- Automation & Robotics

- Hydrogen Peroxide Market

Hydrogen Peroxide Market Size, Share, and Growth Forecast 2026 - 2033

Hydrogen Peroxide Market by Grade (Industrial Grade, Electronics Grade, Food Grade, Pharmaceutical Grade), Concentration (Up to 35%, 35%–50%, 50%–70%, Above 70%), Application (Bleaching, Chemical Synthesis, Oxidizing Agent, Disinfectant & Sterilization, Others), End-use Industry (Pulp & Paper, Chemical Manufacturing, Water & Wastewater Treatment, Healthcare & Pharmaceuticals, Food Processing, Electronics & Semiconductor, Textiles, Mining, Others), by Regional Analysis, 2026 - 2033

Hydrogen Peroxide Market Size and Trend Analysis

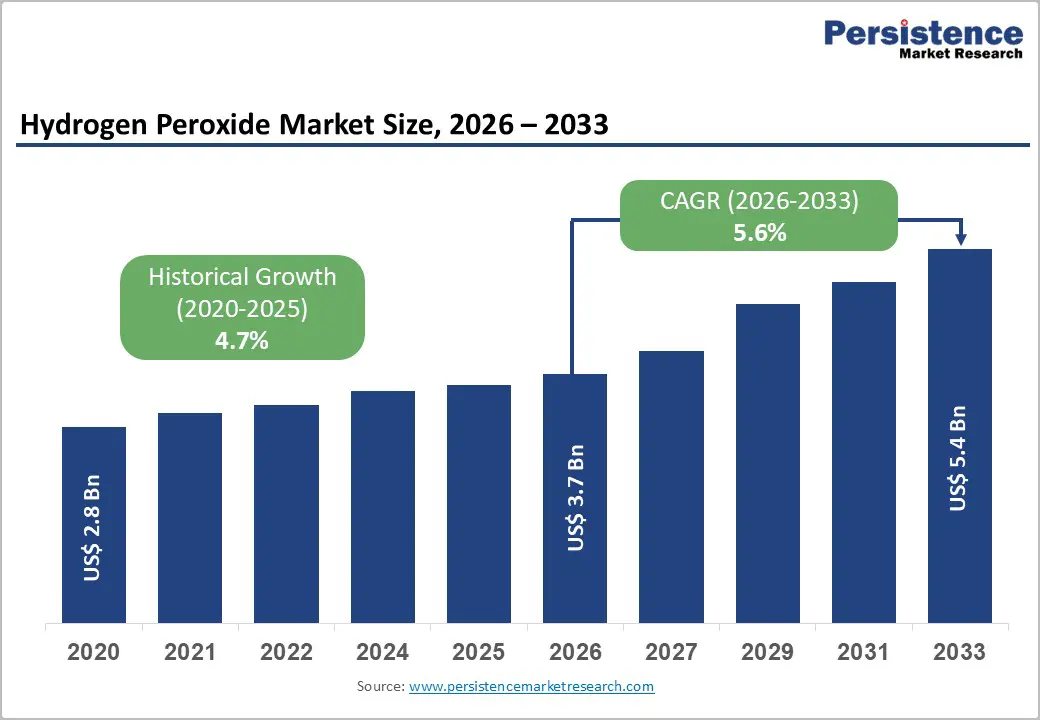

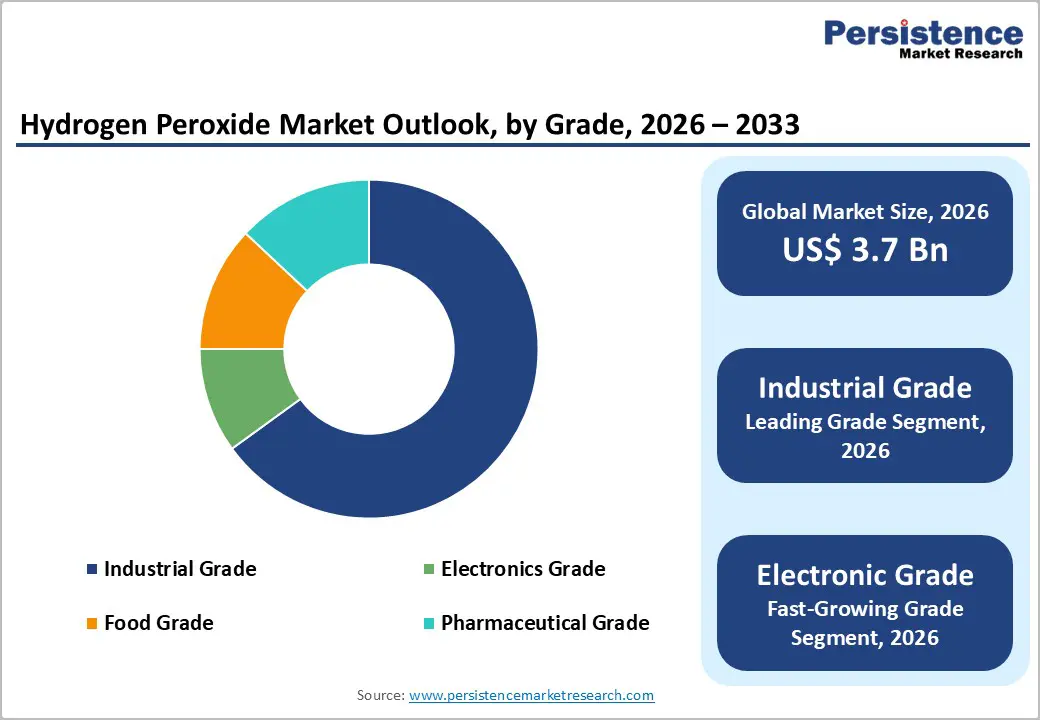

The global Hydrogen Peroxide market size is expected to be valued at US$ 3.7 billion in 2026 and projected to reach US$ 5.4 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

