- Industrial Machinery

- Fabric Spreading Machine Market

Fabric Spreading Machine Market Size, Share, and Growth Forecast 2026 - 2033

Fabric Spreading Machine Market by Machine Type (Manual, Automatic, Semi-automatic), Mechanism (Flatbed, Conveyor Belt, Sectional), Application (Garment Manufacturing, Home Textile, Technical Textiles, Other Applications), and Regional Analysis, 2026 - 2033

Fabric Spreading Machine Market Size and Trend Analysis

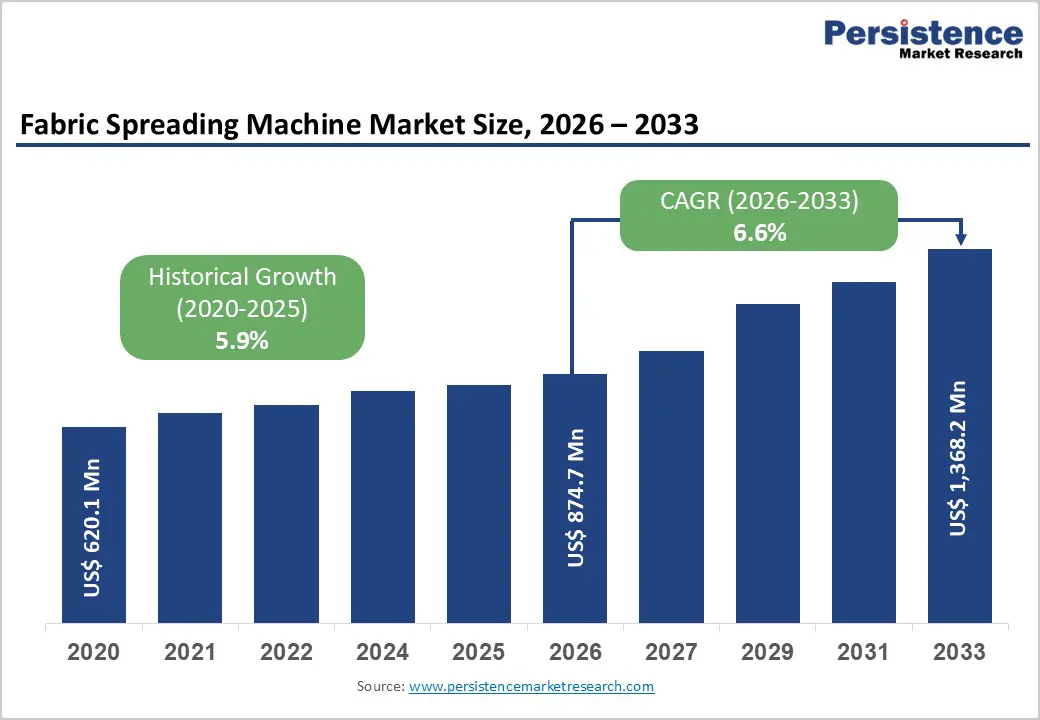

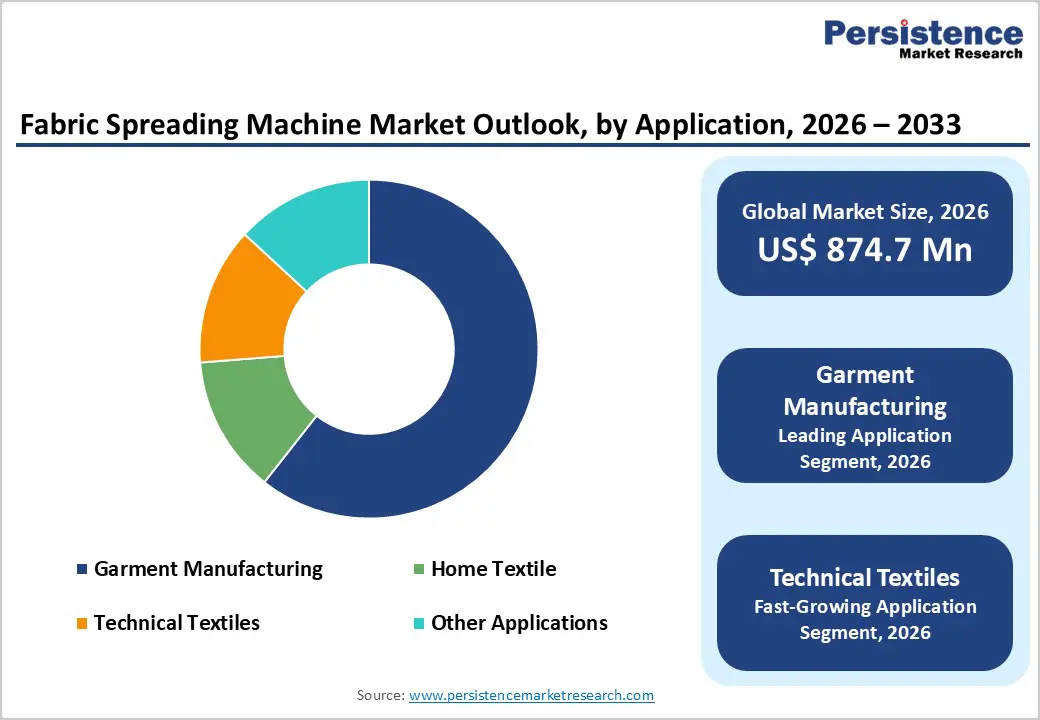

The global fabric spreading machine market size is expected to be valued at US$ 874.7 million in 2026 and projected to reach US$ 1,368.2 million by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

Robust growth in the global apparel and textile manufacturing sector, combined with increasing automation adoption in garment production facilities across Asia Pacific, Europe, and North America, is the primary force propelling the Fabric Spreading Machine market forward. The accelerating shift from manual to automatic spreading systems, driven by labor cost pressures, demand for precision fabric utilization, and rising fast-fashion production volumes, is significantly upgrading the average selling price and feature complexity of installed equipment. Expanding demand for technical textiles across automotive, aerospace, and medical applications is simultaneously broadening the addressable end-use base for spreading machinery manufacturers beyond conventional garment and home textile segments.

