- Marine

- Maritime Simulator Market

Maritime Simulator Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Maritime Simulator Market by Platform (On-premise Simulator Centre, Remote/Networked Instructor-led Simulation, Mobile Deployable Simulator, Cloud-enabled/Subscription Simulation Labs, Others), Application (Merchant Deep-sea Vessels, Tankers, Gas Carriers, Passenger Vessels, Offshore Vessels, Others), End-user (Maritime Academies & Universities, Private Maritime Training Centres, Others), and Regional Analysis from 2026 - 2033

Maritime Simulator Market Size and Trend Analysis

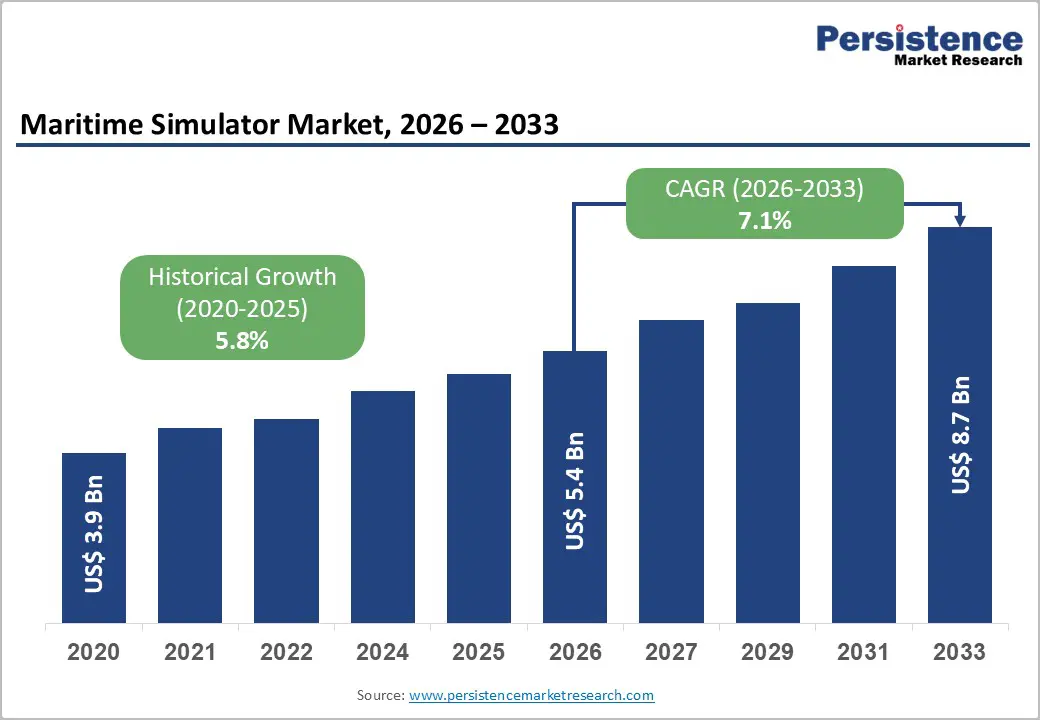

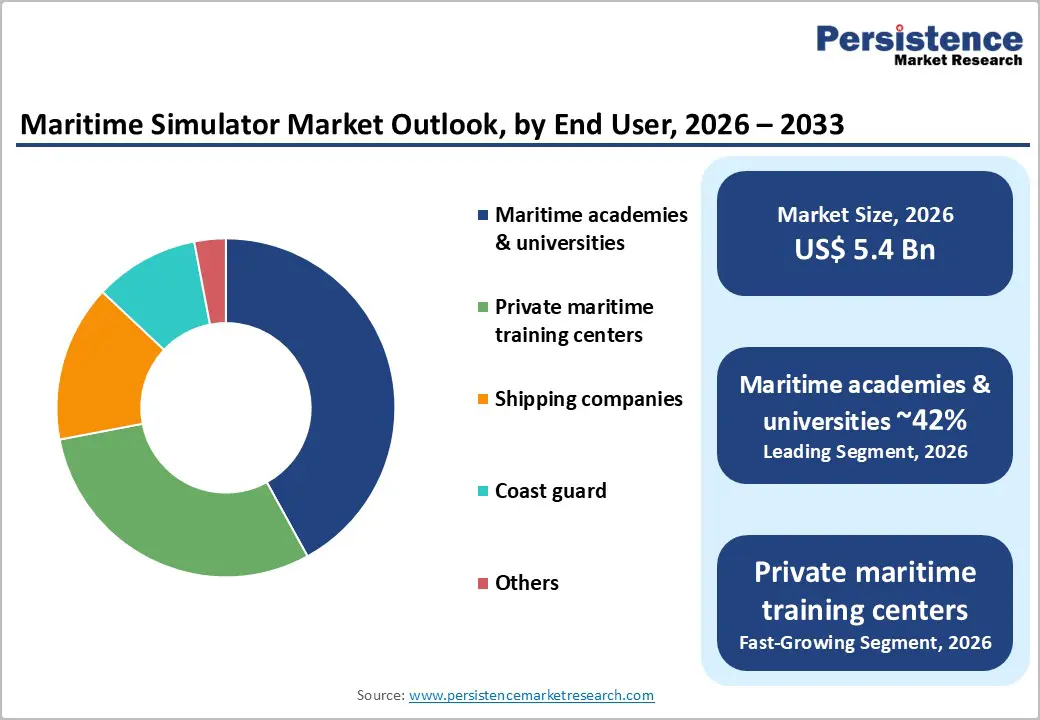

The global Maritime Simulator market is valued at approximately US$ 5.4 Bn in 2026 and is projected to reach US$ 8.7 Bn by 2033, growing at a CAGR of 7.1% between 2026 and 2033. This sustained growth is driven by converging forces of stringent international regulatory mandates, a deepening global seafarer shortage, and rapid adoption of immersive simulation technologies for maritime training.

According to the International Maritime Organization (IMO), over 90% of global trade by volume is carried by sea, making highly skilled maritime personnel a critical priority. The IMO's STCW (Standards of Training, Certification, and Watchkeeping) Convention, currently undergoing a comprehensive revision with adoption targeted by 2027, mandates simulation-based training for officer certification, directly sustaining demand for advanced simulator platforms.

Key Industry Highlights:

- Leading Region – Europe leads the global Maritime Simulator market, home to Kongsberg Maritime and Wärtsilä Voyage, and supported by the EU's STCW implementation framework and a dense network of world-class maritime academies and shipping companies requiring continuous crew certification.

- Fastest-Growing Region – Asia Pacific is the fastest-growing region, driven by the world's largest seafarer supply nations, China, Philippines, India, expanding maritime academy infrastructure, and landmark installations by Wärtsilä and Kongsberg at premier regional training institutions in Malaysia, Singapore, and South Korea.

- Dominant Segment – On-premises full-mission simulator centers hold the dominant platform share (~48%), mandated by IMO's STCW requirements for officer certification training, and anchored by high-value installations at leading maritime academies globally.

- Fastest-Growing Segment – Cloud-based and subscription simulation platforms are the fastest-growing segment, driven by Wärtsilä's Cloud Simulation and VSTEP's NAUTIS Home, enabling anytime, anywhere training without hardware, particularly for dispersed fleet operators and developing-economy training centers.

