- Technology

- Security Printing Market

Security Printing Market Size, Share, and Growth Forecast 2026 - 2033

Security Printing Market by Product Type (Banknotes, Government & Legal Documents, Tax & Revenue Stamps, Certificates, Personal ID Documents, Tickets & Coupons, Brand Protection Labels), by Printing Technology (Intaglio Printing, Offset Lithography, Letterpress Printing, Screen Printing, Digital Printing, Gravure Printing, Hybrid Printing), Security Ink Type, Substrate Type, End-User, and Regional Analysis, 2026 - 2033

Security Printing Market Size and Trend Analysis

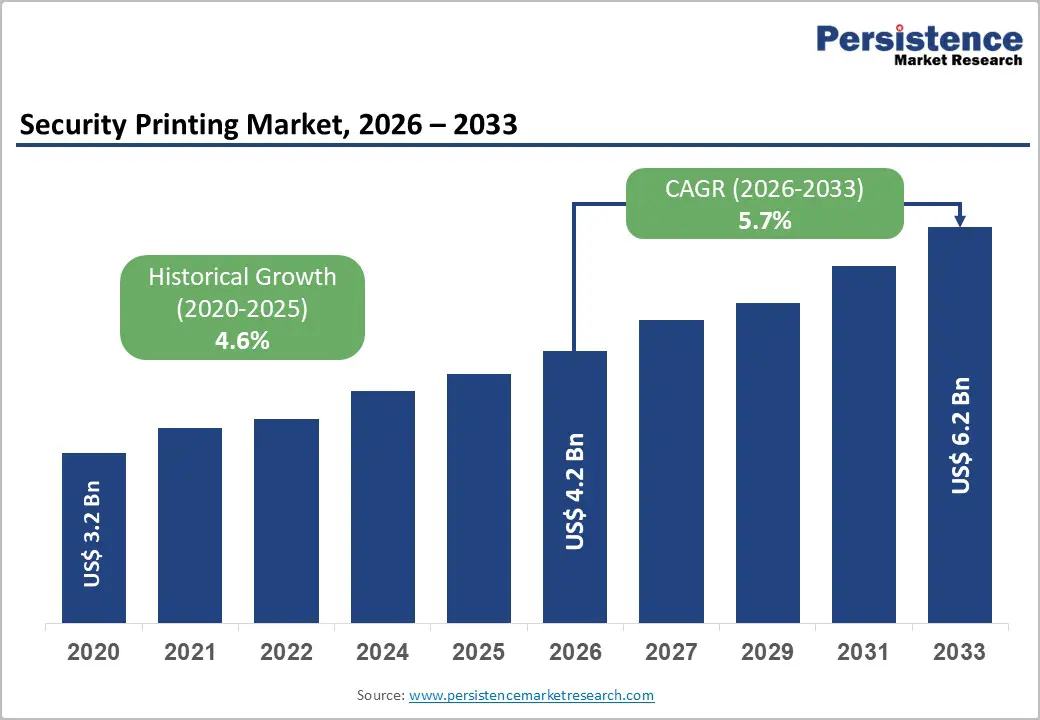

The global security printing market size is likely to be valued at US$ 4.2 billion in 2026 and is expected to reach US$ 6.2 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

The security printing market is advancing on a steady, non-cyclical growth trajectory driven by escalating global counterfeiting threats, government-mandated identity document modernization programs, and continuous technological innovation in anti-counterfeiting printing features.

