033, driven by diversification from oil revenues into manufacturing, GCC Vision programmes expanding aerospace MRO, and growing industrial equipment production requiring advanced metalworking fluid solutions.

- Dominant Segment: Removal Fluids lead with approximately 52% market share in 2025, indispensable across CNC turning, drilling, grinding, and milling operations in automotive and aerospace component production globally, sustaining dominant market position through 2033.

- Fastest Growing Segment: Bio-Based metalworking fluids are the fastest-growing product type, with over 125 new eco-friendly formulations launched globally in 2024, driven by REACH compliance, EPA VOC limits, and automotive OEM sustainability procurement mandates.

- Key Market Opportunity: The EV production ramp-up and aerospace delivery surge to 1,550 aircraft in 2025 are creating structural new demand for advanced synthetic and forming fluids engineered for aluminum alloys, titanium, and battery housing fabrication.

| Key Insights | Details |

|---|---|

| Metalworking Fluids Market Size (2026E) | US$ 8.7 Billion |

| Market Value Forecast (2033F) | US$ 12.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.9% |

DRO Analysis

Drivers - Expanding Automotive and Aerospace Manufacturing Activity

The automotive and transportation sector remains the dominant end-use driver of metalworking fluids consumption globally. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production surpassed 93.5 million units in 2023, recovering from post-pandemic supply chain disruptions while simultaneously transitioning toward electric vehicle (EV) platform manufacturing, which demands precision machining of battery housings, lightweight aluminum structures, and high-strength steel components. Over 40% of global metalworking fluid demand originates from automotive, aerospace, and heavy machinery sectors. In 2025, aerospace deliveries by Airbus and Boeing are projected at approximately 1,550 aircraft combined, sustaining elevated demand for advanced synthetic metalworking fluids engineered for titanium and nickel-alloy machining. In 2025, aerospace applications utilized over 18% more synthetic fluids compared to 2024, a clear indicator of the sector's accelerating specialization and fluid intensity.

Industrial Automation, Precision Machining, and Manufacturing Modernization

The global push toward industrial automation and smart manufacturing is fundamentally elevating metalworking fluid performance requirements, driving market growth in value terms. Automated CNC machining centres demand fluids with superior biostability, extended sump life, and consistent thermal management to minimize unplanned downtime in lights-out manufacturing environments. Quaker Houghton, the global leader in industrial process fluids with operations in over 25 countries, launched its QH FLUID INTELLIGENCE™ digital optimization platform in September 2024 at the International Manufacturing Technology Show (IMTS) in Chicago, enabling manufacturers to measure, control, and optimize fluid performance in real time. In its first operational year at a global automotive OEM, the platform delivered US$ 1.25 million in annual cost savings by eliminating downtime and reducing lubricant consumption by 27% per unit. Such digital-service-enhanced fluid offerings are redefining value propositions and deepening customer lock-in across automotive, aerospace, and precision engineering sectors through 2033.

Restraints - Stringent Environmental and Worker Safety Regulations Driving Reformulation Costs

Metalworking fluids are subject to an increasingly stringent and complex global regulatory framework. In the European Union, the REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation and the European Chemicals Agency (ECHA) impose restrictive limits on volatile organic compounds (VOCs), hazardous substances, and PFAS-containing surfactants. Germany already classifies select fluorinated surfactants as substances of very high concern, with criminal liability for violations. In the United States, the U.S. Environmental Protection Agency (EPA) has proposed draft rules limiting VOC emissions from metalworking fluid mist collectors, compelling costly plant upgrades. Reformulation and compliance costs disproportionately burden smaller blenders, likely accelerating industry consolidation, while raising manufacturing costs and extending product development cycles for new fluid formulations.

Raw Material Price Volatility and Disposal Cost Burdens

The metalworking fluids industry faces persistent cost pressure from base oil and additive price volatility, which is intrinsically linked to crude oil production cycles and petrochemical supply chains. Disruptions in global energy markets, such as those driven by OPEC+ production decisions and geopolitical instability, can sharply elevate the cost of mineral oil base stocks, directly compressing fluid manufacturer margins. Simultaneously, waste fluid management and disposal represent significant operational cost burdens for end-users, governed by regulations including the U.S. Resource Conservation and Recovery Act (RCRA) and EU waste directives. The combination of volatile input costs, expensive disposal obligations, and capital-intensive production line upgrades for compliance creates a challenging commercial environment that constrains volume growth, particularly in price-sensitive emerging manufacturing markets.

