- Industrial Goods & Service

- Industrial Operational Intelligence Solutions Market

Industrial Operational Intelligence Solutions Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Operational Intelligence Solutions Market by Component (Software, Services), by Deployment Mode (On-Premises, Cloud-Based), Solution Type (Enterprise Manufacturing Operational Intelligence, Enterprise Operational Intelligence Software, IT Service Intelligence, Enterprise Security Intelligence), Organization Size, End-user, and Regional Analysis, 2026 - 2033

Industrial Operational Intelligence Solutions Market Size and Trend Analysis

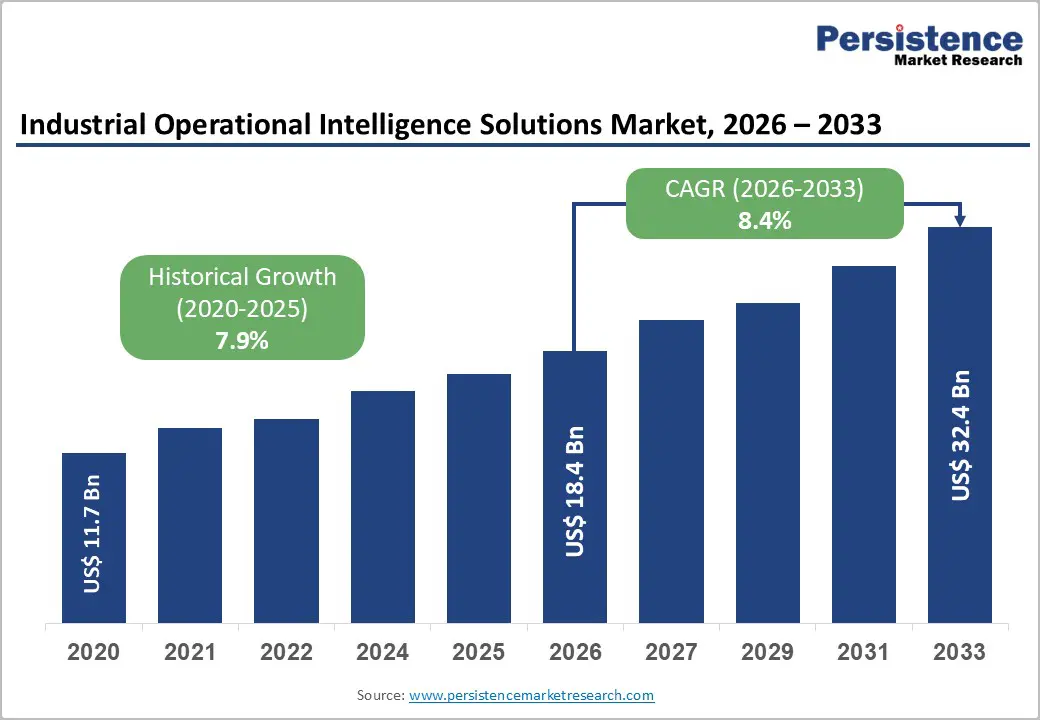

The global industrial operational intelligence solutions market size is likely to be valued at US$ 18.4 billion in 2026 and is expected to reach US$ 32.4 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033.

It is experiencing robust and accelerating growth, driven by the convergence of Industry 4.0 adoption, the proliferation of Industrial Internet of Things (IIoT) sensor infrastructure, and the urgent imperative for real-time data-driven decision-making across asset-intensive industries.

Key Industry Highlights:

