- Medical Devices

- Pulmonology Devices Market

Pulmonology Devices Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Pulmonology Devices Market by Product Type (Airway Extraction Baskets, Endobronchial Ultrasound (EBUS) Needles, Single-Use Bronchoscopes, Airway Stents, Pulmonary Biopsy Devices, Others), Indication (Chronic Obstructive Pulmonary Disease (COPD), Asthma, Sleep Apnea / Sleep Disorders, Lung Cancer, Tracheal & Bronchial Stenosism, Foreign Body Extraction, Others), End-user (Hospitals, Pulmonology Clinics, Ambulatory Surgical Centers, Others), and Regional Analysis from 2026 to 2033

Pulmonology Devices Market Share and Trends Analysis

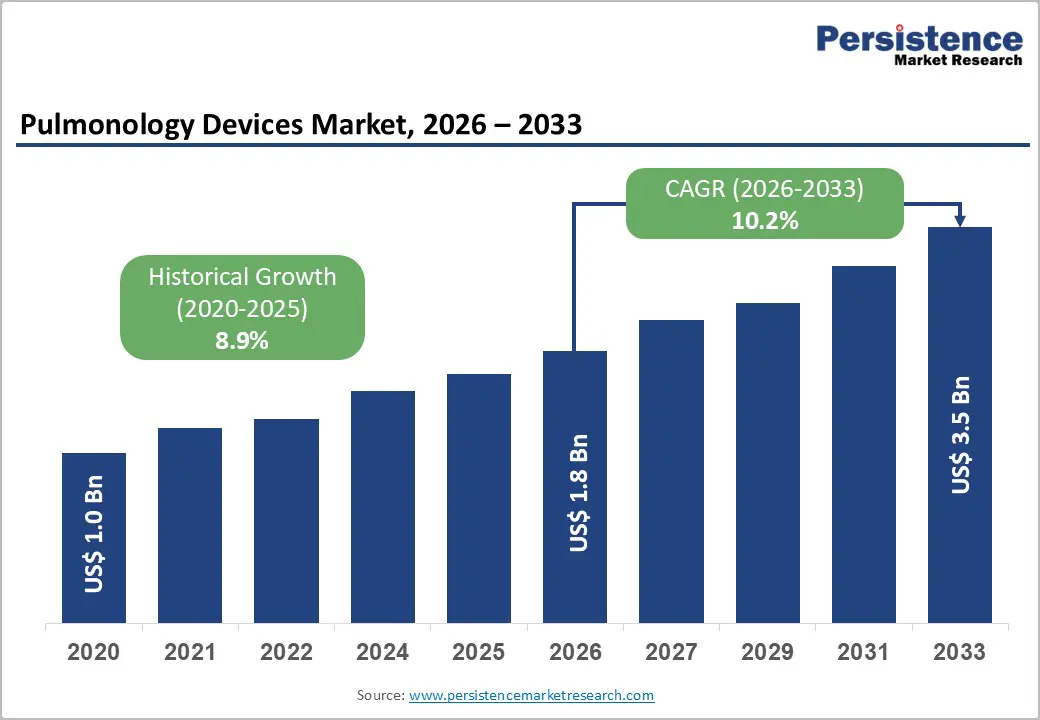

The global pulmonology devices market is estimated to grow from US$ 1.8 billion in 2026 to US$ 3.5 billion by 2033. The market is projected to record a CAGR of 10.2% from 2026 to 2033.

The global market is expanding steadily, driven by the rising prevalence of COPD, asthma, lung cancer, and sleep disorders, along with the growing demand for minimally invasive diagnostic and therapeutic procedures. North America leads due to advanced healthcare infrastructure and high device adoption, while the Asia Pacific is the fastest-growing region supported by healthcare investments, improving access, and increasing disease burden.

