- Smart Packaging

- Honeycomb Packing Paper Market

Honeycomb Packing Paper Market Size, Share, and Growth Forecast, 2026 - 2033

Honeycomb Packing Paper Market by Core Type (Continuous Paper Honeycomb, Expanded Paper Honeycomb, Others), Cell Size (10-30 mm, Up to 10 mm, Others), Application, and Regional Analysis for 2026 - 2033

Honeycomb Packing Paper Market Size and Trends Analysis

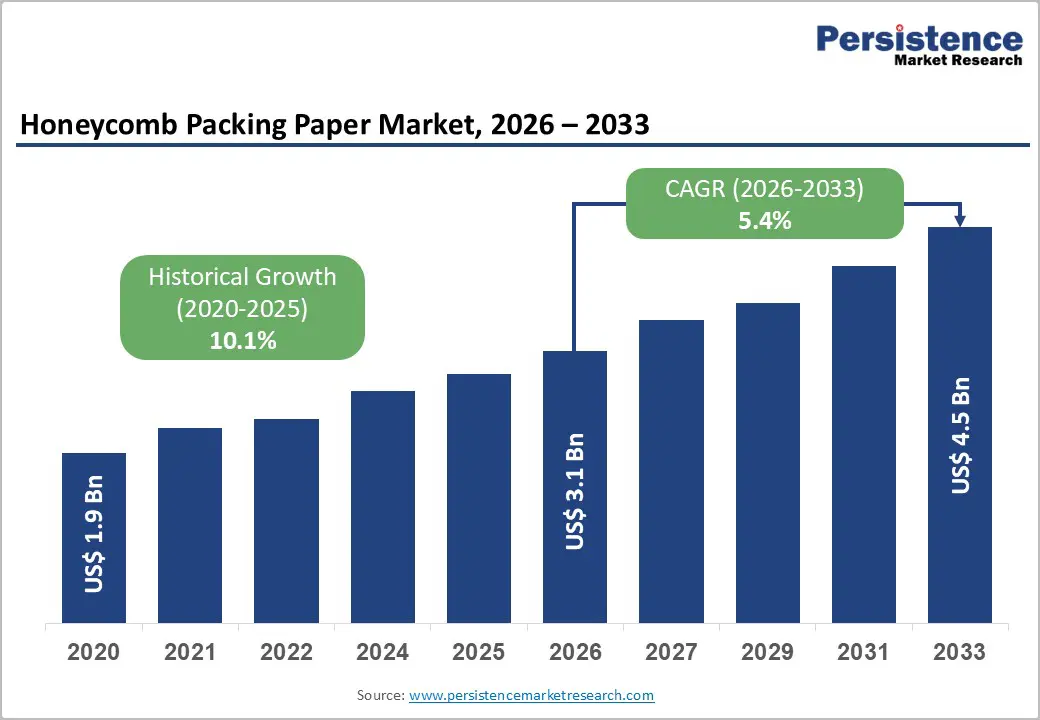

The global honeycomb packing paper market size is likely to be valued at US$ 3.1 billion in 2026 and is expected to reach US$4.5 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by the structural shift toward recyclable protective packaging, expanding global e-commerce logistics, and increasing corporate commitments to replace plastic cushioning materials with fiber-based alternatives.

Honeycomb paper offers high compressive strength, a lightweight structure, and recyclability, making it a viable alternative to foam and plastic packaging in shipping applications. Continuous improvements in automated honeycomb manufacturing technology and rising investments in sustainable packaging solutions are driving market adoption across logistics, furniture, electronics, and industrial packaging.

