- Advanced Materials

- Leather Dyes Market

Leather Dyes Market Size, Share, and Growth Forecast 2026 - 2033

Leather Dyes Market by Formulation (Water-based/Aqueous, Liquid Form, Powder/Dust Form, Solvent-based, Others), Application (Footwear, Garment, Automobile, Furniture, Others), and Regional Analysis for 2026 - 2033

Leather Dyes Market Size and Trend Analysis

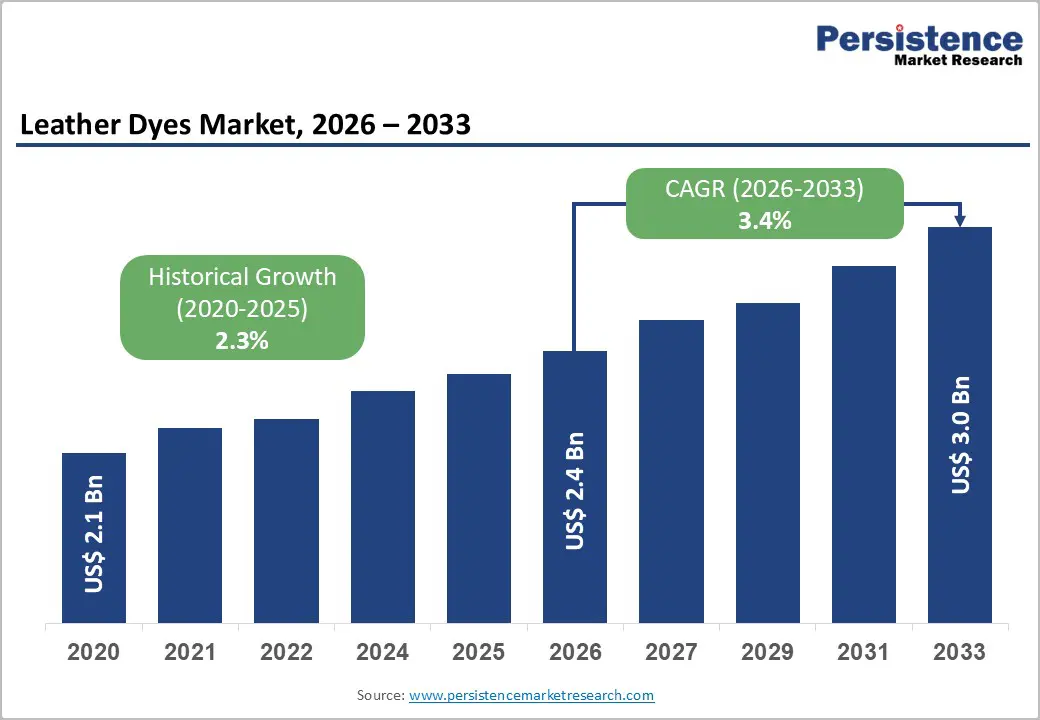

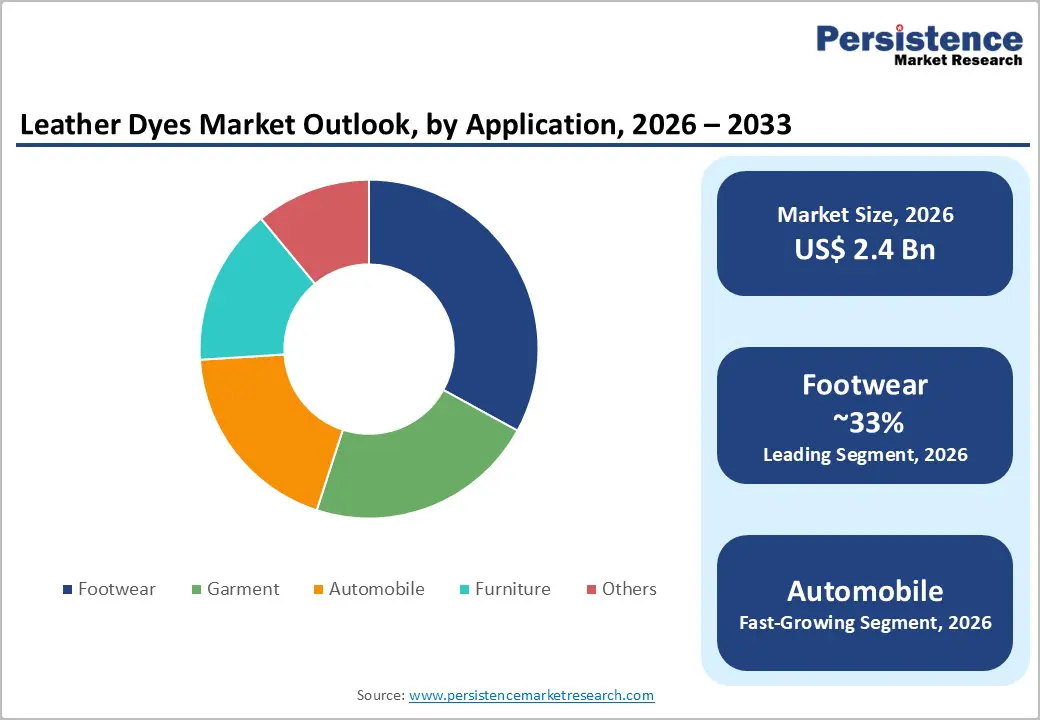

The global Leather Dyes market is valued at approximately US$ 2.4 Bn in 2026 and is projected to reach US$ 3.0 Bn by 2033, growing at a CAGR of 3.4% between 2026 and 2033.

This measured but consistent expansion is driven by sustained demand from the global leather processing industry, led by the footwear, automotive interior, and furniture segments, which collectively account for the largest volumes of coloured