Sustained demand across pulp & paper bleaching, water treatment, and electronics manufacturing is the cornerstone of this market's steady growth trajectory. The expanding global electronics and semiconductor industry, driving consumption of ultra-high-purity electronics-grade hydrogen peroxide, combined with increasingly stringent environmental regulations on chlorine-based bleaching agents in pulp production, rising municipal water disinfection requirements, and growing adoption of hydrogen peroxide as a "green" oxidant in chemical synthesis are collectively broadening the product's end-use penetration across industrial and specialty segments worldwide.

Key Industry Highlights

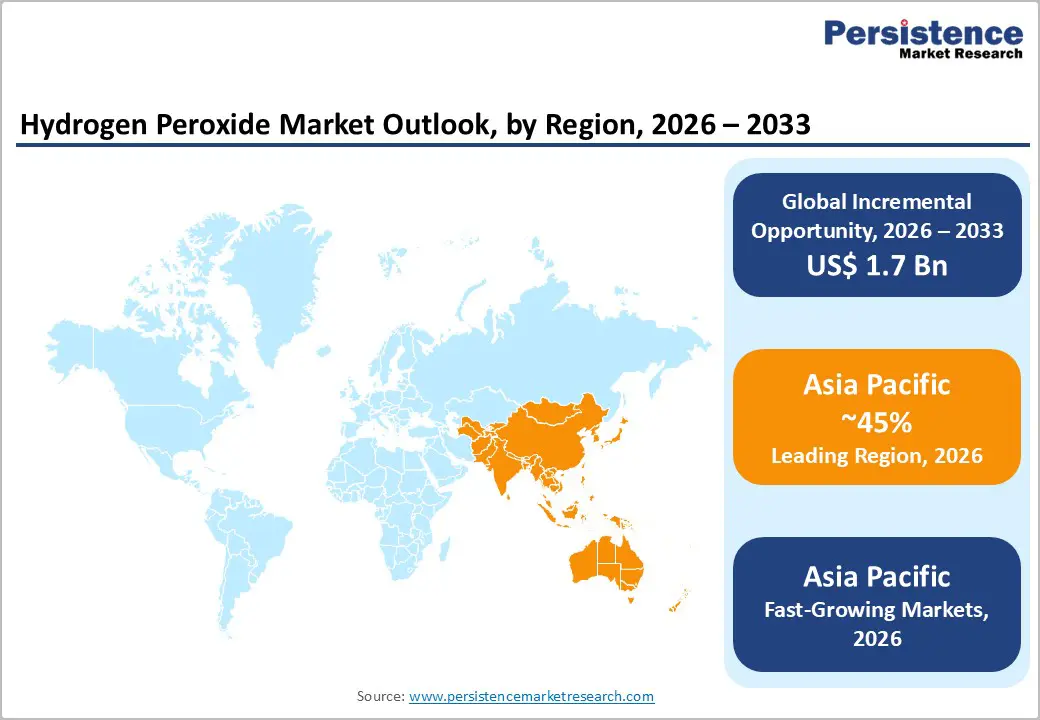

- Leading Region: Asia Pacific leads the global hydrogen peroxide market with approximately 45% share in 2025, driven by China's large-scale pulp, textile, and semiconductor manufacturing sectors, along with India's expanding industrial and water treatment applications.

