- Industrial Goods & Service

- Industrial Chiller Market

Industrial Chiller Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Chiller Market by Product Type (Absorption Chillers, Reciprocating Chillers, Scroll Chillers, Screw Chillers), End User (Food & Beverage Industries, Restaurants, Pharmaceuticals Industries, Chemical Industries, Cosmetic Industries, Rubber Industries, Plastics Industries), and Regional Analysis for 2026 - 2033

Industrial Chiller Market Size and Trend Analysis

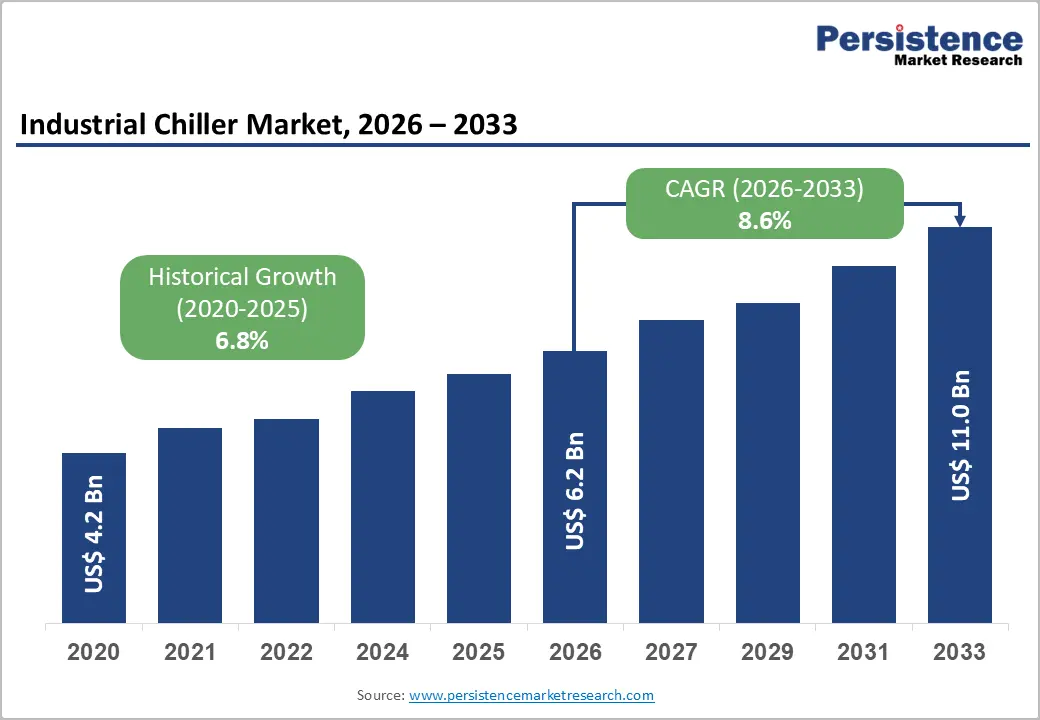

The global industrial chiller market is valued at US$ 6.2 Bn in 2026 and is projected to reach US$ 11.0 Bn by 2033, growing at a CAGR of 8.6% between 2026 and 2033. This robust growth trajectory is primarily driven by rising demand for precise process temperature control across industries such as pharmaceuticals, food & beverage, and specialty chemicals, where operational stability directly influences product quality.

Escalating heat loads from data centres, tightening energy efficiency regulations, and accelerating adoption of low global-warming-potential (GWP) refrigerants are reinforcing industry-wide capital investment in advanced chiller systems. The replacement of aging cooling infrastructure in mature economies, combined with greenfield industrial capacity additions across Asia Pacific and the Middle East, further sustains long-term demand momentum through the forecast period.

