- Industrial Machinery

- Ice Cream Equipment Market

Ice Cream Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Ice Cream Equipment Market by Product Type (Mixing & Pasteurization Tanks, Homogenizers, Continuous & Batch Freezers, Extrusion/Molding Machines, Filling & Packaging Lines, Hardening Tunnels, CIP Systems), Capacity (Low, Medium, High), End-Use (Industrial, Commercial/Retail, Household), and Regional Analysis for 2026 - 2033

Ice Cream Equipment Market Share and Trends Analysis

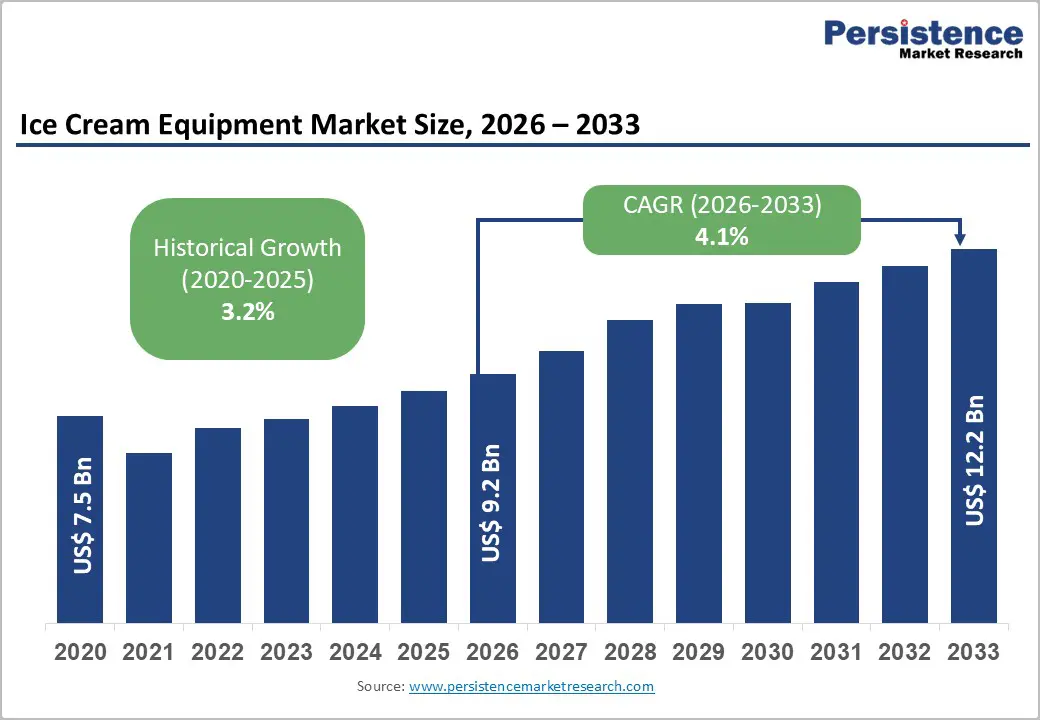

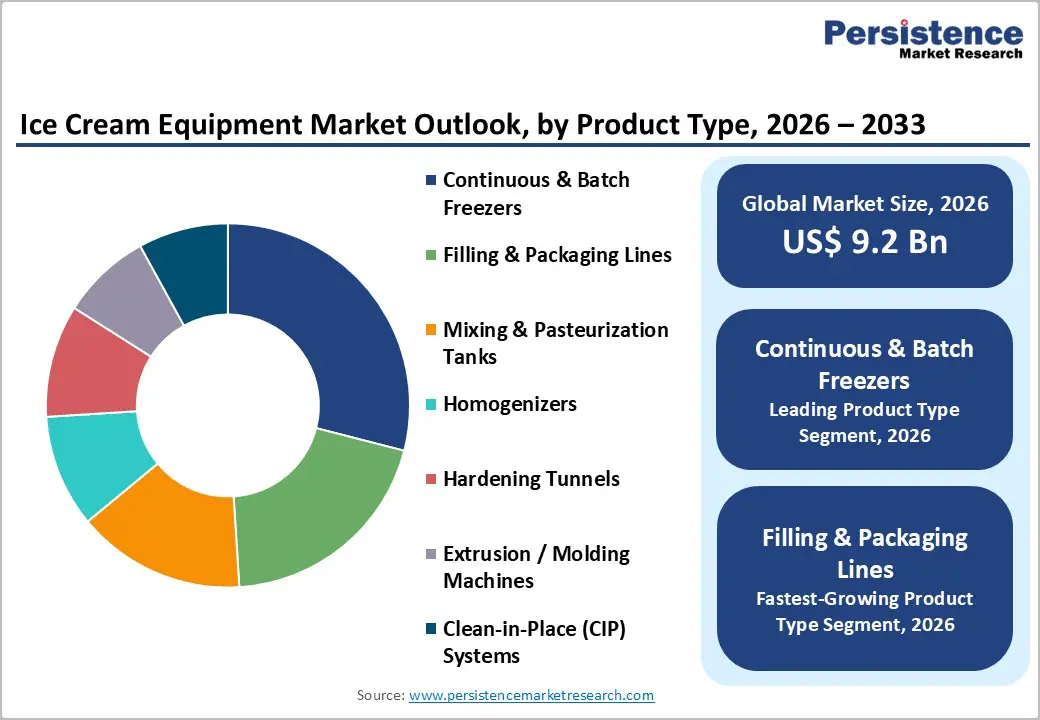

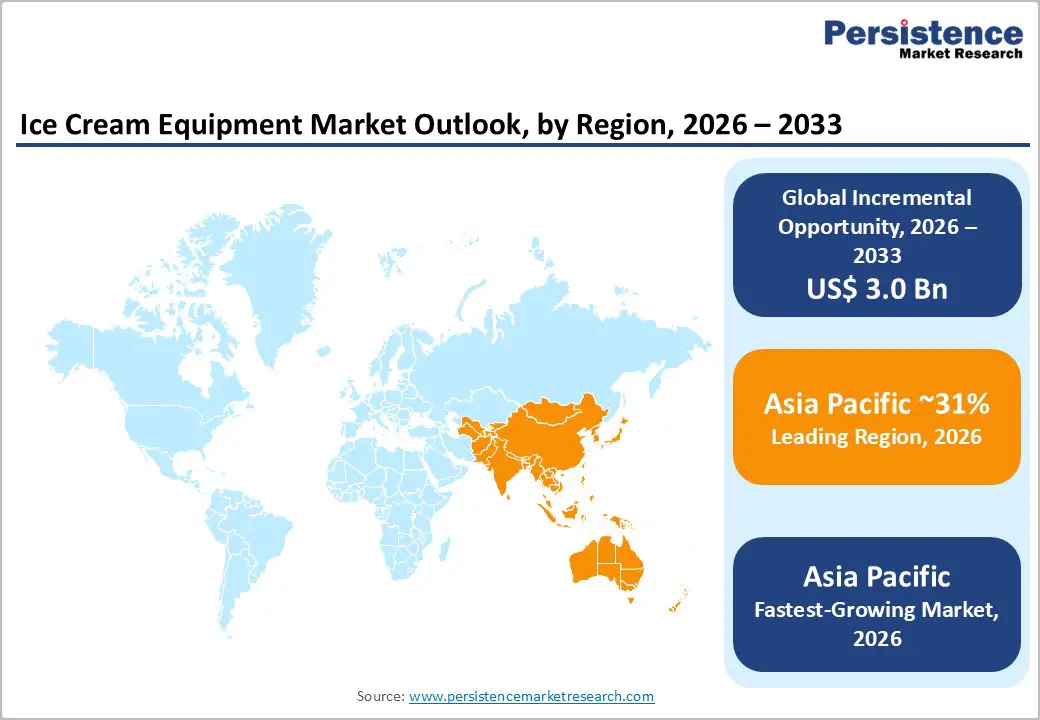

The global ice cream equipment market size is likely to be valued at US$ 9.2 billion in 2026, and is projected to reach US$ 12.2 billion by 2033, growing at a CAGR of 4.1% during the forecast period 2026 - 2033.

The market is entering a relatively stable growth phase, with demand increasingly anchored in capacity replacement, automation upgrades, and energy-efficient retrofits. Sustained growth in frozen dessert consumption, rising penetration of continuous processing systems, and regulatory pressure to modernize refrigeration and sanitation infrastructure across mature and emerging economies are factors fueling market expansion. Industrial manufacturers are continuing to invest in continuous freezers, automated filling lines, and integrated clean-in-place systems to reduce unit operating costs, improve throughput consistency, and comply with tightening food safety and refrigerant regulations.