Key Industry Highlights:

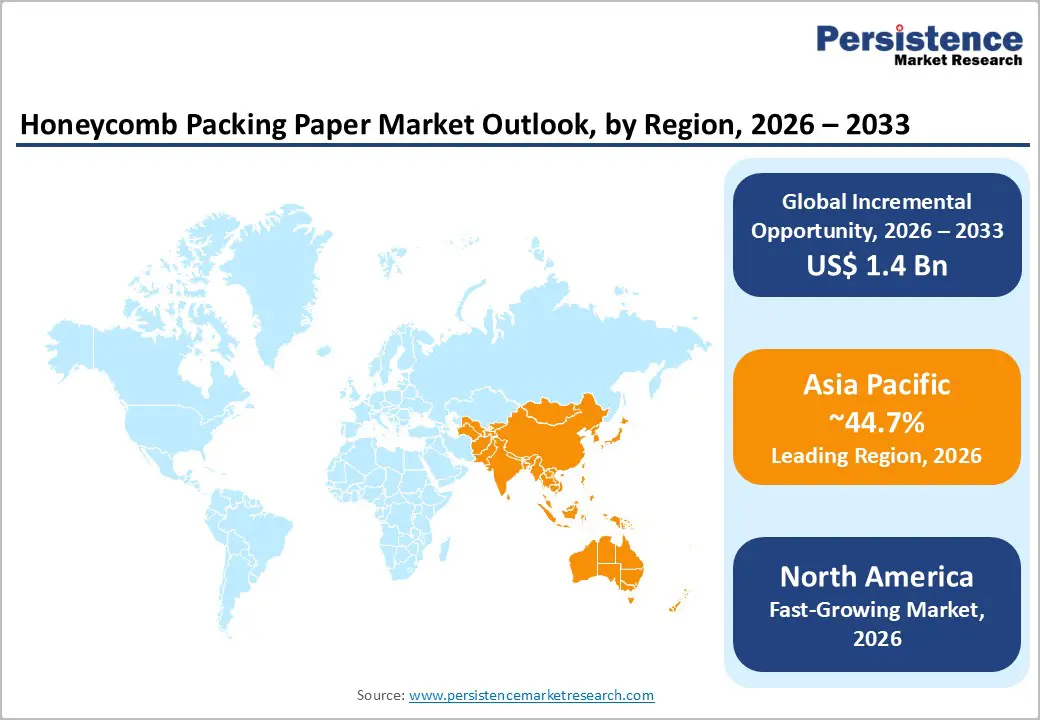

- Leading Region: Asia Pacific dominates the market, accounting for approximately 44.7% of market share, supported by large manufacturing bases in China, Japan, and India, along with strong export activity and expanding e-commerce logistics networks.

- Fastest-growing Region: North America is projected to be the fastest-growing regional market, driven by rising demand for sustainable protective packaging solutions, high parcel shipping volumes from major e-commerce platforms, and increased investments in automated fulfillment and packaging systems.

- Investment Plans: Packaging manufacturers and logistics providers are increasing investments in fiber-based protective packaging technologies, automated packaging lines, and recyclable cushioning materials, particularly in North America and Asia Pacific, to support growing e-commerce shipping volumes and sustainability commitments.

