- Medical Devices

- Loss of Resistance (LOR) Syringe Market

Loss of Resistance (LOR) Syringe Market Size, Share, and Growth Forecast, 2026 - 2033

Loss of Resistance (LOR) Syringe Market by Application (Anesthesia, General Surgery, Urology, Cardiovascular, Orthopedics), End-User (Hospitals, Clinics, Ambulatory Surgical Centers (ASCs)), Modality Type (Disposable, Reusable), and Regional Analysis for 2026 - 2033

Loss Resistance (LOR) Syringe Market Share and Trends Analysis

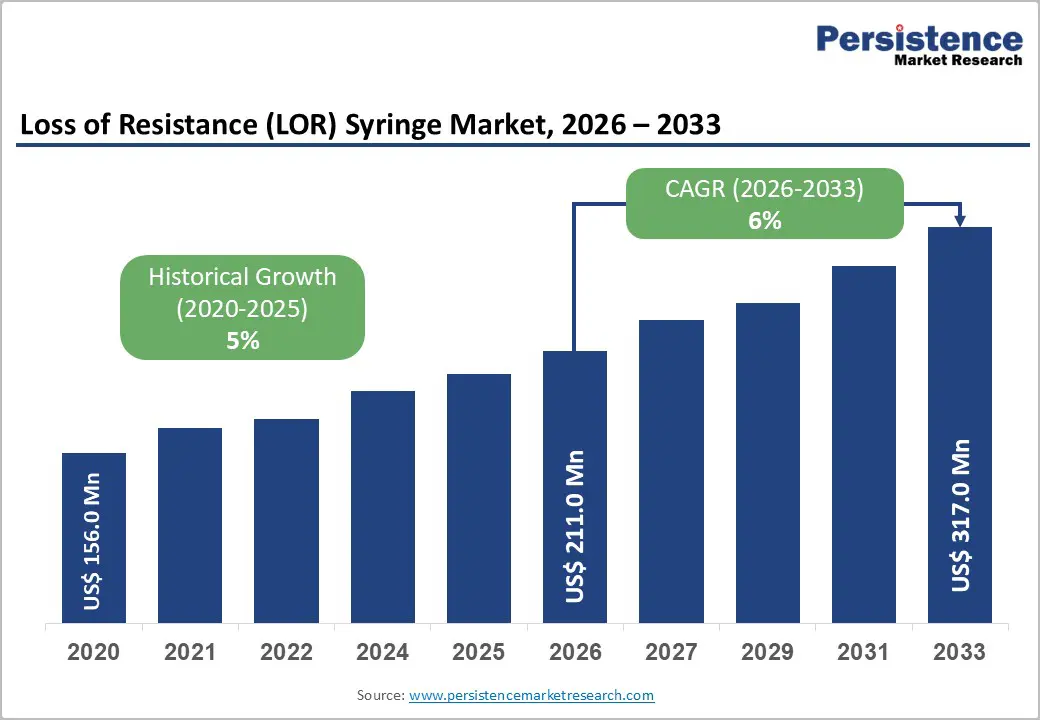

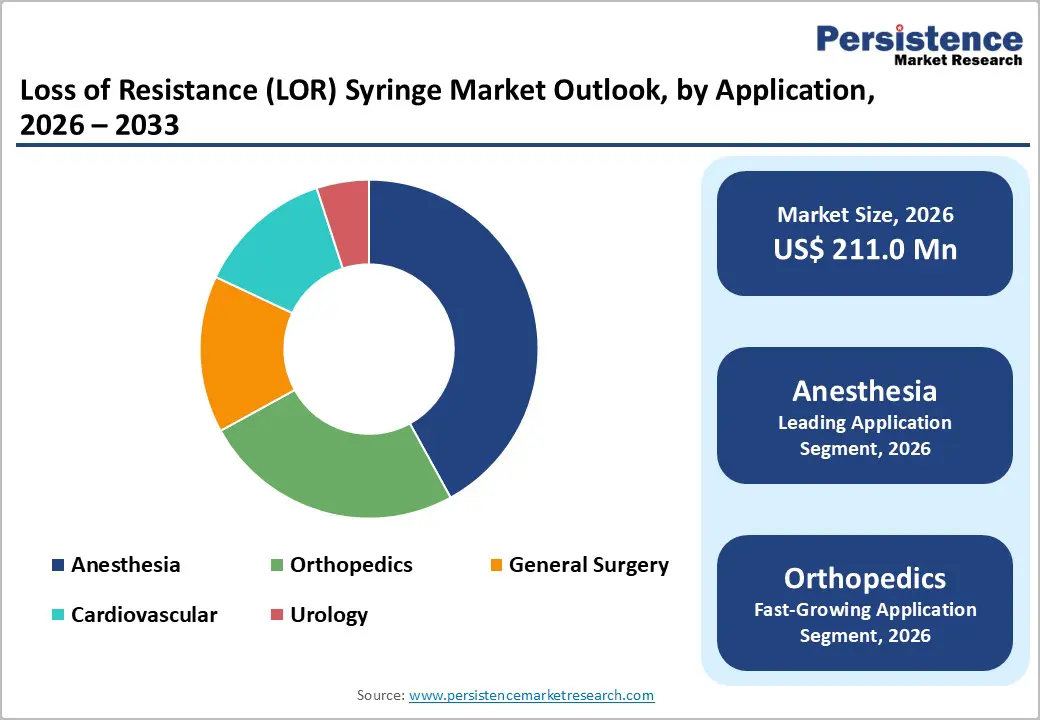

The global loss resistance (LOR) syringe market size is likely to be valued at US$ 211.0 million in 2026. It is projected to reach US$ 317.0 million by 2033, growing at a CAGR of 6% during the forecast period 2026 - 2033.

This market expansion is underpinned by rising global healthcare expenditure, increasing use of epidural anesthesia, and greater awareness of safe injection practices. Growing healthcare investments to address chronic disease burdens are strengthening demand for specialized syringes tailored to complex procedures. Ongoing technological improvements that enhance syringe performance, combined with broader use in pain management for chronic conditions and epidural interventions, further support growth. Loss-of-resistance syringes, engineered to improve accuracy in locating the epidural space, have become standard tools in anesthesia delivery across hospitals and dedicated pain management clinics worldwide.

Key Industry Highlights

- Leading & Fastest-growing Applications: Anesthesia is likely to lead with a projected 42% revenue share in 2026, with orthopedics exhibiting the highest 2026 - 2033 CAGR.

- Leading & Fastest-growing End-User: Hospitals are slated to dominate with an estimated 68% revenue share in 2026, while ambulatory surgical centers are expected to be the fastest-growing through 2033.