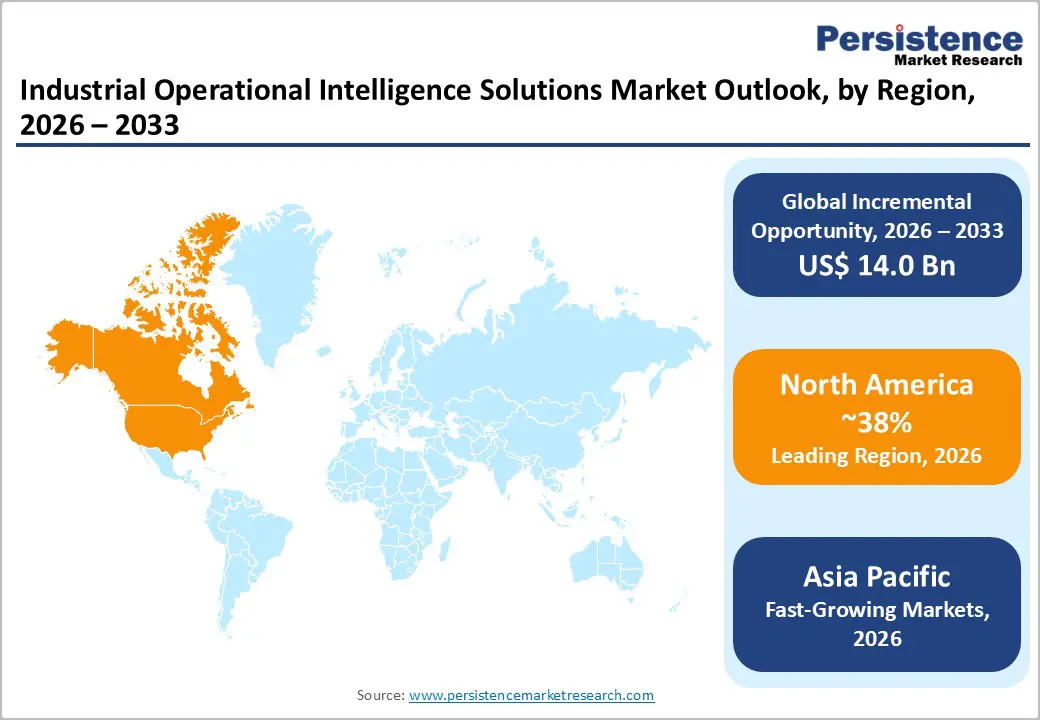

- Leading Region: North America leads the industrial operational intelligence solutions market with 38% share, anchored by the U.S.’s concentration of global OI platform vendors, including Honeywell, Rockwell Automation, GE Vernova, and PTC, combined with a strong enterprise software investment culture and compliance-driven demand from energy and manufacturing sectors.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, with a CAGR of 9.9%, driven by China’s 14th Five-Year Plan industrial internet adoption targets, Japan’s Society 5.0 digitalization, India’s PLI-driven manufacturing expansion, and ASEAN’s accelerating OEM facility investments incorporating operational intelligence standards.

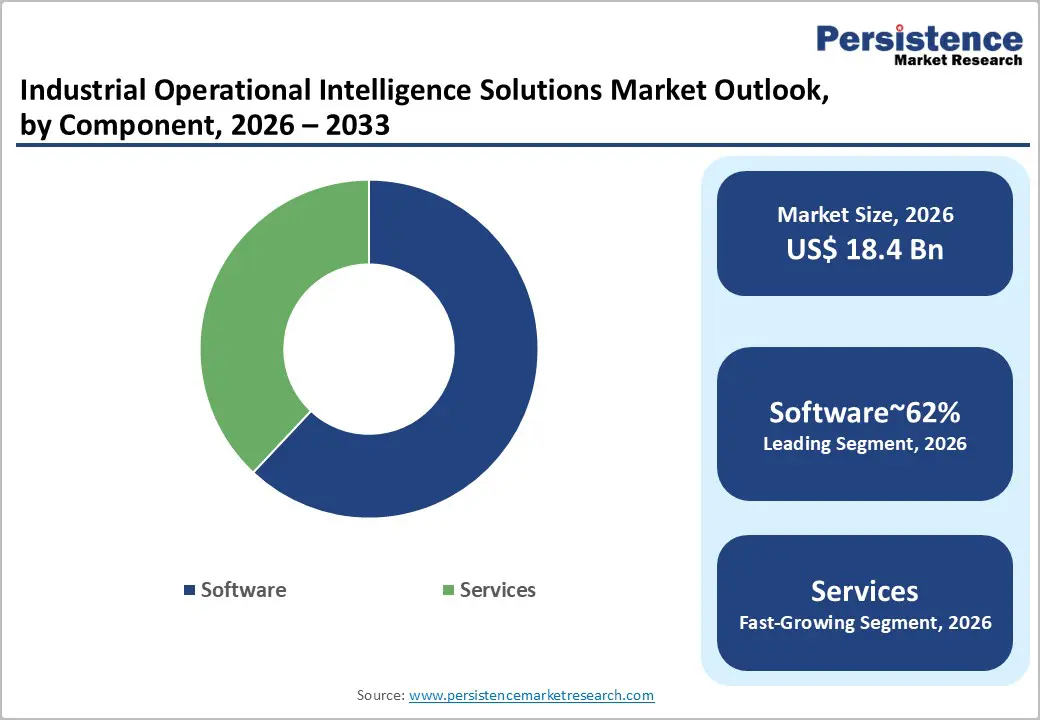

- Dominant Segment: Software leads the By Component category with approximately 62% market share, benefiting from high-margin SaaS subscription models with 75% gross margins, continuous AI feature expansion, and multi-year enterprise license agreements that generate predictable recurring revenue.