Key Industry Highlights:

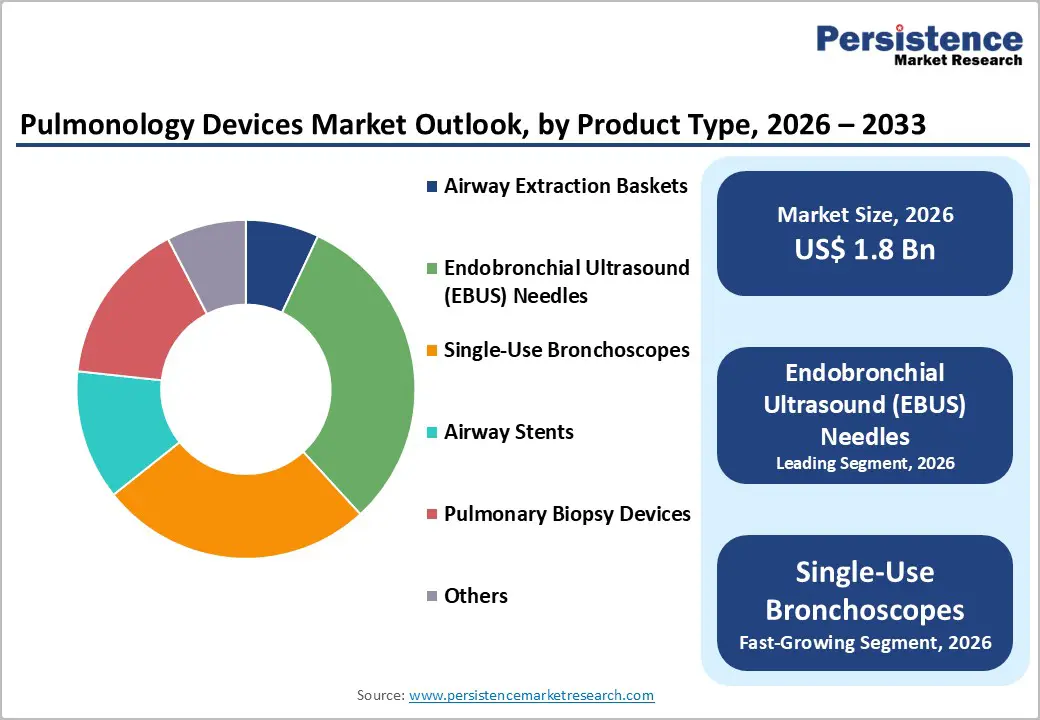

- Dominant Product Segment: Endobronchial Ultrasound (EBUS) Needles holds 31.2% share in 2025, driven by rising lung cancer incidence, increasing preference for minimally invasive diagnostic procedures, and wider adoption of EBUS-guided transbronchial needle aspiration. Their high diagnostic yield, real-time imaging capability, lower risk of complications, and shorter hospital stays compared to surgical biopsy methods continue to strengthen demand across hospitals worldwide.