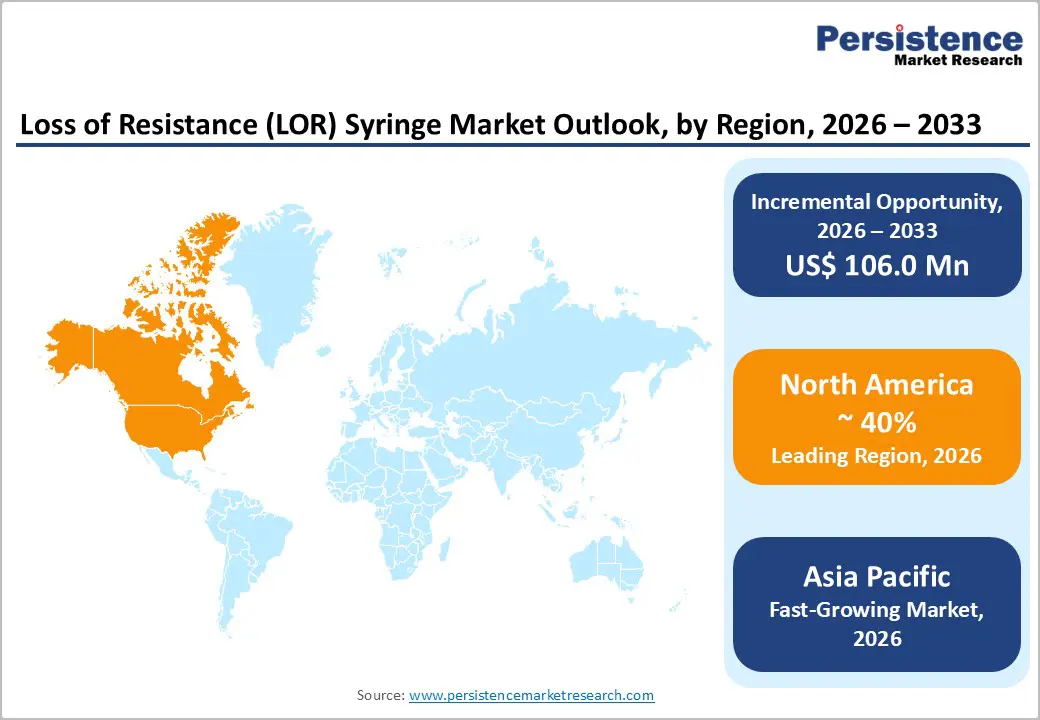

- Dominant Region: North America is expected to command about 40% market share in 2026, supported by a mature healthcare ecosystem and a strong culture of patient safety and quality standards.

- Fastest-growing Regional Market: Asia Pacific is poised to be the fastest-growing regional market through 2033 due to rapid expansion of hospital and surgical infrastructure.

| Key Insights | Details |

|---|---|

| Loss of Resistance (LOR) Syringe Market Size (2026E) | US$ 211.0 Mn |

| Market Value Forecast (2033F) | US$ 317.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Volume of Surgical Procedures and Epidural Anesthesia Applications

The rising number of surgical procedures across the world is a central growth catalyst for the loss of resistance syringe market. Hospitals and surgical centers increasingly rely on regional and neuraxial anesthesia for procedures such as orthopedic, obstetric, and cardiovascular interventions, because these techniques support faster recovery pathways and more targeted pain control. As perioperative teams refine their protocols, they prioritize equipment that improves block success rates, standardizes technique across clinicians, and reduces the risk of complications. In this context, loss-of-resistance syringes serve as a critical enabler, helping anesthesia providers consistently identify the epidural space with greater confidence and better procedural control.

The global shift toward comprehensive pain management is reshaping how surgical and chronic pain services are organized. Health systems aim to reduce reliance on systemic opioids and instead expand interventional approaches, including epidural and regional blocks for both acute and chronic conditions. This trend creates sustained demand for specialized syringes that support repeatable, high-quality neuraxial access in operating rooms, labor and delivery units, and dedicated pain clinics. The aging population, which typically undergoes more frequent and complex surgeries, combined with improving access to surgical care in emerging markets, further amplifies the need for reliable loss-of-resistance devices. For manufacturers and providers, aligning product design, training, and procurement strategies with these clinical and demographic trends is essential to capture long-term value in this evolving markets.

Risk of Complications and Technique Variability

The LOR market growth faces important structural challenges related to how clinicians perform the loss of resistance technique, whether they use saline or air for epidural space detection. Differences in technique can introduce procedural variability, which may influence block quality and perceived safety. Epidural anesthesia carries inherent clinical risks, such as dural puncture headaches, nerve injury, infection at the injection site, bleeding complications, and cardiovascular effects associated with local anesthetic systemic toxicity. These potential complications, even when infrequent in experienced hands, can create hesitation among healthcare providers and patients, especially in facilities that have limited anesthesia expertise or inconsistent training practices.