Key Industry Highlights

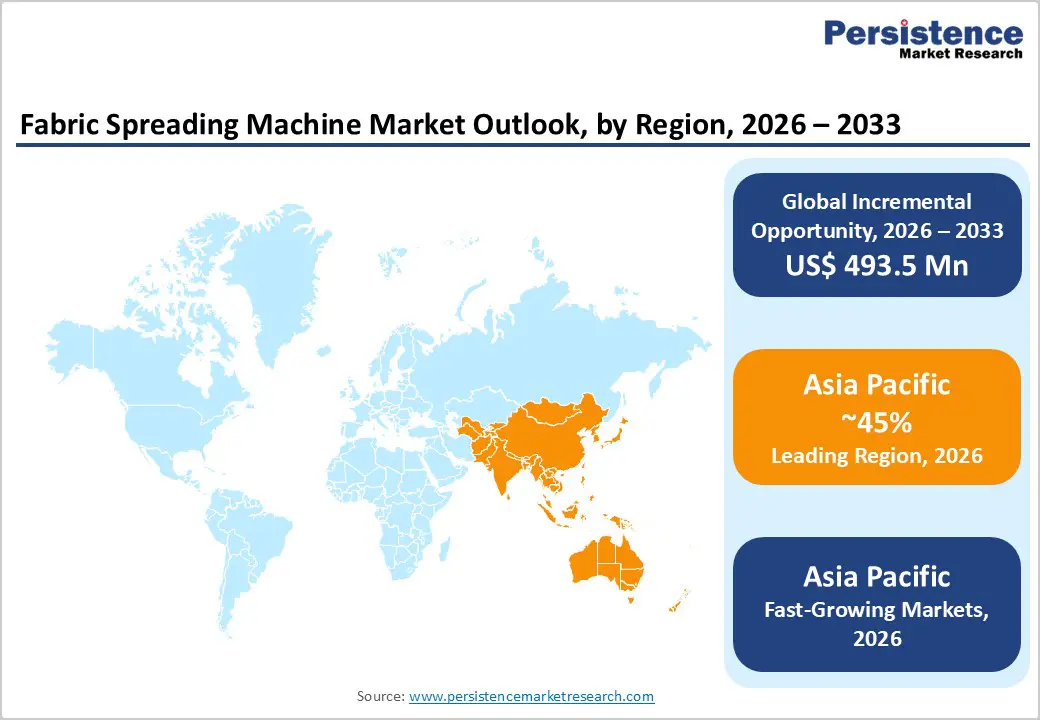

- Leading Region: Asia Pacific leads the global Fabric Spreading Machine market with approximately 45% share in 2025, anchored by China’s massive textile output exceeding US$ 350 billion annually and progressive factory automation across Bangladesh, Vietnam, and India.

- Fastest growing Region: Asia Pacific is also the fastest growing region during 2026 - 2033, driven by Bangladesh’s cutting room modernization programs under BGMEA initiatives, India’s PLI textile scheme investments, and rapid apparel supply chain diversification across Vietnam, Indonesia, and Cambodia.

- Dominant Material Segment: Automatic spreading machines dominate the machine type segment with approximately 48% market share in 2025, driven by labor cost pressures in key producing regions and demand for precision lay accuracy from global fast-fashion and export-oriented garment manufacturers.

- Fastest Growing Segment: Smart spreading systems with Industry 4.0 integration are the fastest growing product innovation trend during 2026 - 2033, as Lectra, Gerber Technology, and Bullmer embed IoT connectivity, AI-assisted fabric optimization, and ERP/MES interfaces into next-generation spreading platforms.

- Key Opportunity: Rising technical textile production for automotive, aerospace, and medical applications, combined with the EU’s Sustainable Textiles Strategy mandating waste reduction, represents the most significant emerging demand opportunity for precision automatic spreading machine manufacturers through 2033.

| Key Insights | Details |

|---|---|

| Fabric Spreading Machine Market Size (2026E) | US$ 874.7 Million |

| Market Value Forecast (2033F) | US$ 1,368.2 Million |

| Projected Growth CAGR (2026 - 2033) | 6.6% |

| Historical Market Growth (2020 - 2025) | 5.9% |

Market Dynamics

Rising Apparel Industry Output and Labor Cost Pressures Driving Automation Adoption

The global apparel and textile manufacturing industry continues to expand in output volume, creating sustained equipment investment demand. According to the World Trade Organization (WTO), global textile and clothing exports exceeded US$ 900 billion in 2022, with production volumes concentrated in China, Bangladesh, Vietnam, India, and Turkey. Rising labor costs in these historically low-cost manufacturing hubs are compelling garment factories to automate labor-intensive processes such as fabric spreading. Automated fabric spreading machines reduce fabric waste by up to 15% through precise tension control, straight-edge alignment, and programmable lay length, directly translating to material cost savings. For mid-to-large garment manufacturers operating at scale, the return on investment for switching from manual to automatic spreading systems is increasingly compelling, providing a structural growth driver for premium equipment segments.

Expanding Fast Fashion and Mass Customization Production Models

The continued dominance of fast-fashion retail business models, characterized by high design turnover, short production runs, and compressed lead times, is placing significant operational pressure on garment manufacturing facilities to increase throughput. According to the International Apparel Federation (IAF), global apparel output volumes have grown consistently, driven by demand expansion in emerging markets and volume-led strategies from fast-fashion groups including Zara (Inditex), H&M, and Shein. Fabric spreading machines equipped with automatic roll-change systems, programmable lay parameters, and integrated fabric detection sensors enable factories to execute multiple short-run lays per shift with minimal operator intervention. The parallel rise of mass customization in online fashion is also driving demand for spreading machines compatible with narrow, multi-style lays, widening the installed base addressable market.

