- Industrial Goods & Service

- Laminating Machines Market

Laminating Machines Market Size, Share, and Growth Forecast 2026 - 2033

Laminating Machines Market by Component (Wet Laminating Machines, Thermal Laminating Machines, Dry Bond Laminating Machines), Material (Paper, Plastic, Foil), End-Use Industry (Food and Beverages, Pharmaceutical, Personal Care and Cosmetics, Automotive, Aerospace and Defense, Others), and Regional Analysis for 2026 - 2033

Laminating Machines Market Size and Trend Analysis

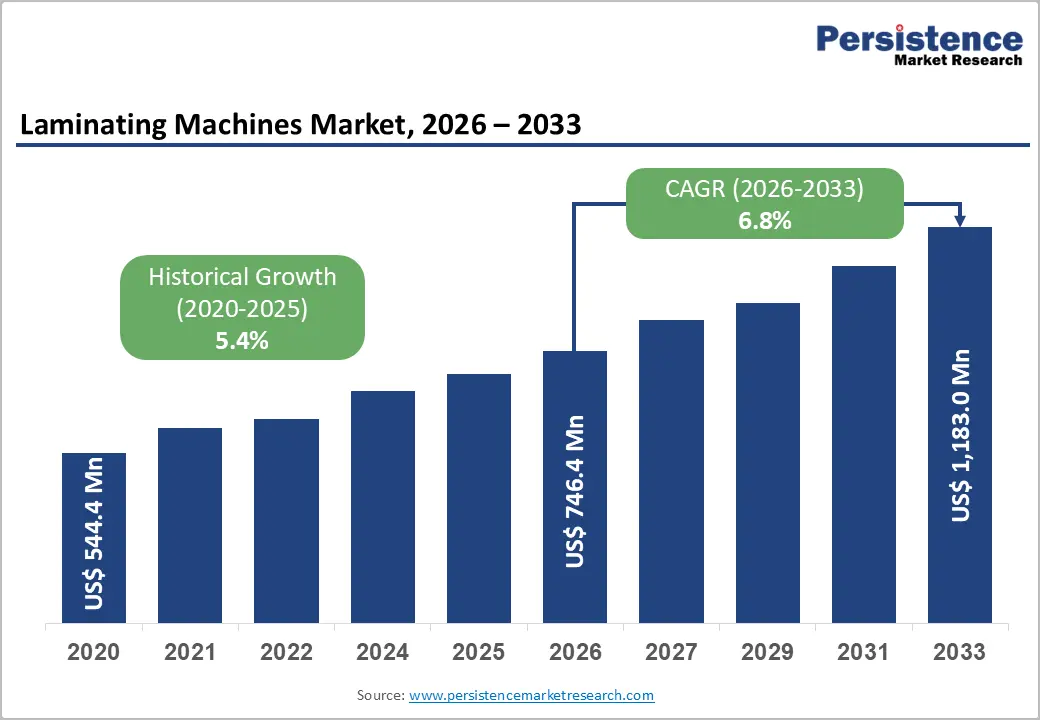

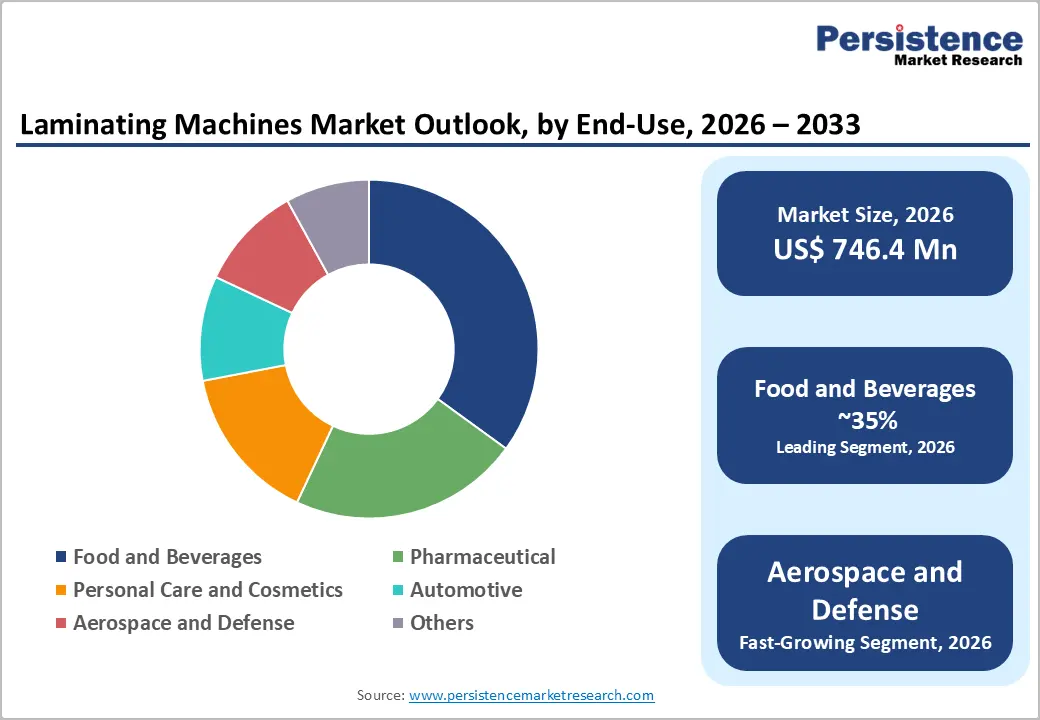

The global laminating machines market size is valued at US$ 746.4 Mn in 2026 and is projected to reach US$ 1,183.0 Mn by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