- Key Opportunity – IMO decarbonization mandates are driving urgent demand for LNG, methanol, hydrogen, and ammonia vessel training modules, while autonomous vessel testing platforms offer high-margin R&D simulation revenue for technology leaders such as Wärtsilä Voyage and Kongsberg Maritime.

| Key Insights | Details |

|---|---|

|

Maritime Simulator Market Size (2026E) |

US$ 5.4 Billion |

|

Market Value Forecast (2033F) |

US$ 8.7 Billion |

|

Projected Growth CAGR (2026–2033) |

7.1% |

|

Historical Market Growth (2020–2025) |

5.8% |

DRO Analysis

Market Growth Drivers

Mandatory STCW Compliance and Evolving IMO Regulatory Framework

The most fundamental growth driver for the Maritime Simulator market is the regulatory compulsion arising from the International Maritime Organization's STCW Convention, which mandates simulation-based competency training for maritime officers worldwide. The IMO's Maritime Safety Committee (MSC 108) has approved new STCW amendments effective January 1, 2026, introducing mandatory training requirements for seafarers around personal safety, harassment prevention, and alternative fuel systems.

The comprehensive revision of the STCW Convention, underway at the IMO Sub-Committee on Human Element, Training and Watchkeeping (HTW), is targeted for completion by 2025 with full adoption and entry into force expected by 2027. As the IMO advances training guidelines for ships powered by alternative fuels including methanol, hydrogen, and ammonia maritime academies and shipping companies worldwide are compelled to invest in new-generation simulators capable of replicating these next-generation vessel technologies, directly expanding the simulator procurement pipeline.

Acute Global Seafarer Shortage Driving Scalable Simulation-Based Training

The worsening global shortage of qualified maritime officers is a powerful structural driver creating sustained demand for efficient, scalable simulation-based training. The International Chamber of Shipping (ICS) estimates the worldwide seafarer population at approximately 1.89 million, of which 857,540 are officers a base that is forecast to fall short of demand as the global fleet expands.

The Global Maritime Forum identified seafarer labour shortages at a 17-year high as of September 2024, while Safety4Sea reports projections of a potential shortfall of 90,000 seafarers by 2026. Maritime simulators directly address this challenge by enabling large-volume training without real vessels or sea time: Wärtsilä's cloud simulation platform notes that 5 simulator days can substitute for 15 sea days in some jurisdictions, dramatically accelerating officer certification cycles.

Market Restraints

High Capital Expenditure and Long Procurement Cycles for Full-Mission Simulators

The high initial investment required for full-mission bridge and engine room simulators constitutes a significant barrier for many maritime academies and training institutions, particularly in developing economies. Full-mission bridge simulators with 360-degree panoramic visualization can cost several million U.S. dollars per installation, with additional recurring expenditure for software licensing, content updates, and maintenance.

Procurement cycles at government-funded maritime academies often extend over 18–36 months due to multi-stage tendering processes, budget approval requirements, and compliance certification. These cost and procurement barriers slow market penetration in South Asia, Africa, and Latin America, where maritime training infrastructure investment is growing but constrained by fiscal limitations.

Cybersecurity Risks and Regulatory Certification Complexity

As maritime simulators become increasingly networked, cloud-connected, and integrated with vessel digital systems, they face growing cybersecurity exposure. The IMO's Maritime Cyber Risk Management guidelines under MSC-FAL.1/Circ.3 require shipping companies to incorporate cyber risk into their Safety Management Systems, and networked simulation platforms represent a potential vulnerability surface.

Simultaneously, achieving simulator approval from classification bodies such as DNV, Bureau Veritas, or flag state administrations for STCW-compliant training can involve lengthy certification processes. Divergent national certification requirements create additional complexity for simulator vendors operating across multiple jurisdictions, slowing product deployment and raising compliance costs.

Market Opportunities

Cloud-Enabled and Subscription-Based Simulation Platforms

The migration of maritime simulation from capital-intensive physical installations to cloud-based, subscription, and software-as-a-service (SaaS) delivery models represents the most disruptive near-term opportunity in the Maritime Simulator market. Wärtsilä Voyage's Cloud Simulation platform, accessible via online training platforms including OTG, Mintra, Maritime Trainer, and Bamboo, enables instructor-led and self-directed simulation exercises without additional hardware, dramatically lowering access barriers for smaller shipping companies and developing-economy training centers.