leather output worldwide. The global footwear segment alone represents the single largest application for leather dyes, with footwear accounting for approximately 32% of all leather dye consumption, underpinned by robust export-oriented production in China, India, Vietnam, and Bangladesh.

Key Market Highlights

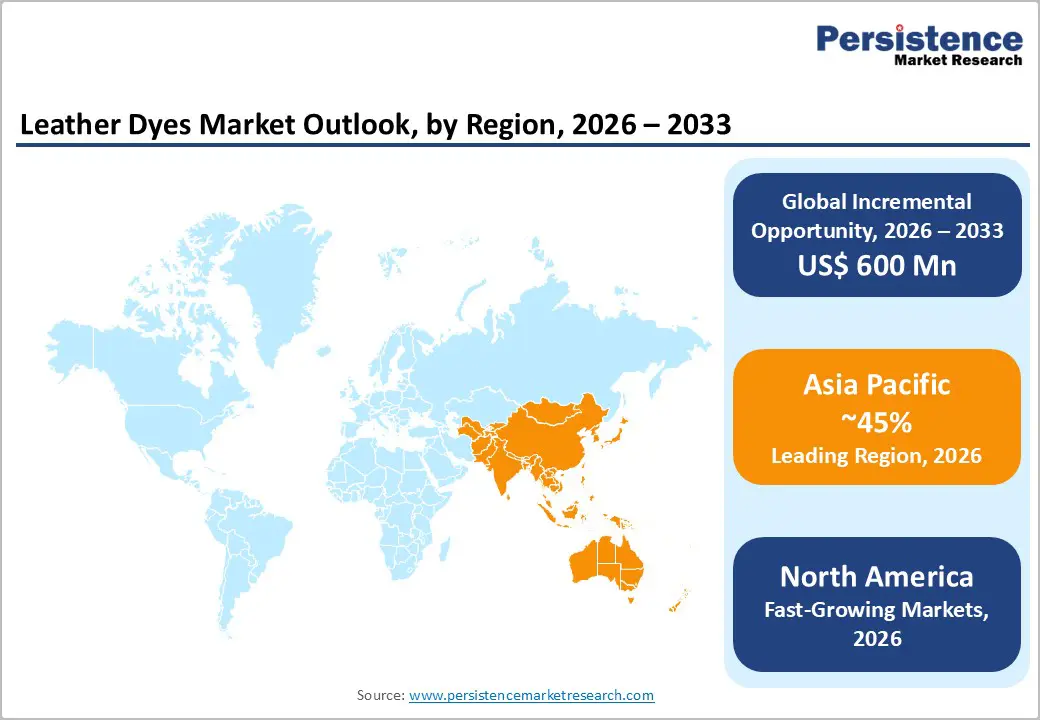

- Leading Region – Asia Pacific leads the global Leather Dyes market with approximately 45% revenue share, anchored by the world's largest tannery clusters in China and India, massive footwear export production in Vietnam and Bangladesh, and growing domestic leather goods demand.

- Fastest-Growing Region – North America holds approximately 18% of the global Leather Dyes market revenue in 2026, led by the United States where demand is anchored in the automotive, footwear, and premium furniture sectors.