Key Market Highlights

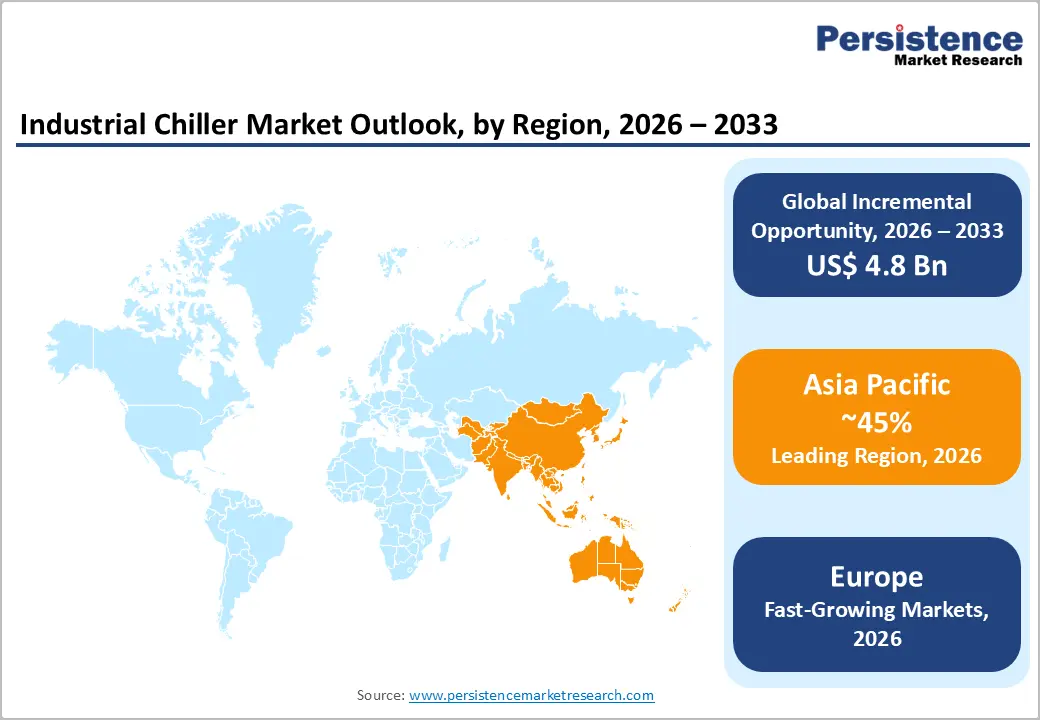

- Leading Region - Asia Pacific dominates the industrial chiller market with approximately 45% revenue share, driven by large-scale manufacturing activity in China, India, and ASEAN economies, supported by rapid industrialization and growing food & beverage and pharmaceutical sector investments.

- Fastest Growing Region - Europe's industrial chiller market is characterized by a mature regulatory environment and an accelerating transition toward low-GWP refrigerant platforms, driven by the EU F-Gas Regulation (EU) 2024/573.

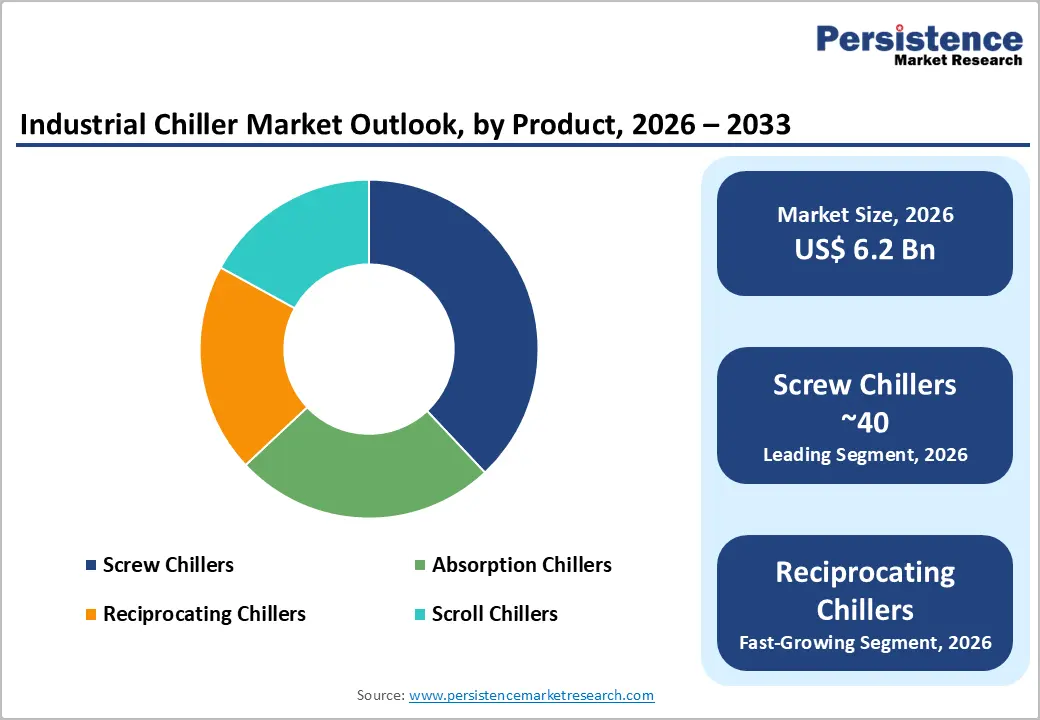

- Dominant Segment - Screw chillers lead the product type category with an estimated 38% market share, valued for their reliability, energy efficiency under variable loads, and broad capacity range making them the preferred choice across chemicals, pharmaceuticals, and large-scale food processing.