Key Market Highlights

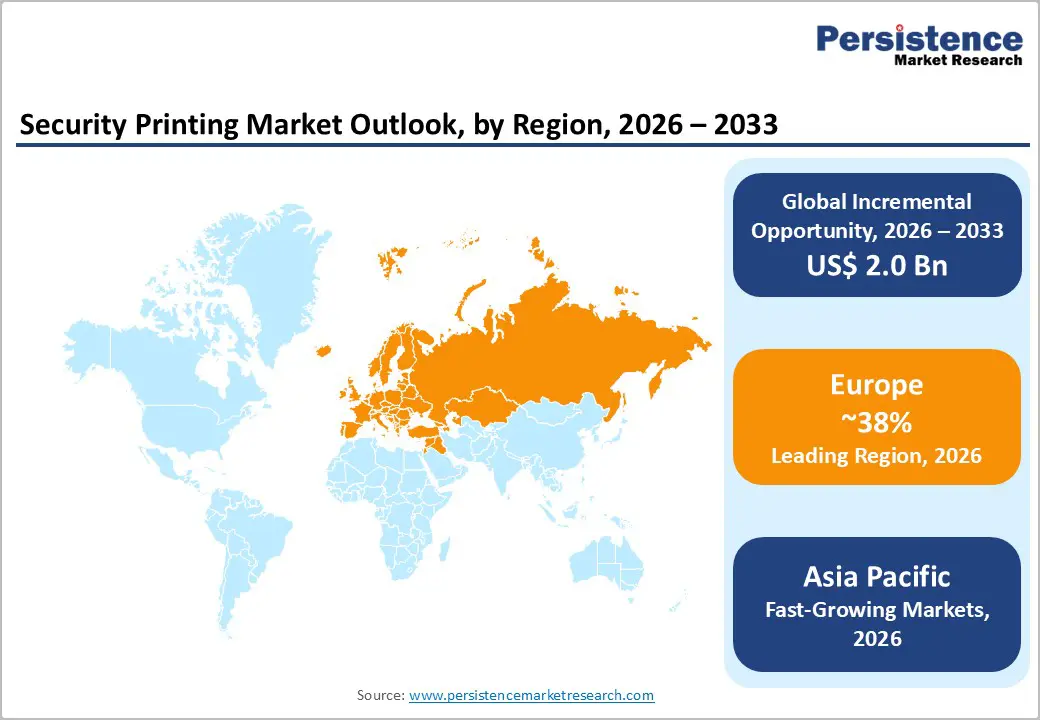

- Leading Region: Europe leads the Security Printing Market, holding 38% share, anchored by ECB Euro banknote printing, Germany's Giesecke+Devrient and Switzerland's SICPA as global technology leaders, and the EU eIDAS regulatory framework harmonizing biometric identity document standards across 27 member states.

- Fastest Growing Region: Asia Pacific is the fastest growing region with a rising CAGR of 8.1%, driven by China Banknote Printing's massive Renminbi currency output, India's Aadhaar biometric ID enrollment exceeding 1.3 billion individuals, and ASEAN nations' modernizing passport and national ID security printing infrastructure.