- Fastest Growing Segment: Cloud-Based deployment within the By Deployment Mode category is the fastest growing segment, driven by hyperscaler industrial IoT platforms from Azure, AWS, and Google Cloud, lowering adoption barriers, with IDC projecting over 80% of enterprise applications to be cloud-hosted by 2025.

- Key Opportunity: AI-powered predictive maintenance delivering documented 50% downtime reduction and 25% maintenance cost savings, and cloud-based SaaS OI platforms targeting the EU’s 99%+ SME industrial base with subscription pricing democratizing operational intelligence adoption beyond large enterprises.

| Key Insights | Details |

|---|---|

| Industrial Operational Intelligence Solutions Market Size (2026E) | US$ 18.4 Billion |

| Market Value Forecast (2033F) | US$ 32.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.4% |

| Historical Market Growth (2020 - 2025) | 7.9% |

Market Dynamics

Drivers - Industry 4.0 and IIoT Adoption Across Asset-Intensive Industries

The widespread adoption of Industry 4.0 principles and Industrial Internet of Things (IIoT) sensor infrastructure is creating an unprecedented volume of industrial operational data that demands intelligent analytics platforms to extract actionable value. The International Energy Agency (IEA) reports that digitalization investment by utilities and energy companies is growing at over 10% annually.

Industrial operational intelligence platforms integrate data from SCADA systems, PLCs, ERP, MES, and IIoT sensors into unified real-time dashboards and AI-driven analytics engines, enabling proactive asset management, predictive maintenance, production optimization, and energy efficiency improvements that deliver documented ROI within 12-24 months of deployment. This compelling value proposition is accelerating adoption across oil and gas, chemicals, automotive, and energy utilities sectors globally.

Growing Cybersecurity Threats and Operational Resilience Requirements

The convergence of operational technology (OT) and information technology (IT) networks in industrial environments is creating significant cybersecurity vulnerabilities that operational intelligence solutions with integrated security intelligence capabilities are specifically designed to address. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) documented a 300%+ increase in cyberattacks targeting industrial control systems between 2020 and 2023.

High-profile incidents, including the Colonial Pipeline ransomware attack and attacks on water treatment facilities, have catalyzed regulatory responses, including the EU Network and Information Security (NIS2) Directive, that mandate enhanced operational monitoring and incident response capabilities for critical infrastructure operators. Enterprise security intelligence modules within operational intelligence platforms are seeing accelerating procurement across energy, utilities, and critical manufacturing sectors as compliance deadlines approach and cyber risk management becomes a board-level priority.

Restraints - High Implementation Complexity and Integration Challenges

Industrial operational intelligence solutions face significant deployment complexity in brownfield industrial environments where legacy systems, including decades-old SCADA, DCS, and PLC infrastructure, generate data in proprietary, non-standardized formats. System integration across heterogeneous IT/OT landscapes requires substantial professional services investment, typically extending project timelines by 6-18 months and significantly increasing total cost of ownership.

An online survey by McKinsey found that over 70% of industrial digital transformation initiatives fail to scale beyond the pilot stage, primarily due to integration and change management challenges. These implementation barriers constrain adoption velocity, particularly among mid-sized industrial operators without large IT and OT integration budgets.

Data Governance, Privacy, and Sovereignty Compliance Burdens

Industrial organizations operating across multiple jurisdictions face increasingly complex data governance requirements that complicate the deployment of cloud-based operational intelligence. The EU’s General Data Protection Regulation (GDPR), emerging industrial data sovereignty frameworks including the EU Data Act (2024), and sector-specific regulations in energy and healthcare impose requirements on data residency, processing consent, and third-party access that significantly increase compliance costs for cloud-deployed operational intelligence platforms. These regulatory complexities slow procurement decision cycles and favor on-premises deployments in regulated sectors, limiting the cloud-based revenue growth trajectory.