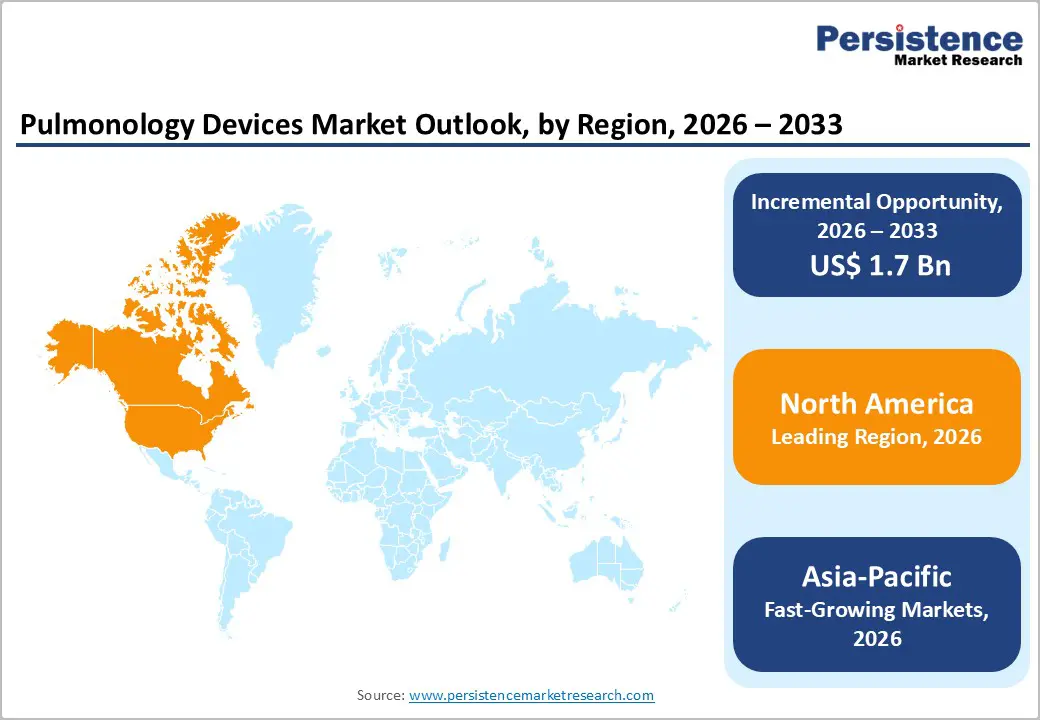

- Dominant Region: North America leads the pulmonology devices market in 2025 with 46.2% share, supported by advanced healthcare infrastructure, high adoption of minimally invasive bronchoscopy technologies, strong reimbursement frameworks, and significant prevalence of chronic respiratory diseases.

- Growth Indicators: Growth is driven by rising incidence of COPD, asthma, lung cancer, and sleep apnea; increasing demand for early and minimally invasive diagnosis; technological advancements in EBUS and single-use bronchoscopes; and expanding home respiratory care.

- Market Opportunity: Opportunities include expanding portable and home-based respiratory devices, integrating AI-enabled diagnostic bronchoscopy, growing in emerging markets, developing cost-effective single-use devices, and forging strategic hospital partnerships.

| Key Insights | Details |

|---|---|

| Pulmonology Devices Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 3.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Dynamics

Driver: Technological Advancements in Bronchoscopy and EBUS Systems

Technological innovation in bronchoscopy, including Endobronchial Ultrasound (EBUS) and navigation systems, has significantly enhanced diagnostic precision and procedural outcomes in respiratory care. EBUS allows real-time ultrasound visualization during biopsy and mediastinal staging, reducing the need for more invasive surgical procedures such as mediastinoscopy. The American College of Chest Physicians reports that utilization of EBUS has increased approximately 400% since 2010, reflecting its clinical value in diagnosing lung cancers and complex thoracic conditions. These advancements also support improved detection of peripheral lesions with combined systems such as electromagnetic navigation bronchoscopy (ENB), which employs CT-based 3D airway mapping to guide instruments deep into the lung.

The rising global burden of respiratory diseases further justifies investment in advanced bronchoscopic tools. Conditions like COPD and lung cancer require precise sampling and staging to inform treatment plans. According to the WHO, chronic respiratory diseases like COPD are among the leading causes of death worldwide, causing 3.5 million deaths in 2021 and affecting millions more. As disease prevalence rises with aging populations and environmental risk factors such as air pollution, clinicians increasingly rely on advanced bronchoscopy and EBUS systems as critical diagnostics and interventional tools, directly driving market demand.

Restraint: High Cost of Advanced Pulmonology Devices

One of the principal restraints in the pulmonology devices market is the very high cost of advanced equipment, which limits accessibility and adoption, especially in resource-constrained settings. For example, sophisticated bronchoscopic and navigational systems, such as robotic-assisted platforms or advanced imaging-integrated bronchoscopy suites, can require capital investments of hundreds of thousands of dollars. These costs include not only the hardware purchase but also ongoing maintenance, software upgrades, and specialized operator training. Smaller hospitals and clinics, particularly in low- and middle-income regions, often struggle to justify such high expenditures, resulting in uneven distribution of advanced pulmonary diagnostics and care.