At the same time, mid-scale processors and organized foodservice chains are accelerating adoption of modular, medium-capacity equipment, reflecting a shift toward decentralized production, private-label manufacturing, and regional co-packing models. These dynamics are supporting a gradual rise in average selling prices (ASPs) and aftermarket service revenues, even as unit shipment growth remains measured. From a macroeconomic standpoint, capital expenditure is remaining sensitive to energy prices, financing costs, and regulatory timelines, particularly in Europe and North America.

Key Industry Highlights

- Dominant Product Type: Continuous and batch freezers are expected to account for approximately 30% of the revenue share in 2026, reflecting their central role in determining throughput efficiency, overrun control, and consistency.

- Fastest-growing Product Type: Filling and packaging lines are projected to expand at the highest CAGR of about 5.2% during 2026 - 2033, driven by private-label expansion and rising demand for automated packaging solutions.

- Dominant End-Use: Industrial manufacturers are anticipated to command nearly 62% of global market demand in 2026, supported by large installed bases and recurring replacement cycles.

- Fastest-growing End-Use: Commercial and retail operators are expected to be the fastest-growing end-users through 2033, underpinned by the expansion of organized ice cream parlors and quick-service restaurant (QSR) chains.

- Regional Leadership: Asia Pacific is projected to hold the largest regional share at around 31% in 2026, owing to rapid capacity additions and formalization of dairy and frozen dessert manufacturing in China, India, and Southeast Asia.

- Fastest-growing Market: Asia Pacific is also set to be the fastest-growing market during 2026 - 2033, supported by rising per-capita consumption and sustained investment in modular, medium-capacity equipment.

| Key Insights | Details |

|---|---|

| Ice Cream Equipment Market Size (2026E) | US$ 9.2 Bn |

| Market Value Forecast (2033F) | US$ 12.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Push for Food Processing and Refrigeration Infrastructure Modernization

Regulatory tightening around food safety, energy efficiency, and refrigerant emissions is increasingly acting as a sustained demand catalyst for ice cream equipment upgrades, particularly across industrial and organized commercial production. Authorities such as the U.S. Food and Drug Administration (FDA) and the European Commission (EC) are continuing to strengthen enforcement of hygienic equipment design, end-to-end traceability, and contamination-control protocols. National food safety regulators across Asia Pacific are also aligning domestic standards with global frameworks. These changes are directly influencing capital procurement decisions, with manufacturers prioritizing pasteurization systems, homogenizers, clean-in-place systems (CIP), and fully enclosed filling and packaging lines that are supporting audit readiness and process standardization. As compliance thresholds are rising, processors are increasingly viewing equipment upgrades as a risk-mitigation investment rather than a discretionary capacity expansion decision.

Climate policy is also influencing refrigeration-related capital expenditure decisions. Revisions to the European Union F-Gas Regulation and global commitments under the Kigali Amendment to the Montreal Protocol are accelerating the phase-down of high global warming potential refrigerants. In response, manufacturers are increasingly replacing legacy freezing and hardening assets with carbon dioxide (CO2)-based or low global warming potential (GWP) refrigeration systems, frequently integrating heat-recovery and energy-monitoring modules. This transition is shortening replacement cycles from historical norms of 18 to 22 years toward an expected 12 to 15 years for critical freezing and hardening equipment. From a market-impact perspective, compliance-driven investment is remaining largely non-discretionary. Even during demand volatility, processors are prioritizing solutions that are lowering regulatory exposure, simplifying inspections, and reducing lifetime energy costs. This trend is steadily benefiting suppliers with certified hygienic designs, advanced engineering capabilities, and lifecycle service models, while supporting a stable demand base for core ice cream processing equipment through 2033.

High Capital Intensity and Energy-linked Operating Cost Exposure

High upfront capital expenditure is continuing to act as a structural constraint for the ice cream equipment market growth, particularly among small and mid-scale processors operating in price-sensitive regions. Advanced systems such as continuous freezers, automated extrusion lines, and integrated filling and packaging solutions are requiring significant initial investment. These costs are increasing further when processors are accounting for essential supporting utilities such as refrigeration plants, steam generation units, and water treatment infrastructure. In many markets, total project expenditure is now exceeding base equipment prices by approximately 35-50% once installation, civil construction, and commissioning activities are included. As a result, investment decisions are increasingly undergoing extended approval cycles, with buyers prioritizing incremental upgrades over full-line replacements.