Market Opportunities

Bio-Based and Sustainable Metalworking Fluid Formulations

The global transition toward sustainable manufacturing presents a compelling first-mover opportunity for metalworking fluid producers investing in bio-based and low-toxicity product lines. As of 2024, more than 30% of metalworking fluids consumed in Europe were bio-based or low-VOC variants, a proportion growing steadily in response to REACH compliance and corporate ESG commitments. In 2024 alone, over 125 new eco-friendly metalworking fluid products were launched globally, a 22% increase compared to 2022, demonstrating rapid industry innovation momentum. FUCHS SE earmarked US$ 100 million annually for sustainable chemistries including PFAS-free surfactants and bio-derived esters following its record EBIT performance in 2024. In December 2025, Halocarbon launched three advanced bio-compatible metalworking fluid formulations under its InfinX product line targeting aerospace, defence, nuclear energy, medical devices, and high-performance automotive precision machining, demonstrating the breadth of addressable premium segments for next-generation sustainable fluid products.

Electric Vehicle Platform Retooling and EV Battery Housing Fabrication

The electric vehicle production ramp-up is creating a structurally new demand category for advanced metalworking fluids, distinct from traditional ICE vehicle manufacturing. EV battery housings, structural crash members, motor casings, and power electronics housings are predominantly fabricated from high-strength aluminum alloys and advanced high-strength steels, materials that require specialized fluid formulations with optimized aluminum compatibility, pH stability, and extended sump life. EV battery casing fabrication is one of the fastest-growing drivers of forming fluid demand globally. The China Association of Automobile Manufacturers (CAAM) reported that China's NEV production exceeded 12 million units in 2024, a substantial base generating enormous metalworking fluid consumption. In July 2024, Quaker Houghton broke ground on a new state-of-the-art manufacturing facility in Zhangjiagang, China, specifically to strengthen supply chain capacity across Asia-Pacific and support the EV-driven retooling boom. This facility is expected to become operational by Q2 2026, positioning the company to capture rising EV-linked metalworking fluid demand across the region.

Category-wise Analysis

Product Type Insights

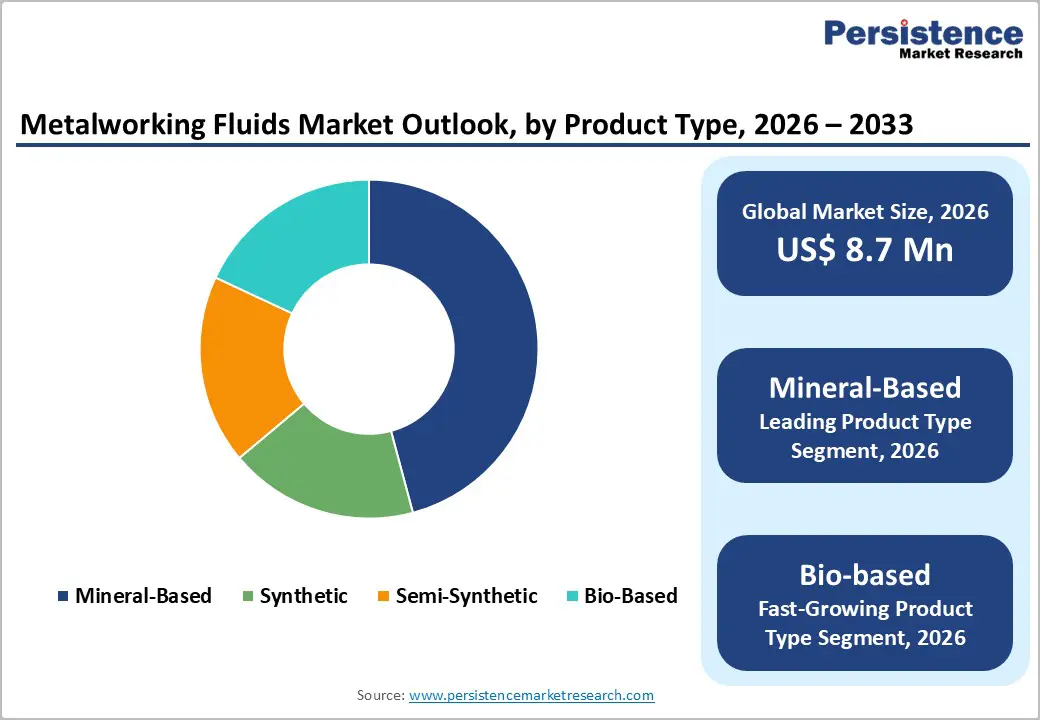

Mineral-Based metalworking fluids constitute the leading product type segment, commanding approximately 44% of global market share in 2025. Mineral-based fluids, derived from refined petroleum base stocks, offer a proven, cost-effective solution for high-volume machining, cutting, and grinding operations across ferrous and non-ferrous metals. Their broad applicability in turning, milling, drilling, and deep-hole machining operations, combined with established supply chain infrastructure and lower per-litre production costs, sustains demand particularly in Asia Pacific's high-volume manufacturing economies. However, the fastest-growing product type is Bio-Based metalworking fluids, driven by tightening VOC regulations under REACH and U.S. EPA standards, surging corporate sustainability commitments, and increasing premium specification by automotive OEMs and aerospace prime contractors seeking environmentally compliant supply chains.