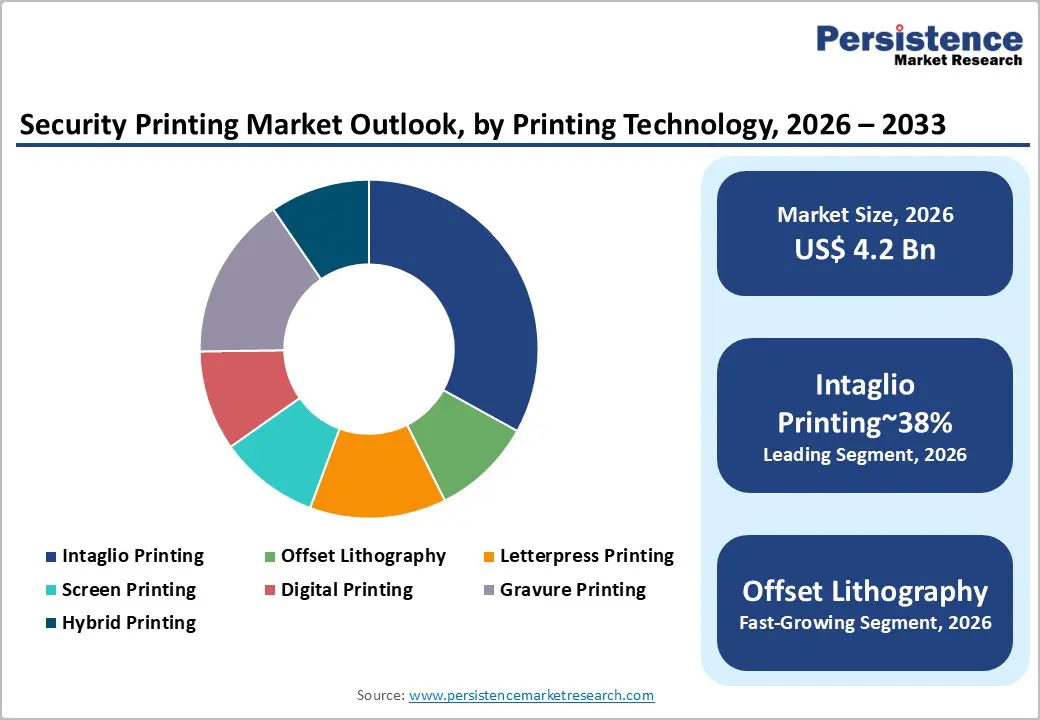

- Dominant Segment: Intaglio printing dominates the technology category with 38% share, mandated by virtually all central banks globally for banknote production, its tactile raised ink characteristics providing a uniquely counterfeiting-resistant authentication feature that cannot be replicated with commercial printing equipment.

- Fastest Growing Segment: Polymer substrates represent the fastest growing substrate segment, with 30+ central banks globally adopting polymer banknotes led by the Bank of England and Bank of Canada, driven by longer durability, superior security feature compatibility, and lower total lifecycle costs than cotton-paper alternatives.

- Key Opportunity: Tax stamp mandates under the WHO FCTC Protocol covering 180+ countries and the EU Tobacco Products Directive create a globally expanding, policy-driven procurement pipeline for security-printed authentication labels, representing a multi-year recurring revenue opportunity for SICPA and specialist security printers.

Market Dynamics

Drivers - Global Growth of Counterfeiting Threats and Document Fraud

The relentless global rise of counterfeiting, spanning currency fraud, identity document forgery, and brand product counterfeiting, is the most fundamental structural driver of the security printing market. The International Criminal Police Organization (INTERPOL) and Europol have consistently identified document fraud and currency counterfeiting as among the most pervasive financial crimes globally, with counterfeit currency representing a perpetual threat to monetary system integrity.

The European Central Bank (ECB) reported approximately 467,000 counterfeit euro banknotes withdrawn from circulation in the first half of 2023 alone, underscoring the ongoing challenge. In response, central banks across the world are upgrading banknote series to incorporate next-generation security features, including Optically Variable Ink (OVI), holograms, and color-shifting security threads, that require highly specialized security printing capability from approved manufacturers, creating a recurring, government-mandated demand cycle.

Mandatory National Identity Document Modernization and Biometric Passport Programs

Governments worldwide are undertaking comprehensive identity document modernization programs, upgrading national ID cards, passports, driving licenses, and border control documents to incorporate biometric data, RFID chips, and advanced anti-counterfeiting security features. The International Civil Aviation Organization (ICAO) mandates biometric Machine Readable Travel Documents (MRTDs) for all member states under Document 9303 standards, compelling governments to procure security-printed biometric passports.

The UNHCR and the World Bank's Identification for Development (ID4D) initiative report that over 1 billion people worldwide still lack official identity documentation, representing a long-term government procurement opportunity for security printing companies delivering ID enrollment and issuance solutions in Africa, Asia, and Latin America as these regions formalize national ID systems.

Restraints - Acceleration of Cashless Payments, Reducing Long-Term Banknote Demand

The accelerating global shift toward cashless and digital payments poses a structural long-term headwind for the banknote printing segment, historically the highest-value component of the security printing market.

The Bank for International Settlements (BIS) documents that digital payment transaction volumes are growing at double-digit rates annually in most advanced economies, while cash usage as a proportion of retail transactions is declining. Sweden's Riksbank has reported cash usage declining to below 8% of retail transactions. While central bank digital currencies (CBDCs) may offset some demand, overall banknote volume trends in developed markets constrain the segment's growth potential.

High Barriers to Entry and Concentration of Certified Manufacturers

The security printing market is characterized by exceptionally high barriers to entry, including specialized machinery, proprietary ink formulations, rigorous security clearance requirements, and long-term exclusive supplier relationships with central banks and government agencies. This concentration limits competitive entry and innovation pace.

Giesecke+Devrient GmbH, De La Rue plc, and Crane Currency collectively serve a large proportion of global central bank banknote contracts. This oligopolistic structure limits price competition and market responsiveness, creating potential supply concentration risks for government clients and restricting the pace of technology adoption across the sector.