- Fastest Growing Region: Asia Pacific is also the fastest growing region at approximately 6.8% CAGR (2026–2033), underpinned by India's PLI-backed chemicals expansion, ASEAN wastewater infrastructure investment, and surging electronics-grade demand from Chinese and South Korean semiconductor fabrication facilities.

- Dominant Grade Segment: Industrial Grade hydrogen peroxide dominates the Grade category with approximately 65% market share in 2025, reflecting its essential and large-volume role in pulp bleaching, textile processing, water treatment, and chemical synthesis applications across global manufacturing industries.

- Fastest Growing Application: Electronics Grade hydrogen peroxide is the fastest growing grade segment, driven by massive global semiconductor capacity investment under the U.S. CHIPS Act, EU Chips Act, and equivalent programs in South Korea, Japan, and Taiwan, creating rapidly escalating demand for ultra-high-purity peroxide.

- Key Opportunity: The key market opportunity lies in green chemistry adoption in pulp bleaching and water treatment, driven by the EU Green Deal, EPA discharge regulations, and the shift to TCF/ECF bleaching processes, expected to structurally expand hydrogen peroxide volumes across paper, textile, and municipal water treatment sectors globally through 2033.

| Key Insights | Details |

|---|---|

|

Hydrogen Peroxide Market Size (2026E) |

US$ 3.7 Billion |

|

Market Value Forecast (2033F) |

US$ 5.4 Billion |

|

Projected Growth CAGR (2026–2033) |

5.6% |

|

Historical Market Growth (2020–2025) |

4.7% |

Market Dynamics

Drivers - Rising Demand from Water and Wastewater Treatment Applications

The accelerating global focus on safe drinking water and industrial effluent compliance is emerging as a powerful structural demand driver for hydrogen peroxide. According to the United Nations Environment Programme (UNEP), over 2 billion people globally still lack access to safely managed drinking water services, driving substantial infrastructure investments in water treatment across developing economies. Hydrogen peroxide's role as a chlorine-free, residue-free disinfectant and oxidant for removing organic contaminants, pharmaceutical residues, and biological oxygen demand (BOD) makes it particularly attractive under increasingly stringent effluent discharge norms. The U.S. Environmental Protection Agency (EPA) and the European Union's Urban Wastewater Treatment Directive (2024 revision) are tightening permissible pollutant limits, compelling municipal and industrial water treatment operators to adopt advanced oxidation technologies utilizing hydrogen peroxide, reinforcing sustained demand growth throughout the forecast period.

Expansion of Electronics and Semiconductor Manufacturing

The global semiconductor and electronics manufacturing boom is generating rapidly growing demand for electronics-grade hydrogen peroxide, which functions as a critical cleaning and etching agent in wafer fabrication, printed circuit board (PCB) processing, and flat panel display manufacturing. According to the Semiconductor Industry Association (SIA), global semiconductor sales reached US$ 526.8 billion in 2023, with continued capacity investment driven by the U.S. CHIPS and Science Act (US$ 52.7 billion in domestic semiconductor incentives) and equivalent programs in South Korea, Japan, Taiwan, and the European Union under the EU Chips Act. Electronics-grade hydrogen peroxide must meet ultra-low metal impurity specifications, typically at parts-per-trillion levels, driving premium pricing and attracting significant R&D investment from specialty chemical producers, including Solvay SA, Evonik Industries AG, and Mitsubishi Gas Chemical Company, to expand high-purity capacity globally.

Restraints - Transportation, Storage, and Handling Hazards

Hydrogen peroxide's strong oxidizing properties pose significant logistical and safety challenges, elevating operational costs across the value chain. High-concentration hydrogen peroxide (above 50%) is classified as a Class 5.1 oxidizing substance under the United Nations Globally Harmonized System (GHS), requiring specialized corrosion-resistant containers, temperature-controlled transport, and rigorous site safety protocols. Accidental contamination with organic materials can trigger rapid decomposition or fire. These requirements translate into substantially higher logistics costs relative to alternative bleaching or disinfection chemistries, limiting adoption in price-sensitive markets and creating a persistent barrier for smaller regional producers lacking specialized distribution infrastructure.