This model allows training providers to offer blended learning combining cloud simulation, in-person exercises, and certification accessible anywhere globally. VSTEP B.V. similarly launched its NAUTIS Home platform, extending simulator access to individual maritime professionals and students beyond institutional settings.

Autonomous and Alternative-Fuel Vessel Training Modules

The maritime industry's twin transitions toward autonomous vessel operations and decarbonized fuel systems are creating entirely new simulator application categories with substantial revenue potential. The IMO's Net-Zero Framework with interim decarbonization goals for 2030 and a net-zero target for shipping by approximately 2050 is driving urgent demand for seafarer training in LNG, methanol, hydrogen, and ammonia propulsion systems.

Wärtsilä's simulation portfolio now includes dedicated LNG bunkering, methanol bunkering, and dual-fuel engine room simulators, while the company has commercialized one of the world's first simulators specifically designed to test autonomous vessel navigation algorithms using digital twin and sensor technology. Kongsberg Maritime's award-winning K-Sim Engine platform delivered to Aboa Mare Maritime Academy in Finland in Q1 2026 covers hybrid, dual-fuel, battery, and methanol propulsion precisely the skill sets the industry's decarbonization trajectory demands.

Category-wise Analysis

Platform Insights

The On-premises simulator centre platform segment leads the global Maritime Simulator market, holding approximately 48% of total revenue in 2026. On-premises full-mission simulator installations encompassing ship bridge simulators with 360-degree panoramic visualizations, engine room simulators with 3D equipment modelling, and liquid cargo handling simulators represent the gold standard for STCW-compliant officer certification training recognized by the IMO and national maritime administrations.

Major maritime academies, including institutions in Norway, the Netherlands, Japan, South Korea, the Philippines, and India, invest in on-premise centers as anchor assets for both initial certification training and continuing professional development. The segment's dominance reflects regulatory requirements mandating full-mission simulation for specific officer competencies under STCW Codes. However, Cloud-enabled/Subscription Simulation Labs is the fastest-growing platform segment, accelerated by offerings from Wärtsilä Voyage and VSTEP B.V.

Application Insights

The Merchant Deep-sea Vessels application segment leads the global Maritime Simulator market, accounting for approximately 35% of revenue in 2026. This segment's dominance is rooted in the sheer scale of the global commercial fleet: the International Chamber of Shipping (ICS) notes over 50,000 merchant ships trading internationally, generating over half a trillion U.S. dollars in annual freight revenue.

The training requirements for bulk carriers, container ships, and general cargo vessels covering navigation, collision avoidance, emergency response, and cargo management constitute the largest and most consistent simulator procurement driver. UNCTAD's Review of Maritime Transport 2024 projects global seaborne trade to grow at an average annual rate of 2.4% between 2025 and 2029, sustaining fleet expansion and the corresponding demand for simulator-based officer certification.

End-user Insights

Maritime academies & universities constitute the dominant end-user segment in the global maritime simulator market, capturing approximately 42% of revenue in 2026. These institutions serve as the primary certification pathway for new maritime officers globally and are legally required to maintain IMO-approved simulation facilities for STCW-compliant training delivery. Leading academies, including Aboa Mare Maritime Academy (Finland), Akademi Laut Malaysia (ALAM), Sharjah Maritime Academy (UAE), and Memorial University (Canada) have made landmark simulator investments in recent years from leading OEMs, including Kongsberg Maritime and Wärtsilä.

The Philippines, China, India, and Indonesia, collectively the world's largest seafarer supply nations per the ICS host large networks of maritime academies that generate sustained, recurring simulator procurement and upgrade demand. Shipping Companies are the fastest-growing end-user segment, driven by the adoption of cloud and on-board simulation for fleet-level crew competency management.