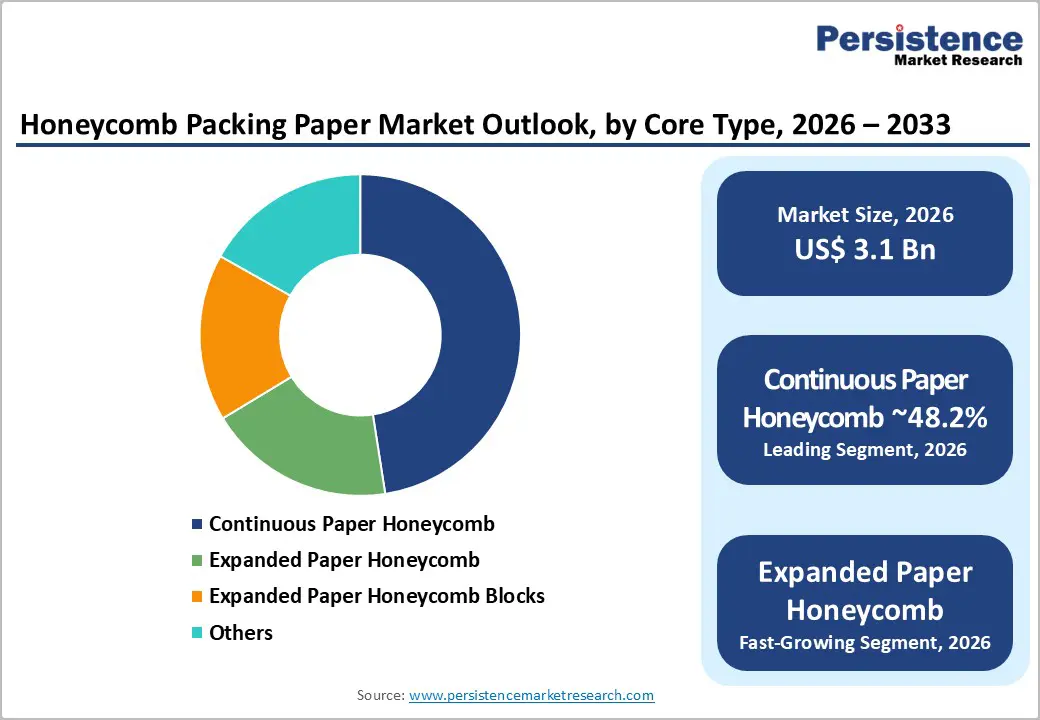

- Dominant Core Type: Continuous paper honeycomb is the leading segment, anticipated to account for around 48.2% of the market share, due to its compatibility with high-speed roll-based production systems and its extensive use in industrial packaging, pallet layers, and protective pads.

- Leading Cell Size: The 10-30 mm cell size segment holds the largest share of approximately 49.5%, as this configuration offers an optimal balance between cushioning strength and material efficiency for applications such as furniture packaging, appliance shipping, and pallet stabilization.

| Key Insights | Details |

|---|---|

| Honeycomb Packing Paper Market Size (2026E) | US$3.1 Bn |

| Market Value Forecast (2033F) | US$4.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Demand for Sustainable and Recyclable Packaging

Governments and corporations worldwide are strengthening commitments to reduce plastic waste and transition toward recyclable packaging materials. Honeycomb packing paper, produced primarily from kraft paper, aligns with circular economy objectives because it is biodegradable, recyclable, and derived from renewable fiber resources. Regulatory frameworks in Europe and North America are increasingly encouraging recyclable packaging formats and restricting single-use plastics. In parallel, multinational retailers and consumer goods manufacturers have announced sustainability targets focused on reducing plastic packaging. As a result, procurement teams are increasingly evaluating fiber-based cushioning materials, such as honeycomb paper, as replacements for plastic foams and bubble wrap. This policy and corporate alignment toward sustainable packaging are driving a structural shift in demand that supports long-term growth in the honeycomb packing paper market.

Expansion of Global E-commerce and Logistics Networks

The rapid expansion of global e-commerce has significantly increased demand for protective packaging solutions that safeguard goods during transportation. Online retail involves multiple logistics stages, including warehousing, shipping, sorting, and last-mile delivery, increasing the risk of product damage during transit. Honeycomb packing paper offers a high strength-to-weight ratio, which enables efficient cushioning while minimizing shipping weight. Lightweight packaging materials help logistics companies reduce transportation costs associated with dimensional weight pricing. The rise of cross-border e-commerce, same-day delivery services, and distributed warehouse networks further increases packaging demand. As parcel volumes continue to grow globally, packaging suppliers are seeing increased demand for protective pads, cushioning inserts, and honeycomb-based packaging components for e-commerce fulfillment operations.

Advancements in Honeycomb Manufacturing Technology

Technological improvements in continuous paper honeycomb production systems, automated cutting machines, and precision die-cutting equipment are significantly improving manufacturing efficiency and product consistency. Modern production lines enable the high-speed manufacturing of honeycomb cores with uniform cell structures and customizable thicknesses. Automation reduces material waste and lowers per-unit production costs, allowing honeycomb packaging to compete more effectively with polymer foam products. These technological advancements also enable manufacturers to develop specialized honeycomb configurations tailored for different industries such as electronics, appliances, and furniture. Improved manufacturing scalability is expanding supply capacity while reducing production costs, supporting wider adoption across global packaging markets.