Feedstock Price Volatility and Energy Intensity of Production

Hydrogen peroxide is commercially produced via the Anthraquinone Oxidation (AO) process, which is highly energy-intensive and dependent on hydrogen gas, anthraquinone carriers, and organic solvents. Natural gas and electricity prices, principal cost inputs, exhibited extreme volatility between 2021 and 2023, with European natural gas benchmark TTF prices peaking at over €300/MWh in August 2022 according to the European Energy Exchange (EEX). This cost exposure significantly compresses producer margins during energy price spikes and makes long-term contract pricing difficult, restraining capacity expansion decisions and contributing to regional supply-demand imbalances that periodically disrupt downstream industries reliant on hydrogen peroxide supply continuity.

Opportunity - Green Chemistry and Sustainable Bleaching in Pulp & Paper

The global pulp and paper industry's accelerating transition from elemental chlorine and chlorine dioxide bleaching to Elemental Chlorine Free (ECF) and Total Chlorine Free (TCF) processes using hydrogen peroxide represents a multi-decade demand opportunity for market participants. The Food and Agriculture Organization of the United Nations (FAO) reported global paper and board production at approximately 400 million metric tonnes per year, with the shift toward sustainably certified, chlorine-free pulp accelerating under pressure from retail brands and regulatory frameworks, including the EU Green Deal and EU Forest Strategy 2030. Kemira, Nouryon, and Arkema are actively developing integrated hydrogen peroxide bleaching solution packages combining peroxide chemistry with proprietary stabilizers and activation agents, creating higher-margin specialty product opportunities. The paperboard packaging boom driven by e-commerce growth further amplifies virgin and recycled fiber pulp bleaching demand, structurally benefiting hydrogen peroxide producers through the 2033 forecast horizon.

Hydrogen Peroxide as a Propellant and Green Energy Carrier

High-concentration hydrogen peroxide (above 70%) is attracting renewed interest as a monopropellant and bipropellant oxidizer in aerospace and defense applications, as well as an emerging green energy carrier in fuel cell and propulsion research. NASA and the European Space Agency (ESA) have evaluated concentrated hydrogen peroxide for micro-satellite propulsion systems given its non-toxic decomposition products, water and oxygen. Several defense programs in the United Kingdom, Poland, and South Korea are evaluating high-test peroxide (HTP) for torpedo and underwater vehicle propulsion. Additionally, research published in journals including Nature Energy and International Journal of Hydrogen Energy highlights hydrogen peroxide's potential as a liquid oxidant in direct hydrogen peroxide fuel cells (DHPFCs), offering compact, high-power-density configurations for portable and stationary power. These emerging applications constitute a nascent but high-value growth avenue for producers capable of manufacturing hydrogen peroxide with a concentration above 70% at the required purity and consistency specifications.

Category-wise Analysis

Grade Insights

Industrial grade hydrogen peroxide is the dominant product grade, accounting for approximately 65% of total global market volume in 2025. Industrial-grade hydrogen peroxide, typically available at concentrations ranging from 27.5% to 50%, serves the broadest array of end-use industries including pulp and paper bleaching, textile processing, chemical synthesis, and water treatment, all of which collectively represent the largest consumption segments. The grade's dominance is underpinned by decades of established supply chain infrastructure, cost-competitive pricing, and wide producer availability from major manufacturers, including Solvay SA, Nouryon, and BASF SE. While Electronics Grade is the fastest-growing grade owing to semiconductor fabrication demand, industrial-grade volumes far surpass specialty-grade volumes in absolute tonnage, driven by its essential role in large-scale manufacturing and environmental compliance applications globally.

Concentration Insights

The up to 35% concentration segment leads the global hydrogen peroxide market by volume, commanding approximately 43% market share in 2025. This segment's dominance is attributable to its extensive use in routine industrial applications, including general-purpose bleaching in the textile and paper industries, wastewater disinfection, and food-grade sterilization, where lower-concentration formulations satisfy process requirements while offering safer handling logistics and lower transportation cost. The 35%–50% concentration band represents the standard commercial supply specification for the pulp and paper industry and accounts for a further substantial share. Regulatory agencies including the U.S. Department of Transportation (DoT) and the European Chemicals Agency (ECHA) impose progressively stricter requirements for concentrations exceeding 50%, structurally constraining the share of higher-concentration products in routine industrial use.