Fluid Type Insights

Removal Fluids, encompassing cutting fluids, grinding fluids, and machining coolants, represent the dominant fluid type segment, accounting for approximately 52% of global metalworking fluids market share in 2025. Removal fluids are the most widely applied category, serving critical functions across turning, drilling, milling, tapping, grinding, and honing operations, the core processes in automotive component machining, aerospace part fabrication, and general precision engineering. Their universality across ferrous and non-ferrous workpieces, combined with mandatory deployment in virtually every CNC machining centre globally, underpins their entrenched market leadership. The fastest-growing fluid type segment is Forming Fluids, reflecting rising demand from EV battery housing stamping, aerospace stretch-forming, and high-precision metal forming operations for automotive structural components, with forming fluids projected to register the highest CAGR through 2033.

Industry Insights

The Automotive & Transportation sector is the dominant end-use segment in the global metalworking fluids market, accounting for approximately 38% of total market revenue in 2025. Automotive manufacturers are among the world's most intensive consumers of metalworking fluids, employing them across engine block and cylinder head machining, transmission gear grinding, axle component turning, and body panel stamping processes. According to OICA, global automobile production of 93.5 million units in 2023 generates billions of litres of MWF consumption per year. The EV transition further reinforces automotive MWF demand by introducing new machining and forming challenges. The fastest-growing end-use segment is Aerospace: in 2025, aerospace applications utilized over 18% more synthetic fluids compared to 2024, driven by record aircraft production backlogs at Airbus and Boeing, rising defence procurement, and the increasing use of difficult-to-machine titanium and nickel alloys in next-generation aircraft structures.

Regional Insights

Asia Pacific Metalworking Fluids Market Trends and Insights

Asia Pacific is the dominant region in the global Metalworking Fluids market, commanding approximately 44% of global market share in 2025, driven by China, Japan, India, and South Korea. China remains the world's largest vehicle manufacturing nation, with the China Association of Automobile Manufacturers (CAAM) reporting NEV output exceeding 12 million units in 2024, as well as the largest single market for metalworking fluids globally. The Chinese government's Made in China 2025 initiative and New Infrastructure campaign continue to drive large-scale investment in automotive, aerospace, and precision engineering manufacturing capacity, directly expanding metalworking fluid consumption. In July 2024, Quaker Houghton broke ground on a new manufacturing facility in Zhangjiagang, China, expected to be operational by Q2 2026, a clear signal of the region's strategic commercial significance.

India is the fastest-growing sub-market in the region, supported by the government's Production-Linked Incentive (PLI) scheme for the automotive sector and rapid expansion of aerospace MRO and manufacturing. According to the India Brand Equity Foundation (IBEF), India's aerospace MRO industry is projected to exceed US$ 2.4 billion by 2028 from US$ 800 million in 2018. In September 2023, FUCHS SE invested EUR 9 million to open a 20,000 tonne/year blending plant in Vietnam, further evidence of multinational producers expanding regional footprints to capture Southeast Asia's rising metalworking fluid demand from electronics, automotive, and general engineering manufacturing sectors.

North America Metalworking Fluids Market Trends and Insights

North America is the second-largest regional market, with the United States accounting for over 72% of regional revenue in 2025. The U.S. market is driven by one of the world's most advanced manufacturing ecosystems, encompassing aerospace, automotive, medical device, and defence sectors, all of which demand high-performance, certified metalworking fluid formulations. The U.S. metalworking fluids market is projected to reach US$ 4 billion by 2033, growing at a CAGR of 6.53% from 2025. Regulatory drivers include EPA draft VOC emission limits for mist collectors and TSCA (Toxic Substances Control Act) compliance requirements, compelling manufacturers to invest in reformulation toward synthetic and bio-based product lines.

The U.S. CHIPS and Science Act is catalysing semiconductor fab construction, creating new demand for precision metalworking fluids in high-tolerance silicon and metal component machining. Quaker Houghton showcased its QH FLUID INTELLIGENCE™ real-time fluid monitoring platform at IMTS Chicago in September 2024, demonstrating digital service leadership that delivered documented savings of US$ 1.25 million per automotive OEM in its first deployment year. The U.S. defence sector's increasing procurement of advanced combat aircraft and hypersonic systems under the National Defense Authorization Act (NDAA) further sustains premium synthetic fluid demand through 2033.