Barrier Analysis - Volatility in Raw Material Prices

Honeycomb packing paper production relies heavily on kraft paper, linerboard, and recycled paper fiber, making the industry sensitive to fluctuations in pulp and paper prices. Variability in energy costs, supply chain disruptions, and pulp production cycles can significantly impact raw material availability and cost structure. In periods of supply imbalance, kraft paper prices can increase substantially, raising manufacturing costs for honeycomb packaging producers. Higher input costs may reduce profit margins or force suppliers to increase product prices, which could limit adoption among cost-sensitive packaging buyers. This raw material volatility remains a structural challenge affecting profitability and long-term price stability within the honeycomb packing paper industry.

Performance Limitations in High-Moisture Environments

Although honeycomb paper provides strong cushioning, it may exhibit performance limitations in humid environments or under long-term outdoor storage conditions. Moisture exposure can weaken paper fibers and reduce structural integrity, especially in shipping routes involving tropical climates or maritime transport. To address these limitations, manufacturers often apply protective coatings or laminates, which may increase production costs and complicate recyclability. These performance constraints can limit honeycomb adoption in certain heavy-duty packaging applications where plastic foams or composite materials offer superior moisture resistance.

Opportunity Analysis - Adoption by Large E-commerce Fulfillment Centers

Large e-commerce platforms and logistics service providers are increasingly investing in sustainable packaging conversion programs. Fulfillment centers ship millions of parcels daily, making packaging material selection a critical factor in cost management and sustainability initiatives. Honeycomb packing paper can replace foam inserts and plastic cushioning in many packaging applications while maintaining protective performance. Large-scale adoption programs allow companies to standardize packaging formats and optimize automated packing systems. Even partial substitution of plastic cushioning materials across large fulfillment networks could generate significant demand for honeycomb packaging products, creating a substantial growth opportunity for suppliers with high-volume production capacity.

Development of Advanced Honeycomb Composite Materials

Research and development initiatives are enabling the development of enhanced honeycomb structures with improved durability and moisture resistance. Innovations in bio-based adhesives, recyclable barrier coatings, and composite paper layers are expanding the application potential of honeycomb packaging solutions. These advanced materials enable the use of honeycomb structures in industries such as electronics, appliances, and high-value consumer goods, where stronger protective performance is required. The commercialization of high-performance honeycomb composites is expected to expand the addressable market and create new premium product segments within the packaging industry.

Growth in Emerging Manufacturing Economies

Rapid industrialization and export-oriented manufacturing growth in emerging economies are increasing the demand for protective packaging materials. Countries in Asia and Southeast Asia are experiencing rising exports of electronics, furniture, and consumer goods that require safe transportation across global supply chains. Honeycomb packing paper offers a cost-effective and lightweight packaging solution for export shipments. As manufacturing clusters continue expanding in these regions, local packaging converters are increasing investments in honeycomb production capacity, creating opportunities for market growth and regional supply chain development.

Category-wise Analysis

Core Type Analysis

Continuous paper honeycomb is anticipated to represent approximately 48.2% market share in 2026, making it the leading segment within the core type category. They are widely used in industrial packaging operations due to their efficiency in large-scale manufacturing processes. Continuous honeycomb structures are produced using roll-based manufacturing systems, enabling converters to generate long sheets of honeycomb cores that can be cut into protective pads, pallet layers, and cushioning inserts.

The format enables seamless integration with automated packaging lines used by furniture manufacturers, appliance exporters, and large logistics providers. The ability to produce uniform honeycomb structures at high speed improves production efficiency and reduces material waste, thereby strengthening its adoption in high-volume packaging environments. For instance, furniture exporters commonly use continuous honeycomb sheets as pallet interlayers to protect wooden panels during long-distance shipments, while appliance manufacturers integrate honeycomb pads within packaging systems for refrigerators and washing machines. The material’s lightweight nature and recyclability further support its widespread use in export packaging, where weight reduction and sustainability targets are increasingly prioritized.