Application Analysis

Bleaching is the leading application segment for hydrogen peroxide, representing approximately 35% of global market share in 2025. This primacy reflects the product's essential role in the pulp and paper industry's shift to chlorine-free bleaching, as well as its widespread use in textile fiber and fabric whitening. The Food and Agriculture Organization (FAO) and industry bodies such as the Confederation of European Paper Industries (CEPI) document consistent annual pulp bleaching volumes underpinning this segment's structural stability. Hydrogen peroxide bleaching generates only water as a by-product, fulfilling ISO 14001 environmental management requirements and enabling paper mills to meet European Union Industrial Emissions Directive (IED) thresholds. This environmental compatibility advantage over chlorine dioxide or sodium hypochlorite makes hydrogen peroxide the preferred bleaching agent across sustainably certified manufacturing operations, cementing its market leadership in the application category.

Industry Insights

Pulp & Paper is the dominant end-use industry segment, accounting for approximately 31% of the global Hydrogen Peroxide market in 2025. The sector's demand is anchored in the structural, high-volume consumption of hydrogen peroxide for both mechanical pulp bleaching and chemical pulp TCF/ECF bleaching. According to the FAO's Forest Products Annual Market Review, global paper and paperboard production has maintained stable long-run growth, with packaging grades accelerating on the back of e-commerce expansion. Major paper producers, including Suzano S.A., International Paper, and UPM-Kymmene Corporation, operate integrated bleaching facilities requiring a consistent, large-volume hydrogen peroxide supply under long-term supply agreements. The chemical manufacturing and water treatment segments follow as significant consumers, though the pulp and paper industry remains the single largest global source of demand for commodity-grade hydrogen peroxide by volume.

Regional Insights

North America Hydrogen Peroxide Market Trends and Insights

North America represents a mature and technologically advanced hydrogen peroxide market, with the United States as the dominant consumer, driven by robust demand from the pulp and paper, electronics, water treatment, and food processing sectors. The U.S. EPA's National Pollutant Discharge Elimination System (NPDES) regulations and increasingly stringent industrial effluent standards are expanding hydrogen peroxide use in advanced oxidation processes (AOPs) for municipal and industrial wastewater treatment. The U.S. CHIPS and Science Act is simultaneously catalyzing new semiconductor fabrication facility investments, notably by Intel Corporation, TSMC, and Samsung Electronics, which will substantially increase regional electronics-grade hydrogen peroxide consumption through the forecast period.

Canada's extensive kraft pulp and paper production base, anchored in British Columbia, Ontario, and Quebec, constitutes a stable, large-volume demand anchor for industrial-grade hydrogen peroxide. Nouryon and Solvay SA maintain significant North American production capacity supporting the region's pulp sector. Growing food safety regulations administered by the U.S. Food and Drug Administration (FDA) and Health Canada are also driving adoption of food-grade hydrogen peroxide as a GRAS (Generally Recognized as Safe) disinfectant in food contact surface sterilization, adding incremental demand in the food processing segment.

Europe Hydrogen Peroxide Market Trends and Insights

Europe is a technologically sophisticated and regulatory-driven hydrogen peroxide market, where stringent environmental and chemical safety frameworks shape product selection and production practices. The European Union's REACH Regulation (EC No 1907/2006) and Classification, Labelling and Packaging (CLP) Regulation set the compliance baseline for hydrogen peroxide handling and marketing. Germany leads regional consumption, with major producers Evonik Industries AG and Solvay SA operating significant production facilities serving the German pulp, paper, chemical, and textile industries. France and Spain are significant consumers in the textile bleaching sector, with Arkema headquartered in France, maintaining pan-European production and distribution capabilities.

The EU Industrial Emissions Directive (IED) and the EU Green Deal are accelerating the substitution of chlorine-based bleaching and disinfection agents with hydrogen peroxide across the United Kingdom, the Netherlands, and Scandinavia, regions with extensive paper and food processing industries. The European Chemicals Agency (ECHA) has also classified elemental chlorine as a substance of very high concern (SVHC) in some applications, indirectly supporting hydrogen peroxide adoption. Kemira's European operations and Nouryon's specialty hydrogen peroxide portfolio for water treatment applications are well-positioned to capitalize on this ongoing regulatory-driven substitution trend.