High Capital Investment Requirements Limiting Adoption Among SMEs

A significant restraint on Fabric Spreading Machine market growth is the considerable capital outlay required for full-featured automatic spreading systems, which typically range from tens of thousands to several hundred thousand dollars depending on working width, speed, and automation level. According to data from the Asian Development Bank (ADB), small and medium-sized enterprises (SMEs) constitute over 80% of the textile and garment manufacturing base in key producing economies such as Bangladesh, Cambodia, and Sri Lanka. For these operators, justifying investment in high-end automatic spreading machinery against uncertain order books and thin operating margins remains a persistent challenge, effectively capping addressable demand in the most price-sensitive segments and geographies where manual spreading remains the default.

Lack of Standardized Technical Training and Skilled Operator Availability

The effective operation, programming, and maintenance of advanced automatic and semi-automatic fabric spreading machines demands a technically skilled workforce that is in short supply across many key textile-producing regions. Complex multi-function spreading machines integrate programmable logic controllers (PLCs), servo motors, optical edge-detection systems, and connectivity interfaces requiring trained technicians for both daily operation and periodic maintenance. The International Labour Organization (ILO) has consistently highlighted skills gaps in the textile and apparel manufacturing sector, particularly in South Asia and Sub-Saharan Africa, as a barrier to productive adoption of advanced machinery. When automated equipment breaks down without accessible technical support, factories often revert to manual processes, undermining the productivity rationale for investment and increasing total cost of ownership perceptions among risk-averse buyers.

Growing Demand for Smart Spreading Systems with Industry 4.0 Integration

The integration of fabric spreading machines into Industry 4.0 factory ecosystems, via IoT connectivity, real-time production monitoring dashboards, and data-driven predictive maintenance platforms, represents a high-value commercial opportunity for leading machine builders. Modern automatic spreaders increasingly incorporate OPC-UA communication protocols and ERP/MES integration interfaces that allow production planners to schedule, monitor, and optimize spreading operations remotely. According to the European Commission’s Digital Compass 2030 policy framework, 75% of EU industrial enterprises are targeted for digital technology adoption by 2030, and textile machinery manufacturers are responding with connected machine portfolios. Companies such as Lectra and Gerber Technology are embedding spreading machine data into broader digital cutting room solutions, creating sticky software ecosystems and recurring revenue streams that increase customer lifetime value and competitive switching barriers.

Rising Technical Textile Production Opening New Application Verticals

The rapidly expanding technical textiles sector, encompassing composites for aerospace, geotextiles, medical fabrics, filtration materials, and automotive interior textiles, presents a structurally new demand vertical for fabric spreading machine manufacturers capable of handling high-performance engineered fabrics. According to the European Technical Textiles Association (EDANA) and sector publications, the global technical textiles industry has sustained above-average growth rates, driven by lightweighting trends in automotive and aerospace manufacturing, infrastructure investment in geosynthetics, and expanding medical textile applications. Technical fabrics, including carbon fiber prepregs, aramid woven structures, and nonwoven medical composites, require precision spreading at controlled tension levels. Spreading machine manufacturers that develop application-specific equipment for technical textile customers can differentiate with premium pricing, lower volume competition, and more defensible intellectual property compared to conventional garment-sector machines.

Category-wise Insights

By Machine Type

The automatic segment dominates with an estimated share of approximately 48% in 2025, reflecting the structural shift among mid-to-large garment manufacturers toward mechanized, high-throughput spreading operations. Automatic fabric spreading machines deliver consistent lay quality across all fabric types, including knits, wovens, and technical materials, while reducing dependency on skilled operators and minimizing material waste through precise tension and edge control. Major garment manufacturing clusters in Bangladesh, China, Vietnam, and Turkey have progressively upgraded from manual to automatic spreading as export order complexity and volume have increased. Leading manufacturers including Lectra, Gerber Technology, and Eastman Machine Company have expanded their automatic machine portfolios with features including dual-ply spreading, automatic roll change, and programmable cut order management, further reinforcing this segment’s dominant position in the global installed base.