This robust expansion is primarily driven by escalating demand for flexible, high-barrier packaging across the food and beverages, pharmaceutical, and personal care sectors, where laminated materials ensure product integrity, extended shelf life, and regulatory compliance. The rapid growth of the flexible packaging industry, valued at over US$ 293 Bn globally in 2025, directly stimulates demand for advanced laminating equipment.

Key Market Highlights

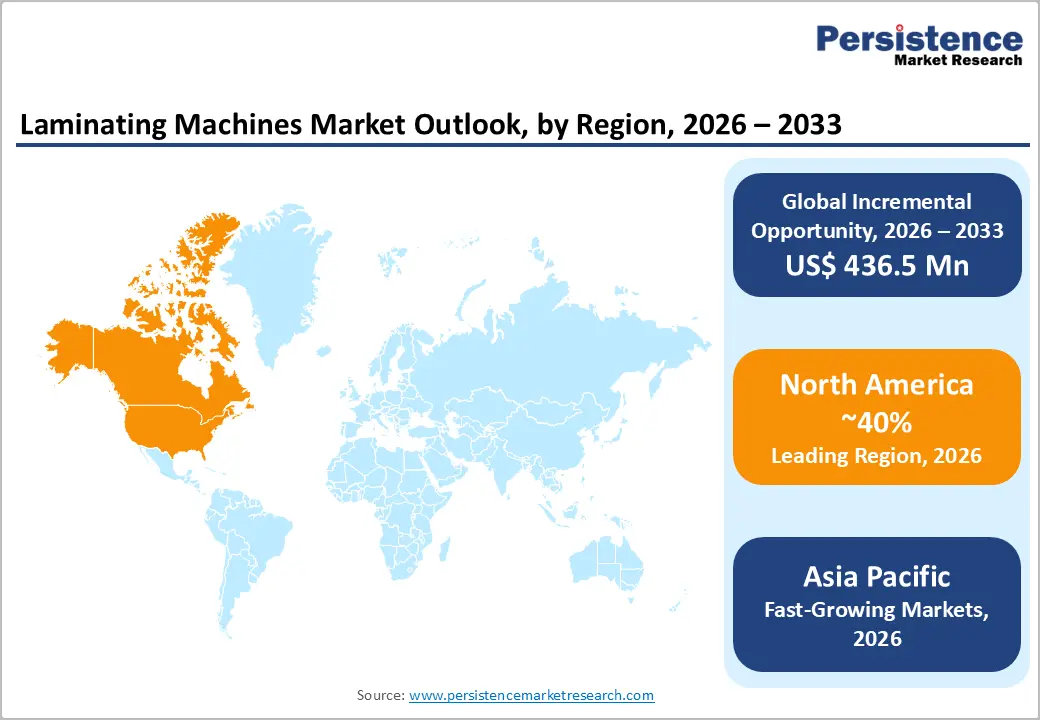

- Leading Region: North America dominates the Laminating Machines market with an estimated 41.9% share in 2026, underpinned by its advanced packaging industry, strong regulatory framework, and established players such as GBC, Fellowes Brands, and D&K Group.

- Fastest Growing Region: Asia Pacific is the fastest growing region, propelled by rapid industrialization, expanding flexible packaging output in China, India, and ASEAN nations, and rising consumer demand for packaged food and pharmaceutical products.