Opportunities - Polymer Substrate Banknote Conversion Driving Premium Equipment and Ink Demand

The global conversion of banknote series from traditional cotton-paper substrates to polymer substrates, pioneered by the Reserve Bank of Australia and now adopted by over 30 central banks worldwide including the Bank of England and Bank of Canada, represents a multi-year premium product opportunity for security printing specialists.

Polymer banknotes require specialized intaglio inks, OVI features, and printing processes adapted for non-porous substrates, demanding investment in advanced security printing equipment. CCL Secure Pty Ltd (formerly Innovia Security) and Landqart AG supply specialized polymer substrate materials. As currency series renewals are typically scheduled every 7-15 years and polymer conversion projects create new tender cycles distinct from routine reissuance, they represent windfall procurement opportunities for manufacturers offering proven polymer banknote production capability.

Tax Stamp and Brand Protection Label Expansion Across Regulated Goods

Government mandates for tax stamps and brand authentication labels on regulated goods, tobacco products, alcoholic beverages, pharmaceuticals, and luxury goods, represent a fast-growing and geographically expanding opportunity for security printing. The World Health Organization (WHO)'s Framework Convention on Tobacco Control (FCTC) Protocol to Eliminate Illicit Trade in Tobacco Products requires signatory governments to implement tracking and tracing systems with security stamps, creating a global policy mandate covering over 180 countries.

The European Commission's Tobacco Products Directive (TPD) and the EU Falsified Medicines Directive impose security labeling requirements on tobacco and pharmaceutical products. SICPA Holding SA is a global leader in this segment, with tax authentication programs covering dozens of jurisdictions. This policy-driven expansion into emerging markets offers long-term, recurring revenue streams for security printers.

Category-wise Analysis

By Product Type Insights

Banknotes are the dominant product type segment, accounting for approximately 35% of the security printing market. Currency printing remains the highest-value and most technically demanding segment, requiring the deepest combination of security features, intaglio printing, OVI inks, holograms, security threads, and watermarks, to deter counterfeiting.

Despite the advance of digital payments in developed markets, global banknote demand remains structurally supported by the Bank for International Settlements (BIS), which notes that physical currency in circulation has grown in absolute terms globally, including through the COVID-19 period when cash hoarding increased. Emerging economies with high unbanked populations and strong cash cultures, including India, Nigeria, and Brazil, sustain significant banknote printing demand, reinforcing the segment's dominant position.

By Printing Technology Insights

Intaglio Printing is the dominant printing technology segment, representing approximately 38% of the market by technology. Intaglio, which produces tactile raised ink deposits by pressing engraved plates against substrate under high pressure, is the gold standard security printing technique mandated for banknote production by virtually all central banks globally.

Its distinctive tactile feel is uniquely difficult to replicate with commercial printing equipment, making it the most critical anti-counterfeiting technology in currency and high-security document production. Equipment manufacturers including Koenig & Bauer AG and Komori Corporation supply specialized intaglio presses to central banks and approved security printers. The technology's mandated status in banknote specifications globally ensures its sustained revenue dominance regardless of broader digital printing trends in commercial segments.

By Security Ink Type Insights

Optically Variable Ink (OVI) is the dominant security ink segment, accounting for approximately 32% of the security ink market. OVI, which shifts color when viewed at different angles, is among the most widely specified and publicly recognizable anti-counterfeiting features on banknotes globally. The European Central Bank (ECB) and the U.S. Federal Reserve both specify OVI features as mandatory visible security elements on circulating currency.

SICPA Holding SA is the world's leading OVI manufacturer, holding a dominant global market position in specialized security inks. The public-facing nature of OVI, enabling end-consumers to verify currency authenticity, makes it a preferred feature for central banks issuing new banknote series, sustaining its ink segment leadership.

By Substrate Type Insights

Paper-based substrates remain the dominant substrate type segment, accounting for approximately 52% of the market. Cotton-paper substrates, typically a 75-25% cotton-linen blend, have been the established banknote substrate for centuries and remain specified by the majority of the world's central banks for circulating currency. Their proven compatibility with intaglio printing, security thread embedding, and watermark formation maintains their dominance.