Energy cost volatility is further constraining purchasing behavior and shaping equipment selection strategies. Ice cream manufacturing is inherently energy intensive, with freezing, hardening, and cold storage accounting for a substantial share of lifetime operating costs. In regions facing unstable electricity tariffs and fluctuating natural gas prices, processors are increasingly delaying capacity expansion or shifting toward refurbished and reconditioned equipment instead of new installations. This trend is particularly evident among independent producers and smaller foodservice operators, where cash flow sensitivity is higher and access to long-term financing is limited. At the same time, supply-chain concentration is introducing additional risk. Critical components such as compressors, control systems, and food-grade stainless steel assemblies are being sourced from a limited pool of suppliers, leading to longer lead times and price escalation. These combined pressures are dampening short-term demand elasticity and reinforcing a cautious, return-focused investment approach.

Modular, Energy-Efficient Mid-Capacity Systems for Processors in Emerging Markets

The most attractive growth opportunity for market players lies in modular, medium-capacity ice cream equipment designed for emerging economies and regional production clusters. Rapid urbanization, steady expansion of organized retail formats, and accelerating growth of private-label frozen desserts are driving demand for standardized and dependable production systems without the capital intensity of large industrial plants. Markets across South Asia, Southeast Asia, parts of the Middle East, and selected African countries are increasingly prioritizing regional manufacturing over centralized imports to improve supply reliability and reduce logistics costs. As a result, processors are actively investing in scalable equipment platforms that are supporting faster market entry, localized product customization, and improved responsiveness to seasonal demand fluctuations.

From a technology and investment perspective, processors in these regions are increasingly seeking plug-and-play solutions that are integrating mixing, pasteurization, freezing, and basic packaging within compact footprints. Equipment demand is shifting toward systems that are balancing automation with operational simplicity, enabling consistent product quality while reducing reliance on highly specialized technical labor. Energy-efficient designs and low GWP refrigeration systems are becoming core procurement requirements, particularly in markets where electricity availability is constrained or power costs are volatile. Suppliers that are combining modular engineering, localized service capabilities, and flexible financing structures are likely to be capturing disproportionate value. Strategically, this segment is offering original equipment manufacturers (OEMs) a clear pathway to volume expansion, installed-base growth, and long-term aftermarket revenue in regions where modern ice cream equipment penetration remains structurally low.

Category-wise Analysis

Product Type Insights

Continuous and batch freezers are likely to lead in 2026, accounting for an estimated 30% of the ice cream equipment market revenue share. Their leadership position is stemming from their direct influence on product texture, overrun control, and throughput consistency across ice cream manufacturing operations. Industrial processors are increasingly prioritizing freezer upgrades to improve energy efficiency, reduce batch-to-batch variability, and accommodate higher inclusion content such as nuts, fruit pieces, and chocolate chips. Replacement-driven demand across North America and Europe is sustaining shipment volumes, as aging installed bases are requiring modernization to meet current energy and hygiene standards. New plant installations across Asia Pacific are adding incremental demand, particularly as regional manufacturers are scaling production to serve organized retail and private-label channels.

Filling and packaging lines are set to register the highest 2026-2033 CAGR at about 5.2%, driven by increasing stock keeping unit (SKU) proliferation, expansion of private-label offerings, and rising demand for portion-controlled, single-serve, and multipack formats. Manufacturers are increasingly viewing packaging automation as a bottleneck-reduction investment rather than a downstream add-on, as it is improving line balancing, reducing labor dependence, and enhancing output predictability. From a supplier perspective, this segment is offering higher ASPs and stronger service attachment potential compared to upstream processing equipment. As a result, OEMs are increasingly prioritizing innovation in filling accuracy, sealing integrity, and changeover flexibility to capture long-term value in this rapidly expanding category.

Capacity Insights

Medium-capacity (1-3 gallons/batch) systems are slated to hold the dominant position in 2026, commanding approximately 42% of the global market value. This segment is benefiting from steady demand across regional manufacturers, contract producers, and organized foodservice chains that require scalable production without excessive capital exposure. Medium-capacity equipment is supporting a wide range of product formats, including tubs, bars, and novelty items, while maintaining manageable investment thresholds and operating complexity. As a result, processors in both developed and emerging markets are increasingly selecting this capacity range as the default option for incremental expansion, pilot-to-commercial scale-up, and decentralized manufacturing strategies.