- Dominant Segment: Wet Laminating Machines lead the component category with approximately 74% market share in 2026, favoured for their high production efficiency, low operating costs, and versatility across food, pharmaceutical, and flexible packaging substrates.

- Fastest-Growing Segment: The Pharmaceutical end-use segment is among the fastest-growing

- verticals, driven by rising global drug output, stringent packaging compliance requirements, and growing demand for foil and multi-layer laminated barrier structures for sterile drug packaging.

- Key Market Opportunity: The transition toward sustainable, solventless, and eco-friendly laminating technologies, accelerated by EU packaging regulations and corporate ESG mandates, presents a significant revenue opportunity for manufacturers offering water-based and low-VOC laminating systems compatible with recyclable substrates.

| Key Insights | Details |

|---|---|

| Laminating Machines Market Size (2026E) | US$ 746.4 Mn |

| Market Value Forecast (2033F) | US$ 1,183.0 Mn |

| Projected Growth CAGR (2026 - 2033) | 6.8% |

| Historical Market Growth (2020 - 2025) | 5.4% CAGR |

DRO Analysis

Market Growth Drivers

Rising Demand for Flexible and Protective Packaging Across End-Use Industries

The sustained expansion of the global flexible packaging sector is among the most powerful catalysts for the adoption of laminating machines. According to industry data, the global flexible packaging market was valued at approximately US$ 293 Bn in 2025 and is projected to grow at a CAGR of 5.3% through 2033. Industries such as food and beverages, pharmaceuticals, and personal care depend on multi-layer laminated structures to extend product shelf life, maintain hygiene standards, and comply with stringent regulatory requirements.

Laminating machines are essential for producing high-barrier, multi-substrate packaging films that combine paper, plastic, and foil layers. The growing consumer shift toward packaged and convenience foods, particularly in emerging economies, has intensified demand for advanced, high-speed laminating equipment capable of meeting both volume and quality requirements, directly propelling market growth.

Technological Advancements and Automation Integration in Laminating Equipment

The integration of automation, robotics, artificial intelligence (AI), and the Internet of Things (IoT) into laminating machines is significantly transforming operational efficiency. Modern automated laminating systems reduce manual intervention, minimize material wastage, and deliver consistent lamination quality at high speeds, some systems achieving production rates exceeding 12,000 sheets per hour.

For instance, in November 2023, DGM introduced the SMARTFLUTE X 1450, a fully automated, high-speed laminating machine reaching speeds up to 160 meters per minute. Similarly, in March 2026, Konica Minolta introduced the world's first inline finisher capable of laminating immediately after printing a breakthrough for commercial print operations. These advancements reduce the total cost of ownership and drive wider adoption across commercial and industrial end-users, supporting long-term market momentum.

Market Restraints

High Initial Capital Investment and Maintenance Costs

One of the key constraints limiting broader market penetration is the significant upfront capital expenditure required for advanced, industrial-grade laminating machines. High-speed, automated systems with IoT and AI capabilities can cost substantially more than conventional semi-automatic models, posing a barrier for small and medium-sized enterprises (SMEs) and printing firms in price-sensitive markets.

Additionally, ongoing maintenance, spare parts procurement, and skilled technician requirements add to total ownership costs. This financial barrier can slow adoption, particularly in developing economies where manufacturers are cost-constrained, thereby limiting the addressable market for premium laminating equipment manufacturers and moderating overall market growth rates.

Competition from Alternative Finishing Technologies

The laminating machines market faces intensifying competition from alternative material-finishing and protective-coating technologies, including digital UV coating systems, adhesive bonding techniques, and direct-to-substrate printing solutions that can replicate some of the functional and aesthetic properties of lamination.

Digital printing machines that produce durable, high-resolution finishes without a separate laminating step are increasingly prevalent in commercial print and packaging environments. According to industry observers, the photography industry a traditional lamination user grew at approximately 2.2% in the U.K. and 2.5% in the U.S., partly shifting toward digital solutions. These substitution trends exert downward pricing pressure and constrain the total addressable market for laminating machinery.

Market Opportunities

Expanding Demand from Pharmaceutical and Healthcare Packaging

The pharmaceutical industry represents a high-growth opportunity for laminating machine manufacturers, driven by heightened regulatory scrutiny, rising drug output, and increasing adoption of sterile, multi-layer barrier packaging. According to the European Federation of Pharmaceutical Industries and Associations (EFPIA), the Indian pharmaceutical market alone grew by 11.8% between 2016 and 2021.