Expanded paper honeycomb is the fastest-growing segment within the core type category, driven by its versatility and customization capabilities. Expanded honeycomb blocks can be formed into various shapes and thicknesses to meet specific protective packaging requirements. This flexibility makes expanded honeycomb particularly suitable for custom packaging applications involving fragile or irregularly shaped products.

Manufacturers can produce thicker honeycomb panels, structural inserts, or molded supports that provide enhanced cushioning and load-bearing strength. Industries such as furniture, consumer electronics, and industrial machinery increasingly utilize expanded honeycomb blocks to create protective interior packaging solutions. For example, electronics manufacturers often use expanded honeycomb inserts to secure televisions or computer monitors within shipping cartons, while machinery exporters rely on heavy-duty honeycomb blocks to stabilize equipment during international transport. The segment’s rapid growth is driven by increasing demand for customized packaging designs, engineered protective materials, and sustainable alternatives to plastic foam.

Cell Size Insights

The 10-30 mm cell size segment is anticipated to hold approximately 49.5% of the market share in 2026, representing the largest share within the cell size category. This cell size range provides an optimal balance between cushioning strength and material efficiency, making it suitable for a wide variety of packaging applications. Honeycomb structures within this range offer sufficient compressive strength for shipping protection and pallet stabilization while maintaining relatively low material consumption.

As a result, the 10-30 mm cell size is widely used in protective pads, pallet interlayers, and structural packaging components for furniture, appliances, and consumer goods. For instance, furniture manufacturers often use 20 mm honeycomb sheets as internal protective layers to prevent surface damage during transport, while appliance packaging commonly incorporates 25 mm honeycomb pads for shock absorption. Packaging converters favor this configuration because it delivers reliable structural performance across multiple product categories while remaining cost-efficient to manufacture at scale.

The up to 10 mm cell size segment is projected to be the fastest-growing category due to increasing demand for precision packaging applications. Smaller cell structures provide a denser surface area, improving cushioning performance for delicate or high-value products such as electronics, glassware, laboratory instruments, and medical equipment. These compact honeycomb configurations distribute pressure more evenly across product surfaces, reducing the risk of damage during shipping and handling.

As global shipments of consumer electronics, specialty equipment, and premium consumer goods continue to expand, demand for fine-cell honeycomb packaging is expected to rise. For example, smartphone and laptop manufacturers increasingly adopt fine-cell honeycomb inserts to secure devices within packaging while maintaining lightweight shipping structures. Similarly, medical device companies utilize small-cell honeycomb cushioning to protect diagnostic instruments during transportation. Manufacturers capable of producing high-precision honeycomb structures are therefore positioned to capture significant opportunities within this rapidly growing segment.

Regional Insights

North America Honeycomb Packing Paper Market Trends - E-commerce Fulfillment Expansion and Corporate Plastic-Reduction Packaging Initiatives

North America represents one of the most technologically advanced packaging markets globally and is projected to be the fastest-growing region in the honeycomb packing paper market during the forecast period. The U.S. dominates regional demand due to its large e-commerce ecosystem, extensive logistics infrastructure, and strong presence of packaging manufacturers. High parcel shipping volumes from companies such as Amazon, Walmart, and Target Corporation create sustained demand for protective packaging materials that reduce product damage during transit. Large distribution networks supported by logistics providers, including UPS and FedEx, handle billions of parcels annually, which increases the need for lightweight and shock-absorbing packaging solutions such as honeycomb paper cushioning. Corporate sustainability initiatives are a major growth driver in the region. Many large retailers and consumer goods companies have introduced commitments to reduce plastic packaging and improve recyclability across supply chains. For example, Amazon has implemented its Frustration-Free Packaging and plastic reduction programs that encourage suppliers to shift toward recyclable paper-based materials for protective packaging. Similarly, Apple Inc. has expanded its use of fiber-based packaging for electronics shipments as part of its strategy to eliminate plastic from its packaging. These initiatives encourage the adoption of paper-based protective packaging formats, including honeycomb paper cushioning, across large distribution networks.