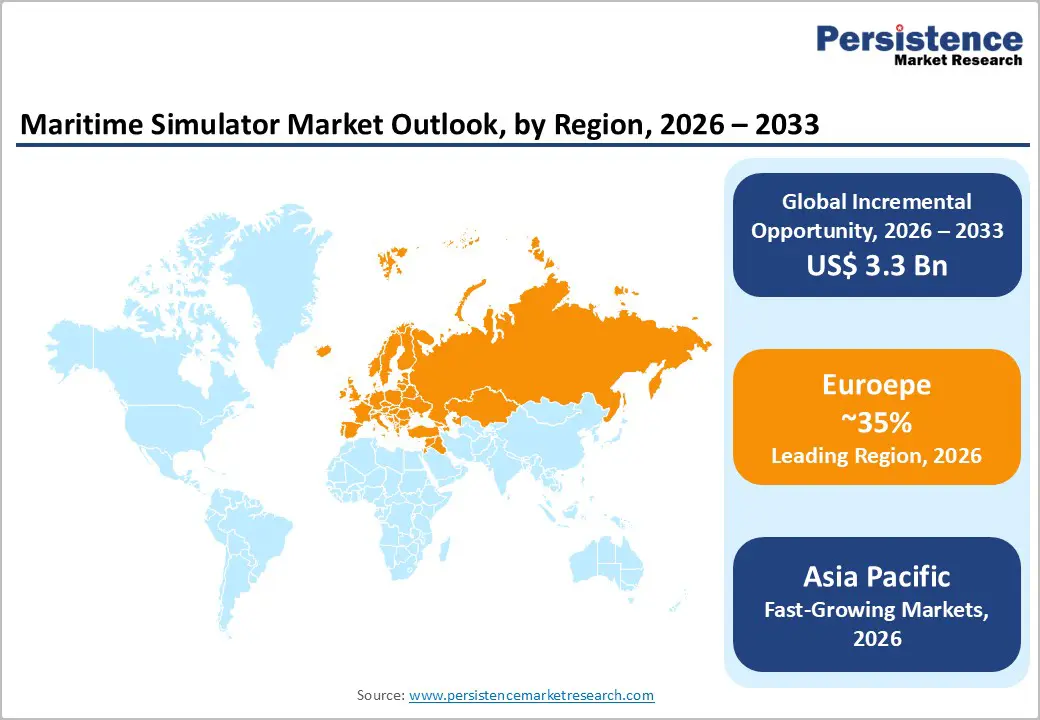

Regional Insights

Europe Maritime Simulator Trends

Europe is the dominant region in the global Maritime Simulator market, anchored by industry-leading OEMs headquartered in Norway (Kongsberg Maritime), Finland (Wärtsilä Voyage), the Netherlands (VSTEP B.V.), and Germany (Raytheon Anschütz). The region benefits from the European Maritime Safety Agency's (EMSA) oversight of STCW implementation across EU member states, creating a harmonized regulatory framework that drives sustained simulator investment across Germany, Norway, the Netherlands, the UK, Finland, and Spain.

Wärtsilä delivered its advanced dual-fuel simulator suite to Akademi Laut Malaysia (ALAM) in July 2025, and Kongsberg Maritime won the tender to equip Aboa Mare Maritime Academy in Finland with a state-of-the-art K-Sim Engine system, delivering to Q1 2026, both highlighting Europe's role as the global anchor for maritime simulator innovation and institutional collaboration.

Asia Pacific Maritime Simulator Market Trends

Asia Pacific is the fastest-growing regional market for maritime simulators, driven by its position as the world's largest source of seafarers, largest shipbuilding hub, and rapidly expanding maritime training infrastructure. China, Japan, South Korea, and the Philippines are the dominant national markets. China leads in volume, with its large network of maritime academies and vocational training institutions driving high-volume procurement of simulator systems from both international and domestic vendors.

India is one of the fastest-growing individual country markets in the region, with the Directorate General of Shipping (DGS) actively expanding STCW-compliant training infrastructure. Wärtsilä inaugurated its advanced simulator suite at ALAM (Akademi Laut Malaysia) in July 2025, marking ALAM as the first institution in the Asia Pacific region to join Wärtsilä's MASTERS program underscoring the region's growing integration with global simulation technology ecosystems.