As pharmaceutical manufacturers globally scale up production of generic drugs, biologics, and over-the-counter products, the demand for precision laminating machines capable of handling foil, plastic film, and specialty substrates under stringent hygiene conditions is rising sharply. In July 2024, Trinseo unveiled LIGOS A 9200, an acrylic waterborne adhesive designed for dry lamination of flexible packaging materials in direct food contact applications, reflecting the growing need for food-safe and pharma-grade laminating solutions that open significant revenue opportunities for equipment suppliers.

Growth of Sustainable and Eco-Friendly Lamination Technologies

Growing environmental regulations worldwide, combined with brand commitments to sustainability, are creating substantial opportunities for manufacturers of eco-friendly laminating solutions. Governments across the European Union (EU), the United States, and major Asia-Pacific economies are introducing mandates to restrict single-use plastics and promote recyclable, compostable, and bio-based packaging materials.

This regulatory tailwind is accelerating demand for laminating machines compatible with water-based adhesives, solventless processes, and recycled-content films. In January 2024, Neschen Coating launched the ColdLam 1650 SW, a wide-format laminator designed around sustainable media. Similarly, in June 2023, Bobst Group SA launched the NOVA MW LAMINATOR, a solventless laminator that reduces volatile organic compound (VOC) emissions. As brands and converters align with circular economy principles, the sustainable laminating machines segment is poised for above-average growth over the forecast horizon.

Category-wise Analysis

Component Insights

Within the component category, the Wet laminating machines segment holds the dominant position, accounting for an estimated market share of approximately 74% in 2026. Wet laminating machines are preferred by end-users primarily because they offer high production output at relatively low operational costs, making them a cost-effective choice for large-scale, continuous industrial operations.

These machines are equipped with pneumatic laminating pressure rollers synchronized with motor speed and tension controls, which deliver superior, consistent lamination quality across a range of substrates, including food-grade packaging films, pharmaceutical foil laminates, and industrial-grade plastic films. Their versatility in handling high volumes at sustained speeds without the energy-intensive heating required in thermal machines has made them the workhorse of industrial flexible packaging lamination, reinforcing their leading market position.

Material Insights

The Paper segment leads the material category in the laminating machines market, holding an estimated share of approximately 44% in 2026. Paper remains the most widely used substrate in lamination applications across commercial printing, packaging, and label manufacturing, valued for its printability, recyclability, and versatility.

The growing shift toward sustainable packaging, driven by EU single-use plastics regulations and global brand sustainability commitments, is further accelerating the adoption of paper-based laminated structures. Paper-based laminates are gaining traction in food packaging, book covers, and promotional materials, where they offer superior moisture resistance when combined with functional barrier coatings.

End-Use Industry Insights

The Food and Beverages segment dominates the end-use industry, with a market share of approximately 35% in 2026. The food and beverage industry's reliance on high-barrier, multi-layer laminated packaging to preserve freshness, ensure hygiene, and extend shelf life is a primary revenue driver for laminating machine manufacturers.

Laminated packaging in this sector must meet strict FDA and EFSA (European Food Safety Authority) regulatory standards, mandating the use of precision laminating equipment. The growing global demand for packaged and convenience food, particularly in urban markets across Asia Pacific and North America, is driving high-volume flexible packaging production, creating sustained demand for advanced laminating machines capable of processing diverse substrates at industrial speeds.

Regional Analysis

North America

North America holds the leading position in the global Laminating Machines market, accounting for an estimated share of 41.9% in 2026. The United States is the primary revenue contributor, supported by its well-established packaging, pharmaceutical, and commercial printing industries. The presence of leading players such as D&K Group and Black Bros. Co. known for innovation and customized industrial laminating solutions further strengthens the regional competitive landscape.

In May 2024, American Packaging Corporation (APC) launched a new Digital Printing Unit at its Center of Excellence in Columbus, Wisconsin, equipped for flexible packaging production including laminating signaling continued U.S. investment in advanced lamination capabilities. Additionally, the North American market is witnessing growing adoption of solventless and water-based laminating systems aligned with EPA emission reduction targets, as sustainability mandates and corporate ESG commitments accelerate the transition toward eco-friendly laminating processes.

Asia Pacific

Asia Pacific represents the fastest-growing region in the global laminating machines market, propelled by rapid industrialization, expanding consumer markets, and significant investments in packaging infrastructure across China, India, Japan, and ASEAN nations. China alone accounts for over 40% of regional laminating machine production, supported by government-backed industrial parks and great domestic demand from food processing and e-commerce packaging sectors.