Packaging manufacturers across North America are also expanding their honeycomb production capabilities. Companies such as Packaging Corporation of America and WestRock Company have increased investments in paper-based protective packaging technologies that support recyclable cushioning materials for industrial and e-commerce packaging. In parallel, specialized packaging providers, including Sealed Air Corporation and Pregis, are developing fiber-based cushioning systems that replace plastic foam packaging in fulfillment operations. Investment activity in North America includes packaging innovation programs, automation upgrades in fulfillment centers, and partnerships between packaging suppliers and logistics providers. The expansion of automated packaging lines in large fulfillment facilities has increased demand for standardized honeycomb pads and protective inserts that can be integrated into automated packing processes. These developments strengthen the region’s position as a key market for sustainable protective packaging innovation, supporting continued adoption of honeycomb packing paper across logistics, retail distribution, and manufacturing supply chains.

Europe Honeycomb Packing Paper Market Trends - Circular Economy Regulations and Industrial Export Packaging Demand

Europe represents a mature and policy-driven market for sustainable packaging materials. Countries such as Germany, the U.K., France, and Spain are leading adopters of honeycomb packaging due to strong environmental regulations and advanced recycling infrastructure. European industries, including automotive manufacturing, furniture production, and consumer goods exports, require durable protective packaging solutions that comply with strict sustainability requirements. Large industrial exporters such as IKEA increasingly utilize paper-based protective materials in furniture shipments to replace plastic foam and reduce packaging waste. European regulatory frameworks emphasize recycling, waste reduction, and circular economy principles. Policies developed by the European Commission under the Circular Economy Action Plan and the evolving Packaging and Packaging Waste Regulation encourage companies to replace plastic packaging materials with recyclable alternatives. Honeycomb packing paper aligns well with this regulatory environment because it can be produced using recycled fiber and processed through existing paper recycling systems. Countries such as Germany have highly efficient paper recovery systems supported by organizations such as the European Paper Recycling Council, enabling large-scale recycling of paper-based packaging materials.

Industrial demand is another important growth driver. Europe hosts large furniture manufacturing clusters and electronics exporters that rely on protective packaging for international shipments. Honeycomb packaging provides lightweight yet strong cushioning for these products, reducing shipping costs while ensuring product safety. Automotive component manufacturers across Germany and France frequently use honeycomb pads as pallet separators and interior protective layers when shipping sensitive parts across supply chains. Packaging manufacturers across Europe are investing in advanced honeycomb production technology and developing new materials with improved durability and moisture resistance. Companies such as Smurfit Kappa Group and DS Smith have introduced fiber-based protective packaging systems that incorporate honeycomb structures designed for recyclable cushioning applications. For instance, DS Smith has expanded its plastic-replacement packaging portfolio across Europe to support retailers transitioning to fiber-based protective packaging. Continued regulatory pressure combined with corporate sustainability commitments is expected to support steady market growth in Europe.

Asia Pacific Honeycomb Packing Paper Market Trends - Manufacturing Expansion and E-commerce Logistics Growth

Asia Pacific is projected to represent the largest regional market, accounting for approximately 44.7% of the market share in 2026. The region’s dominance is supported by its extensive manufacturing base, high export volumes, and rapidly expanding e-commerce sector. Countries such as China, Japan, and India play critical roles in regional market development by combining large manufacturing industries with growing logistics networks. China serves as a major production hub for honeycomb packaging materials due to its large paper manufacturing industry and strong export-oriented manufacturing sector. Chinese manufacturers supply honeycomb packaging for electronics, furniture, and industrial equipment exported worldwide. The expansion of Chinese e-commerce platforms such as Alibaba Group and JD.com has significantly increased demand for protective packaging materials used in parcel shipments. Government initiatives supporting sustainable packaging and waste reduction have also encouraged manufacturers to adopt recyclable paper-based packaging alternatives.