Opportunities - AI-Powered Predictive Maintenance and Asset Performance Management

The integration of advanced artificial intelligence, particularly machine learning-based anomaly detection, digital twin simulation, and generative AI-assisted root cause analysis, into industrial operational intelligence platforms is transforming traditional reactive maintenance into proactive, prediction-driven asset management.

The predictive maintenance enabled by AI and operational intelligence can reduce equipment downtime by up to 50% and maintenance costs by 25%. The oil and gas, energy utilities, and heavy manufacturing sectors, which collectively manage trillions of dollars in capital assets, represent enormous addressable markets for AI-enhanced operational intelligence. Companies, including GE Vernova’s APM solutions, Honeywell’s Forge platform, and ABB Ability, are investing heavily in AI-embedded operational intelligence that can justify premium subscription pricing through documented asset performance improvement outcomes.

SME Digital Transformation via Cloud-Based SaaS Operational Intelligence

Small and medium enterprises (SMEs) in manufacturing and process industries represent a vast, largely underpenetrated addressable market for cloud-based, SaaS-delivered operational intelligence solutions. Traditional on-premises OI platforms required multi-million-dollar investments that excluded SME participation, but cloud-delivered SaaS models with subscription pricing starting from US$ 1,000-10,000 per month are democratizing access.

The European Commission estimates that over 99% of EU enterprises are SMEs, collectively employing two-thirds of all private-sector workers. Government-backed digital transformation programs, including the EU’s Digital Europe Program and India’s Digital India Initiative, are providing co-financing and technical support for SME industrial digitalization. Vendors that develop purpose-built, low-complexity SaaS operational intelligence offerings with pre-configured industry templates can capture significant market share in this high-volume, high-growth customer segment.

Category-wise Analysis

By Component Insights

Software is the dominant component segment, commanding approximately 62% of total market share. Industrial operational intelligence software, encompassing data integration platforms, real-time analytics engines, visualization dashboards, AI/ML model libraries, and reporting modules, constitutes the core value-delivery component of the entire solution stack.

The software segment benefits from recurring revenue through subscription and SaaS licensing models, which are increasingly preferred by both vendors and customers over perpetual licensing. Platform vendors including AVEVA Group plc, PTC Inc., and Honeywell’s Forge™ have built substantial recurring software revenue bases through multi-year enterprise license agreements. The software segment’s high gross margins, typically 70-85% for SaaS platforms, attract significant R&D investment, driving continuous feature expansion that reinforces the segment’s market dominance.

By Deployment Mode Insights

Cloud-based deployment is the leading and fastest-growing deployment mode, accounting for approximately 54% of total market share. Cloud deployment offers industrial operators compelling advantages, including lower upfront capital investment, faster implementation timelines, automatic software updates, and elastic scalability to accommodate growing data volumes and user bases.

Major hyperscale cloud providers, including Microsoft Azure, Amazon Web Services (AWS), and Google Cloud, have developed dedicated industrial IoT and operational intelligence cloud stacks, including Azure Industrial IoT, AWS IoT SiteWise, and Google Cloud’s Manufacturing Data Engine, that lower the barrier to cloud OI adoption. The International Data Corporation (IDC) projects that over 80% of enterprise applications will be cloud-hosted by 2025, and industrial operational intelligence is tracking this broader enterprise software trends.

By Solution Type Insights

Enterprise Manufacturing Operational Intelligence is the leading solution type segment, accounting for approximately 38% of the market. Manufacturing OI solutions, encompassing production monitoring, OEE (Overall Equipment Effectiveness) tracking, quality management, and supply chain visibility, address the most fundamental and universal requirement of industrial operators: understanding and optimizing the efficiency of their production processes.

The Manufacturing Enterprise Solutions Association (MESA International) consistently identifies real-time production visibility as the highest-priority digital capability sought by manufacturing executives globally. The direct and measurable link between manufacturing OI deployment and production cost reduction, typically yielding 5-15% OEE improvement within 12 months of implementation per industry case studies, provides the ROI justification that drives capital allocation decisions.

By Organization Size Insights

Large Enterprises are the dominant organization size segment, representing approximately 67% of the total market share. Large industrial enterprises, including multinational oil companies, global automakers, major utilities, and Fortune 500 manufacturers, possess the IT/OT infrastructure, data volumes, and capital budgets to support the deployment of full-scale operational intelligence platforms. Companies such as Shell, ExxonMobil, Siemens, and Toyota have made multi-year, enterprise-wide investments in operational intelligence as foundational components of their digital transformation strategies.