The technique-dependent nature of epidural procedures requires substantial, ongoing education and hands-on experience, which can constrain adoption in hospitals and clinics that lack specialized pain management or anesthesia teams. Clinicians can choose from alternative pain management options, such as peripheral nerve blocks, general anesthesia, and pharmacological regimens, which may appear more straightforward in certain clinical scenarios and thereby reduce reliance on epidural techniques. Regulatory focus on device safety and clinical outcomes further increases complexity for manufacturers, who must demonstrate consistent product quality, robust risk-mitigation features, and clear clinical value through rigorous validation.

Strengthening Adoption of Advanced Medical Devices in Outpatient and ASCs

The healthcare industry’s transition toward outpatient surgical procedures and ambulatory surgical centers presents a significant growth avenue for the loss of resistance syringe market. Ambulatory surgical centers and day-care facilities increasingly adopt regional and neuraxial anesthesia techniques for procedures such as orthopedic, gynecological, urological, and soft-tissue interventions, because these approaches support faster recovery and efficient patient turnover. Epidural anesthesia provides targeted pain control while enabling same-day discharge, which helps providers manage capacity and control costs within value-based care models. As clinical teams refine enhanced recovery protocols, they integrate regional anesthesia more systematically to achieve better pain relief with fewer systemic opioid requirements, aligning with institutional strategies to address opioid dependence and improve patient satisfaction.

Beyond perioperative use, specialized chronic pain clinics represent an expanding end-user segment for loss of resistance syringes. These centers routinely employ epidural injections and related neuraxial interventions to manage conditions such as radiculopathy, spinal stenosis, and chronic low back pain, which creates recurring device demand outside the traditional operating room environment. This shift broadens the addressable market for epidural-related devices and encourages manufacturers to tailor offerings to outpatient workflows. Product innovations that emphasize portability, intuitive design, and clear feedback during epidural space identification, and integrated safety features can strengthen adoption in these settings.

Category-wise Analysis

Application Insights

Anesthesia is the leading application segment with a projected 42% of the loss of resistance syringe market revenue share in 2026. The anesthesia segment benefits from several structural advantages. It applies to a wide range of procedures, relies on well-established clinical protocols and practitioner expertise, and is supported by a strong evidence base for efficacy and safety. Obstetric anesthesia is particularly important, because epidural techniques play a central role in labor and delivery care in many hospital systems. Beyond the operating room, therapeutic epidural injections for chronic pain conditions such as herniated discs, spinal stenosis, cancer-related pain, and post-herpetic neuralgia generate ongoing device use that does not depend on surgical case volumes.

Orthopedics is likely to be the fastest-growing segment during the 2026 - 2033 forecast period. The aging global population is associated with a higher incidence of degenerative joint diseases, while increasing sports-related injuries create a greater need for surgical intervention in younger patients. At the same time, advances in minimally invasive orthopedic techniques encourage wider use of regional anesthesia, which offers benefits in pain control, early mobilization, and shorter hospital stays. Within this context, procedures such as hip and knee replacement surgeries increasingly employ epidural or combined spinal-epidural techniques, which creates sustained demand for reliable epidural anesthesia systems and loss of resistance syringes.

End-User Insights

Hospital is slated to be the dominant with an estimated 68% of market revenue share in 2026. Major hospitals and medical centers perform most surgical procedures that require epidural anesthesia, maintain dedicated anesthesiology departments with trained personnel, and hold comprehensive inventories of anesthesia-related medical devices. The hospital segment benefits from centralized procurement structures that support volume purchasing, long-standing relationships with distributors, and quality assurance processes that uphold consistent product standards and regulatory compliance. Within hospitals, emergency departments and labor and delivery units are particularly intensive users of epidural anesthesia, generating steady baseline demand for loss of resistance syringes and related devices regardless of fluctuations in elective surgery volumes.