In India, manufacturers such as Manugraph and APL Machinery are launching low-cost, high-speed laminating solutions tailored to local market needs. South Korea and Japan continue to drive demand for high-precision laminating systems in semiconductor, electronics, and specialty packaging applications. The growing middle-class population, rising disposable incomes, and escalating packaged food consumption across Southeast Asia further reinforce Asia Pacific's position as the most dynamic and high-potential region for laminating machine investment over the 2026 - 2033 forecast period.

Europe

Europe represents a mature yet dynamic market for laminating machines, driven by its highly regulated packaging sector and strong commitment to sustainability. Germany, the United Kingdom, France, and Spain are the key contributors to regional demand, supported by well-established printing, pharmaceutical, and automotive industries. EU directives on single-use plastics, the European Green Deal, and the Packaging and Packaging Waste Regulation (PPWR) are compelling manufacturers to adopt laminating equipment compatible with recyclable mono-material films and paper-based substrates.

In October 2024, Cavitec, the Swiss maker of technical textile technology, selected Vetaphone corona treatment for its hotmelt coating and laminating machines, reflecting Europe's focus on precision engineering and sustainable process innovation.

Competitive Landscape

The global Laminating Machines market is characterized by a fragmented competitive landscape, with many regional and global manufacturers competing across product quality, innovation, pricing, and service capability. No single player commands a dominant share; instead, the top manufacturers collectively hold a moderate share while numerous mid-size and specialized players address niche segments and regional markets. Leading companies are pursuing strategies such as product portfolio diversification, integration of automation and IoT capabilities, geographic expansion, and partnerships with packaging converters.

Key Market Developments

- In March 2026, Konica Minolta introduced the world's first inline finisher that laminates immediately after printing, supporting paper weights from 75-300 gsm across multiple format sizes including A4, A3, SRA4, and SRA3, targeting commercial print and on-demand publishing markets.

- In February 2025, Ashwin Enterprises launched new laminating models including the heavy-duty fully automatic Lami Press for the digital printing industry, the Tofo laminator for the Indian market, the HQ Series Lami digital machines for offset printing, and the Smart Cut 6090 auto-fit flatbed cutter, expanding its industrial laminating portfolio.

Companies Covered in Laminating Machines Market

- GBC (ACCO Brands Corporation)

- Fellowes Brands

- D&K Group Inc.

- Black Bros. Co.

- MSE Technology

- Komfi spol. s r.o.

- Autobond Laminating Machines

- Bagla Group

- Wenzhou Guangming Printing Machinery Co., Ltd.

- Shanghai Dragon Printing Machinery Co., Ltd.

- Hangzhou Taoxing Printing Machinery Co., Ltd.

- Bobst Group SA

- Nordmeccanica Group

- Neschen Coating GmbH

- Monotech Systems Ltd.

- APL Machinery Pvt. Ltd.

- DGM (Digital Graphic Machines)

- Konica Minolta Inc.

Frequently Asked Questions

The global Laminating Machines market is valued at US$ 746.4 Mn in 2026 and is projected to reach US$ 1,183.0 Mn by 2033, growing at a CAGR of 6.8% over the forecast period 2026 - 2033.

The market is primarily driven by the rapid growth of the flexible packaging industry valued at over US$ 293 Bn globally increasing demand for barrier packaging in the food and beverages and pharmaceutical sectors, and widespread adoption of automated, IoT-enabled laminating technologies that enhance production efficiency and consistency.

Wet Laminating Machines represent the dominant component segment, holding approximately 74% market share in 2026. These machines are preferred due to their high-output capability, low operating costs, and superior lamination quality across diverse industrial substrates, making them the equipment of choice in flexible packaging and food-grade lamination applications.

North America is the leading regional market, accounting for an estimated 41.9% share in 2026. The region's dominance is supported by its advanced packaging and pharmaceutical industries, strong regulatory environment (FDA, EPA compliance standards), and the presence of major players including GBC, Fellowes Brands, and D&K Group Inc.

Leading companies in the Laminating Machines market include GBC (ACCO Brands), Fellowes Brands, D&K Group Inc., Black Bros. Co., MSE Technology, Komfi spol. s r.o., Autobond Laminating Machines, Bagla Group, Wenzhou Guangming Printing Machinery Co., Ltd., Shanghai Dragon Printing Machinery Co., Ltd., and Hangzhou Taoxing Printing Machinery Co., Ltd., among others.