High-capacity (>3 gallons/batch) systems are projected to be the fastest-growing from 2026 to 2033. The expansion of this segment is being driven by consolidation among large dairy and frozen dessert manufacturers, increasing export-oriented production, and heightened focus on cost-per-unit optimization. Investments are increasingly targeting fully integrated, high-throughput production lines that are maximizing uptime, reducing manual intervention, and improving energy efficiency per unit of output. As competitive pressure intensifies, large producers are prioritizing scale-driven efficiency gains, positioning high-capacity systems as a critical enabler of long-term margin protection and supply reliability.

End-Use Insights

Industrial end users are poised to dominate market demand with an estimated 62% of the revenue share in 2026. This leadership position is reflecting their large-scale production requirements, predictable replacement cycles, and higher adoption of automated processing and packaging systems. Large manufacturers are increasingly investing in equipment standardization across multiple plants to improve performance benchmarking, streamline preventive maintenance, and ensure consistent regulatory compliance. Standardized equipment platforms are also enabling faster operator training and simplified spare-parts management, which is reducing downtime and improving asset utilization across geographically dispersed manufacturing networks.

Commercial and retail end users are anticipated to grow at the highest CAGR through 2033, supported by the rapid growth of organized ice cream parlors, QSR chains, and in-store production formats within supermarkets and convenience retail. The demand trajectory of this segment is being increasingly charted by compact and reliable systems that are offering consistent output, low downtime, and simplified cleaning and sanitation protocols. Operators are prioritizing equipment that is enabling quick changeovers, limited operator intervention, and compliance with local food safety standards. As organized foodservice penetration increases across urban and semi-urban markets, commercial and retail end users are expected to remain a key incremental demand driver for ice cream equipment suppliers through the forecast period.

Regional Insights

North America Ice Cream Equipment Market Trends

North America is expected to account for approximately 29% of the ice cream equipment market share in 2026. This position is being supported by a large and mature installed base, which is driving consistent replacement demand rather than greenfield capacity expansion. Manufacturers across the United States and Canada are increasingly prioritizing automation upgrades to address rising labor costs and persistent workforce availability challenges. At the same time, strict food safety enforcement by the U.S. Food and Drug Administration is reinforcing demand for hygienic processing equipment, enclosed filling systems, and validated cleaning and sanitation solutions.

The North America market is forecast to expand at a steady CAGR through 2033. Investment activity is increasingly concentrating on high-efficiency freezing systems, energy-optimized hardening equipment, and automated packaging lines that are improving throughput consistency while lowering operating costs. Processors are also integrating digital monitoring and predictive maintenance capabilities to extend asset life and reduce unplanned downtime. As regulatory scrutiny and cost pressures persist, equipment purchasing decisions in North America are remaining strongly focused on lifecycle economics, compliance assurance, and operational resilience, positioning replacement-led demand as the primary growth engine over the forecast period.

Europe Ice Cream Equipment Market Trends

Europe is projected to represent approximately 27% of the ice cream equipment market value in 2026, with demand increasingly driven by regulatory-led replacement rather than new capacity creation. Regulatory pressure related to energy efficiency and refrigerant transition under European Union climate policy is continuing to accelerate equipment upgrades across the region. Policy enforcement by institutions such as the European Commission is requiring manufacturers to phase down high global warming potential refrigerants and improve energy performance across freezing, hardening, and cold storage systems. As a result, processors are increasingly prioritizing investments in hygienic, energy-efficient equipment that is aligning with food safety compliance and long-term operating cost reduction objectives.

Ice cream equipment market growth in Europe is forecast to be slower than the one observed in North America between 2026 and 2033. Germany, Italy, and France are continuing to lead regional investment, supported by strong industrial processing bases, advanced engineering ecosystems, and early adoption of low GWP refrigeration technologies. Equipment procurement is increasingly focusing on integrated systems that are combining freezing, heat recovery, and automated cleaning functions to improve asset utilization and regulatory compliance. As energy prices and environmental scrutiny remain elevated, European processors are expected to maintain a disciplined but steady investment approach, with replacement-driven demand and sustainability-linked upgrades shaping market growth over the forecast period.