- Dominant Segment – The Footwear application segment leads with approximately 33% of the global Leather Dyes market revenue, underpinned by global footwear production exceeding 24 billion pairs annually and concentrated export-oriented manufacturing across China, India, Vietnam, and Ethiopia.

- Fastest-Growing Segment – Water-based dye formulations are the leading and fastest-growing formulation category (~48% share), driven by EU REACH restrictions on hazardous azo dyes, ZDHC MRSL compliance mandates, and brand-owner sustainability requirements compelling global tannery reformulation.

- Key Market Opportunity – The global shift toward sustainable leather processing is creating high-margin growth potential in certified bio-based, water-based dye systems, with the EU's €4.05 million Fabulose project, Stahl's 2024 bio-dye launch, and brand sustainability mandates driving rapid adoption.

| Key Insights | Details |

|---|---|

|

Leather Dyes Market Size (2026E) |

US$ 2.4 Billion |

|

Market Value Forecast (2033F) |

US$ 3.0 Billion |

|

Projected Growth CAGR (2026–2033) |

3.4% |

|

Historical Market Growth (2020–2025) |

2.3% |

DRO Analysis

Market Growth Drivers

Expanding Global Footwear and Leather Goods Industry

The most significant structural driver for the global Leather Dyes market is the sustained growth of the worldwide footwear and leather goods industry, which generates the single largest volume demand for colorants across all leather applications. According to the World Footwear Yearbook, global footwear production exceeded 24 billion pairs in recent years, with China, India, Vietnam, and Bangladesh collectively accounting for the majority of global leather footwear output.

The footwear segment alone constitutes approximately 32% of total leather dye consumption, driven by the need for consistent color matching, vibrant seasonal shades, abrasion resistance, and durability. Simultaneously, rising disposable incomes in the Asia Pacific and Latin America are fuelling demand for premium leather accessories, handbags, and belts, which require specialized dye formulations offering superior color fastness and depth.

Rising Automotive Leather Interior Demand and Premiumization

The global automotive industry's persistent preference for high-quality leather interiors in premium and mid-range passenger vehicles constitutes a major, stable demand source for specialized leather dyes. Automotive leather requires dye systems that deliver exceptional colorfastness under UV exposure, heat cycles, and abrasion performance specifications substantially more demanding than those for footwear or garment leather.

According to OICA (Organization Internationale des Constructeurs d'Automobiles), global automobile production exceeded 93 million vehicles in 2023, with a growing proportion of mid-range and luxury vehicles featuring genuine leather seating, dashboards, and door trim. The shift toward Electric Vehicles (EVs) is also influencing interior design trends, as automakers use distinctive color palettes and premium materials to differentiate EV interiors directly increasing demand for specialized, high-performance leather dye formulations.

Market Restraints

Stringent Chemical Regulations Restricting Traditional Dye Formulations

The Leather Dyes market faces significant compliance-driven restraints from the European Union's REACH Regulation (EC) No. 1907/2006), which restricts the use of carcinogenic azo dyes, chromium VI, formaldehyde, and other hazardous substances in leather and textile articles. REACH Annex XVII Entry 43 restricts azo dyes that can release specific aromatic amines above 30 mg/kg in leather articles contacting skin, and Entry 72 extends restrictions to multiple CMR substances used in textile and leather processing.

These regulatory mandates require tanneries and dye manufacturers to invest in reformulation and compliance testing, raising costs for smaller producers and restricting market access for legacy solvent-based products in European export supply chains.

Volatile Raw Material Prices and Environmental Compliance Costs

The Leather Dyes market is exposed to significant raw material price volatility, as key dye precursor chemicals, including aniline, naphthalene, and aromatic intermediates, are petrochemical derivatives subject to oil price fluctuations and supply chain disruptions. Rising environmental compliance costs, including wastewater treatment, effluent management, and certification against standards such as the Zero Discharge of Hazardous Chemicals (ZDHC) MRSL, are further compressing margins for mid-tier dye manufacturers. Stahl Holdings B.V. achieved ZDHC MRSL 3.1 Gateway certification for 2,151 products in January 2024, demonstrating the cost and effort required for full portfolio compliance in this increasingly regulated market.

Market Opportunities

Water-Based and Bio-Based Eco-Friendly Dye Formulations

The global transition toward sustainable leather processing presents one of the most compelling growth opportunities in the Leather Dyes market, as tanneries and brand owners shift away from solvent-based and hazardous chemical dye systems in response to regulatory pressure, consumer demand, and sustainability commitments. Stahl Holdings B.V. launched a new range of bio-based leather dyes in April 2024, reflecting the commercial maturation of green chemistry in leather colorant formulations.