- Fastest Growing Segment - The pharmaceutical end-user segment is the fastest growing sub-category, driven by expanding biologics and specialty drug manufacturing globally and stringent cGMP temperature control mandates requiring validated, high-precision chiller installations at production facilities.

- Key Market Opportunity - Surging AI and hyperscale cloud infrastructure investment is creating a high-value opportunity for chiller OEMs. Data center cooling applications are forecast to grow at 12.7% CAGR through 2030 as high-density rack deployments push thermal management requirements beyond conventional air-based systems.

| Key Insights | Details |

|---|---|

| Industrial Chiller Market Size (2026E) | US$ 6.2 Billion |

| Market Value Forecast (2033F) | US$ 11.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.6% |

| Historical Market Growth (2020 - 2025) | 6.8% CAGR |

DRO Analysis

Drivers - Rising Demand for Energy-Efficient Cooling in Industrial Processing

Industrial facilities are under mounting regulatory and commercial pressure to reduce energy consumption without compromising production integrity. According to the U.S. Department of Energy (DOE), industrial cooling systems account for approximately 16% of total electricity consumed in the manufacturing sector, making them priority targets for efficiency retrofits. Governments across the European Union have reinforced this pressure through the F-Gas Regulation and the Energy Efficiency Directive, mandating systematic phase-down of high-GWP refrigerants and minimum seasonal energy performance standards.

Manufacturers are responding with variable-speed compressor chillers, magnetic bearing technology, and IoT-enabled predictive maintenance platforms that lower lifecycle energy costs by up to 40% compared with conventional fixed-speed systems. These technology transitions are compelling operators across pharmaceuticals, specialty chemicals, and food processing to accelerate capital replacement cycles, directly driving new chiller shipments.

Expansion of Pharmaceutical Cold Chain and Food Safety Infrastructure

Stringent product integrity requirements in life sciences and food processing sectors are generating sustained, predictable demand for precision chiller systems. The global pharmaceutical cold chain was valued at approximately US$ 21.3 Bn in 2024, with temperature-sensitive medicines accounting for a rising share of total drug portfolios. Regulatory frameworks such as the U.S. FDA's Current Good Manufacturing Practice (cGMP) guidelines and the EU GMP Annex 15 require validated and continuously monitored thermal environments throughout production.

Similarly, food safety standards under Codex Alimentarius and HACCP protocols mandate uninterrupted cooling across processing lines. As India targets a US$ 300 Bn chemical sector output and the ASEAN bloc accelerates pharmaceutical manufacturing capacity, industrial chiller installations are experiencing accelerated demand across both greenfield plants and capacity expansion projects.

Restraints - High Capital Investment and Long Payback Periods

Industrial chillers particularly screw and centrifugal configurations involve significant upfront capital expenditure. Large-capacity systems can range from US$ 50,000 to over US$ 1 Mn per installation, excluding civil works, cooling towers, and auxiliary piping. For small and mid-sized manufacturers in price-sensitive emerging economies, this capital intensity presents a critical adoption barrier.

Combined with payback periods that often extend beyond 5-7 years, decision-makers in sectors such as cosmetics and rubber processing frequently defer upgrades in favor of legacy equipment maintenance. This dynamic can slow unit replacement cycles and compress near-term market volumes, particularly when access to credit is restricted or industrial output growth moderates.

Volatility in Refrigerant Compliance and Raw Material Costs

The global transition away from hydrofluorocarbons (HFCs) under the Kigali Amendment to the Montreal Protocol is creating near-term supply chain disruptions for chiller manufacturers. Compliance requires redesigning compressor stages, expanding lubricant compatibility, and revalidating safety certifications processes that inflate development timelines and costs. Simultaneously, fluctuating prices for copper, aluminum, and steel key bill-of-materials components create margin pressure for OEMs.

Copper prices rose significantly between 2022 and 2024 due to supply concentration risks in the DRC and Chile. These combined cost headwinds limit manufacturers' ability to offer competitive pricing and may incentivize end users to delay chiller procurement or extend maintenance contracts on existing installations.

Opportunities - Surging Demand from AI-Driven Data Center Infrastructure Expansion

The proliferation of artificial intelligence workloads and hyperscale cloud computing is transforming data center thermal management requirements. The U.S. DOE reported in late 2024 that data center energy loads have tripled over the past decade and are projected to double or triple again by 2028. High-density server racks now routinely exceed 100 kW per rack, pushing facility operators beyond the limits of conventional air cooling toward liquid-ready and direct chilled-water systems.