Europe Metalworking Fluids Market Trends and Insights

Europe is the third-largest regional market, with Germany, France, the United Kingdom, Italy, and Spain constituting the primary demand centres. Germany, Europe's largest automotive and industrial manufacturing economy, is undergoing a significant transition, with over EUR 4.7 billion committed to green manufacturing infrastructure upgrades that embed sustainability requirements into production processes, directly influencing metalworking fluid specification. Germany accounted for approximately 29% of European metalworking fluid consumption in 2025, followed by France at 17 % and the United Kingdom at 15%.

European metalworking fluid demand is uniquely shaped by the REACH regulatory framework and the European Chemicals Agency (ECHA), which have progressively restricted traditional extreme-pressure additives containing chlorinated paraffins, sulfur compounds, and PFAS. As of 2024, more than 30% of metalworking fluids used in Europe were bio-based or low-VOC variants, with this share growing annually. FUCHS SE, headquartered in Mannheim, Germany, earmarked US$ 100 million annually for sustainable chemistry R&D following record EBIT in 2024, reinforcing Europe's leadership in environmentally advanced MWF formulation. The region's emphasis on precision engineering in automotive and aerospace sectors, combined with regulatory-driven product innovation, positions Europe as a global benchmark market for next-generation fluid technologies.

Competitive Landscape

The global metalworking fluids market is moderately consolidated, with a mix of large multinational producers and regional specialists competing across diverse industrial applications. Market structure is characterized by strong entry barriers due to formulation expertise, regulatory compliance, and long-standing customer relationships, particularly in automotive and aerospace manufacturing.

Key business strategies focus on advanced formulation development, including high-performance synthetic and bio-based fluids tailored for precision machining and EV-compatible materials. Companies are increasingly integrating digital platforms and IIoT-enabled fluid management systems to optimize performance, reduce downtime, and enhance lifecycle efficiency. Sustainability is a central theme, with growing investments in recyclable coolants and circular fluid management solutions. Strategic acquisitions and partnerships are being used to expand geographic reach and technological capabilities, while regional players compete through application-specific customization, faster service delivery, and niche expertise in specialized machining environments.

Key Developments:

- December 2025: Halocarbon launched three advanced metalworking fluid formulations under its InfinX product line, targeting high-precision aerospace, defence, nuclear energy, and medical device machining applications with MQL-compatible, CNC-ready formulations.

- November 2025: Americo Chemical Products acquired Fusion Chemical, a U.S.-based specialty metalworking fluids manufacturer, to expand its product portfolio with advanced lubricants and coolants and strengthen capabilities in high-performance and environmentally sustainable machining solutions.

- October 2025: Master Fluid Solutions introduced TRIM E950, a next-generation emulsion metalworking fluid designed to enhance machining performance, extend sump life, and improve operational efficiency in demanding multi-metal applications.

Companies Covered in Metalworking Fluids Market

- Houghton International, Inc. (Quaker Houghton)

- Blaser Swisslube AG

- BP plc (Castrol)

- TotalEnergies SE

- FUCHS SE

- Chevron Corporation

- China Petroleum & Chemical Corporation (Sinopec)

- Kuwait Petroleum Corporation

- Idemitsu Kosan Co., Ltd.

- Exxon Mobil Corporation

- PJSC Lukoil

- Saudi Aramco

- Shell Plc

- Yushiro Chemical Industry Co., Ltd. (Yushiro Inc.)

- Motul

- Master Fluid Solutions

- Cimcool Industrial Products LLC

- Halocarbon Products Corporation

- Rocol (ITW)

- Valvoline Inc.

Frequently Asked Questions

The global Metalworking Fluids market is valued at US$ 8.7 billion in 2026 and is projected to reach US$ 12.8 billion by 2033 at a CAGR of 5.7%.

Demand is driven by growth in automotive and aerospace manufacturing, industrial automation, and increasing adoption of advanced fluid formulations.

Asia Pacific leads the market with around 44% share due to strong automotive, aerospace, and industrial manufacturing activities.

Key opportunities lie in EV manufacturing, aerospace machining, and the development of sustainable bio-based and high-performance fluids.

Key players include Quaker Houghton, FUCHS SE, Shell, TotalEnergies, ExxonMobil, BP (Castrol), Chevron, Blaser Swisslube, Idemitsu Kosan, Yushiro Chemical, and Saudi Aramco.