Asia Pacific Hydrogen Peroxide Market Trends and Insights

Asia Pacific dominates the global hydrogen peroxide market, accounting for approximately 45% of market share in 2025, and is simultaneously the fastest-growing regional market, projected at a CAGR of approximately 6.8% from 2026 to 2033. China is the epicenter of Asian hydrogen peroxide production and consumption, with dozens of domestic producers supplying a vast network of pulp mills, chemical plants, textile manufacturers, and semiconductor fabs. According to China's Ministry of Industry and Information Technology (MIIT), the country's semiconductor industry has attracted over CNY 300 billion in investment commitments under the "Made in China 2025" strategy, driving exponential growth in the consumption of electronics-grade hydrogen peroxide. Japan's Mitsubishi Gas Chemical Company is among the global leaders in ultra-high-purity electronics-grade peroxide supply to Japanese and Korean semiconductor OEMs.

India is an emerging high-growth market, with the government's Production-Linked Incentive (PLI) Scheme for chemicals and pharmaceuticals and robust expansion of the domestic paper, textile, and water treatment sectors driving demand. Gujarat Alkalies and Chemicals Limited (GACL), Meghmani Finechem Limited, National Peroxide Limited, and Aditya Birla Chemicals form the core of India's domestic production base, with ongoing capacity expansions targeting both domestic consumption and regional export markets. ASEAN nations, particularly Indonesia, Vietnam, and Thailand, are registering rapid consumption growth in pulp bleaching, food processing, sterilization, and industrial wastewater treatment, supported by government investment in sanitation infrastructure and a growing export-oriented manufacturing base.

Competitive Landscape

The global hydrogen peroxide market exhibits a moderately consolidated structure, with a limited number of large multinational chemical producers accounting for a substantial share of global production capacity. These companies operate integrated manufacturing networks and supply hydrogen peroxide to diverse industries, including pulp and paper, water treatment, chemical processing, electronics, and healthcare. Alongside these large producers, several regional manufacturers—particularly in Asia—operate smaller production facilities primarily serving domestic and nearby markets.

Competition in the market is driven by technological capabilities, production efficiency, and the ability to provide reliable supply solutions to large industrial customers. Leading companies focus on improving process efficiency through advanced anthraquinone auto-oxidation (AO) technology and expanding high-purity production for sensitive applications such as electronics and pharmaceuticals. Strategic priorities across the industry include capacity expansion near major end-use industries, development of on-site hydrogen peroxide generation systems for industrial clients, and strengthening long-term supply agreements.

Key Developments:

- February, 2025: Nouryon launched a low-carbon hydrogen peroxide product, becoming the first Nordic supplier to offer reduced-carbon-footprint peroxide. The initiative supports European industries in lowering emissions and advancing more sustainable chemical production and supply chains.

- January, 2025: Evonik Industries announced a joint venture with Fuhua Tongda Chemicals Company to produce and market specialty hydrogen peroxide in Leshan, China, targeting applications in solar panels, semiconductors, and food packaging, with commercial supply expected to begin in 2026.

Companies Covered in Hydrogen Peroxide Market

- Solvay SA

- Evonik Industries AG

- Arkema

- Nouryon

- Mitsubishi Gas Chemical Company

- OCI Company Ltd.

- Kemira

- BASF SE

- Gujarat Alkalies and Chemicals Limited (GACL)

- Meghmani Finechem Limited

- National Peroxide Limited

- Aditya Birla Chemicals

- Barentz

- OCI Limited

- Airedale Group

- Huatai Interchemical (Shandong) Co., Ltd.

- Hansol Chemical Co., Ltd.

- Ube Corporation (formerly Ube Industries)

Frequently Asked Questions

The global Hydrogen Peroxide market is estimated to reach about US$ 3.7 billion in 2026.

Rising demand from water treatment, pulp and paper bleaching, and semiconductor manufacturing drives market growth.

Asia Pacific leads the global market due to strong industrial, textile, and electronics manufacturing activity.

Increasing replacement of chlorine-based chemicals with hydrogen peroxide in industrial and water treatment applications.

Key companies include Solvay SA, Evonik Industries AG, Nouryon, Arkema, BASF SE, Kemira, and Mitsubishi Gas Chemical Company.