Cost pressures are compounded by healthcare reimbursement limitations and out-of-pocket spending burdens. Government health systems and insurers are frequently cautious about adopting new payment models for complex procedures and premium devices, delaying clinical integration and reducing clinicians' willingness to invest in costly tools without assured reimbursement. Data from the U.S. CDC show that COPD and related chronic lower respiratory conditions contribute significantly to healthcare costs and hospital admissions, yet financial barriers remain a major challenge to scaling advanced diagnostics and early intervention programs. Until cost barriers are addressed through policy support, subsidies, or scalable device innovations, high prices are likely to restrain widespread adoption in many global markets.

OPPORTUNITY: Integration of AI in Respiratory Diagnostics and Imaging

The integration of Artificial Intelligence (AI) into respiratory diagnostics represents a significant opportunity for the pulmonology devices market by enhancing diagnostic accuracy and workflow efficiency. AI-driven image analysis, anomaly detection, and decision-support algorithms can assist clinicians in interpreting complex data from CT scans, bronchoscopy images, and pulmonary function tests. For instance, in the AI in respiratory diseases segment, CT scan imaging held a 31.6% revenue share in 2024, reflecting its central role, and AI integration further improves detection accuracy and clinical throughput while reducing interpretation time. Academic research also demonstrates the strong performance of machine learning models in pulmonary disease prediction and detection, highlighting AI’s potential in both specialized care and broader screening contexts.

Government and health institutions are increasingly supporting AI adoption to address the burdens of respiratory disease. Chronic respiratory diseases, including asthma and COPD, remain among the top global causes of death and disability, making early and precise diagnosis essential to reducing morbidity. AI can also enhance telemedicine and remote diagnostics, enabling pulmonology providers to expand services to underserved regions with limited access to specialists. Cloud-based and AI-assisted tools have shown higher adoption rates in mid-sized clinics than purely on-premises systems, indicating a scalable model for broader market penetration. As healthcare systems seek to improve outcomes while controlling costs, AI-augmented pulmonary device solutions offer a major opportunity to transform respiratory care delivery.

Category-wise Analysis

By Product Type Insights

Endobronchial Ultrasound (EBUS) needles is leading with 31.2% share in 2025, due to its extensive production and ubiquitous use in both culinary and health applications. India alone contributes over 75-80% of global turmeric production, with an estimated 11.6 lakh tonnes cultivated across ~3.24 lakh ha in 2022-23, supporting its prominence in the spice trade and organic segment alike. Turmeric’s integration into traditional cuisines, decorative dyes, and medicinal systems like Ayurveda cements its demand across households and commercial food processors.

The spice’s bioactive compound curcumin has attracted global health-conscious consumers, driving turmeric inclusion in functional foods, beverages (e.g., golden milk), nutraceuticals, and natural supplements. Government backing, such as the establishment of the National Turmeric Board aimed at expanding exports and product development, also supports turmeric’s dominant position within organic spices.

By Indication Insights

Chronic Obstructive Pulmonary Disease (COPD) dominates because it is one of the most prevalent and costly respiratory conditions globally, necessitating long-term diagnostics, monitoring, and supportive care. The World Health Organization reports COPD as the third leading cause of death worldwide, responsible for an estimated 3.23 million deaths in 2019. (who.int) Aging populations, persistent smoking, and rising air pollution increase COPD incidence, driving widespread use of spirometers, oxygen therapy systems, ventilators, and monitoring devices. In the U.S., COPD accounted for over 1.5 million emergency department visits in 2018, with frequent exacerbations requiring hospital support. (cdc.gov) These factors make COPD the largest clinical indication for pulmonology devices, as clinicians prioritize early detection, disease management, and reduction of acute exacerbations.

Regional Insights

North America Pulmonology Devices Market Trends

North America dominates the pulmonology devices market, with a 46.2% share, driven by advanced healthcare infrastructure, a high disease burden, and robust adoption of medical technology. The Centers for Disease Control and Prevention (CDC) reports that over 16 million Americans have been diagnosed with COPD, and millions more remain undiagnosed, underscoring the heavy use of spirometry, ventilators, and respiratory monitoring. The U.S. also records a high incidence of lung cancer, with over 230,000 new cases annually, driving demand for diagnostic bronchoscopy and EBUS tools. Widespread insurance coverage and reimbursement for advanced procedures incentivize hospitals to invest in cutting-edge pulmonology devices, while strong clinical research and training ecosystems accelerate the adoption of innovations, solidifying North America’s leadership in the global market.