By Mechanism

The flatbed mechanism segment held the leading market share of approximately 57% in 2025, underpinned by its universal compatibility with virtually all fabric types, its relative mechanical simplicity, and its established position as the industry-standard platform for garment and home textile cutting room operations. Flatbed spreading machines accommodate the broadest range of fabric weights, constructions, and surface characteristics, making them the default choice for multi-product garment manufacturers handling diverse material portfolios. Their straightforward maintenance requirements and wide availability of spare parts, supported by an established global supplier network, reduce total cost of ownership compared to conveyor or sectional alternatives. While conveyor belt spreading systems are gaining traction in high-throughput knitwear and technical textile applications, the flatbed platform’s versatility and proven reliability ensure it retains majority share across the forecast period.

By Application

The garment manufacturing segment accounted for approximately 62% of total share in 2025. Garment manufacturing represents the historical foundation and largest volume end-use for fabric spreading equipment, driven by the global apparel industry’s enormous scale and the universal requirement to spread woven and knit fabrics prior to cutting. The World Trade Organization (WTO) and International Trade Centre (ITC) data consistently place garment and apparel among the top globally traded product categories, with major production hubs in Asia Pacific operating large-scale cutting rooms equipped with multiple spreading lines. The increasing adoption of computer-integrated cutting room workflows, where spreading machines are digitally linked to CAD marker systems from companies like Lectra and Gerber Technology, is further expanding per-facility machine utilization and upgrade cycles within this segment.

Regional Insights

North America Fabric Spreading Machine Market Trends and Insights

North America accounted for approximately 18% of the global Fabric Spreading Machine market in 2025, with the United States serving as the dominant national market driven by its combination of high-value domestic apparel manufacturing, advanced technical textile production, and a robust innovation ecosystem. While the U.S. apparel manufacturing base contracted significantly over the past two decades due to offshoring, a reshoring momentum supported by Made in USA branding, the Berry Amendment for military textile procurement, and domestic supply chain resilience initiatives is sustaining investment in modern cutting room equipment. The American Apparel & Footwear Association (AAFA) has highlighted growing interest in domestic manufacturing reinvestment among U.S. brands seeking supply chain transparency.

The U.S. technical textiles sector, spanning industrial filtration, medical nonwovens, automotive composites, and defense-grade fabrics, is a growing adopter of precision spreading equipment capable of handling engineered materials. Companies including Eastman Machine Company and Gerber Technology, both headquartered in the U.S., maintain strong domestic customer relationships and drive product innovation in automatic and semi-automatic systems. Canada’s relatively smaller but technically sophisticated textile sector contributes regional demand, particularly in workwear and protective clothing manufacturing segments that require consistent spreading quality for compliance-critical garment production.

Europe Fabric Spreading Machine Market Trends and Insights

Europe held approximately 22% of the global Fabric Spreading Machine market share in 2025, supported by a concentration of high-quality apparel brands, technically advanced textile machinery manufacturers, and progressive regulatory frameworks. Germany, home to leading textile machinery exhibitions including ITMA and a sophisticated manufacturing base, is a key market for premium automatic spreading systems. Italy and Spain are significant apparel production centers where investment in cutting room automation remains active, particularly among fashion-forward manufacturers. France contributes demand through its luxury fashion and technical textile sectors, where fabric handling precision is paramount.

The European Union’s Ecodesign for Sustainable Products Regulation (ESPR) and the EU Strategy for Sustainable and Circular Textiles are increasing pressure on manufacturers to minimize fabric waste, a driver that directly benefits automatic spreading machine adoption, as these systems demonstrably reduce fabric consumption through optimized lay planning and tension control. Bullmer and Morgan Tecnica, both with strong European roots, continue to develop advanced spreading platforms with sustainability and connectivity features tailored to European market preferences, reinforcing the region’s position as a premium machine technology development hub through 2033.