The Portals Group (a Giesecke+Devrient company) and Crane Currency's paper mill operations are major global suppliers of security paper. While polymer substrates are gaining rapid share through currency conversion programs, the broad installed base of cotton-paper specifications in established currency series globally ensures paper substrates retain the majority share through the forecast period.

By End-User Insights

Central Banks are the dominant end-user segment, accounting for approximately 40% of the security printing market. As the sole authoritative issuers of legal tender currencies and sovereign procurers of a product that cannot be sourced from non-approved suppliers, central banks represent the most structurally stable and highest-value customer segment in security printing.

The Bank for International Settlements (BIS) notes that over 180 central banks globally issue national currencies, each procuring security-printed banknotes through long-term exclusive or competitive tender contracts with approved manufacturers. Banknote series redesigns, typically every 7-15 years per currency, create concentrated procurement events of very high value. Central banks' non-negotiable security specification requirements and political sensitivity of currency integrity make them the most demanding and highest-margin end-user segment.

Regional Insights

North America Security Printing Market Trends & Analysis

North America remains a technologically advanced security printing market, driven by continuous currency redesign, secure ID mandates, and anti-counterfeiting initiatives. The Bureau of Engraving and Printing produces 7.9 billion notes annually, while the REAL ID Act sustains ID document demand. Strong collaboration between enforcement agencies and private firms ensures steady innovation in authentication technologies.

- U.S. Security Printing Market Size

The U.S. dominates the regional market, accounting for approximately 75% share of North America, valued at around USD 1.4 billion in 2026, growing steadily with currency upgrades and federal/state ID programs. Demand is driven by advanced features like microprinting, polymer substrates, and biometric-enabled identity solutions.

Europe Security Printing Market Trends, Drivers & Insights

Europe leads globally in security printing innovation, supported by centralized currency management under the European Central Bank and regulatory frameworks like eIDAS Regulation. The region hosts major players such as De La Rue and Giesecke+Devrient, reinforcing its dominance in banknotes and secure identity solutions.

- Germany Security Printing Market Size

Germany represents a core innovation hub, contributing approximately USD 450 million in 2026, driven by firms like Bundesdruckerei and strong R&D investments in biometric passports and e-ID systems.

- U.K. Security Printing Market Size

The U.K. security printing market is valued at around USD 350 million in 2026, led by global exporter De La Rue. Growth is supported by international contracts, currency printing, and authentication solutions for global clients.

- France Security Printing Market Size

France accounts for approximately USD 300 million in 2026, driven by Oberthur Fiduciaire and strong government demand for secure IDs, passports, and banknotes within Europe and export markets.

Asia Pacific Security Printing Market Size

Asia Pacific is the fastest-growing market, supported by large population bases, high cash circulation, and national identity initiatives. Government-led programs such as Aadhaar and frequent banknote redesigns across major economies drive volume demand. The region benefits from domestic production capabilities and rising investments in anti-counterfeiting technologies.

- China Security Printing Market Size

China leads the region with an estimated USD 1.1 billion market size in 2026, supported by the People's Bank of China and large-scale operations of China Banknote Printing and Minting Corporation, producing currency, passports, and secure documents.

- India Security Printing Market Size

India’s market is valued at approximately USD 700 million in 2026, driven by institutions like Security Printing and Minting Corporation of India Limited and BRBNMPL. The Aadhaar program continues to generate large-scale ID printing demand.

- Japan Security Printing Market Size

Japan accounts for around USD 250 million in 2026, with strong contributions from companies such as Toppan Inc. and Komori Corporation, focusing on advanced printing technologies and secure packaging solutions.

Competitive Landscape

The security printing market is highly consolidated, with a small number of specialized global operators, Giesecke+Devrient GmbH, De La Rue plc, Crane Currency, and Oberthur Fiduciaire SAS, serving as preferred suppliers to the majority of the world's central banks and government document programs under long-term exclusive or framework contracts. Market leaders differentiate through proprietary banknote security feature portfolios, intaglio printing capability, government security clearances, and integrated supply chains encompassing substrate, ink, and printing.

Key strategies include capacity expansion in emerging markets, investment in digital security feature integration (QR codes, RFID), and expansion into tax stamp and brand protection segments. Emerging business model trends include end-to-end document lifecycle management services and digital authentication platform integration with physical security documents.