Europe Pulmonology Devices Market Trends

Europe is an important region in pulmonology devices due to a high prevalence of chronic respiratory diseases and strong healthcare systems that emphasize early diagnosis and management. According to the European Lung Foundation, respiratory diseases affect approximately one in five Europeans, with COPD and asthma among the most common conditions. Lung cancer remains a leading cause of cancer mortality in Europe, with over 270,000 deaths annually, reinforcing the need for advanced diagnostic and interventional pulmonology solutions. Countries like Germany, France, and the U.K. have well-established reimbursement systems that support access to complex procedures such as EBUS and navigational bronchoscopy. European regulatory frameworks also facilitate device innovation and safety, making the region a key market for both device utilization and clinical research contributions.

Asia-Pacific Pulmonology Devices Market Trends

Asia Pacific is the fastest-growing region due to rising respiratory disease burden, expanding healthcare access, and increasing investment in medical infrastructure. The World Health Organization notes that countries like China and India contribute significantly to global COPD and lung cancer cases, driven by high smoking rates and air pollution exposure. Rapid economic development has led to expanding hospital networks, increased ICU capacity, and broader adoption of advanced diagnostic tools such as bronchoscopy and EBUS. Growing health awareness and government initiatives to improve access to respiratory care further fuel demand. For example, China’s Healthy China 2030 plan prioritizes chronic disease management, including respiratory conditions, thereby boosting demand for pulmonology devices. Coupled with rising disposable incomes, these factors accelerate market growth across the Asia Pacific.

Competitive Landscape

The pulmonology devices market is highly competitive, led by major medical technology companies such as Medtronic, Philips Healthcare, Boston Scientific, and Olympus. Firms focus on technological innovation, minimally invasive solutions, regulatory approvals, and strategic hospital partnerships, while expanding portfolios in bronchoscopy, ventilators, and home respiratory care to strengthen global market presence.

Key Industry Developments:

- In October 2025, Boston Scientific announced that it had completed the acquisition of Asthmatx, a medical device company focused on developing minimally invasive treatments for severe asthma. The acquisition strengthened Boston Scientific’s interventional pulmonology portfolio by adding innovative bronchoscopic technologies designed to improve outcomes for patients with uncontrolled asthma.

- In January 2025, Ambu announced the launch of a new video laryngoscopy solution designed to enhance airway management and improve visualization during intubation procedures. The company introduced the system as part of its expanding single-use endoscopy portfolio, aiming to provide clinicians with improved image quality, ergonomic handling, and infection control advantages compared to reusable devices.

Companies Covered in Pulmonology Devices Market

- Ambu A/S

- Boston Scientific Corporation

- Chart Industries (CAIRE)

- CONMED Corporation

- Cook Medical

- Drägerwerk AG & Co. KGaA

- Drive DeVilbiss Healthcare

- Fisher & Paykel Healthcare Limited

- FUJIFILM Corporation

- GE HealthCare

- Hamilton Medical AG

- Hunan Vathin

- Inogen Inc.

- Karl Storz

- Koninklijke Philips N.V. (Philips Healthcare)

- Medtronic

- ResMed

- Others

Frequently Asked Questions

The global pulmonology devices market is projected to be valued at US$ 1.8 Bn in 2026.

Rising respiratory disease prevalence, aging population, technological advancements, and expanding critical care infrastructure.

The global pulmonology devices market is poised to witness a CAGR of 10.2% between 2026 and 2033.

AI integration, portable devices, emerging markets expansion, homecare growth, minimally invasive innovations.

Ambu A/S, Boston Scientific Corporation, Chart Industries (CAIRE), CONMED Corporation, Cook Medical, Drägerwerk AG & Co. KGaA.