Asia Pacific Fabric Spreading Machine Market Trends and Insights

Asia Pacific is the largest and fastest growing region in the Fabric Spreading Machine market, commanding approximately 45% of global market share in 2025 and expected to sustain the highest CAGR through 2033. China remains the world’s largest textile and apparel producer, with the China National Textile and Apparel Council (CNTAC) reporting that the country’s textile industry output value exceeds US$ 350 billion annually. China’s ongoing automation upgrades, driven by rising labor costs, the Made in China 2025 industrial policy, and increasing export quality requirements, are creating sustained demand for advanced automatic and semi-automatic spreading machines. Domestic manufacturer Richpeace is competing aggressively with international brands on price while rapidly improving technology capability.

Bangladesh, the world’s second-largest garment exporter after China, is progressively upgrading its cutting room infrastructure. The Bangladesh Garment Manufacturers and Exporters Association (BGMEA) has actively promoted factory modernization programs, creating favorable conditions for spreading machine investment. India’s expanding garment export ambitions, supported by the government’s Production Linked Incentive (PLI) scheme for textiles, are driving new greenfield factory investments. Vietnam, Indonesia, and Cambodia represent fast-growing secondary markets as global apparel supply chain diversification away from China accelerates post-pandemic, collectively expanding the regional installed base for fabric spreading machinery.

Competitive Landscape

The global fabric spreading machine market is moderately fragmented, with a combination of international machinery manufacturers and regional equipment suppliers competing across various price and performance segments. Large technology providers maintain a competitive advantage through integrated cutting room automation solutions, advanced machine control systems, and strong global service and support networks. Their ability to deliver complete digital cutting room ecosystems strengthens long-term customer relationships with apparel and technical textile manufacturers.

Mid-sized manufacturers primarily compete through precision engineering, customization capabilities, and application-specific machine designs tailored to different fabric types and production scales. At the same time, regional players focus on cost-effective equipment and localized distribution networks to capture demand in emerging textile manufacturing hubs. Key competitive strategies include increasing machine connectivity, integrating automation and data monitoring features, and aligning spreading machines with CAD-based cutting workflows. Companies are also expanding product capabilities to support technical textiles and high-performance fabrics, while strengthening partnerships across the digital cutting room technology ecosystem.

Key Developments

- May, 2024: Yili (Zhaoqing) Intelligent Technology Co., Ltd. introduced a knitted fabric automatic spreading machine designed to automate fabric spreading in textile production, improving efficiency, reducing manual labor, and enabling precise, high-speed spreading for various knitted and woven fabrics.

- January, 2026: Danyang Yixun Machinery Co., Ltd. showcased its advanced warp knitting and fiber-spreading technologies at the ITMA exhibition, highlighting machines designed for technical textiles and composite reinforcement materials used in aerospace, automotive, and renewable energy applications.

Companies Covered in Fabric Spreading Machine Market

- Lectra

- Gerber Technology

- Eastman Machine Company

- Bullmer

- Richpeace

- Morgan Tecnica

- FK Group

- TukaSpreader

- IMA SpA

- Ozbilim

- YIN USA, Inc.

- Cosmotex

- Kuris Spulmaschinen GmbH

- Pathfinder Company

- Oshima Attaching Machine Co., Ltd.

- Comelz S.p.A..

- Danyang Yixun Machinery Co., Ltd.

- Yili (Zhaoqing) Intelligent Technology Co., Ltd.

Frequently Asked Questions

The global Fabric Spreading Machine market is estimated to reach US$ 874.7 million in 2026, driven by increasing automation in garment manufacturing and growing demand from technical textile production.

Demand is driven by rising labor costs, the need for faster and more precise fabric handling in apparel production, and increasing adoption of automated cutting room technologies.

Asia Pacific leads the market due to its large textile manufacturing base and growing investments in automation across major garment-producing countries.

Key opportunities include integration of Industry 4.0 technologies, AI-enabled production optimization, and expanding applications in the technical textiles sector.

Key companies include Lectra, Gerber Technology, Eastman Machine Company, Bullmer, Richpeace, Morgan Tecnica, and FK Group.