Asia Pacific Ice Cream Equipment Market Trends

Asia Pacific is set to emerge as the largest and fastest-growing regional market, holding an estimated 31% of global market value in 2026. Growth across the region is being driven by rising per-capita consumption of frozen desserts, rapid expansion of organized retail formats, and increasing localization of ice cream manufacturing capacity. Countries such as China and India, along with key Southeast Asian markets, are continuing to invest in domestic production to reduce reliance on imports and improve supply chain resilience. As a result, demand is steadily shifting toward modern processing equipment that is supporting higher volumes, consistent quality, and regulatory compliance.

In terms of growth rate, the market here is forecast to expand at a CAGR of approximately 5.1% through 2033, outpacing other regions. Investment activity is increasingly concentrating on modular, medium-capacity systems that are balancing scalability with manageable capital requirements. Manufacturers are also prioritizing localized service and spare-parts support to minimize downtime and ensure operational continuity. As competitive intensity increases and consumer expectations rise, equipment adoption in the region is increasingly aligning with automation, energy efficiency, and lifecycle cost optimization, positioning Asia Pacific as the primary engine of global market growth over the forecast period.

Competitive Landscape

The global ice cream equipment market exhibits a moderately consolidated structure, with a limited group of multinational OEMs controlling nearly half of the total industry revenue. Alongside these global players, a broad base of regional and niche manufacturers is actively serving local and application-specific demand. This structure is enabling competition across multiple price and technology tiers, while allowing global suppliers to leverage scale, brand credibility, and long-term customer relationships. As capital investment decisions are becoming more scrutinized, buyers are increasingly favoring suppliers with proven execution capability and stable service support rather than purely cost-driven offerings.

Competitive positioning within the market is increasingly being shaped by engineering depth, automation capability, and aftermarket service coverage instead of upfront equipment pricing alone. Market leaders are differentiating themselves through integrated portfolios that are spanning processing, freezing, and packaging equipment, which is enabling turnkey project delivery and simplified supplier management for large customers. These integrated offerings are supporting faster commissioning, standardized maintenance practices, and improved lifecycle cost visibility. Strong aftermarket service networks are becoming an equally critical competitive lever, as processors are prioritizing uptime, spare parts availability, and performance optimization. As a result, suppliers with comprehensive service models and modular upgrade pathways are strengthening customer retention and reinforcing their competitive advantage over the forecast period.

Key Industry Developments

- In December 2025, Rollney Singapore launched a fully robotic soft-serve ice cream vending machine, automating dispensing to presentation for contactless, hygienic service. The machines deliver fresh servings in under 45 seconds with self-cleaning tech, targeting 100 units island-wide within a year.

- In July 2025, Hudsonville Ice Cream invested US$ 40 million to expand its Michigan headquarters, adding a new novelty bar production line, upgrading mechanical/plumbing/electrical systems, and purchasing new machinery. The project creates at least 44 jobs, supported by a US$ 700,000 Michigan grant and tax exemptions.

- In March 2025, Tetra Pak introduced a new processing product for ice cream manufacturers, enhancing efficiency in mix preparation, freezing, and inclusions dosing. The equipment supports modular ice cream production lines, from extrusion and molding to packaging, with features such as high-speed stick insertion and energy-efficient hardening tunnels.

Companies Covered in Ice Cream Equipment Market

- Tetra Pak

- GEA Group Aktiengesellschaft

- Alfa Laval AB

- SPX FLOW, Inc.

- JBT Corporation

- Bühler Group

- Krones AG

- Carpigiani Group (Ali Group)

- Gram Equipment A/S

- Syntegon Technology GmbH

- Paul Mueller Company

- ROKK Processing Ltd.

- Ice Group S.p.A.

Frequently Asked Questions

The global ice cream equipment market is projected to reach US$ 9.2 billion in 2026.

Escalating consumption of frozen desserts, deepening adoption of continuous processing systems, and regulatory pressure to modernize refrigeration and sanitation infrastructure are driving the market.

The market is poised to witness a CAGR of 4.1% from 2026 to 2033.

Shift toward decentralized production, private-label manufacturing, regional co-packing models, and unlocking of aftermarket service revenues are key market opportunities.

Tetra Pak, GEA Group, Alfa Laval AB, and SPX FLOW are some of the key players in the market.