North America Maritime Simulator Market Trends

North America is a mature and strategically important region in the global Maritime Simulator market, led by the United States, which maintains one of the world's most rigorous maritime training regulatory frameworks. The U.S. Coast Guard (USCG) mandates simulation components in officer training curricula for certification under STCW standards and requires periodic simulator-based drills and recertification for active mariners. Memorial University of Newfoundland in Canada is recognized globally for its Centre for Marine Simulation, which has developed expertise in offshore and harsh-environment vessel simulation.

The U.S. also leads in simulator applications for Coast Guard and defense maritime operations, with platforms from Thales Group and L3Harris Technologies serving military and search-and-rescue training requirements. CALSTART reported a 12% surge in zero-emission marine adoption, and the U.S. Navy's commitments to autonomous vessel testing have created additional simulation demand for R&D-oriented platforms.

Competitive Landscape

The global maritime simulator market is moderately consolidated, dominated by a small group of technology-driven incumbents primarily Kongsberg Maritime, Wärtsilä Voyage, and CAE Inc. that hold significant global share through comprehensive product portfolios, regulatory certifications, and deep institutional partnerships.

Market differentiation is driven by simulator fidelity, software platform breadth, regulatory compliance credentials, and after-sales support networks. Key emerging business model trends include cloud-based simulation-as-a-service offerings (championed by Wärtsilä and VSTEP), digital twin integration for autonomous vessel testing, and blended learning ecosystems combining physical, virtual, and cloud simulation.

Key Developments:

- In September 2025, Aboa Mare solidified its position as a top supplier of maritime training by purchasing a cutting-edge K-Sim Engine Full Mission and Desktop Simulator system from Kongsberg Maritime.

- In March 2025, Kongsberg Maritime rolled out the K-Sim Offshore DP3 Anchor Handling Simulator. The simulator focuses on enhancing maritime safety and has been designed to train personnel for complex offshore operations.

Companies Covered in Maritime Simulator Market

- Kongsberg Maritime

- Wärtsilä Voyage

- CAE Inc.

- L3Harris Technologies Inc.

- Transas

- Thales Group

- Northrop Grumman Corporation

- Seagull Maritime AS

- Rheinmetall AG

- VSTEP B.V.

Frequently Asked Questions

The global Maritime Simulator market is estimated to be valued at US$ 5.4 billion in 2026 and is projected to reach US$ 8.7 billion by 2033, registering a CAGR of 7.1% during the forecast period.

The primary drivers are the IMO's STCW Convention mandating simulation-based officer certification, the comprehensive STCW revision targeted for adoption by 2027 which will introduce new training requirements for alternative fuel vessels and autonomous ships, and the global seafarer shortage reaching a 17-year high per the Global Maritime Forum with projections indicating a shortfall of 90,000 seafarers by 2026.

Maritime Academies & Universities is the leading end-user segment, accounting for approximately 42% of the global Maritime Simulator market revenue in 2025. These institutions are legally required under IMO STCW to maintain approved simulation facilities for officer certification training.

Europe leads the global Maritime Simulator market, home to the two dominant OEMs Kongsberg Maritime (Norway) and Wärtsilä Voyage (Finland), and supported by the European Maritime Safety Agency's (EMSA) harmonized STCW implementation framework.

The leading companies in the global Maritime Simulator market include Kongsberg Maritime, Wärtsilä Voyage, CAE Inc., L3Harris Technologies Inc., Transas, Thales Group, Northrop Grumman Corporation, and VSTEP B.V. Kongsberg Maritime and Wärtsilä Voyage collectively dominate the commercial maritime simulation segment through comprehensive IMO-compliant simulator portfolios, global service networks, and long-standing institutional partnerships with leading maritime academies worldwide.