Key Developments:

- March, 2025: De La Rue plc announced a new contract with a Central Asian sovereign central bank to supply polymer substrate banknotes featuring next-generation SAFEGUARD polymer technology, marking its expansion into the Commonwealth of Independent States (CIS) currency conversion segment.

- October, 2024: Giesecke+Devrient GmbH launched its Banknote 2030 initiative, unveiling a new generation of biometric-integrated security printing features for high-denomination banknotes combining AI-verifiable digital watermarks with traditional intaglio and OVI anti-counterfeiting elements.

- May, 2024: SICPA Holding SA expanded its SICPATRACE tobacco tax stamp authentication platform to three new African markets, responding to WHO FCTC Protocol requirements for illicit trade prevention in tobacco products across the continent.

Security Printing Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.2 Bn |

| Current Market Value (2026) | US$ 4.2 Bn |

| Projected Market Value (2033) | US$ 6.2 Bn |

| CAGR (2026 - 2033) | 5.7% |

| Leading Region | Europe, 38% share |

| Dominant Application | Intaglio Printing, 38% share |

| Top-ranking Product | Central Banks, 40% |

| Incremental Opportunity | US$ 2.0 Bn |

Companies Covered in Security Printing Market

- Giesecke+Devrient GmbH

- De La Rue plc

- SICPA Holding SA

- Koenig & Bauer AG

- CCL Secure Pty Ltd

- Oberthur Fiduciaire SAS

- Crane Currency

- Toppan Inc.

- IDEMIA Group

- Komori Corporation

- Canadian Bank Note Company Limited

- Landqart AG

- Orell Füssli Holding Ltd

- China Banknote Printing and Minting Corporation

- Security Printing and Minting Corporation of India Limited

- Bundesdruckerei GmbH

- ANY Security Printing Company

- Louisenthal GmbH

Frequently Asked Questions

The global security printing market is estimated at US$ 4.2 Billion in 2026 and is forecast to reach US$ 6.2 Billion by 2033, at a CAGR of 5.7%. Historically, the market grew at a CAGR of 4.6% from 2020 to 2025, reflecting steady demand from central bank currency printing, government identity document programs, and expanding tax stamp mandates globally.

Primary drivers include the ICC-estimated US$ 4.5 trillion annual global counterfeiting cost compelling security feature upgrades, ICAO biometric MRTD mandates driving passport security printing, and the World Bank ID4D initiative targeting over 1 billion undocumented individuals, creating long-term government procurement demand for security-printed identity documents across Africa, Asia, and Latin America.

Intaglio printing leads with approximately 38% market share, as it is mandated by virtually all central banks globally for banknote production. Its distinctive tactile raised ink, produced by engraved plate printing under high pressure, provides a uniquely counterfeiting-resistant authentication feature that cannot be replicated with commercial printing equipment, making it the irreplaceable technology foundation of the global security printing industry.

Europe is the leading regional market, home to the world's dominant security printing manufacturers, Giesecke+Devrient GmbH (Germany) and SICPA Holding SA (Switzerland), the ECB's centralized Euro banknote printing program, and the EU eIDAS regulation harmonizing biometric identity standards. De La Rue plc (UK) and Oberthur Fiduciaire SAS (France) further reinforce Europe's position as the global hub for security printing technology and manufacturing.

The most compelling opportunities are polymer banknote substrate conversion (30+ central banks converting, with long series renewal cycles creating concentrated procurement events) and tax stamp expansion under the WHO FCTC Protocol covering 180+ countries and the EU Tobacco Products Directive, both creating policy-mandated, recurring revenue streams for security printers and authentication ink suppliers including SICPA and Giesecke+Devrient.

Leading companies include Giesecke+Devrient GmbH, De La Rue plc, SICPA Holding SA, Crane Currency, Oberthur Fiduciaire SAS, CCL Secure Pty Ltd, Koenig & Bauer AG, Toppan Inc., IDEMIA Group, and China Banknote Printing and Minting Corporation. These companies compete on proprietary security feature technology depth, government security clearances, intaglio printing capability, global manufacturing footprint, and long-term exclusive central bank relationships.