Large enterprises also typically operate complex, multi-site production environments where the operational optimization value of enterprise-scale OI platforms is most pronounced, with network effects across sites amplifying per-site ROI. The segment generates the highest average contract values, supporting premium revenue concentration even though it does not represent the majority of potential customer accounts.

By End-user Insights

Oil & Gas is the leading end-user segment, accounting for approximately 22% of total market share. The oil and gas sector’s combination of extremely high asset values, hazardous operating conditions, stringent regulatory reporting requirements, and intense cost optimization pressures makes operational intelligence solutions not just commercially attractive but operationally essential.

Offshore platforms, refineries, and pipelines operate critical, capital-intensive assets where unplanned downtime can cost over US$ 1 million per day, according to Deloitte estimates, making the ROI case for predictive OI platforms immediately compelling. Major oil and gas operators, including Saudi Aramco, BP, Chevron, and TotalEnergies, are investing heavily in integrated operational intelligence to improve reservoir management, optimize production rates, reduce flaring, and comply with emissions reporting mandates.

Regional Insights

North America Industrial Operational Intelligence Solutions Market Trends

North America is the dominant market for industrial operational intelligence solutions, led by the United States’ advanced technology ecosystem, large industrial base, and strong enterprise software investment culture. The U.S. hosts the headquarters of multiple global OI platform leaders, including Honeywell International Inc., Rockwell Automation, Inc., GE Vernova, and PTC Inc. The U.S. Department of Energy’s (DOE) Industrial Efficiency and Decarbonization Office is channeling significant federal funding toward industrial digitalization, and the CHIPS and Science Act is driving semiconductor manufacturing facility investments that require sophisticated operational intelligence infrastructure.

U.S. regulatory frameworks, including the EPA’s greenhouse gas reporting requirements, NERC CIP standards for electric utility cybersecurity, and OSHA Process Safety Management (PSM) regulations, are creating compliance-driven demand for operational intelligence monitoring and reporting capabilities. Canada’s oil sands and mining sectors are significant adopters of asset performance management and operational intelligence solutions. The region’s innovation ecosystem, combining world-class university research programs, venture capital investment in industrial software, and a culture of technology-driven operational improvement, sustains continuous investment in product development.

Europe Industrial Operational Intelligence Solutions Market Trends

Europe is the second-largest regional market for industrial operational intelligence solutions, driven by the region’s advanced manufacturing sector, robust regulatory environment, and strong Industry 4.0 policy framework. Germany is the dominant national market, home to globally recognized industrial automation and OI vendors, including Siemens AG, SAP SE, and KUKA, alongside world-class automotive (Volkswagen, BMW, Mercedes-Benz) and chemical (BASF, Bayer) end users. Germany’s Platform Industrie 4.0 initiative has been a global benchmark for industrial digitalization policy, coordinating government, industry, and research investment.

The EU’s NIS2 Directive, which entered into force in January 2023 with member state implementation deadlines in October 2024, is compelling critical infrastructure operators across energy, transportation, and manufacturing to invest in operational monitoring and security intelligence capabilities.

The UK’s Advanced Manufacturing Plan and France’s France 2030 industrial sovereignty strategy are providing co-financing for industrial digital transformation. Spain’s growing renewable energy and automotive EV manufacturing sectors are emerging as fast-growing OI adoption markets. The EU’s Carbon Border Adjustment Mechanism (CBAM) is driving investment in industrial emissions monitoring that directly overlaps with operational intelligence platform capabilities.

Asia Pacific Industrial Operational Intelligence Solutions Market Trends

Asia Pacific is the fastest-growing regional market for industrial operational intelligence solutions, driven by China’s massive manufacturing modernization programs, Japan’s Society 5.0 initiative, India’s industrial digitalization push, and ASEAN’s expanding manufacturing base. China is the dominant market, with the government’s ‘14th Five-Year Plan for Digital Economy Development’ explicitly targeting industrial internet platform adoption across key manufacturing sectors. Chinese domestic OI platform vendors, including Huawei’s FusionPlant™ and Alibaba Cloud’s Industrial Brain, are competing with global players for the enormous domestic market.

Japan’s advanced manufacturing sector, particularly automotive and electronics OEMs, is investing in digital operational intelligence as a core component of competitive differentiation and the evolution of lean manufacturing. India’s National Manufacturing Competitiveness Program and PLI (Production Linked Incentive) scheme are driving manufacturing capacity expansion that increasingly incorporates operational intelligence as a standard facility investment. ASEAN nations, particularly Singapore (a regional technology hub), Thailand, and Vietnam, are attracting manufacturing facility investments from global OEMs that bring with them OI platform deployment requirements, rapidly expanding the regional market.