In January 2025, Amazon Web Services (AWS) announced an investment of approximately US$ 11 Bn in Georgia to expand infrastructure for AI and cloud capabilities. Chiller OEMs that develop ultra-efficient, modular, and waterless cooling architectures such as Johnson Controls' YORK® YVAM magnetic bearing chiller are well-positioned to capture this high-value end-use segment, which is projected to grow at a 12.7% CAGR through 2030.

Industrialization-Led Demand Growth Across Asia Pacific

Asia Pacific represents the most structurally compelling growth opportunity for industrial chiller manufacturers, supported by a convergence of policy initiatives and manufacturing capacity expansion. India's national "Make in India" initiative targets manufacturing's contribution rising to 25% of GDP, anchoring multi-year process cooling demand across chemicals, pharmaceuticals, plastics, and food processing.

China's 14th Five-Year Plan emphasizes advanced manufacturing and green industrial parks, driving adoption of energy-efficient chillers. According to the Asian Development Bank (ADB), infrastructure investment in ASEAN economies is projected to exceed US$ 210 Bn annually through 2030. Manufacturers that localize production, establish regional service networks, and offer financing-linked procurement models will gain outsized share in markets such as Vietnam, Indonesia, Thailand, and India where industrial cooling infrastructure remains significantly underpenetrated.

Category-wise Analysis

Product Type Insights

Among the four key product types in the industrial chiller market, Screw Chillers hold the dominant position, commanding approximately 38% of the overall market share. This leadership is attributable to their exceptional balance of energy efficiency, operational reliability, and scalability across a wide range of cooling capacities typically from 20 tons to over 2,000 tons. Screw compressors are particularly valued in continuous-duty industrial environments, including chemical reactors, pharmaceutical cleanrooms, and plastics processing facilities, where uninterrupted cooling is operationally critical.

Their ability to function efficiently under partial load conditions offering consistent coefficient of performance (COP) even at varying operational demands, makes them a preferred choice over reciprocating alternatives in large-scale installations. Leading manufacturers including Daikin Industries, Trane Technologies, and Carrier Corporation, continue to invest in next-generation screw chillers incorporating low-GWP refrigerants such as R-513A and R-1234ze, reinforcing the segment's competitive positioning through the forecast period.

End-user Insights

The food & beverage Industries segment emerges as the leading end-user category in the industrial chiller market, accounting for an estimated 30% of total demand. The sector's reliance on consistent, validated temperature management across processing, packaging, and cold storage stages creates a structurally recurring and non-discretionary demand base for process chillers. Regulatory mandates under the U.S. Food Safety Modernization Act (FSMA), EU Food Hygiene Regulation (EC) No 852/2004, and equivalent frameworks in Asia Pacific compel food manufacturers to maintain precise thermal environments throughout production.

The global food processing industry has seen sustained capital investment, with beverage producers and protein processors deploying dedicated chiller circuits for ingredient preparation, fermentation, pasteurization, and blast-freezing. Pharmaceuticals Industries represent the second largest and fastest-growing sub-segment, driven by validation requirements under cGMP and expanding biologics manufacturing capacity globally.

Regional Analysis

Asia Pacific Industrial Chiller Market Insights

Asia Pacific is the dominant region in the global industrial chiller market, accounting for approximately 45% of global revenue, driven by China, Japan, India, and the rapidly industrializing ASEAN bloc. China leads regional volumes on the strength of its chemicals, electronics, and automotive manufacturing sectors, alongside robust data center construction linked to national digital infrastructure programs. In January 2025, Midea Group announced the construction of two new manufacturing plants in Rayong, Thailand including a facility producing 600,000 chiller units annually underscoring the region's expanding manufacturing capacity.

India's industrial chiller market is benefiting from the country's targeted US$ 300 Bn chemical sector output initiative and expanding pharmaceutical export capacity, both of which require precision process cooling. Japan's focus on high-efficiency centrifugal and absorption chillers for district cooling systems and industrial clusters reflects the country's energy conservation mandate under the Act on the Rational Use of Energy. Governments in Vietnam, Indonesia, and Thailand are actively pursuing industrial policy transitions toward higher-value manufacturing creating new procurement pipelines for process cooling infrastructure.