The European Union provided €4.05 million in funding for DITF's Fabulose project aimed at developing eco-leather and greener dye technologies. In April 2024, researchers at Imperial College London engineered bacteria to produce self-dyeing animal-free leather, illustrating the frontier of sustainable bio-fabrication that could reshape dye-use models.

Automotive Electric Vehicle Interiors and Custom Color Formulation

The global shift toward Electric Vehicles (EVs) is creating a significant new application frontier for specialty leather dyes, as automakers design EV interiors with distinctive, fashion-forward color palettes to differentiate their platforms in the premium and luxury segments. Unlike traditional combustion vehicle interiors constrained by conservative colour choices, EV interior design is adopting bold, personalized colour statements, creating demand for high-performance dyes capable of delivering unique shades with exceptional lightfastness and thermal stability.

The International Energy Agency (IEA) reported that global EV sales surpassed 17 million units in 2024, with premium EV models from BMW, Mercedes-Benz, Tesla, and BYD featuring leather or bio-leather interiors. Simultaneously, the trend toward mass customization in fashion and automotive interiors is opening opportunities for dye houses offering quick-turnaround custom color formulation services for small-batch production, a niche ideally served by digitally enabled, flexible water-based dye dispensing systems increasingly deployed at the tannery level.

Category-wise Analysis

Formulation Insights

The Water-based/Aqueous formulation segment leads the global Leather Dyes market, accounting for approximately 48% of total revenue in 2026. Water-based leather dyes have displaced solvent-based alternatives across most developed-market tanneries as the default formulation standard, driven by compliance with the EU's REACH Regulation, the ZDHC MRSL industry standards, and brand owners' Restricted Substance Lists (RSLs) mandating low-VOC leather processing.

Water-based formulations offer effective penetration into chrome-tanned and vegetable-tanned hides, strong colorcast performance, compatibility with modern drum-dyeing equipment, and significantly reduced environmental and occupational health impact compared to solvent-based systems. Stahl Holdings B.V.'s STAHL NEO® 2024 product catalogue, specifically designed for low-impact leather finishing aligned with ZDHC MRSL standards, exemplifies the market's pivot toward aqueous systems.

Application Insights

The footwear application segment dominates the global Leather Dyes market, holding approximately 33% of total revenue in 2026. This leadership is rooted in the sheer scale of global leather footwear manufacturing the World Footwear Yearbook documents production of over 24 billion pairs annually, with leather shoes, safety footwear, and premium lifestyle footwear all requiring consistent, vibrant, and durable coloration. Footwear leather dyes must deliver uniform shade penetration across diverse grain structures, resistance to flexing, abrasion, and perspiration, and alignment with seasonal colour trends demanding both consistent quality and formulation flexibility.

Export-oriented tannery clusters in China, India, Vietnam, and Ethiopia process massive volumes of footwear leather, generating high-throughput demand for both bulk aqueous dye systems and specialty finishing colorants. The Automobile application is the second-largest segment, driven by OEM specifications for premium leather seats and trim coloration.

Regional Insights

Asia Pacific Leather Dyes Market Trends

Asia Pacific is both the largest producing and largest consuming region in the global Leather Dyes market, accounting for approximately 45% of global revenue in 2025, according to industry data. China dominates, operating the world's largest integrated leather tanning and finishing industry, with major cluster zones in Wenzhou, Guangzhou, and Hebei producing footwear leather, automotive leather, and leather accessories at massive scale. Chinese tanneries collectively consume the largest single volume of leather dyes globally, and Chinese dye manufacturers supplying both domestic and export markets compete aggressively on price while increasingly investing in water-based and low-impact formulations to meet international REACH and ZDHC compliance requirements for export-market tanneries.

India is the region's fastest-growing individual country market, with major tannery clusters in Tamil Nadu (Chennai, Vellore), West Bengal (Kolkata), and Uttar Pradesh serving global footwear, garment, and accessories leather markets. India's leather exports exceeded US$ 5 billion in recent years, with ongoing investments in effluent treatment plants and sustainable tanning driving the adoption of water-based leather dyes.

North America Leather Dyes Market Trends

North America holds approximately 18% of the global Leather Dyes market revenue in 2026, led by the United States, where demand is anchored in the automotive, footwear, and premium furniture sectors. The U.S. is home to significant automotive leather finishing demand, with OEM specifications from General Motors, Ford, and Stellantis as well as premium brands requiring leather dyes that meet stringent automotive interior durability and emissions standards. The Environmental Protection Agency (EPA) regulates VOC emissions from leather finishing operations, directly steering the market toward water-based and UV-curable dye systems.