Ambulatory surgical centers are expected to be the fastest-growing during the 2026 - 2033 forecast period. This accelerated expansion is driven by healthcare delivery model shifts toward cost-effective outpatient settings, favorable reimbursement policies from Medicare and private insurers, and patient preferences for same-day surgical experiences with reduced costs and convenience. ASCs are increasingly capable of performing complex procedures including spine surgery and total joint replacements due to advances in surgical tools and patient monitoring systems. The segment benefits from lower overhead costs compared to hospitals, streamlined workflows optimizing efficiency, and specialized focus enabling high-volume standardized procedures.

Modality Type Insights

Disposable segment currently leads with an approximate 60% market share in 2026. The disposable segment benefits from regulatory preferences and hospital policies that mandate single-use devices for invasive procedures, growing awareness of healthcare-associated infection risks, and cost-effectiveness when total costs such as sterilization and reprocessing are considered. Manufacturers now concentrate product development primarily on disposable variants to align with these demand patterns, which results in greater innovation, design refinement, and product variety within this segment. Modern disposable loss of resistance syringes uses advanced polymers and manufacturing techniques to deliver performance that is comparable to, or better than, traditional reusable options, while also providing a stronger safety profile for patients and healthcare staff.

Reusable is anticipated to be the fastest-growing segment during the 2026 - 2033 forecast period. Reusable loss of resistance (LOR) syringes can be sterilized and used multiple times, which makes them an economical option for facilities that handle high procedure volumes and have reliable reprocessing capability. Their robust construction and consistent performance often lead clinicians in certain hospitals, research centers, and specialty clinics to view them as a dependable choice for repeated use. The higher upfront purchase cost and the requirement for validated sterilization workflows, staff training, and documentation can restrict adoption in resource-constrained settings or smaller practices that may lack sufficient infrastructure.

Regional Insights

North America Loss Resistance Syringe Market Trends

North America is set to command a significant portion of the loss resistance syringe market share at approximately 40% in 2026. The market is characterized by characterized by a mature healthcare ecosystem, extensive surgical capacity, and a strong culture of patient safety and quality standards. The United States dominates regional demand because it has advanced hospital infrastructure, high volumes of obstetric, orthopedic, and spine procedures, and broad use of epidural anesthesia across perioperative and pain management pathways. Growth in this market is further supported by an aging population that requires more frequent surgical and interventional pain procedures, a substantial burden of chronic pain conditions managed with therapeutic epidural interventions, and well-established pain management and anesthesiology specialties that routinely rely on dedicated loss of resistance syringes.

The regional regulatory environment, led by the United States Food and Drug Administration (FDA) and Health Canada, enforces stringent quality, safety, and performance requirements, which reinforces trust in approved products and favors manufacturers with strong compliance capabilities. Large academic medical centers and teaching hospitals act as key opinion leaders, shaping clinical guidelines, training standards, and device preferences that then spread across wider provider networks. Canada reflects many of these characteristics, with universal healthcare coverage and standardized clinical pathways supporting steady procedure volumes, although at a smaller overall market scale than the United States. Mexico and other parts of the region offer emerging growth potential, driven by healthcare modernization, expansion of private hospital groups, and medical tourism that increases demand for high-quality anesthesia disposables.

Europe Loss Resistance Syringe Market Trends

Europe constitutes the second-largest regional market for loss resistance syringes, representing approximately 30% of the global market share with steady growth driven by advanced healthcare systems and aging demographics. Germany, United Kingdom, France, and Spain represent the largest individual country markets, collectively accounting for the majority of European demand. Within this context, Germany stands out as the largest individual market due to its extensive hospital network, strong surgical capacity, and established medical device industry, while the United Kingdom, France, and Spain contribute significant volumes through centralized or regionally coordinated health systems undergoing continuous modernization.

The regulatory setting is shaped by the European Union (EU) Medical Device Regulation (EU MDR), which harmonizes technical and safety standards across member states and requires robust documentation, clinical evaluation, and quality system controls from manufacturers. Once devices meet MDR requirements, companies can leverage a single approval to access multiple national markets, although the cost and complexity of compliance favor well-resourced players with strong regulatory and quality capabilities. The competitive environment combines large multinational manufacturers and specialized European firms with strong local or regional positions, all operating under growing pressure to support value-based procurement, cost containment, and sustainable product design.