Europe Industrial Chiller Market Insights

Europe's industrial chiller market is characterized by a mature regulatory environment and an accelerating transition toward low-GWP refrigerant platforms, driven by the EU F-Gas Regulation (EU) 2024/573. Germany leads regional demand, anchored by its extensive chemical, automotive, and pharmaceutical manufacturing base. The country's Chemie3 sustainability initiative and compliance with DIN EN ISO 50001 energy management standards are prompting widespread adoption of high-efficiency screw and absorption chillers. France, Spain, and the United Kingdom contribute meaningfully through their food & beverage and specialty chemical sectors.

The European Green Deal and the RePowerEU Plan set ambitious industrial decarbonization targets that are effectively mandating chiller technology upgrades across energy-intensive sectors. Trane Technologies' EcoWise portfolio featuring refrigerants with 78% lower GWP than conventional HFCs is gaining traction in European markets.

North America Industrial Chiller Market Insights

North America remains a pivotal market for industrial chillers, supported by strong regulatory infrastructure, advanced manufacturing ecosystems, and significant investment in data centres and pharmaceutical production. The United States accounts for the largest single-country share, driven by the robust presence of food processing conglomerates, life sciences manufacturers, and petrochemical operators.

The U.S. DOE's Energy Star program and the Inflation Reduction Act (IRA) provide meaningful financial incentives for adopting high-efficiency cooling equipment, catalysing commercial and industrial chiller replacements. Canada's expanding pharmaceutical and food processing clusters particularly in Ontario and Quebec contribute incrementally to regional demand. Non-residential construction spending in the U.S. rose approximately 7% year-on-year in 2024, with manufacturing projects surging by 23%, according to the U.S. Census Bureau directly translating into expanded HVAC and process cooling procurement.

Competitive Landscape

The global industrial chiller market reflects a moderately consolidated competitive structure, with the top five players Daikin Industries, Carrier Corporation, Trane Technologies, Johnson Controls, and Mitsubishi Electric, collectively accounting for approximately 26-30% of the market. Beyond these leaders, the landscape is populated by specialized regional players and niche technology providers.

Key competitive differentiators include refrigerant compliance portfolios, energy efficiency ratings, IoT integration capabilities, and strength of after-sales service networks. Strategic development trends emphasize product launches incorporating low-GWP refrigerants, digital cooling management platforms, and modular design architectures.

Key Developments:

- In September 2025, Johnson Controls was named to Fortune's 2025 Change the World list for its YORK® YVAM Air-Cooled Magnetic Bearing Chiller, consuming 40% less power with zero on-site water for AI-intensive data centres.

- In January 2025, Midea announced it is expanding its manufacturing in Thailand, a key production base, by building two new plants in Rayong. A 66.4 million baht plant, expected to open in Q2 of this year, will produce VRF systems and chillers (600,000 units annually, 90% for export).

Companies Covered in Industrial Chiller Market

- Daikin Industries, Ltd.

- Carrier Corporation

- Trane Technologies plc

- Johnson Controls - Hitachi Air Conditioning

- Mitsubishi Electric Corporation

- Smardt Chiller Group Inc.

- KKT Chillers

- MTA S.P.A.

- Friulair S.R.L.

- HYDAC International

- Reynold India Pvt. Ltd.

Frequently Asked Questions

The global Industrial Chiller market is projected to reach US$ 11.0 Bn by 2033, up from US$ 6.2 Bn in 2026, expanding at a CAGR of 8.6% over the forecast period. This growth is supported by escalating demand from pharmaceuticals, food & beverage, chemicals, and data center cooling applications globally.

Key growth drivers include rising demand for energy-efficient process cooling across regulated industries, tightening environmental regulations mandating low-GWP refrigerant adoption, expansion of pharmaceutical and food safety cold chain infrastructure, and surging data center thermal management requirements driven by AI and cloud computing workloads.

Screw Chillers represent the dominant product type, accounting for approximately 38% of market share. Their superiority in energy efficiency, reliability under variable loads, and adaptability to a wide range of industrial cooling capacities spanning pharmaceuticals, chemicals, and food processing underpins their market leadership.

Asia Pacific is the leading region, commanding approximately 45% of global market revenue. This dominance is driven by large-scale manufacturing expansion in China, India, and ASEAN nations, combined with growing investments in industrial infrastructure, food processing, and pharmaceutical production across the region.

Prominent companies operating in the global Industrial Chiller market include Daikin Industries, Ltd., Carrier Corporation, Trane Technologies plc, Johnson Controls - Hitachi Air Conditioning, Mitsubishi Electric Corporation, Smardt Chiller Group Inc., KKT Chillers, MTA S.P.A., Friulair S.R.L., HYDAC International, and Reynold India Pvt. Ltd., among others.