Competitive Landscape

The global industrial operational intelligence solutions market is moderately consolidated, dominated by a mix of large industrial technology conglomerates, enterprise software specialists, and specialized industrial analytics platform providers. Companies such as ABB Ltd., Honeywell, GE Vernova, Schneider Electric, and Rockwell Automation hold strong positions through deep OT domain expertise, large installed bases, and integrated hardware-software-services portfolios.

Enterprise software leaders, including SAP SE, IBM, and Oracle, compete through data integration capabilities and broad enterprise ecosystem connectivity. Key differentiators include AI/ML analytics depth, real-time edge-to-cloud data processing, domain-specific pre-built content libraries, and certified integration with major SCADA, DCS, and ERP systems. Emerging trends include AI-first platform architectures, digital twin integration, and outcome-based subscription pricing models tied to documented operational improvements.

Key Developments:

- February 2025: Honeywell International Inc. launched Honeywell Forge 5.0, an AI-enhanced industrial operational intelligence platform featuring generative AI-assisted root cause analysis and automated prescriptive maintenance recommendations for energy and industrial manufacturing customers.

- October 2024: AVEVA Group plc released AVEVA Operations Control 2024, integrating real-time AI anomaly detection, cloud-native architecture, and enhanced OT/IT security monitoring for oil and gas and energy utility customers globally.

- May 2024: Rockwell Automation, Inc. announced expanded integration between its FactoryTalk Optix operational intelligence platform and Microsoft Azure OpenAI Service, enabling natural language querying of production data and AI-assisted process optimization recommendations for manufacturing operators.

Companies Covered in Industrial Operational Intelligence Solutions Market

- ABB Ltd.

- Honeywell International Inc.

- General Electric Company

- Rockwell Automation, Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Yokogawa Electric Corporation

- IBM Corporation

- SAP SE

- Oracle Corporation

- Dassault Systèmes SE

- AVEVA Group plc

- PTC Inc.

- TIBCO Software Inc.

- Siemens AG

- AspenTech

- OSIsoft

Frequently Asked Questions

The global Industrial Operational Intelligence Solutions Market is projected to reach US$ 32.4 Billion by 2033, growing from US$ 18.4 Billion in 2026 at a CAGR of 8.4% during the 2026-2033 forecast period. This accelerates from a historical CAGR of 7.9% between 2020 and 2025, driven by IIoT adoption, AI integration, and escalating cybersecurity compliance requirements across industrial sectors.

The primary drivers are the Industry 4.0 and IIoT adoption wave, and growth in OT/IT cybersecurity threats prompting a 300%+ increase in industrial control system attacks since 2020, driving NIS2 Directive-mandated operational monitoring investment across European critical infrastructure operators.

Software leads the By Component category with approximately 62% of total market share. Its dominance is driven by high-margin SaaS subscription models at 75% gross margins, continuous AI/ML feature expansion, and the growing adoption of recurring enterprise license agreements by platform vendors including Honeywell Forge, AVEVA, and PTC ThingWorx.

North America leads the global market, underpinned by the U.S.’s concentration of world-leading OI platform vendors including Honeywell International, Rockwell Automation, GE Vernova, PTC, and IBM, combined with strong regulatory drivers from EPA greenhouse gas reporting, NERC CIP cybersecurity standards, and OSHA PSM compliance requirements generating sustained software procurement demand.

The highest-value opportunities are AI-powered predictive maintenance delivering documented 50% downtime reduction and 25% cost savings in oil and gas and heavy manufacturing sectors, and cloud-based SaaS OI platforms targeting the EU’s 99%+ SME industrial base through Digital Europe Programme-supported digitalization programs democratizing access to enterprise-grade operational intelligence tools.

The key market participants include ABB Ltd., Honeywell International Inc., GE Vernova, Rockwell Automation Inc., Schneider Electric SE, Emerson Electric Co., Yokogawa Electric Corporation, IBM Corporation, SAP SE, Oracle Corporation, Dassault Systèmes SE, AVEVA Group plc, PTC Inc., TIBCO Software Inc., and Siemens AG, collectively spanning OT automation, enterprise software, and industrial analytics platform leadership positions.