Japan focuses on high-precision honeycomb packaging solutions for advanced electronics and industrial applications. Electronics manufacturers, including Sony Group Corporation and Panasonic Holdings Corporation, require protective packaging materials that prevent vibration and shock during international transport of sensitive electronic products. Japanese packaging companies have therefore developed high-precision honeycomb structures with smaller cell sizes to meet the strict protection requirements of electronics and optical equipment. India represents a rapidly expanding market driven by growth in e-commerce logistics, manufacturing exports, and domestic consumer goods production. Online retail platforms such as Flipkart and Amazon India process millions of shipments daily, creating increasing demand for recyclable protective packaging materials. At the same time, government initiatives supporting manufacturing expansion, such as Make in India, have stimulated exports of electronics, appliances, and furniture that require protective packaging during transport. Packaging companies across the Asia Pacific are investing in honeycomb converting equipment and expanding paper recycling capacity to support sustainable packaging materials. Regional packaging leaders such as Nine Dragons Paper Holdings have increased production of recycled paperboard used in honeycomb packaging structures. The combination of manufacturing growth, rising online retail activity, and increasing adoption of recyclable packaging materials positions Asia Pacific as the most significant market for honeycomb packing paper over the forecast period.

Competitive Landscape

The global honeycomb packing paper market is moderately fragmented, consisting of global packaging companies and numerous regional converters specializing in paper honeycomb production. Large packaging corporations typically integrate honeycomb solutions within broader paper packaging portfolios, while smaller manufacturers focus on specialized protective packaging applications. Competitive differentiation is based on manufacturing capacity, product customization capabilities, and supply chain efficiency. As sustainability regulations and demand for recyclable packaging increase, consolidation activity among packaging converters is gradually rising, particularly in North America and Europe.

Market leaders focus on innovation in sustainable packaging materials, production automation, and geographic expansion. Companies differentiate themselves through recyclable material technologies, customized packaging solutions, and integrated logistics partnerships. Strategic collaborations with e-commerce retailers and manufacturing exporters are emerging as key growth strategies.

Key Industry Developments:

- In February 2025, International Paper announced a strategic combination with DS Smith PLC to create a global leader in sustainable fiber-based packaging solutions. The development strengthens innovation capacity in paper-based protective packaging, including honeycomb structures used in logistics and industrial shipments.

Companies Covered in Honeycomb Packing Paper Market

- DS Smith PLC

- Smurfit Kappa Group

- Mondi plc

- Stora Enso Oyj

- Cascades Inc.

- Eltete TPM Ltd.

- Dufaylite Developments Ltd.

- Axxor B.V.

- Grigeo AB

- Hexacomb Corporation

- Packaging Corporation of America

- WestRock Company

- International Paper Company

- Georgia-Pacific LLC

- Sonoco Products Company

- Rengo Co., Ltd.

- Nine Dragons Paper Holdings Limited

- Shanying International Holdings Co., Ltd.

Frequently Asked Questions

The global honeycomb packing paper market is estimated to reach US$3.1 billion in 2026.

The honeycomb packing paper market is projected to reach US$4.5 billion by 2033.

Key trends include the rapid transition toward sustainable fiber-based packaging materials, expansion of e-commerce logistics networks, rising adoption of automated packaging systems using standardized honeycomb pads, and increasing product innovation in moisture-resistant and high-strength honeycomb structures.

The continuous paper honeycomb core type segment is the leading category in the market, anticipated to account for around 48.2% of market share, as it supports high-volume production and integrates efficiently with automated packaging operations.

The honeycomb packing paper market is expected to grow at a CAGR of 5.4% between 2026 and 2033.

Some of the major companies include DS Smith PLC, Smurfit Kappa Group, Mondi plc, Stora Enso Oyj, and Cascades Inc.