Asia Pacific Loss Resistance Syringe Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing loss resistance syringe market through 2033, supported by large patient populations, rising healthcare expenditure, and rapid expansion of hospital and surgical infrastructure. The increasing awareness of effective pain management and the rising number of surgical procedures across Asia Pacific are key factors driving sustained demand for loss of resistance syringes in the region. As hospitals and surgical centers expand the use of regional and neuraxial anesthesia for procedures such as obstetric, orthopedic, urological, and abdominal interventions, clinicians place greater emphasis on reliable identification of the epidural space to enhance safety and patient outcomes. This shift directly supports higher utilization of specialized LOR syringes compared with generic alternatives, particularly in tertiary and referral centers that manage complex cases.

Government initiatives to improve healthcare access, expand public insurance coverage, and upgrade perioperative services further reinforce this momentum by increasing the number of patients who qualify for surgery and structured pain management pathways. At the same time, the expanding middle-class population with higher disposable incomes is more likely to seek hospital-based care and expect quality standards that align with international practices, which includes a preference for advanced single-use devices designed for safety and consistency. As health systems in China, India, and ASEAN countries modernize their infrastructure and clinical protocols, they create a more supportive environment for wider adoption of specialized loss of resistance syringes in both public and private facilities.

Competitive Landscape

The global loss of resistance syringe market structure is moderately concentrated, dominated by leading players such as Becton, Dickinson and Company, Terumo Corporation, B. Braun Melsungen AG, Smiths Medical, and Teleflex Incorporated. Market concentration highlights the advantages of scale, including global distribution reach, broad product portfolios, strong customer relationships, and research and development capabilities that support ongoing innovation. Larger companies also gain from brand recognition among healthcare professionals, deep regulatory experience that streamlines multi-country approvals, and manufacturing efficiencies that support competitive pricing. The market still provides room for smaller players that can differentiate through regional specialization, focused product features, or value-oriented pricing strategies.

Key Industry Developments

- In June 2025, Flat Medical signed a dealership agreement with Mercury Medical to distribute its EpiFaith smart syringe in the U.S. EpiFaith replaces the traditional tactile loss-of-resistance method with an objective visual signal, helping anesthesiologists locate the epidural space more accurately, keep both hands on the needle, and reduce accidental dural punctures.

- In January 2025, BD invested over US$ 10 million to add new syringe and needle production lines in Connecticut and Nebraska, boosting U.S. capacity for safety-engineered injection devices by more than 40% and conventional syringes by over 50%, and creating 215+ jobs.

Companies Covered in Loss of Resistance (LOR) Syringe Market

- Becton, Dickinson and Company

- Terumo Corporation

- B. Braun Melsungen AG

- Smith’s Medical

- Teleflex Incorporated

- Nipro Corporation

- Weigao Group Medical Polymer Company Limited

- Gerresheimer AG

- Owen Mumford Ltd

- PAJUNK GmbH Medizintechnologie

- Vygon SA

- Well Lead Medical Co., Ltd.

- Zhejiang Fert Medical Device Co., Ltd.

- Vogt Medical Vertrieb GmbH

- Medline Industries, Inc.

Frequently Asked Questions

The global loss of resistance (LOR) syringe market is projected to reach US$ 211.0 million in 2026.

The market is primarily driven by growing surgical and epidural procedure volumes, rising patient-safety and infection-control requirements, and technological improvements.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Expanding healthcare infrastructure, development of smart and eco-friendly safety syringes, and increased use of regional anesthesia in ambulatory and outpatient settings.

Becton, Dickinson and Company, Terumo Corporation, B. Braun Melsungen AG, Smiths Medical, and Teleflex Incorporated are some of the key players in the market.