Innovation in North America is concentrated around digitally enabled custom colour systems, sustainable dye chemistry, and certification frameworks. Archroma headquartered in Switzerland but with major operations in North America is a leading supplier of eco-forward dye solutions serving the region's leather and textile industries.

Europe Leather Dyes Market Trends

Europe is the most demanding and most technologically advanced regional market in the global Leather Dyes market, holding approximately 17–18% of global revenue in 2026. The region hosts the world's most stringent leather dye regulations under the European Chemicals Agency's (ECHA) administration of REACH, which restricts hazardous azo dyes in leather articles to a maximum of 0.003% by weight for skin-contact applications.

The EU's Zero Discharge of Hazardous Chemicals (ZDHC) MRSL standards are widely adopted by European tanneries and brand owners as supply chain requirements, driving mass reformulation toward certified water-based and bio-based dyes. Germany, Italy, and Spain are the dominant national markets, anchored by their world-class automotive (BMW, Mercedes-Benz, Volkswagen, SEAT) and luxury leather goods (Gucci, Prada, Zara) industries.

Italy is home to some of the world's most prestigious tanneries in the Arzignano and Solofra industrial districts is a critical demand centre for high-performance, aesthetically superior leather dye formulations serving luxury fashion brands. UK leather dye demand is driven by premium automotive suppliers and fashion houses.

Competitive Landscape

The global leather dyes market is moderately consolidated at the premium tier, with leading multinational specialty chemical companies Stahl Holdings B.V., TFL Ledertechnik GmbH, DyStar Singapore Pte Ltd, and Archroma collectively anchoring the top of the market through comprehensive product portfolios, global technical service networks, and regulatory compliance capabilities.

The top five players collectively hold approximately 40% of global market share, with the remainder fragmented among regional and national dye manufacturers in Asia Pacific, Latin America, and Eastern Europe. Key differentiators among leaders include REACH and ZDHC certified formulations, integrated technical service to tanneries, digital colour management tools, bio-based product portfolios, and automotive OEM qualification.

Key Developments:

- In April 2024, Stahl Holdings B.V. launched a new range of bio-based leather dyes designed to reduce environmental impact in leather tanning operations, reflecting the growing commercial demand for sustainable, plant-derived colorant systems in the leather processing industry.

- In April 2024, Imperial College London researchers engineered bacteria to grow animal-free, self-dyeing leather as a breakthrough in sustainable bio-fabrication, reducing the environmental impact of conventional leather dyeing and advancing vegan leather alternatives.

Companies Covered in Leather Dyes Market

- TFL Ledertechnik GmbH

- Stahl Holdings B.V.

- DyStar Singapore Pte Ltd

- Archroma

- Everlight Chemical Industrial Co.

- Colourtex Ind Ltd

- Burboya

- NK ITALIA

- Gayatri Industries

- Reactive Dyes

- Mordant Dyes

Frequently Asked Questions

The global Leather Dyes market is estimated to be valued at US$ 2.4 Billion in 2026 and is projected to reach US$ 3.0 Billion by 2033, registering a CAGR of 3.4% during the forecast period 2026-2033.

The primary drivers include the sustained growth of the global leather footwear industry with global production exceeding 24 billion pairs annually per the World Footwear Yearbook robust automotive leather interior demand aligned with OICA's reported global vehicle production of over 93 million units in 2023, and rising premiumization of leather goods in emerging markets.

The Water-based/Aqueous formulation segment is the leading category in the global Leather Dyes market, accounting for approximately 48% of total revenue in 2025. This dominance is driven by the widespread adoption of water-based dye systems as the default compliance-aligned choice for tanneries supplying leather to REACH-regulated European and North American brand markets.

Asia Pacific leads the global Leather Dyes market, accounting for approximately 45% of global revenue in 2025. China dominates, operating the world's largest integrated leather tanning industry across multiple cluster zones, while India's leather exports exceeding US$ 5 billion annually make it the region's fastest-growing market.

The leading companies in the global Leather Dyes market include Stahl Holdings B.V., TFL Ledertechnik GmbH, DyStar Singapore Pte Ltd, Archroma, Everlight Chemical Industrial Co., Colourtex Ind Ltd, LANXESS AG, Zschimmer & Schwarz, and Bodal Chemicals Ltd.